jetcityimage

Wayfair (NYSE:W) is a popular eCommerce company that focuses on the “home goods” category. This includes items such as sofas, tables, chairs, and decor. Wayfair benefited massively from the surge in e-commerce adoption during the lockdown of 2022. Customers had no choice but to shop online, with traditional retail stores being shut down. Since that point, the company has reported declining active customers, whilst its customer loyalty is growing. In addition, the company beat both top and bottom-line financial estimates for the third quarter of 2022. In this post I’m going to break down its business model, financials, and valuation, let’s dive in.

Tailored Business Model

Traditional e-commerce companies struggle with selling large furniture items due to logistical challenges and returns. For example, if you order a sofa and it doesn’t fit, then you will want to return it immediately. For this reason, home furniture is suited to brick-and-mortar retail stores, and customers can see the product, try it out etc. However, as almost everything has accelerated online now, furniture has also followed.

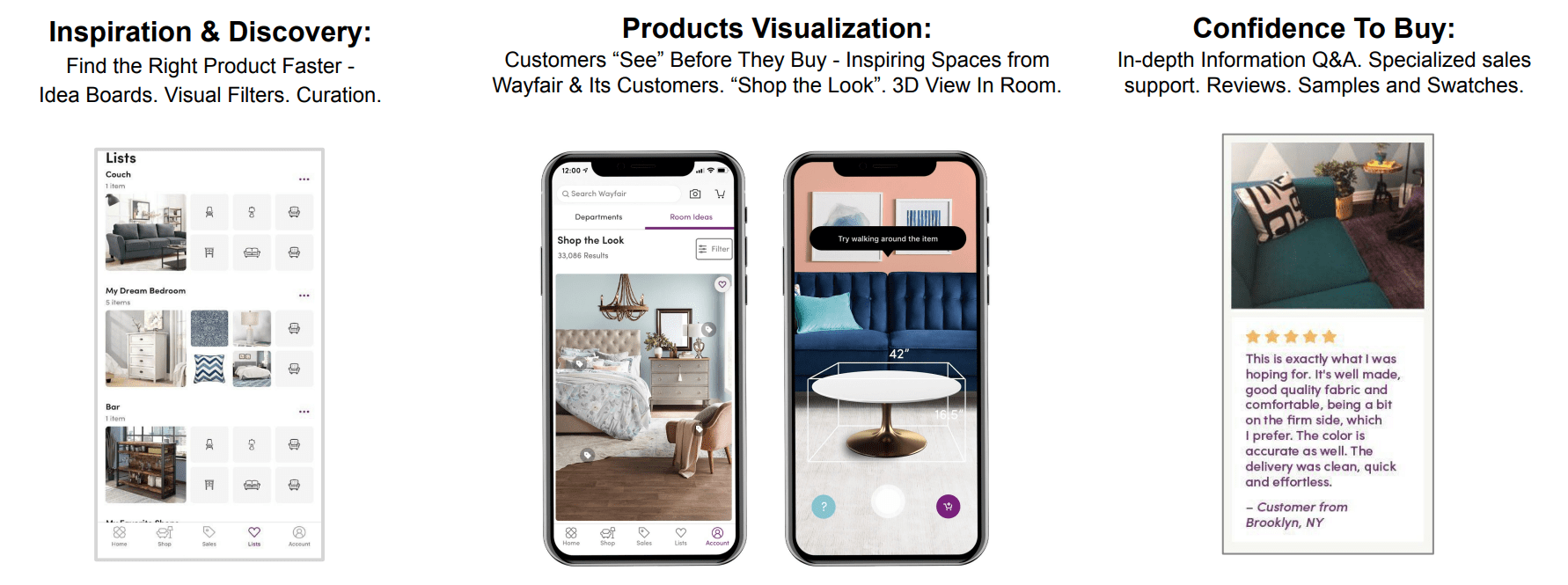

Wayfair is purpose-built for the home goods market they have a few advantages over other companies. Firstly, the company offers a bespoke and tailored user experience that assists customers in buying furniture. For example, the product offers “idea boards”, visual filters, and even an Augmented Reality [AR] powered 3D viewer for a room. The AR solution is particularly useful as I mentioned prior, a big issue with furniture is checking it fits and “visualizing” it in the space. Wayfair also offers specialist support and its review section has created a community feel to the platform, making it feel less mechanical than Amazon.

