hapabapa

Company description

Wayfair (NYSE:W) is a global e-commerce business which specializes in furniture, décor, housewares, and home improvement products. Wayfair offers millions of products through its supplier network, operating asset-light although does utilize the use of warehouses.

E-commerce has had a tough year in 2022. EMQQ, an E-commerce ETF, is down 63% from its ATH. One of the main reasons for this is COVID-19. Many western countries chose to provide income support (such as furlough payments), but lockdowns meant there was little to spend money on beyond necessities. For this reason, people flocked to e-commerce businesses, be it clothing, gaming or furniture.

Businesses like Wayfair were perfectly placed to benefit from this increased traffic, with a superior website, strong supply chain and many delivery options. Furniture businesses performed abnormally well due to an unexpected boom in many housing markets. In the UK, this was due to a Stamp duty (tax levied when selling a property) holiday. This could only last so long however, those who wanted to move house did and those who wanted to make home improvements had.

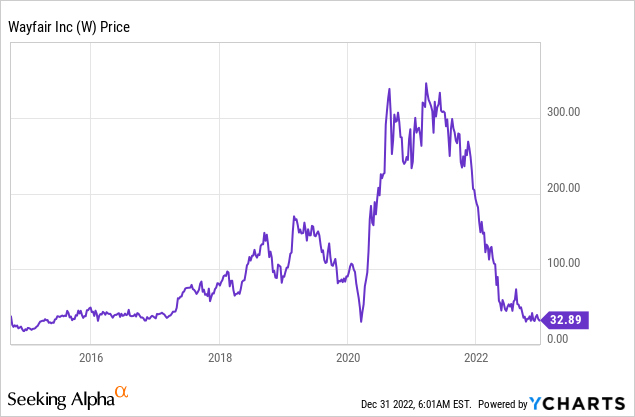

This leads us to where we are now, sales began to fall, and markets have transitioned from bullish to bearish. Wayfair is down 90% from its ATH and the general feelings towards the business is negative.

The objective of this paper is to assess the quality of the business going forward through an assessment of the current macro conditions and the financial position of the business. The stock being down 90% does not necessarily mean it is under or fairly valued, a stock can certainly continue to fall double digits.

Economic consideration:

Equity markets have deteriorated across 2022 as a result of changes in the macro economy. Money printing, record low interest rates and the Russian invasion of Ukraine contributed to inflation of >5% across many countries. Interest rates have been increased to respond to this, causing a squeeze to people’s finances on two fronts. Inflation is deteriorating the value of their money and higher interest rates are increasing their cost of borrowing.

The home improvements industry has been heavily impacted by this, as when discretionary spending declines, consumers focus on high priority spending.

Going forward, things look to be continuing in this vein. Many consider a recession to be inevitable as monthly GDP growth is slowing in many countries.

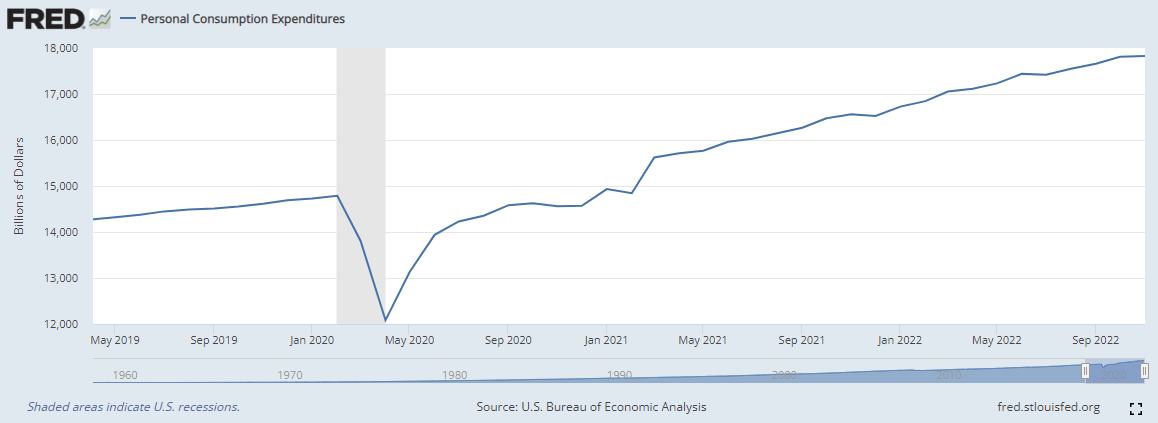

Further, consumer spending looks to be plateauing and could fall as early as January 2023, assuming a spike in December due to Christmas. This is generally seen as a lagging indicator which could suggest we will see declining growth in December 2022.

