Artur Nichiporenko

Vicor Corporation (NASDAQ:VICR) serves multiple sectors, and offers international revenue exposure. In addition, management recently reported impressive quarterly numbers from the sale of Brick Products. In my opinion, if the company continues to offer sufficient differentiation, and free cash flow expectations trend higher, the fair valuation could stay close to $83 per share. I obviously identified several risks from large competitors, suppliers, and lawsuits. With that, in my opinion, Vicor appears undervalued by the market.

Vicor Generates Most Of Its Revenue Outside The United States, And Most Employees Are Based In The United States

Established in Massachusetts, Vicor Corp is a company dedicated to the design and manufacture of power modules. In addition to product development, Vicor manages their marketing and distribution, which are mainly used for the conversion of electrical energy. The devices and the design of the power control systems of the company have four specific functions: transformation, isolation, rectification, and regulation.

I appreciate quite a bit that Vicor targets very different markets. Due to the nature of its products, the company has access to a large number of industries, which use complex electrical networks in their daily operations. Some examples of Vicor Corp’s frequent customers are the automotive, communication, computer, defense and aerospace, robotics, and LED panel industries.

Vicor has offices throughout the United States as well as established support centers in foreign countries. It is quite beneficial that Vicor’s employees are mainly based in the United States. However, 2021 sales outside the United States touched 67%. In my view, it means that Vicor’s internationalization does not seem that complicated. Vicor does not need employees overseas to generate revenue.

As of December 31, 2021, we had 1,027 full-time employees, of which 924 were in the U.S. and 103 were in our international locations.

For the years ended December 31, 2021, 2020, and 2019, revenues from sales outside the United States were 67.0%, 64.4%, and 53.7%, respectively, of our total revenues. Source: 10-k

With An Asset/Liability Ratio Close To 7x, Vicor’s Balance Sheet Appears Healthy

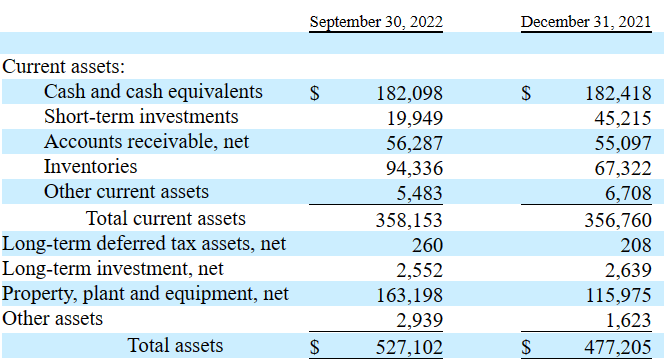

As of September 30, 2022, Vicor reported cash worth $182.098 million in addition to short term investments of close to $19.949 million. The accounts receivable were $56.287 million, with inventories of $94.336 million and total current assets of $358.153 million. Total current assets are close to 5x the total amount of current liabilities, so Vicor appears to have an abundant amount of liquidity.

Property was worth $163.198 million, and adding everything up gives us a result of total assets of $527.102 million. Considering these figures, I believe that the balance sheet appears quite healthy.

Source: 10-Q

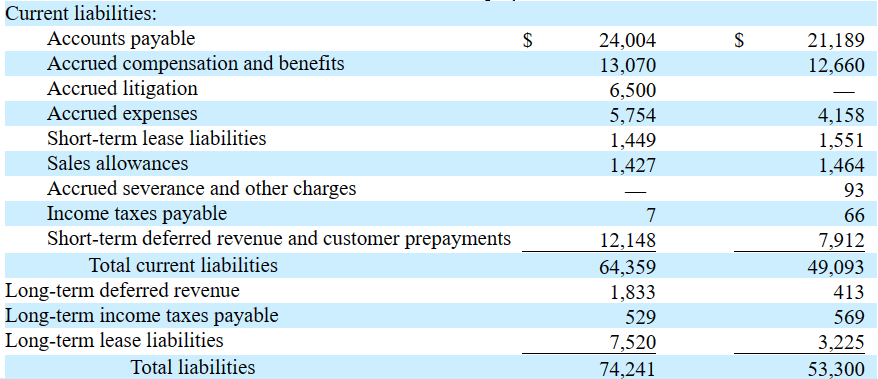

Vicor also reported accounts payable worth $24 million together with accrued compensation of $13 million, accrued litigation of $6.5 million, and accrued expenses of $5.754 million. Besides, short term deferred revenue was equal to $12.148 million with total current liabilities of $64.359 million. Finally, with long term lease liabilities worth $7.520 million, total liabilities stand at only $74.241 million.