Product overview (Q2,22 report)

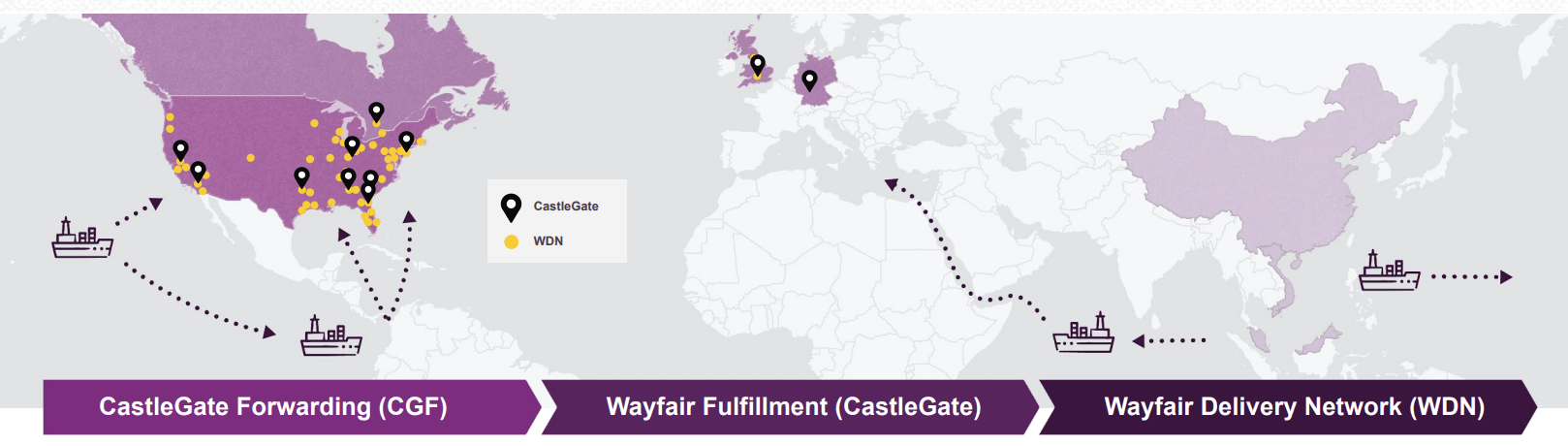

Wayfair has built out a network of over 23,000 suppliers with a “proprietary” logistics network called “CastleGate”. As Wayfair effectively “owns” the supply chain, the company has better control over shipping times for customers and can use its scale to improve unit economics. Suppliers benefit from “freight forwarding” and “fulfillment”, via its footprint of 16 fulfillment centers. In 2021, over 80,000 TEUs (ten-tonne equivalent unit containers) were carried. This surprisingly made the company a “top 20” importer by U.S. volume. Its small parcels can reach 95% of the U.S. population in two days or less, which makes them close to Amazon’s high standard.

CastleGate Logistics (Q3,22 report)

