Justin Sullivan

Walgreens Boots Alliance, Inc. (NASDAQ:WBA) operates as an integrated healthcare, pharmacy, and retailer in the United States (U.S.), the United Kingdom, Germany, and internationally.

In December 2022, we published an article on Seeking Alpha, titled: “We Like Walgreens Boots Alliance’s Dividends”. Back then, we had been analysing WBA’s valuation based on its dividends, using the Gordon Growth Model. At the time of our writing, the company’s stock price had been around $39/per share, falling within our estimated range of fair values of $26 to $45 per share, depending on how aggressive/conservative dividend growth rate we have assumed.

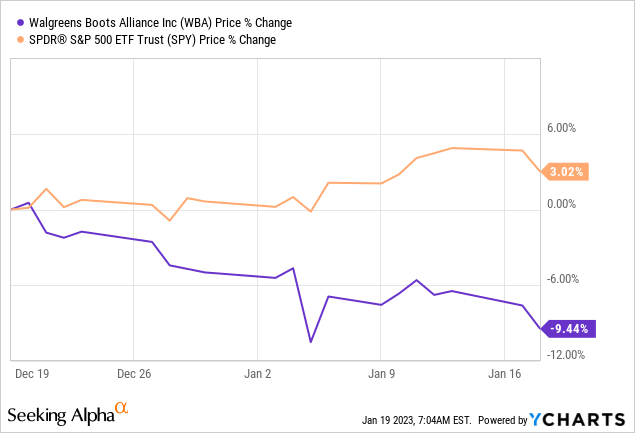

Since our writing, WBA’s stock price has declined by more than 9%, while the broader market has gained about 3% in the same period. Early January, when the firm published its fiscal Q1 2023 financial results, the stock price saw another sharp drop.

In today’s article, we will be discussing whether the previously established “buy” rating is still intact, or we should be selling the stock because of the latest financial results. As our previous valuation and rating have been based on the firm’s dividend and dividend growth, we will be primarily focusing on how the latest financial results may impact the dividend and its growth.

Will the dividend remain sustainable?

