metamorworks

Main Thesis & Background

The purpose of this article is to evaluate the Vanguard Utilities ETF (NYSEARCA:VPU) as an investment option at its current market price. The fund’s stated objective is “to track the performance of a benchmark index that measures the investment return of stocks in the utilities sector” and is managed by Vanguard.

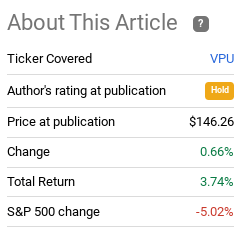

I review VPU ETF periodically because it is a popular way to get broad exposure in the Utilities space and is my largest holding in this sector. I covered the fund almost one year ago to the day, and it is worth noting that it has held up pretty well over what has been a fairly turbulent twelve month period:

Fund Performance (Seeking Alpha)

We dig into 2023, I continue to see a backdrop where Utilities (and VPU) have merit. Personally, I believe the January run-up is a perfect time to take some chips off the table and get more defensive. VPU is one reasonable way to do that, which supports my “buy” rating going forward. I will discuss the logic behind this outlook in the review to follow.

Stocks Rising, Expected Earnings Falling

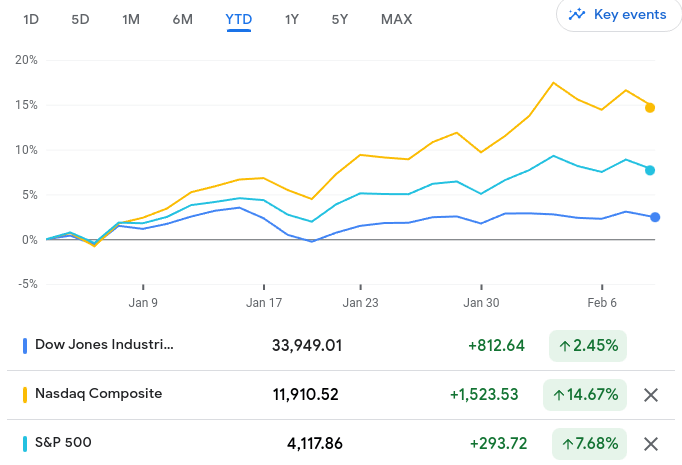

To begin this discussion I will illustrate a key reason behind my general concern about equity prices. This has to do with rising prices and declining expectations – a worrying combination. What I am referring to is the fact that the broad U.S. indices are pushing markedly higher since January 1. This is especially true for the Tech-heavy NASDAQ and S&P 500:

YTD Performance (Google Finance)

Great news, right? Yes, of course, for long equity positions. My concern isn’t stemming from these gains per se. I have enjoyed them and quite frankly they were long overdue! Rather, the broader macro-outlook is getting increasingly challenged. When I combine this reality with rising stock prices, you can see why I might hesitate to maintain a bullish sentiment on the major indices.

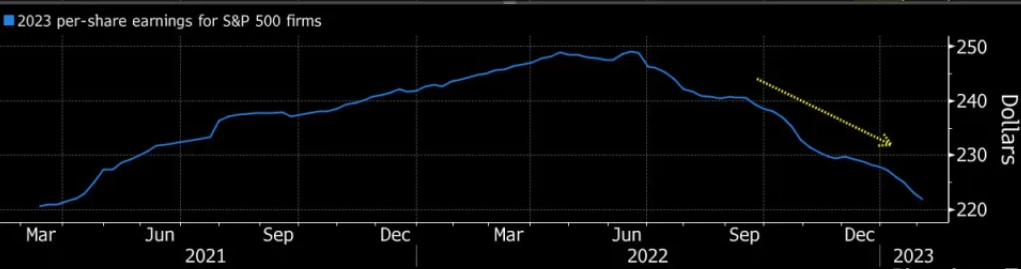

Case in point has to do with expected earnings for 2023. While Q4 earnings have been reasonably well given the challenges of 2022, the outlook for 2023 keeps getting pushed lower. While nobody can know for sure what large-cap earnings will end up being this year, the prevailing sentiment is that earnings are not going to be as strong as once thought. This is evident in the consistent decline among analyst’s 2023 full-year earnings estimates:

Expected Calendar Year Earnings For S&P 500 (2023 Estimated) (Bloomberg)

It is fairly straightforward why this is a potential problem. Of course, equities could keep pushing higher even if earnings come in at those lower levels. Price to earnings multiples are not set in stone and can trade at what is considered “frothy” levels for a long time. But when I see this backdrop I tend to get more conservative. A favorite strategy of mine to do so is VPU, so that is precisely why I am looking to add to my position at these levels.