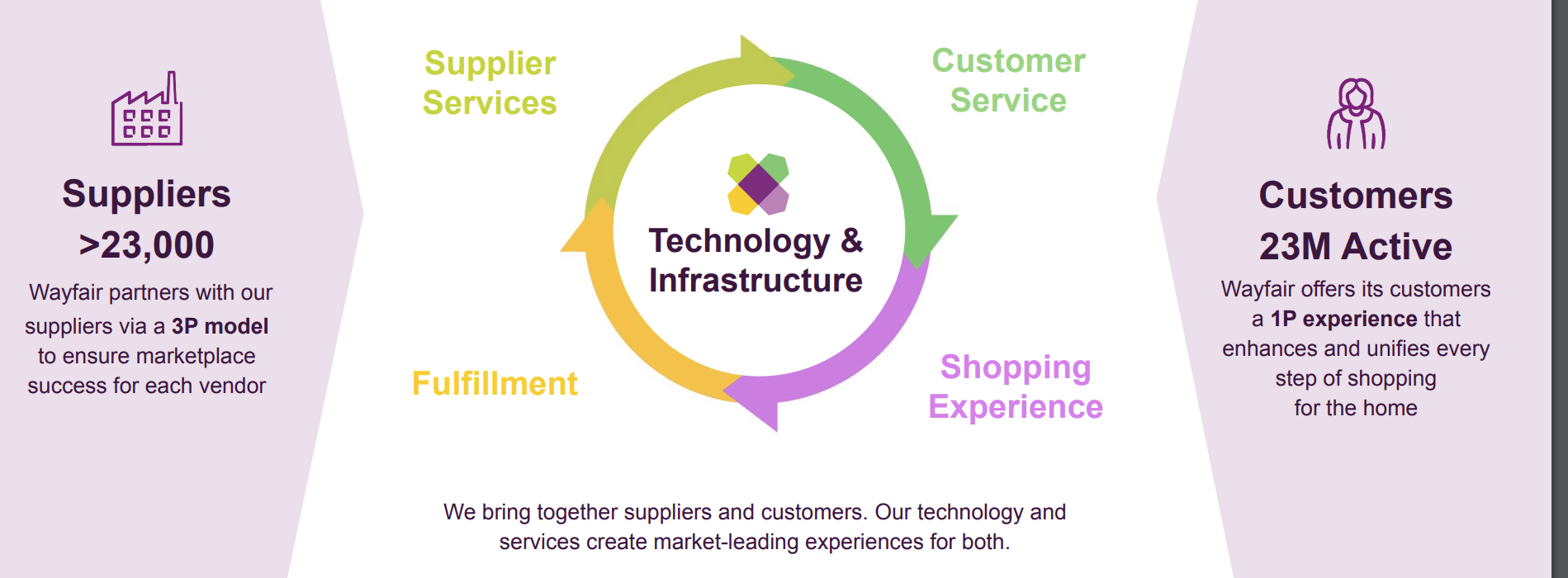

Wayfair has also focused on providing its customers with an “exceptional” customer experience. This is more important when selling large items as often they require a hands-on approach to delivery and extra information (dimensions etc). To accomplish its service goals, Wayfair employs an in-house customer service team of over 4,900 people in the U.S. and Europe. The team is motivated via an NPS (Net Promoter score), incentivized compensation structure, which is great to see.

Wayfair business Model (Q3,22 report)