Source: 10-Q

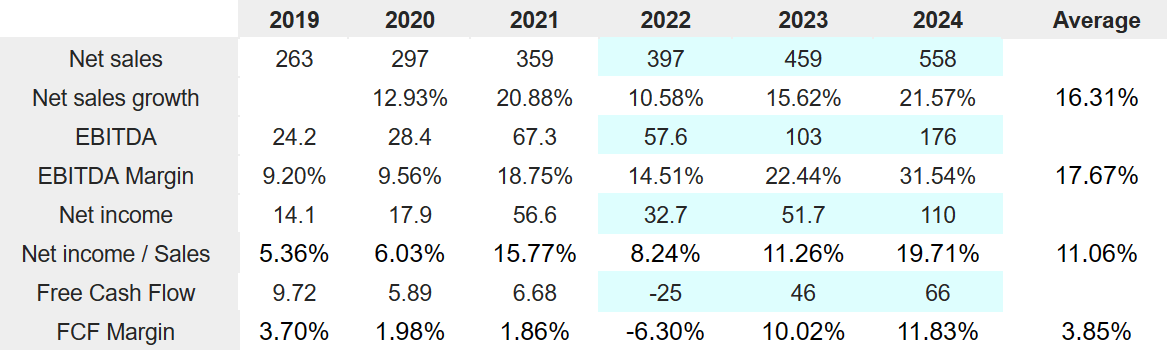

Expectations From Other Financial Analysts Include An Average Sales Growth Of 16%, Average EBITDA Margin Of 17%, And Average Margin Of 3.85%

I believe that most investment advisors are expecting beneficial figures for Vicor. 2024 net sales are expected to be $558 million with a net sales growth of 21.57%. In addition to 2024 EBITDA of $176 million and an EBITDA margin of 31.54%, 2024 net income would stand at $110 million along with a net income / sales of 19.71%. Finally, 2024 FCF would be $66 million with 2024 FCF margin of 11.83%.

Source: S&P Capital IQ Estimates

Further Successful Development Of Brick Products And More Differentiation Could Lead To A Valuation Of $83 Per Share

Vicor’s strategy at present is based on the differentiation of its products from other similar products on the market as well as the effectiveness of their performance and the high quality of the solutions they provide. Under this scenario, I assumed that Vicor would successfully continue to offer innovative products. More in particular, I believe that further investment and design of new Brick Products could bring revenue growth. Let’s keep in mind that in the last quarterly report, net revenue from Brick Products increased significantly.

Net revenues for Brick Products increased 27.2% compared to the second quarter of 2022, primarily due to the ability to shift manufacturing resources to focus on available backlog, as well as, favorable market conditions in North America and Europe for Brick Products. Source: 10-Q

Vicor offers products to final consumers such as family groups or devices that are used in common home electrical network installations. Besides, it offers advanced and highly developed products, marketed in specific niches. Among its common clients, the telecommunications industry is the one that concentrates Vicor’s energies the most, since it is where they understand that there will be a greater projection in the future. Under this scenario, I assumed that the company’s know-how accumulated working for the telecommunications industry and home electrical networks will likely bring further revenue growth.

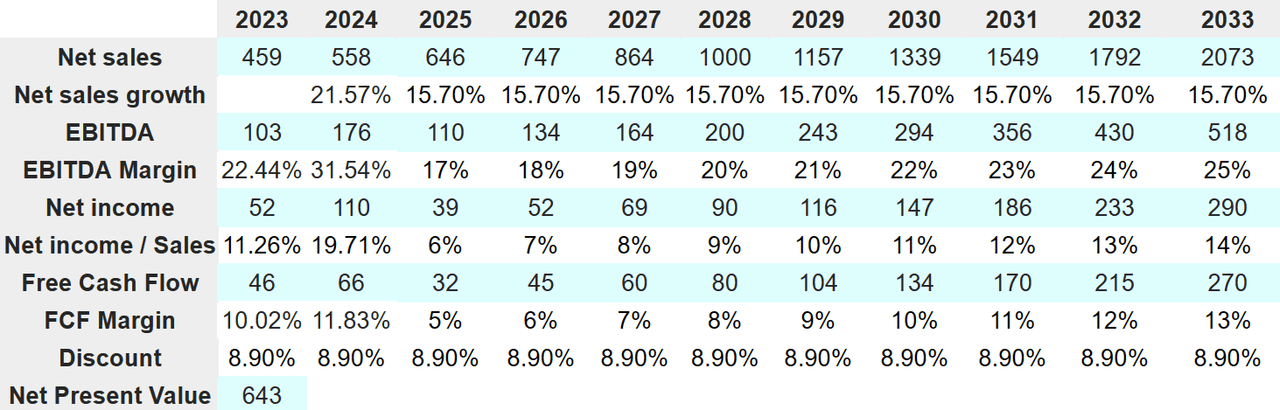

I included 2033 net sales close to $2.073 billion together with a net revenue growth of 15.70%, 2033 EBITDA of $518 million, and an EBITDA margin of 25%. 2033 net income would stand at $290 million with a net income/sales ratio of 14%. Besides, 2033 free cash flow would be $270 million with a 2033 FCF margin of 13%. Summing the FCF and using a discount of 8.90%, net present value is $643 million.