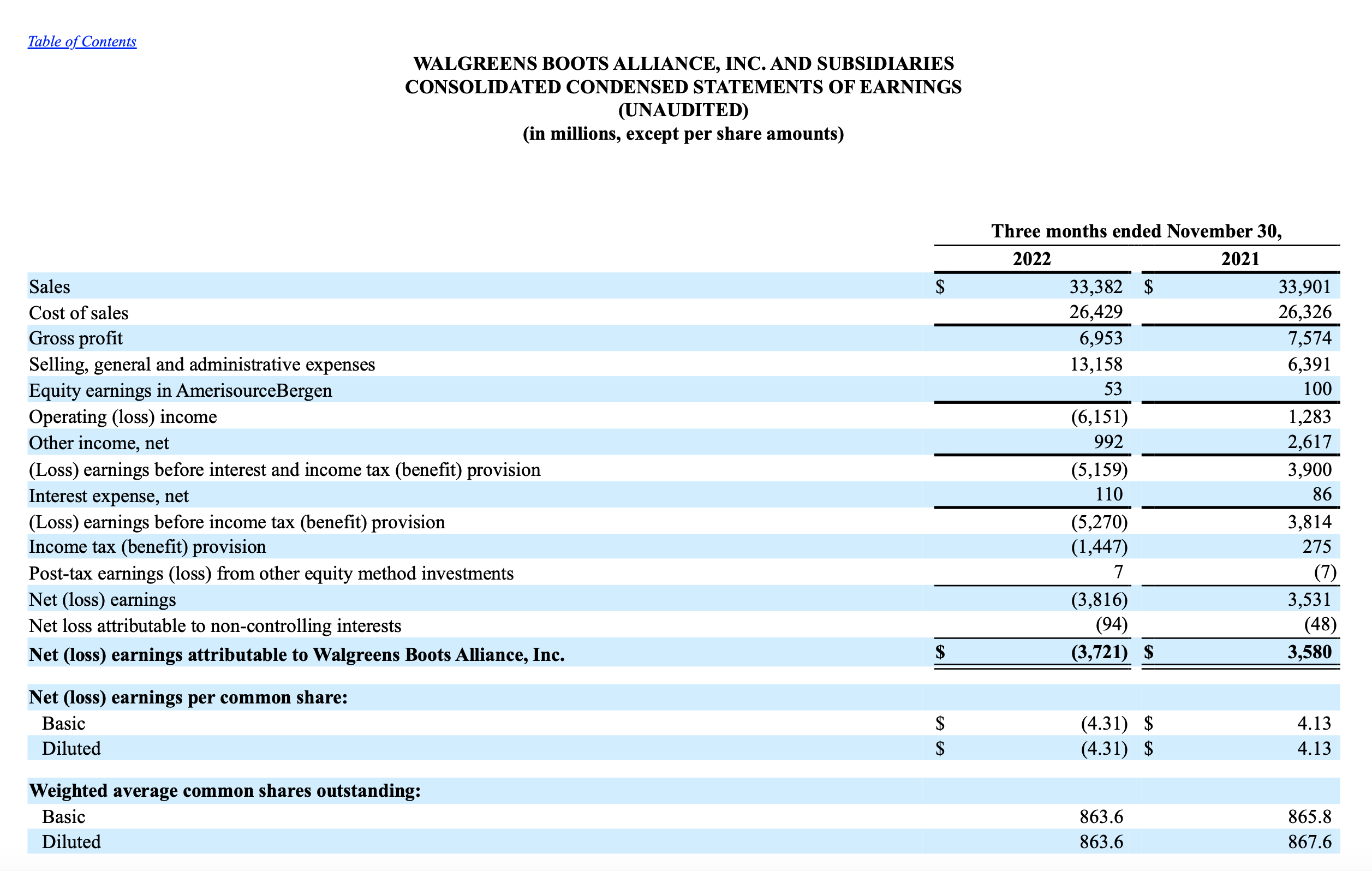

In fiscal Q1 2023, WBA reported a net loss of $4.31 per share, which is a substantial drop from the net earnings per share of $4.13 in the year ago quarter.

10-Q WBA

To understand how this change may impact the dividend payment, we have to understand what has been the primary driver of this decline.

While sales have slightly contracted (but have been up 1.1% on a constant currency basis) and the cost of sales has slightly increased, they have not significantly contributed to the loss. The skyrocketing Selling, General and Administrative (SG&A) expenses have been the reason for the loss in Q1. So what has actually happened? The firm in its press release has provided a brief description of the reason:

[…]a $6.5 billion pre-tax charge recognized in connection with the previously announced opioid litigation settlement frameworks and certain other opioid-related matters […]

This pre-tax charge has been recognised under SG&A expenses. It is however a non-cash expense at the moment and does not have an immediate impact on the firm’s cash position.

Another factor, which has been negatively impacting WBA’s business, is the weakening demand for Covid-19 vaccines. Covid-19 vaccines have been fuelling the 53.1% adjusted EPS growth in the year ago quarter. In Q1, adjusted EPS have declined by 30.8 percent to $1.16, down 29.9 percent on a constant currency basis.

When talking about dividend sustainability, we have to however understand the firm’s cash position and the outlook for 2023 and beyond.