Personal Consumption (FRED)

Home improvement spending is relatively elastic and so continued falling demand will disproportionately impact furniture retailers.

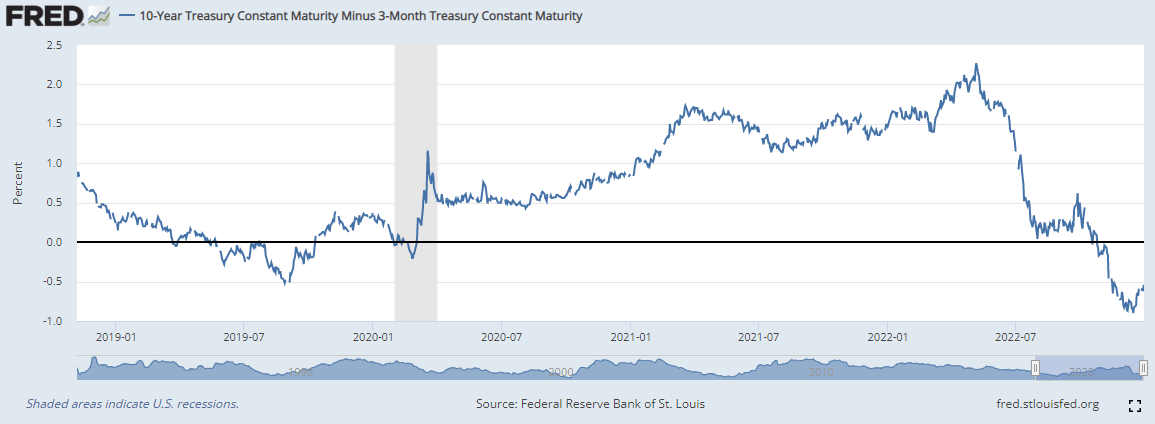

Finally, for those who value the yield curve as a leading indicator, the 10Y / 3M curve has inverted for the first time since 2020, and at a level deeper than 2008.

10Y / 3M yield curve (FRED)

For these reasons, Wayfair will likely see noticeable headwinds coming from a global economic decline. Sales have already fallen as a result of slowing growth in 2021/2022 and so it is reasonable to assume this will continue in 2022 and 2023.

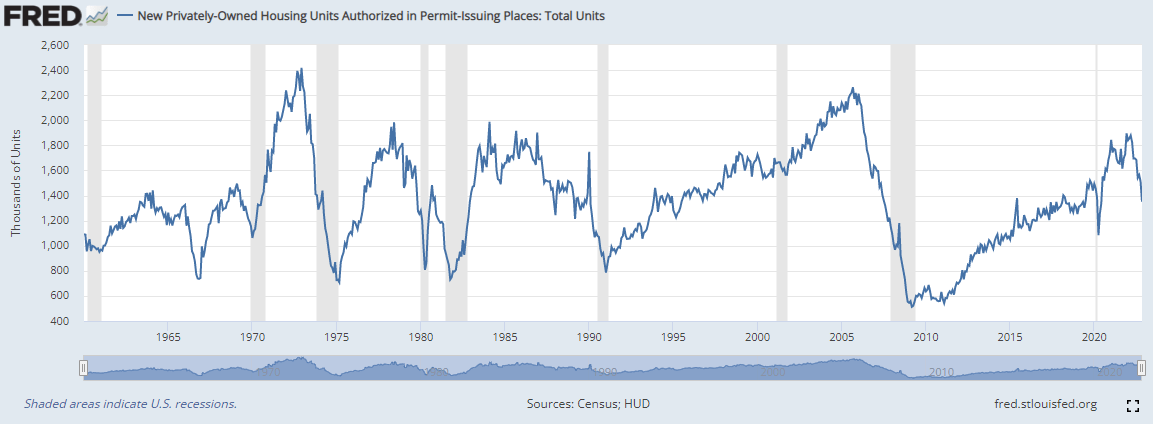

Housing market:

The home improvement industry is very much tied to the housing market. More activity in the housing market contributes to greater demand in the home improvement industry as new properties are furnished.

