Klaus Vedfelt/DigitalVision via Getty Images

Rating Downgrade

We are downgrading our rating of Warby Parker (NYSE:WRBY) from “HOLD” to “SELL”. Our initial coverage of the stock was on September 20, 2022, and we cited “no catalysts to boost the stock price higher” such as slowing growth and exposure to macroeconomic headwinds. The Q3 earnings have reaffirmed this sentiment, and we believe that the stock has limited upside and has major downsides as macroeconomic risks endure.

Deceleration in Key Metrics

Management reported a revenue growth of 8% on a YoY basis from $137.4 million to $148.8 million. This a 75% deceleration from the 32% YoY growth seen in Q3 2021. The number of active customers also grew from 2.15 million to 2.26 million in Q3 2022, which represent a 5% growth on a YoY basis. That metric too is also much smaller compared to 22.2% growth seen in Q3 2021. Finally, we are also interested in the average revenue per customer, as this metric would indicate amount of customer demand and the willingness to pay for these products. The company reported $258 in average revenue per customer this year, which is only a 6.6% growth from the previous year. Given that in Q3 2021, the company saw 13.6% growth in this metric, we believe that we are starting to see the company starting to reach its optimal revenue per user. Furthermore, contextually, the 6.6% growth in this metric is close to the 6.5% inflation that the economy saw in 2022, which would make its real revenue growth close to flat on a year-over-year basis.

Economic Risks and Profitability

Management also reported a -$23.8 million net loss in in Q3 2022. The company’s cash and cash equivalents stood at $197.9 million at the end of the quarter. Warby Parker has a wide exposure to the U.S. consumer segment as it predominantly operates in the sale of fashion items, such as sunglasses. As mentioned in our coverage article, it is logical to see growth and profitability be affected if the U.S. were to enter a steep consumer-led recession as determined by lower consumption and higher unemployment rate. Recent data suggests that consumer spending is cooling, and we have yet to see the bulk of the interest rate hikes impact the economy. The continued losses and the uncertainty in a path to profitability make us concerned about the company’s ability to navigate through uncertain economic territory.

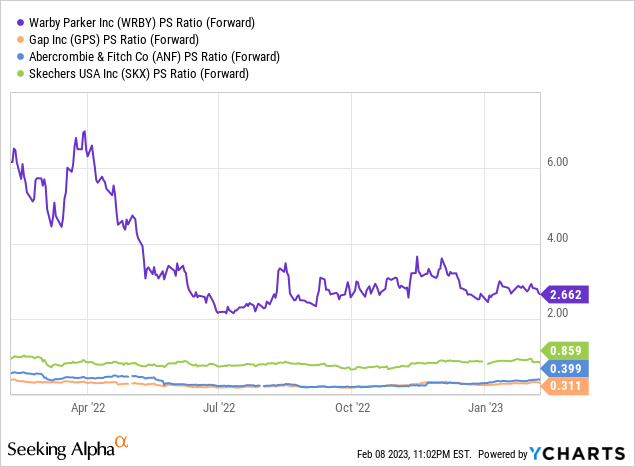

Valuation

Warby Parker in unprofitable and its valuation metrics have D-level rating based on Seeking Alpha’s valuation metrics comparing the company to the sector median. We also believe that the company’s valuation is elevated and not reflective of market conditions and the risks of further economic deterioration. As seen below, though Warby Parker’s P/S ratio is far below its highs of early 2022, the P/S ratio is magnitudes higher than other fashion companies such as Gap Inc (GPS), Abercrombie & Fitch Co (ANF), and Skechers USA (SKX). Though Warby Parker sees higher growth than these comparable companies, the exercise below demonstrates the need for outsized growth compared to peers to justify its P/S valuation metrics. Given the fast deceleration in growth levels and uncertainty in the economy, we believe the Warby Parker has major downside risks if growth were to stall or see financial decline.

Conclusion

We are downgrading our rating of Warby Parker as a result of continued affirmation of our concerns in the initial coverage. The company continues to post decelerating metrics and post net losses though it is unlikely we have not seen the brunt of the economic impacts arising from higher interest rates. Valuation also remains elevated despite the risks, and we believe that there are other investments in the segments that would be better than Warby Parker due to its increased downside potential in the foreseeable future.

Be the first to comment