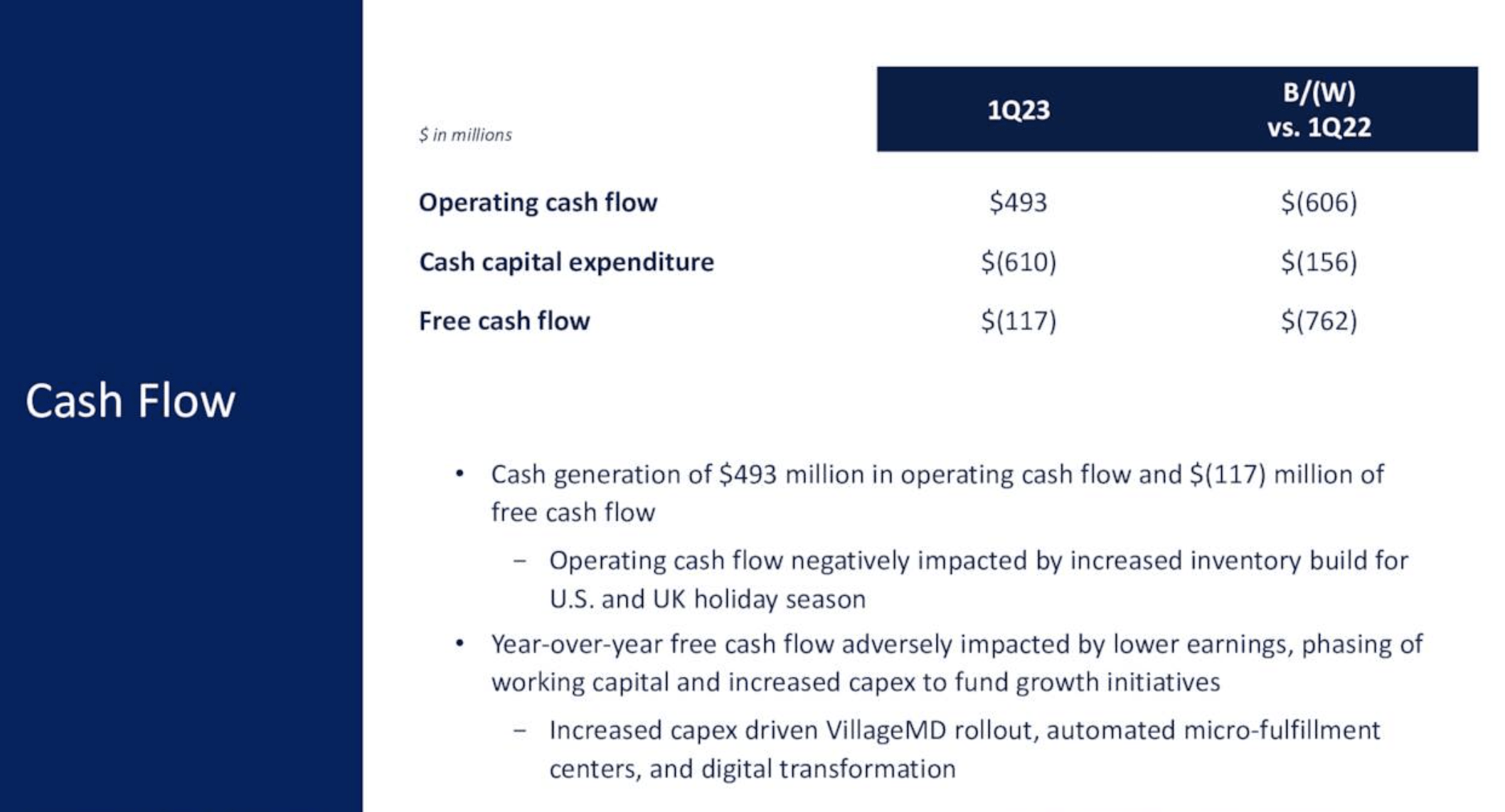

WBA has closed Q1 with negative free cash flow. The drivers have been primarily increased inventory build, lower earnings, increased CAPEX to fund growth and phasing of working capital. Negative cash flow is naturally bad news for both dividend and share buybacks and their sustainability.