Financial Review

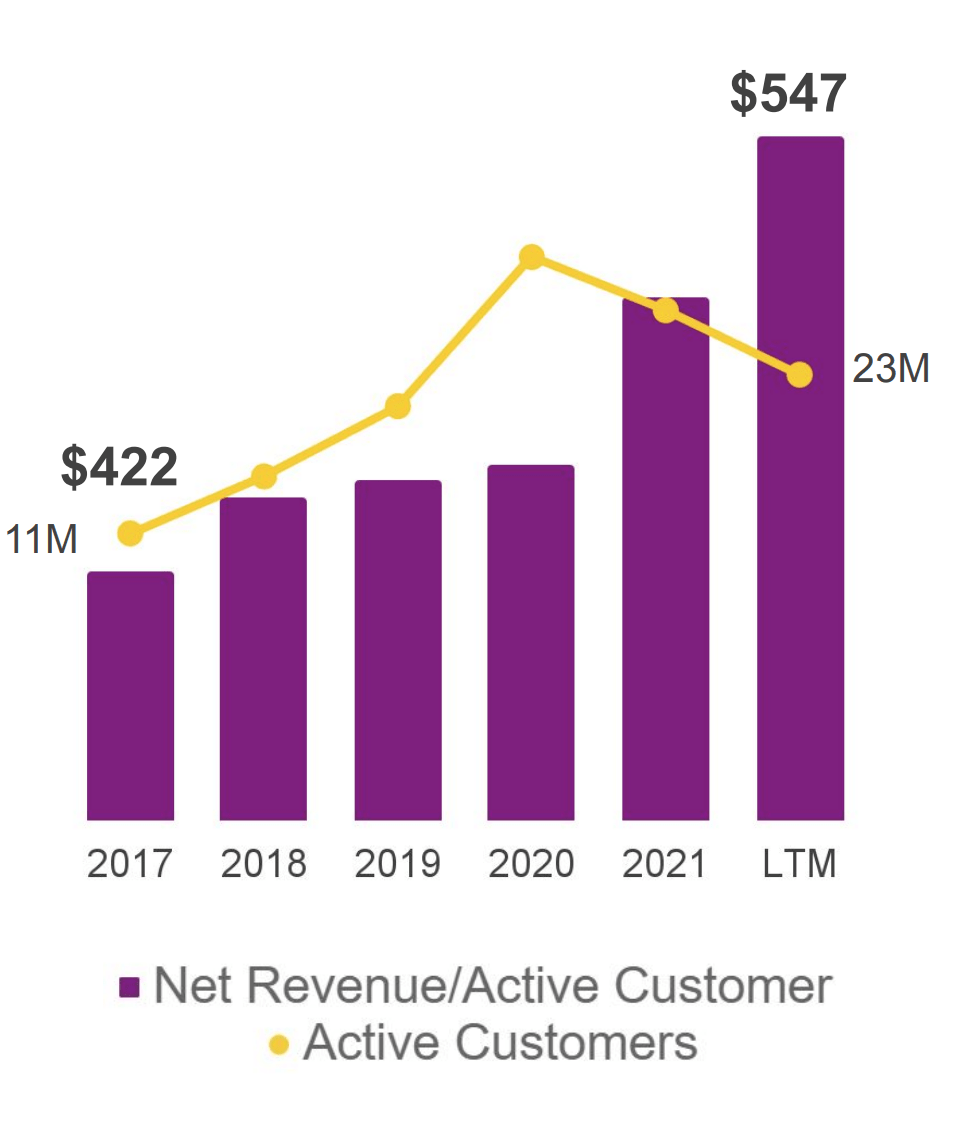

Wayfair reported mixed financial results for the third quarter of 2022. Revenue was $2.8 billion, which declined by 9% year over year, but still beat analyst expectations by $30.31 million. Management blamed a “weakening” macroeconomic environment, which exacerbated the expected “flat” sequential revenue between the second and third quarters. The U.S. is still Wayfair’s strongest market, while Europe was impacted by geopolitical uncertainty and macroeconomic headwinds. A positive for Wayfair is its net revenue per active customer in the trailing 12 months has increased by 29.6% since 2017 and was up versus 2021 to $547. Its number of active customers has declined from its peak in 2020, (as expected) but is still a solid 23 million. This metric is over double the 11 million in 2017 and slightly higher than pre-pandemic levels.

Revenue per customer (Q3,22 report)

