BrettCharlton

Nobody said picking your own stocks would be easy, but that’s what makes it fun. For one thing, many retail investors like being engaged with the market, and it’s simply a good feeling to have a direct ownership stake in premium brands.

Furthermore, index funds and non-leveraged ETFs generally yield less than 4%, making it difficult for income investors to extract meaningful immediate income from them. That’s why it may pay better to invest in REITs, which despite the recent downturn due to higher interest rates, is one of the asset classes that are primed to benefit from inflation.

This brings me to VICI Properties (NYSE:VICI), which is currently trading well below its recent high of ~$34 reached in December. In this article, I highlight why VICI is an easy choice for dividend growth investors at present, so let’s get started.

Why VICI?

VICI Properties is a premier experiential REIT that’s headquartered in New York City, and holds iconic gaming and hospitality properties along the Las Vegas strip and around the U.S. It kicked off with a bang in 2018, when it was spun-off from Caesars Entertainment (CZR).

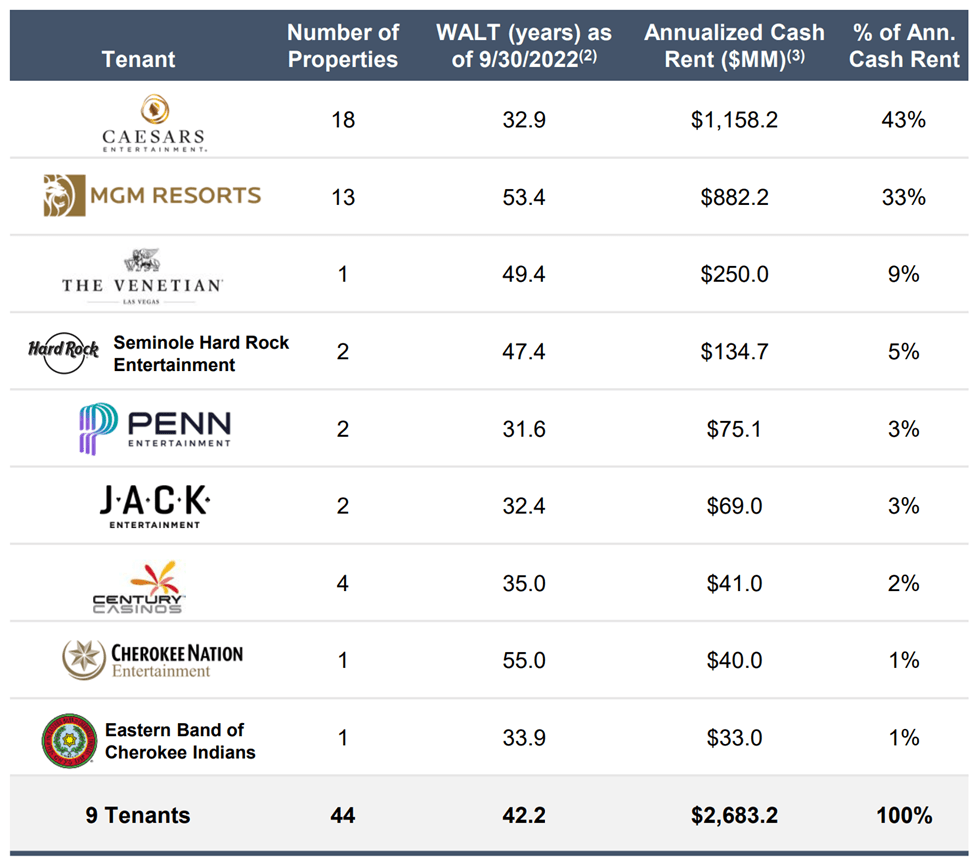

VICI has since bolted out of the gate with a series of transformational acquisitions in recent years, among which include MGM Growth Properties and the Venetian Resort. As shown below, VICI is not very diversified, but makes up for that with high exposure to very high quality tenants, with Caesars, MGM, and the Venetian making up 85% of its annual base rent.

VICI Tenant Mix (Investor Presentation)

A key advantage of VICI is its partnership with leading operators that reside in its properties under 100% triple net leases, which makes the tenant responsible for property maintenance, tax, and insurance. Like for that of VICI’s net lease peers, this arrangement results in far higher operating margins for the landlord, and makes it more able to handle adversity due to a lower operating cost structure.