Cash flow , WBA

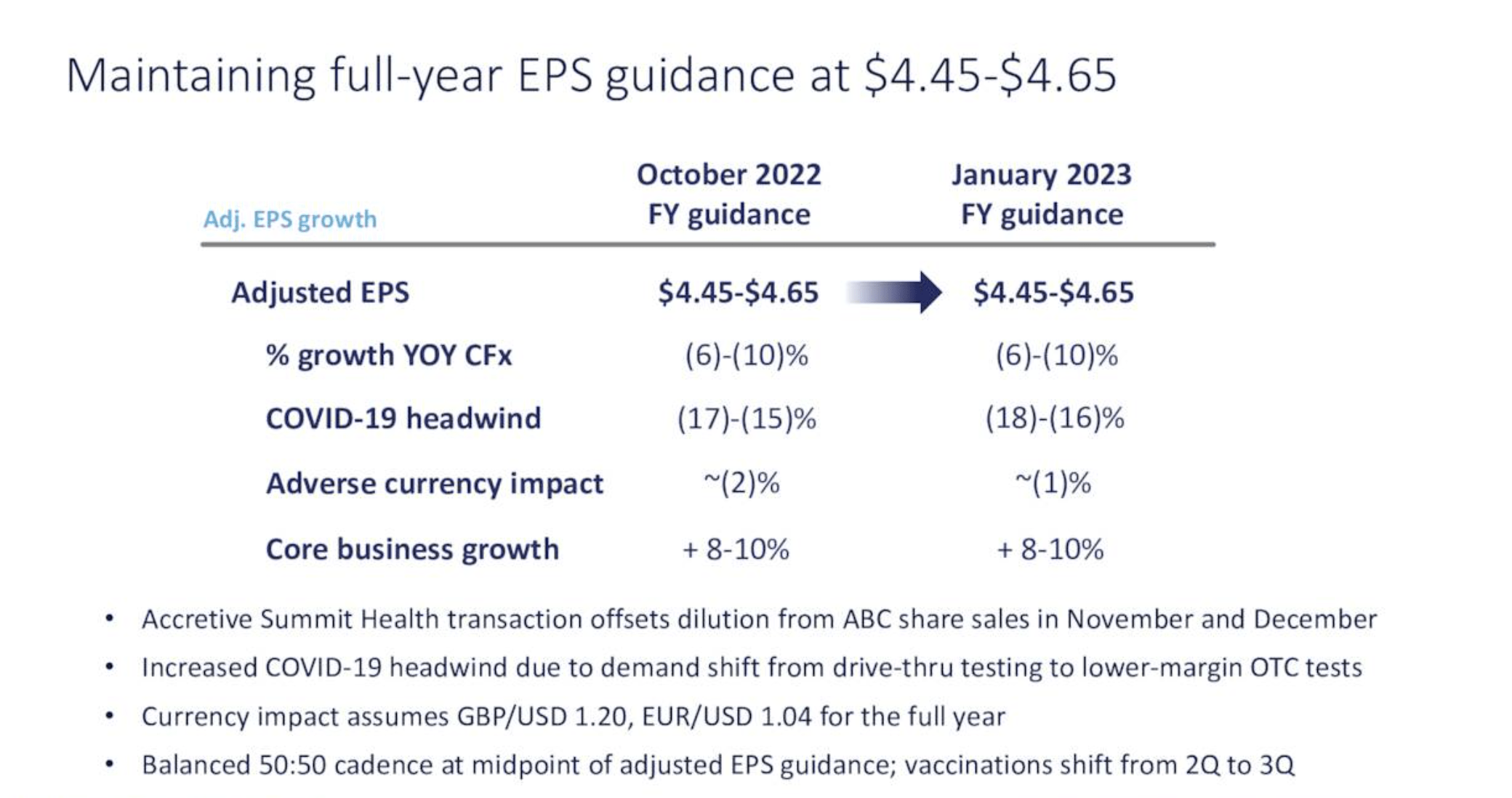

Going forward, however, WBA mostly maintains its earlier published guidance. The negative impact of Covid-19 headwinds is likely to be somewhat worse than expected, but the currency headwinds are now expected to be less severe.

Guidance , WBA

So let us answer now our initial question in light of the new Q1 information, will the dividend remain sustainable?

