ShutterWorx/E+ via Getty Images

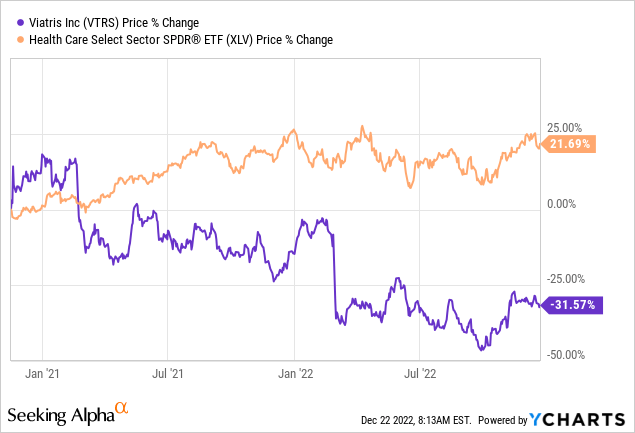

Viatris Inc. (NASDAQ:VTRS) has struggled to deliver good returns since its formation. The combination of Mylan Labs and Pfizer’s (PFE) generic division has always kept the allure of the low multiple to draw in investors. But it has failed to turn that into something they can smile about. Since the spin-off listing, VTRS has trailed the Health Care Select Sector SPDR by 53%.

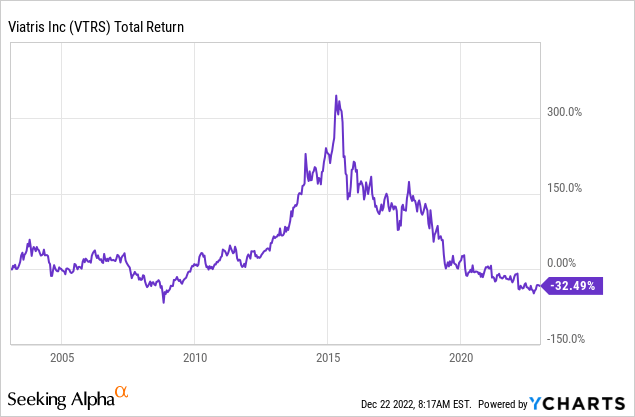

From a very long-term perspective, owners of the former Mylan Labs are still smarting. If you bought on January 1, 2003, you would be down 32.49%, almost 20 years later.

As is often the case, these long periods of underperformance are worth watching as they create good entry points for risk-averse investors. We go over the recently released results, the announced acquisitions and tell you where we stand.

Q3-2022

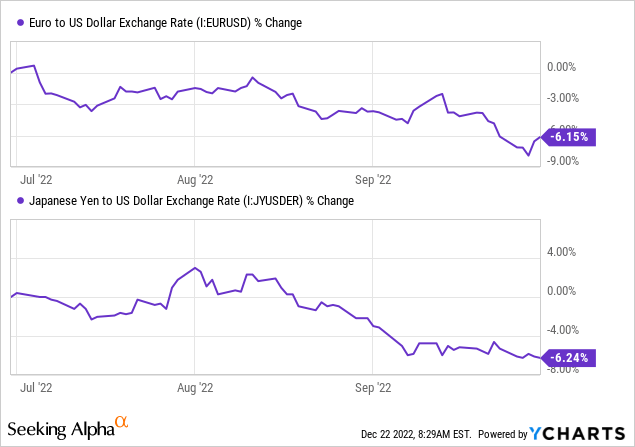

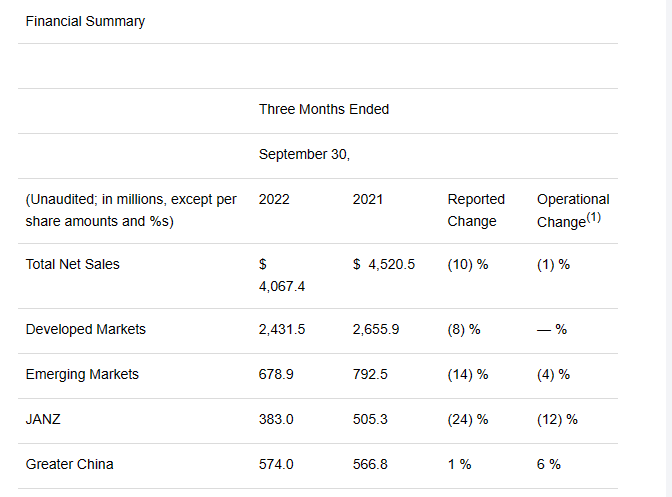

VTRS had one tough quarterly setup as Q3-2022 saw the strongest forex headwinds to date. Both the Euro and the Yen fell about 6% during the quarter.