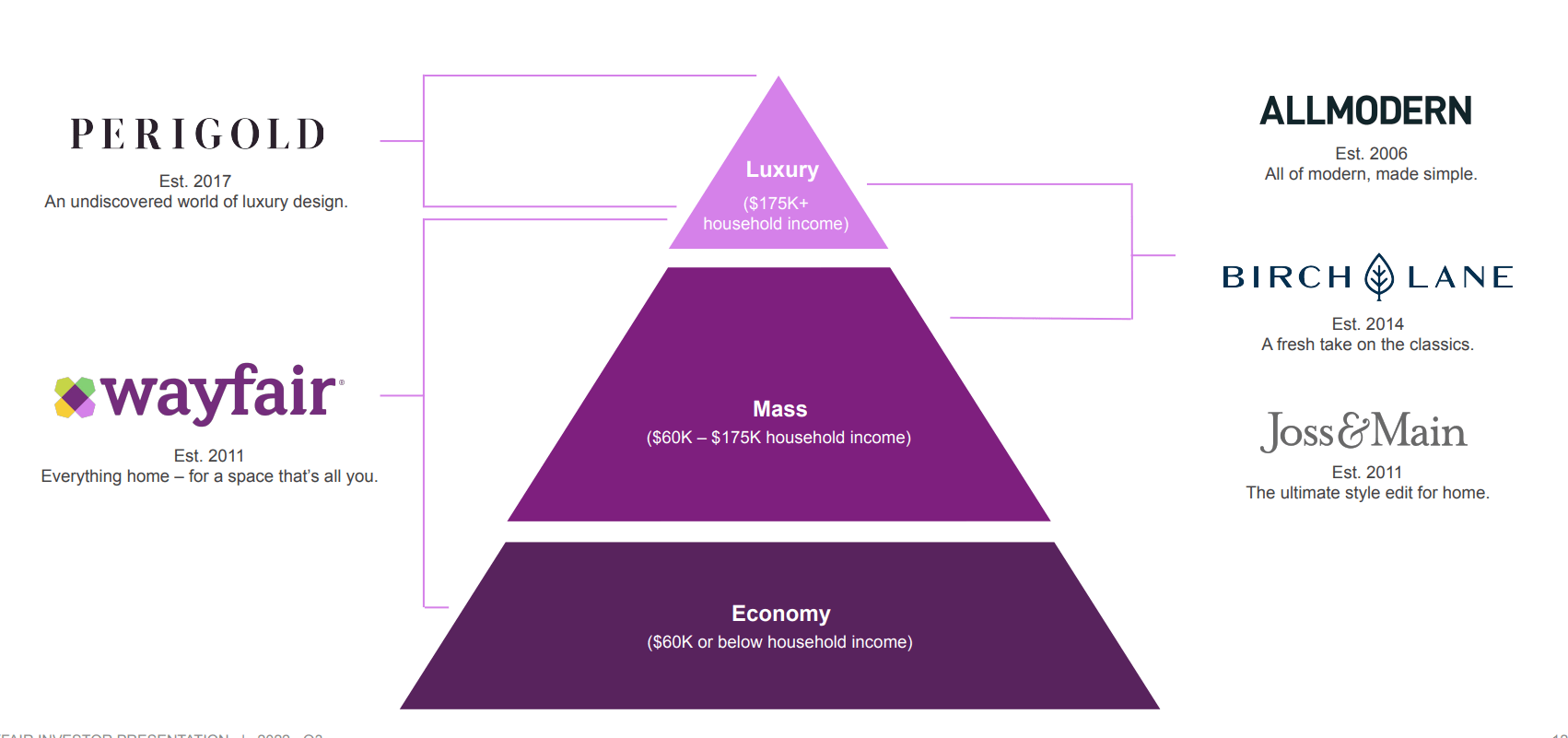

Wayfair has also continued to build out its brands on the platform, with 124 in total. This gives customers a range of choices across various price points. Wayfair sits primarily in the mass market segment, which targets households between $60k and $175k in income.

Wayfair brands (Q3,22 report)