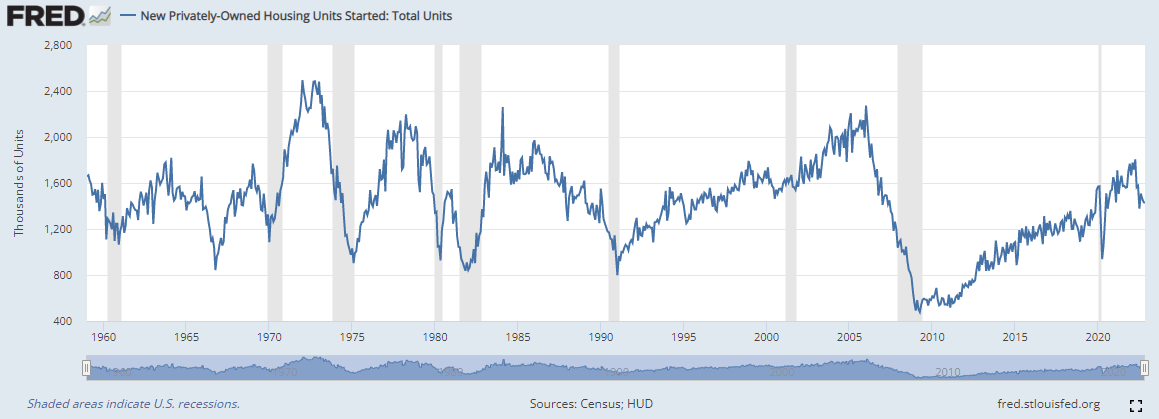

What we observe is a noticeable decline in both units beginning construction and permits issued for construction. There are many reasons for this, but a leading factor is the belief that the desired level of profits cannot be achieved. This can only be because property businesses believe demand and / or prices will fall.

Privately-owed housing units started (FRED) Privately-owned housing units permit authorized (FRED)

This again is headwinds for Wayfair as demand will likely fall, the onus is on Wayfair to improve its competitiveness in order to grow. The problem with this is that Wayfair has had an online competitive advantage for many years, yet has still struggled to grow post-COVID.

Financials:

Wayfair – Financial analysis (Tikr Terminal)

Despite declining sales following the COVID-19 boom, Wayfair has grown revenue at a CAGR of 24%. This has been as a result of aggressive marketing and innovation in the home improvements business. Historically, one would have to visit multiple stores, organize transportation and was generally a very time-consuming process, especially if items needed returning. Wayfair’s selling point is that you can easily shop from thousands of suppliers and easily return items if they are unwanted. This is a great selling-point for Wayfair and is only increasing in prevalence following COVID. Research has found growth in e-commerce v. brick-and-mortar sales is significant, as consumers seek flexibility and ease of purchase.

This is the only bright spot of the P&L, however. From a GPM perspective, we observe very little in the way of scale economies, as margins have improved only 2% in over 5 years. COGS includes product costs and shipping. Given that volume has increased we would expect that product costs fall overtime, with Wayfair leveraging its scale to obtain better prices / share of sale. It could be that increased shipping costs have offset this but regardless, this is an underperformance.

Furthermore, the most concerning line in the whole of Wayfair’s financials is Operating expenses. The largest component of this is Advertising and selling expenses. This line has grown at a rate in excess of revenue and when taken alongside COGS, results in a loss-making business. This means that Wayfair, and its shareholders by extension, are net paying customers in order to receive their businesses. Now this is not an alien concept and certainly occurs for many e-commerce businesses, but our concern lies in the fact that the company achieved profitability in 2021 and has reverted to 2019 levels following a fall in demand. This suggests no operational improvements in several years and may decline further into 2023.

Moving onto the balance sheet, the companies cash cycle is well maintained, with a slight uptick in cash received days suggesting more credit purchases are occurring. The very good inventory turnover is a characteristic of an asset-light e-commerce business and must be maintained, Wayfair does not want to transition into holding much stock.