Moreover, 91% of VICI’s leases come with parent guarantees, 76% are from S&P 500 (SPY) tenants, and 80% are publicly-traded, subject to SEC reporting rules. This means transparency of operations for VICI as the landlord. It also has the longest remaining lease term among its net lease peers, at 42 years, compared to the 9 to 13 years of the industry average.

Importantly, VICI’s strong external growth is translating to its bottom line, with AFFO per share growing by 8.5% YoY to $0.49 during the fourth quarter. It also continues to grow with two loan investments with Great Wolf Resorts totaling $186 million, two hotel and casino property acquisitions in Mississippi for $293 million from Foundation Gaming & Entertainment, and announced a $204 million acquisition of Rocky Gap Casino Resort.

Meanwhile, VICI is well-positioned with a BBB- rated balance sheet with a last quarter annualized net leverage ratio of 5.8x, sitting below the 6.0x market that’s viewed as being safe by credit ratings agencies. Management has also stated a long-term leverage target in the 5.0 to 5.5x range.

Plus, VICI is shielded from the immediate impact of higher interest rates, as 100% of its outstanding debt is held at fixed rates. VICI’s debt maturities are also well-staggered as to lessen the risk of higher rates in any one year, and has 6.9 weighted average years to maturity.

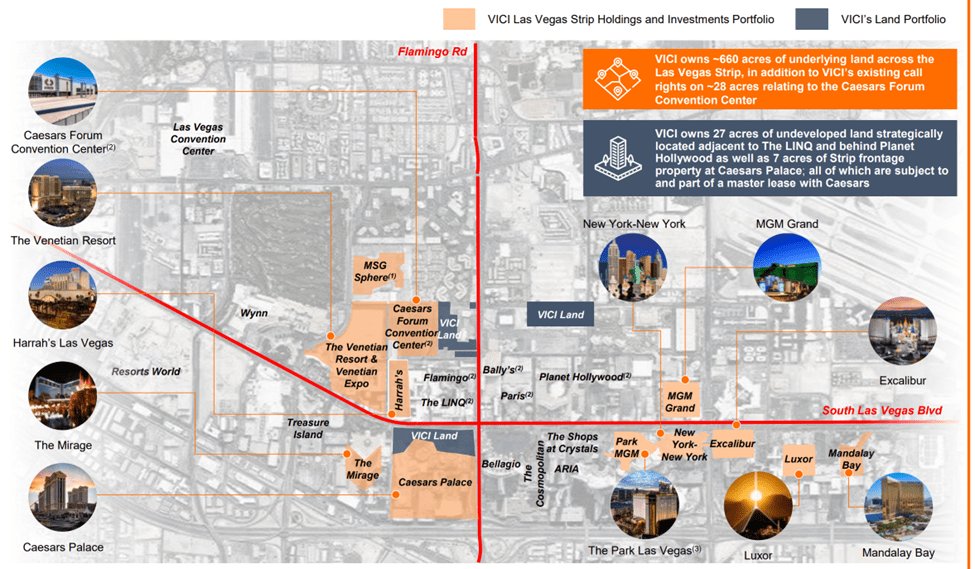

Looking forward, VICI is well-positioned due to its well-placed properties in high barrier to entry markets. It also has limited impact from inflation, as 47% of its leases have uncapped CPI-linked escalation, with much of the remainder having CPI-linked escalation subject to caps. VICI also carries a valuable land bank, with 660 acres of prime undeveloped land that’s strategically located along the Las Vegas strip, as shown below.

VICI Development Opportunities (Investor Presentation)

Importantly, VICI is rewarding shareholders with dividend raises, including the last 8.3% raise last year. The dividend is also well-covered by a 79.6% payout ratio and I would expect to see another raise announcement in August of this year.

While VICI doesn’t necessarily scream cheap at the current price of $31.81 with Price to annualized AFFO of 16.2, it’s also not unreasonably expensive. Plus, analysts expect double-digit FFO per share growth next year, which would materially drive down the valuation based on the current price.

Analysts have a consensus Strong Buy rating on the stock with an average price target of $37.61, which could mean potentially very strong double-digit total returns from the present level.

Investor Takeaway

VICI Properties owns premier and iconic properties with strong external growth, a solid balance sheet, and a well-protected and growing dividend. The current price doesn’t seem to fully bake in the incremental revenue and income that VICI should see throughout this year, presenting a value opportunity at current levels. As such, I view VICI as being an “easy” buy for those looking for a high quality yield coupled with an attractive valuation.

Be the first to comment