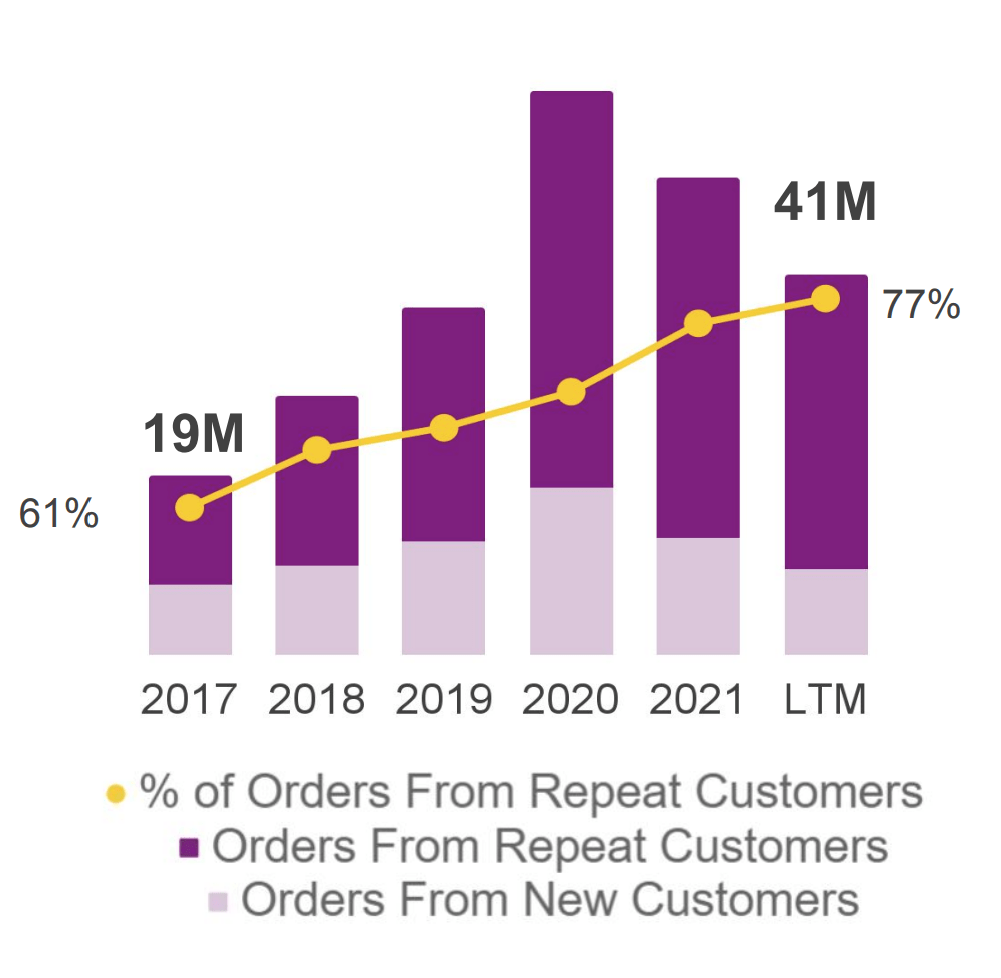

Its range of brands, combined with optimizing of analytics and great service has helped Wayfair boost its customer loyalty. Its number of customers with over 3 lifetime purchases has increased 30% in 2015, to 63% by the end of 2021. In addition, the company has boosted its percentage of orders from repeat customers to 77% of the total in the TTM, up from 61% in 2017. This metric is also higher than the previous years, despite its customer base declining from the “pandemic peak” in 2020. I imagine its number of repeat orders will continue to increase, as customers break the initial psychological barrier towards ordering furniture online. Longer term this should result in lower customer acquisition costs and improve margins. The reason for this is the company won’t have to keep paying for advertising to win back its prior customers.

Orders from repeat customers (Q3,22 report)