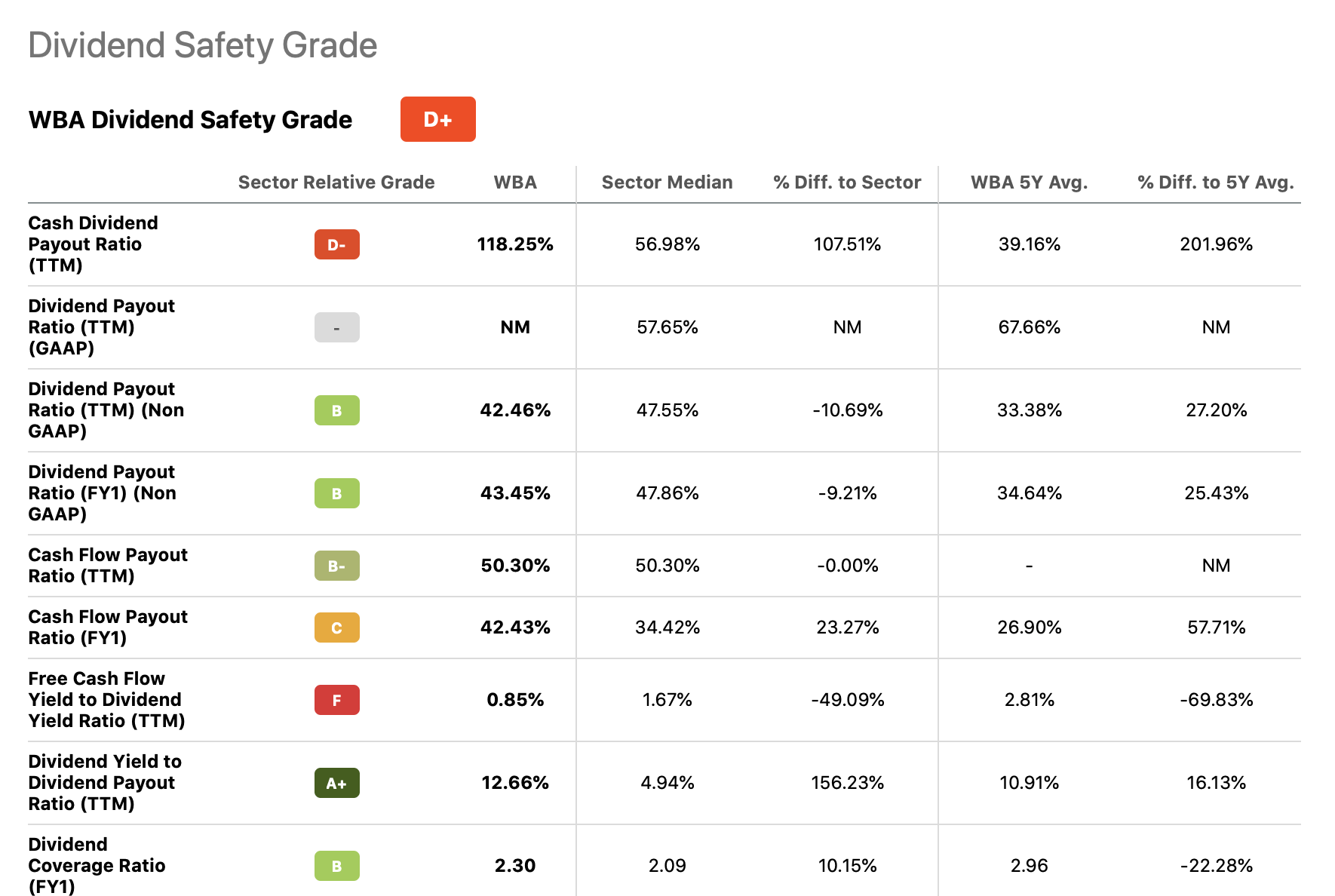

When looking at the dividend safety grades of WBA, we see a substantial decline in terms of the cash dividend payout ratio TTM, compared to the figure in December 2022 (77%). While a figure above 100% is naturally concerning, we expect that WBA will be cash flow positive in the coming quarters and this figure is likely to improve in the near term.

Dividend safety (Seeking Alpha)

Further, the firm’s recent announcement about raising the long-term guidance for the U.S. Healthcare segment, driven by the Summit Health acquisition, is also promising for investors with a longer investment horizon.

All in all, while the news and results have been indeed somewhat negative lately, we believe that the recent weakness in the share price provides a better entry point for investors interested in dividends and dividend growth.

For these reasons, we maintain our “buy” rating.

Be the first to comment