Source: Malak’s Financial Model

Now, with an EV/EBITDA multiple of 14x, the terminal value would be $7.256 billion, and the NPV would be close to $2.841 billion. If we also assume debt of $13 million and cash of $182 million, the enterprise value would be close to $3.48 billion, and the equity would stand at $3.653 billion. Finally, the fair price would be $83 per share with an internal rate of return of 2.73%.

Source: Malak’s Financial Model

Competitors, Risks From Suppliers, Lawsuits, or Brand Destruction Could Bring The Fair Price To $55

Regarding Vicor’s competition both nationally and globally, the company coexists with other companies of different sizes for both of its segments. If we refer to advanced products, Vicor competes with large companies that have capital and infrastructure that allow them to carry out a large amount of research in the technological field. In regional markets, Vicor competes with local products and service providers at a smaller scale. Under this case scenario, I assumed that competitors may offer better technology than that of Vicor, which would bring the company’s FCF margin down.

In addition, due to Vicor’s type of production, the company directly depends on a large number of suppliers as well as third-party activities, which in the event of complications or interruptions in the supply chain could affect the normal operations of the company.

Besides, international regulations regarding the export and import of materials, such as the recent Chinese taxes on US exports, could increase the costs for Vicor. As a result, shareholders may see how free cash flow expectations would decline.

Finally, Vicor has an uncertain legal situation regarding securing its intellectual materials in the future and the current state of development of its products, which have received various lawsuits regarding intellectual property and design plans. These legal complications can generate high costs, and damage the brand and credibility of the company in the sector:

From time to time, we may be subject to claims or litigation, including intellectual property litigation. Any such claims or litigation may be time-consuming and costly, divert management resources, require us to change our products, or have other adverse effects on our business. Any of the foregoing could have a material adverse effect on our operating results and could require us to pay significant monetary damages. Source: 10-k

The Company is the defendant in a patent infringement lawsuit originally filed on January 28, 2011 by SynQor, Inc. in the U.S. District Court for the Eastern District of Texas. Vicor filed a motion for summary judgment of non-infringement on February 4, 2022. The Court has not yet ruled on that motion. Source: 10-k

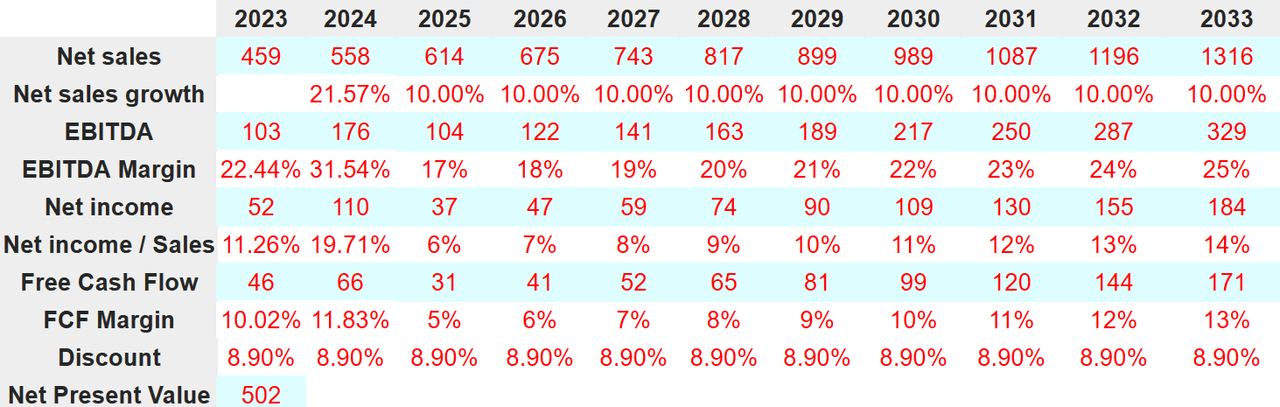

Under my bearish case scenario, 2033 net revenue would be $1.316 billion together with a net sales growth of 10%, 2033 EBITDA of $329 million, and 2033 EBITDA margin of 25%. I also expect 2033 net income of $184 million along with a net income/sales ratio of 14%. 2033 Free cash flow would be close to $171 million accompanied by an FCF margin of 13%. Under this case, if we use a discount of 8.90%, the net present value would be $502 million.

Source: Malak’s Financial Model

Under this case, I obtained a NPV of terminal value of $1.73 billion, enterprise value of $2.2 billion, and equity of $2.409 billion. Finally, with a share count close to 44 million, the price would stand at $55 per share with an IRR of -1.02%.

Source: Malak’s Financial Model

My Takeaway

With accumulated know-how in very different sectors, Vicor appears well diversified, and obtains revenue from a number of countries. Considering the recent quarterly numbers delivered from the sale of Brick Products, I am quite optimistic about Vicor’s future and differentiation strategy. In my view, basic assumptions about Vicor’s free cash flow would imply a valuation that is significantly higher than what the market indicates. Even taking into account risks from competitors or supply chain disruptions, Vicor appears cheap.

Be the first to comment