S&P 500 Remains Under-Weight Utilities

Looking at Utilities as a whole, I will emphasize why this has been a long-term component of my portfolio. This stems to diversification, so it is more than just a defensive and income-oriented play. I do view those latter components as important. But VPU and other Utilities ETFs are not the sole way to get income or defensive positioning.

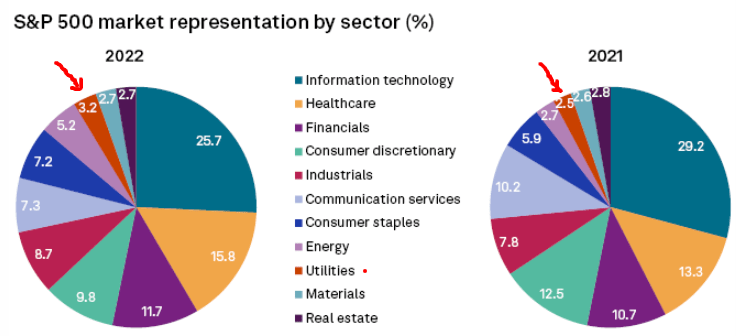

The diversification aspect entices me because my portfolio tends to be large-cap and U.S. dominated. This means I have an overweight positioning to the S&P 500 and the Tech sector as a result. By contrast, the S&P 500 is extremely light on Utilities exposure. While the allocation has ticked up recently from the end of calendar year 2021 to the end of calendar year 2022, that doesn’t mean much:

S&P 500 Sector Weightings (End of Year) (S&P Global)

What I take away from this is that Utilities will generally have a place in my portfolio to round out my sector exposure. I do keep a keen eye on the market for finding the right/best places to add to my position. But I fundamentally have an inclination for owning VPU because it balances what would otherwise be a very Tech/large-cap heavy allocation. Until this balance changes within the S&P 500 (and I don’t see that happening any time soon), the Utilities sector is going to be one favored way to get diversity.

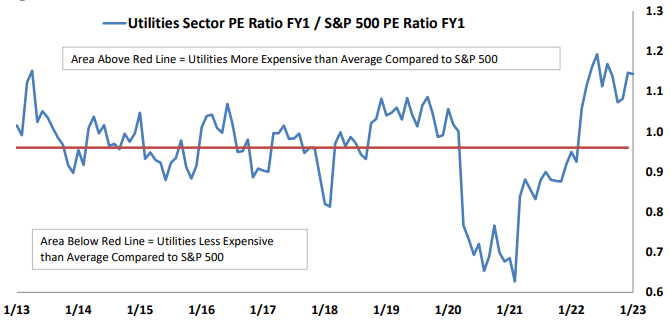

Valuations Still Matter

As with all investments there are usually better times than others to buy. In the case of Utilities, the sector had a relatively good 2022. This was evident in the out-performance by VPU against the S&P 500 since my review one year ago. While positive, the downside to this was the sector was expensive in historical terms. As the P/E of the S&P compressed, that of Utilities pushed higher. This made funds like VPU less attractive for investors looking for value:

Utilities Looked Expensive (FactSet)

Of note, that valuation dispersion was a warning sign that was useful. Going into mid-January, the valuation gap for Utilities certainly turned investors off. Over the past month, we saw a rotation out of the sector and in to more cyclical sectors that drove the S&P 500 higher:

Performance Felt The Impact (Google Finance)

I use this to illustrate two points. One, keep a careful eye on valuation because Utilities are not always a good value. This is not some “ace in the hole” that is immune to market realities. Two, while the valuation gap proved to be a trap over the past month, this performance divergence has removed a good portion of this risk for investors who buy in now. My thought is this recent weakness in VPU and strength in the S&P has evened out the valuation gap. So positions today are once again fairly priced by historical standards – a key distinction.