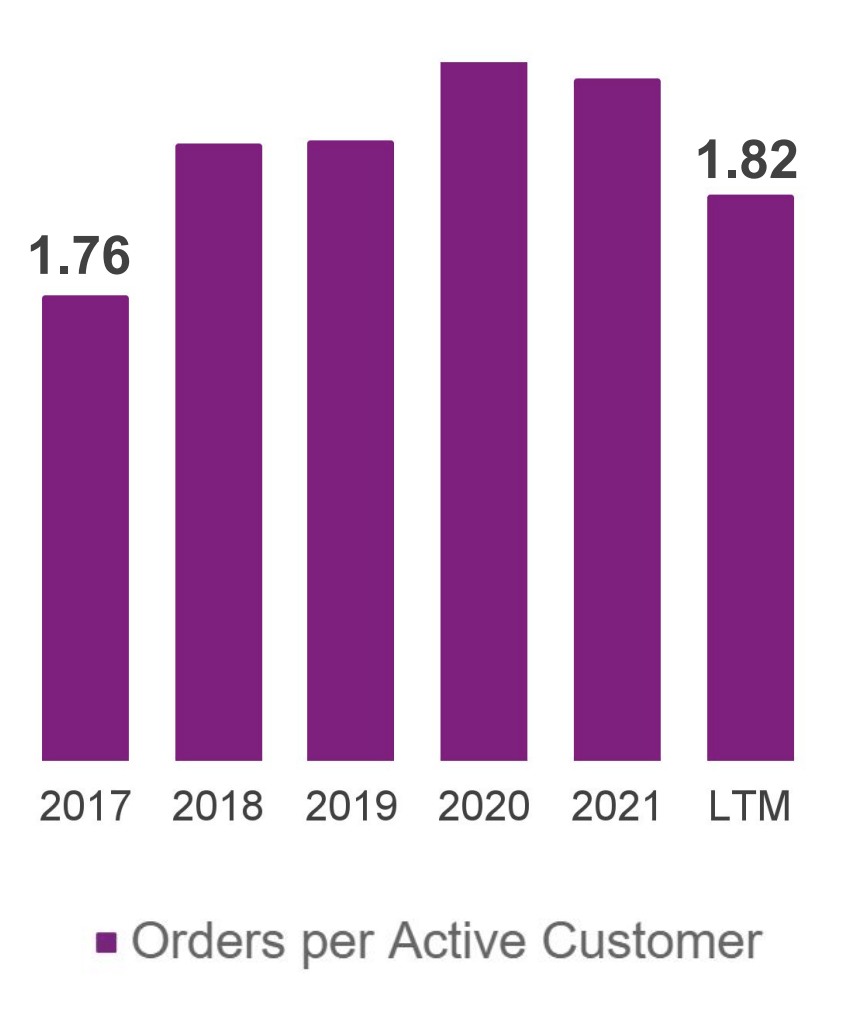

Wayfair has also boosted its number of orders per customer from 1.76 in 2017, to 1.82 in the last 12 months. This is slightly lower than pre-pandemic levels, which I believe is driven by macroeconomic factors.

Orders per customer (Q3,22 report)

Moving onto profitability, Wayfair’s gross margin has improved to 29.1%, which was higher than management’s guided range of between 27% and 28%. This was also higher than the trailing 12-month average of 27.6%. This was driven by increased adoption of its CastleGate logistics solution and improvement in the overall supply chain.

The company reported earnings per share [EPS] of negative $2.66, which was down substantially year over year, but still beat analyst estimates by $0.71. Customer service and merchant fees made up 5.2% of revenue and was just above management’s guidance. However, G&A expenses were $543 million, which came in just below guidance. Over time I would like to see, the company improving its margins and reducing its operating losses substantially. Management alluded to some cost “savings” in Q4 but it is unclear how substantial these would be. Wayfair operates an inventory light model, with its value making up just 0.8% of net revenue. This is a strong positive as it means the company can quickly adapt to changing supply and demand characteristics. Wayfair also has a solid balance sheet with $1.3 billion in cash and short term investments. The company does have fairly high debt of $4 billion, but the majority of this $3.1 billion is long-term debt, and thus manageable. In addition, manageable plans to “chip away” at its debt levels to give the company greater flexibility long term.

Margins and Cash (Q3,22 report)

In the fourth quarter of 2022, management is forecasting strong results driven by the holiday shopping season. In addition, the company expects a net working capital benefit from improved operating leverage.

Advanced Valuation

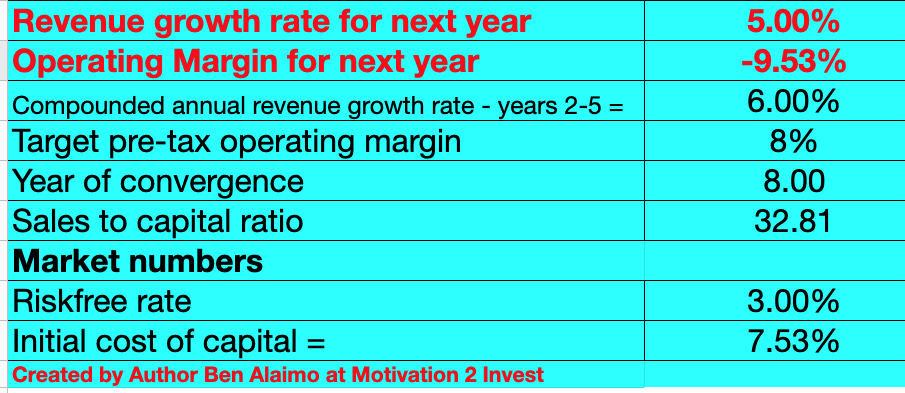

In order to value Wayfair, I have plugged its latest financials into my discounted cash flow valuation model. I have forecast 5% revenue growth for next year, which I forecast to be impacted by a tough macroeconomic environment. However, in years 2 to 5, I have forecast 6% revenue growth per year.