From a credit perspective, we see how these losses have been financed. Debt has increased substantially (alongside share issuance) and net debt has drifted higher and higher. An investor in this business will have to appreciate that they will need to actively fund the business in order to realize future alpha. With the company burning over $1bn in the LTM period, we would expect either debt or equity to be raised in FY23 in order to shore up Wayfair’s balance sheet. Wayfair’s most expensive loan currently has an effective interest rate of 3.6% (Raised in September 2022), although most of these instruments have conversion options (the lowest being $63).

Overall, Wayfair’s financials are extremely messy. The company has the classic hallmarks of a growing e-commerce business but lacks the substance to show a route to profitability. They lack any real scale economies and have significantly weakened their balance sheet, which will impact delivering their targets going forward.

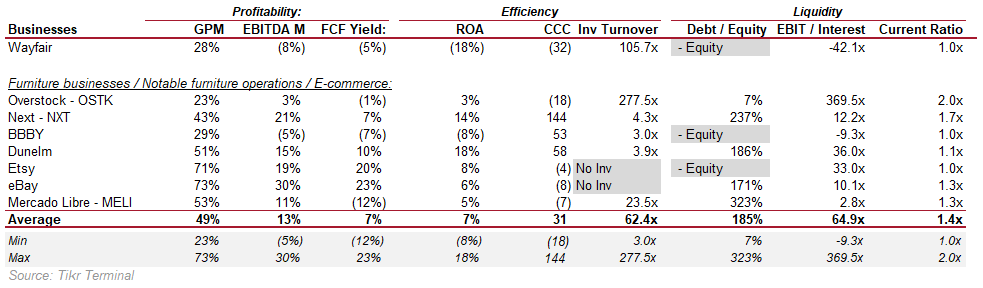

Peer comparison:

There are not many directly comparable businesses to Wayfair, which is one of the reasons they have grown as quickly as they have. A prospective investor can consider e-commerce businesses or furniture retailers as alternatives.

Peer comparison (Tikr Terminal)

What we observe is that both the retailers and e-commerce businesses outperform Wayfair, both on the top and bottom line. It’s clear that the attractiveness of investing in Wayfair is derived from their ability to grow revenue and the subsequent souring is due to a lack of translation into profits.

If investors are looking for home improvements exposure, an investor would be better off looking at Overstock (OSTK) or Etsy (ETSY).

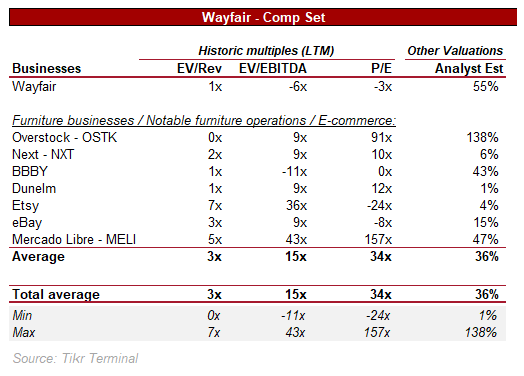

Valuation:

Wayfair remains too expensive relative to its peers. Given the low quality of its revenue, we think even a 1x value is too high.

Peer group valuation (Tikr Terminal)

Analysts suggest an upside of 55%, believing Wayfair will be EBITDA positive in 2024 and net income positive in 2025. Given that 2023 will likely be another down year for the reasons stated in this paper, we cannot see how Wayfair will turn profitable the year after. Importantly, we cannot see how Wayfair will become cost efficient to the extent that Opex can fall without reducing revenue equally.

Conclusion:

Wayfair has used e-commerce to revolutionize an archaic industry, similar to Amazon (AMZN) with books. The difference however is Amazon’s transition to profitability and its reinvestment in its other services. Wayfair have not yet been able to crack this, struggling to transition into profitability.

It is certainly too early to give up on the business, brand value and traffic are extremely valuable. Building a $12BN revenue business shows the competency of Management and the focus should now be on cost management.

Despite their share price falling 90%, it is still too expensive in our view. Investors can find significant value elsewhere and should only consider Wayfair when either profitability is within sight, or the value of revenue is more appropriate. We thus rate the stock a sell.

Be the first to comment