Electricity/Power Boom Just Getting Started

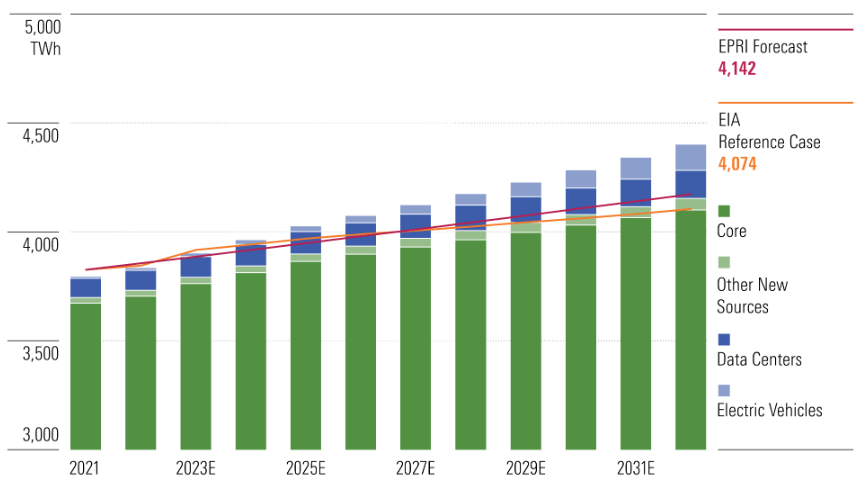

A theme that has been ongoing for the past few years that makes me view Utilities favorably is the change in sentiment towards “clean” energy goals. This is especially true in the U.S. and Europe and is likely to remain top of mind for developed-world governments for the foreseeable future.

Why does this matter? Simply put, the electrification goals right now will require more electricity and power to fund electric vehicles, power stations, household/business electric conversions, solar panel installations, among other trends. When you look at all of the infrastructure investment that’s needed accomplish these objectives, there is growth potential for utility companies and we should expect to see a surge in demand for the services those companies deliver:

Electricity/Power Demand (By Year) (Morningstar)

And the good news for the providers in VPU’s portfolio is that this demand is going to be paid for. Even if their customers (businesses and households) are unable to come up with the green cash themselves, the government is here to help make up the difference. The $430 billion “Inflation Reduction Act” is set to devote billions for tax credits and direct payments for solar, wind, and battery projects. Utility companies, especially the majors, will reap these federal dollars to re-develop their power stations and supply channels.

This is a critical tailwind that the sector can take full advantage of. I expect the next decade will continue to see a move on the part of electric power supplies at the expense of fossil fuels, and the good news for investors is they are not going to have to come up with all the research and development dollars themselves. The government has stepped in to shoulder some of this burden.

Q4 Dividend Growth Provides Comfort

My final point is that Q4 was a reasonably strong quarter for the Utilities sector and that is reflected in the year-over-year dividend growth evident in VPU. This gives me confidence that, as an investor, I am positioned well to benefit from a sector that is willing and able to keep pumping out cash to shareholders. With a current yield still over 3% and impressive growth, there is quite a bit to like:

| Q4 2021 Distribution | Q4 2022 Distribution | YOY Growth |

| $1.06/share | $1.19/share | 12% |

Source: Vanguard

The conclusion I draw here is there is a lot of momentum in the sector. It had a good 2022 (in relative terms) and is set up to have more good years this decade. I see VPU continuing to have a sizable place in my portfolio for these reasons.

Bottom-line

VPU has sold off a bit over the past week and I view that weakness opportunistically. The underlying sector has a lot of growth opportunity, which is historically rare for what used to be a “boring” sector. The fund’s dividend growth impresses and the fund will benefit if the Fed does pump the brakes with respect to rate hikes (which I expect). Looking ahead, I see value in the opportunity and diversification benefits, and will be using any further weakness to build my position in the fund. Therefore, I believe a “buy” rating is warranted and suggest readers give the idea some thought at this time.

Be the first to comment