Pgiam/iStock via Getty Images

Washington Trust Bancorp (NASDAQ:WASH) is the largest regional bank headquartered in the state of Rhode Island. The bank has a long history, as it has been in business since 1800. It has paid a dividend for more than a century.

As you might expect given that pedigree, Washington Trust is a conservatively run bank. The firm remained profitable, for example, during the 2008 Financial Crisis and was able to gain market share from other larger banks that stumbled during that period.

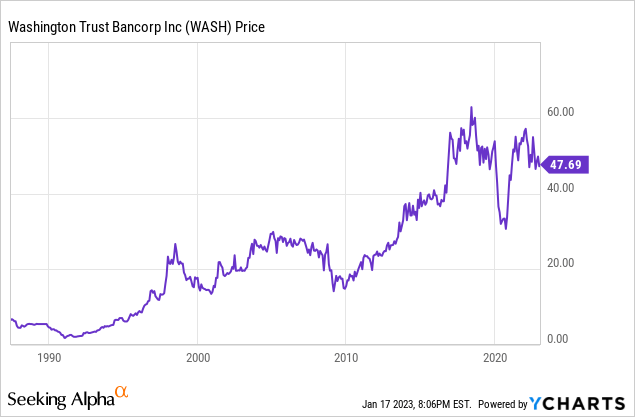

The bank has been a tremendous performer over the long-haul, with shares rising from the low single digits in the 1990s to $48 now:

This chart doesn’t even include the firm’s generous dividends, as shares often yield 3.5% or more in any given year. The bank is also notable for avoiding steep drawdowns, with shares holding up well even during major banking downturns such as 2008-9.

However, the stock has been an underperformer in recent years. Shares peaked at $60 prior to the pandemic and have largely traded sideways since then. And, zooming in a bit, shares are near 52-week lows today even with the recent rally in the overall market.

So, has something gone wrong with the business model, or is this a great buying opportunity?

Earnings Down Slightly, But With Good Reason

For the bank’s Q3 ’22 results, we saw earnings per share fall to $1.08 from $1.14 from the same period of 2021. While this is hardly a massive drop, investors are never fond of declines in earnings.

However, not all earnings declines are equal. In Washington Trust’s case, earnings are down because the company is investing in opening new branches. Here’s CEO Edward Handy on the latest conference call:

“We remain committed to our customers and expanding our presence within our geographic footprint. During the quarter, we opened a new commercial lending office in New Haven, Connecticut, opened a new full-service branch in Cumberland, Rhode Island and recently announced our intention to open three new branches in Rhode Island in 2023.”

With banking in particular, it takes some time for a new branch to pay off. You have to pay out for employees, rent, and all the other overhead associated with a new location. However, branches pay for themselves by gathering deposits from people that live nearby so they can be lent out. This deposit-gathering process typically takes a few years as people become familiar with your bank and brand.

A new bank branch, by default, is usually going to lose money for the first couple of years until it collects enough deposits and retail activity to make up for the added overhead. However, I’d argue that this expansion makes sense, particularly in an environment where interest rates are higher, which increases the value of a strong deposit base. Washington Trust is sacrificing some profits in 2022 and 2023 with these new branches, but it will significantly add to the bank’s profitability over a longer-term time horizon.

It’s also interesting in that the trend across the industry has been to consolidate branches and reduce footprints. Banks have put less value on deposits and retail banking given the low interest rate environment that had prevailed until recently. This gives banks taking a contrarian approach, such as Washington Trust, the opportunity to pick up some market share and lower its funding costs compared to peer banks.

WASH Stock: A Compelling Dividend Growth Story

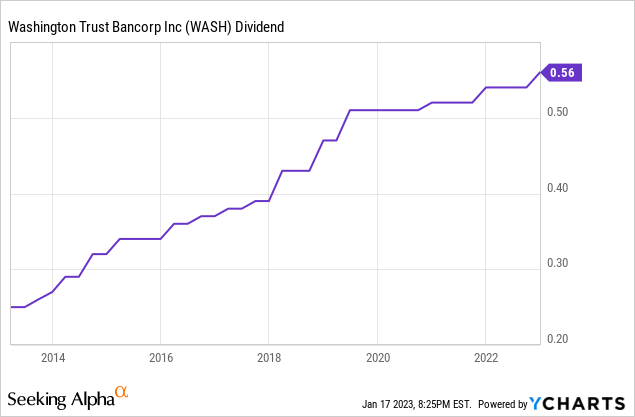

Washington Trust has been an excellent dividend growth story. The dividend has slightly more than doubled over the past ten years:

Of note, the company often raises its dividend more than once per year. Aside from a brief pause during Covid-19, Washington Trust has unceasingly increased its dividend payout. That streak continued in 2022, with the company bumping the quarterly dividend from 54 cents to 56 per cents last month.

The interesting thing now is that Washington Trust has hiked its dividend from around 40 cents to 56 cents per quarter since 2018 while the share price has been essentially flat. If you increase your dividend that much without seeing the share price rise, that leads to a much higher dividend yield.

And, indeed, that’s what we see, as the dividend yield is now up to 4.7%. Aside from a brief period during Covid-19, this is the highest yield that WASH stock has offered. Traditionally, its yield has been closer to 3.5% or 4% instead of the current more generous figure.

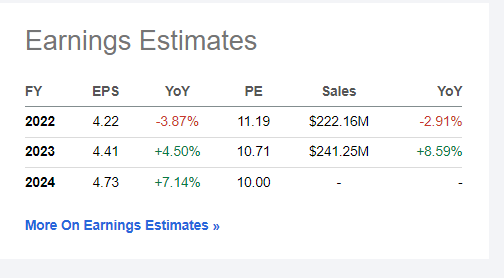

An observant reader might wonder if Washington Trust is seeing its payout ratio get stretched given the steady dividend increases. However, there’s nothing to worry about there, earnings easily cover the dividend. Here’s the analyst forecast for Washington Trust’s earnings going forward:

Washington Trust earnings forecast (Seeking Alpha)

As you can see, the company’s $2.24 of annual dividends is not an issue, given that Washington Trust earns more than $4/share in annual profits.

And, despite the weak share price in 2022, earnings have been fine. Even with the expansion efforts under way, Washington Trust will merely see a low single-digits decline in earnings for 2022.

Analysts project the firm returning to growth in 2023 and 2024. I’d also point out Washington Trust has a significant wealth management division, and the down market was a drag on fee revenue for 2022. Whenever markets turn back up, that should provide another tailwind for the firm’s earnings as well.

WASH Stock Verdict

Washington Trust Bancorp is a fairly sleepy investment, even by regional banking industry standards. It’s been in business for more than two centuries and has the low-risk business model that you’d expect with such a durable franchise. The share price is rarely volatile, and both earnings and the dividend tend to increase at a steady measured rate.

Washington Trust will almost never dazzle investors with particularly outsized returns over any brief period of time. However, Washington Trust has managed to grow its loan book, earnings, and dividend all by around 7% annually, give or take a point or two, for an extended period of time.

You can make strong total returns owning a stock at a starting 11x P/E ratio with a 4.7% dividend yield that grows at 7%/year.

WASH stock won’t be an overnight home run, but over time, its economic engine should continue to grind out market-beating returns for its loyal shareholders. And, in a volatile market like this one, a low-risk 4.7% dividend yield with frequent increases is quite appreciated as well.

Be the first to comment