Wayfair stock valuation 1 (created by author Ben at Motivation 2 Invest))

I have forecast Wayfair to increase its operating margin to 8% over the next 8 years, as the company scales and benefits from cost structure improvements. In addition, its increasing customer loyalty will likely drive higher margins due to the aforementioned reasons regarding lower customer acquisition costs.

Wayfair stock valuation 2 (created by author Ben at Motivation 2 invest)

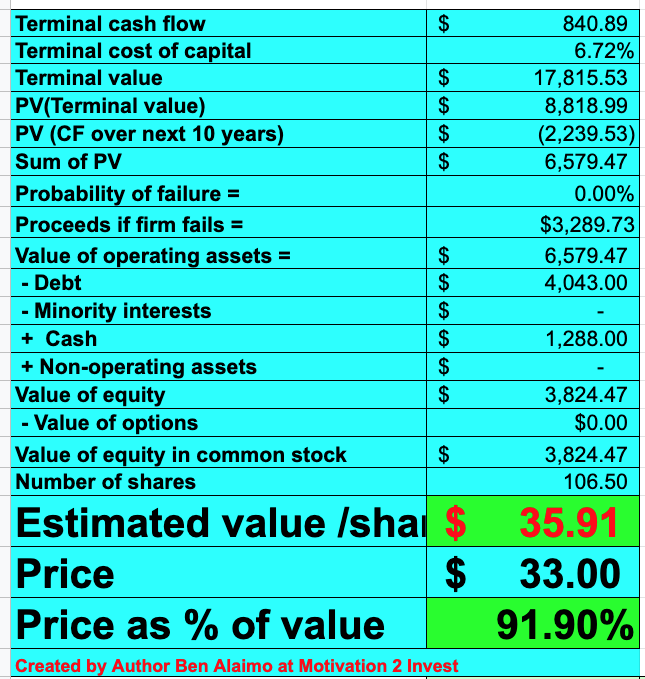

Given these factors I get a fair value of $35.91 per share, the stock is trading at $33 per share and thus it is ~7% undervalued.

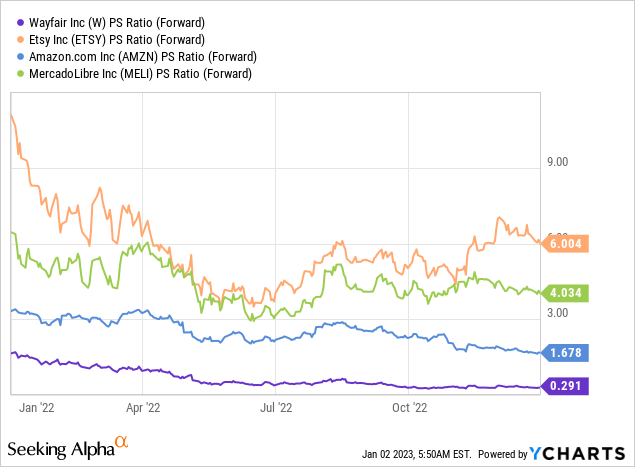

The company also trades at a Price to sales ratio = 0.28, which is 81% cheaper than its 5-year average. Relative to other e-commerce companies, such as Amazon and Etsy, Wayfair is the cheapest.

Risks

Recession/Ecommerce headwinds

Many analysts are forecasting a recession, due to the high inflation and rising interest rate environment. This will likely cause a tepid macroeconomic environment, driven by lower consumer demand. The e-commerce industry as a whole is also facing a series of challenges as margins are getting squeezed. Even the king of e-commerce Amazon, has seen its stock price plummet by 54% from its all-time highs.

Final Thoughts

Wayfair is a great e-commerce company that has found its niche in the home goods and furniture market. The company has built up a loyal customer base and an extensive supply chain network. Given its stock is undervalued currently, I would be tempted to give it a buy rating. However, given the macroeconomic environment and the unfavorable headwinds against e-commerce stocks as a whole, I believe a “hold” rating is more appropriate. I believe there are better opportunities to deploy capital in the market currently, see my post on Amazon for details.

Be the first to comment