While we can make light of stocks moving even 6% in a day, major developed world currencies moving 6% in a quarter is a big deal. This was on top of an already strong US Dollar performance for most of 2022. The result was that VTRS had a really sloppy showing on total net sales, down 10% year over year.

VTRS Q3-2022 Press Release

The positive though was that the operational change, which strips out Forex impacts, was looking more respectable. You can see that in the emerging markets, declines were moderated to just 4%. Interestingly, China, which has in the past been a source of a lot of declines, was actually up, adjusted for the Yuan weakness.

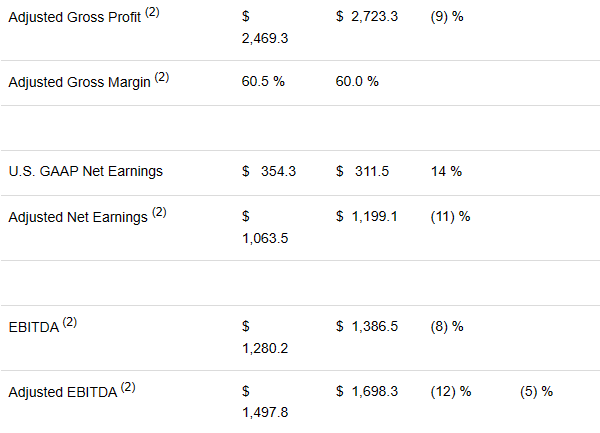

Readers who have followed our work would know that we are definitely not cheerleaders and generally overdo our critique rather than our praise. But there were some really praiseworthy things in the performance. Adjusted gross profit for the third quarter (shown on screen left), was down just 9%, and adjusted gross margins were up from 60.0% to 60.5%.

VTRS Q3-2022 Press Release

Adjusted EBITDA was down 12% in Q3-2022 and only 5% when stripping out currency impacts. While investors may think we are being facetious, we definitely are not. This was a brutal quarter when you consider the combination of sales declines, forex impacts, and very high levels of inflation. It is amazing how adjusted gross margins actually went up. Adjusted EBITDA of course dropped, but it should have dropped far more. While management has rightly been criticized for a lot of misses, this quarter was quite impressive.

Valuation Compression

Bulls keep focusing on the low P/E ratio and wondering why VTRS has not been able to increase its multiple. For a heavily indebted company, an 18% decline in adjusted EBITDA (from Q1-2020 till Q3-2022) can wipe away a lot of good news.

VTRS Q1-2021 Presentation

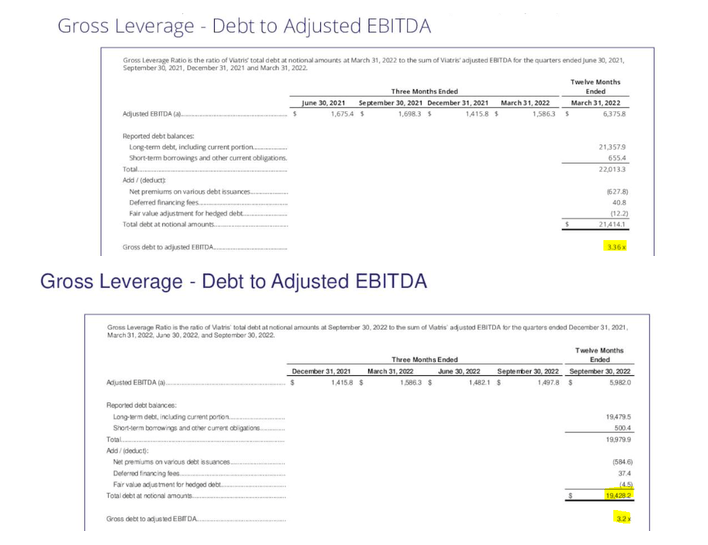

Despite the EBITDA declines, the leverage ratio is improving modestly. It has moved from 3.36X at the end of Q1-2022 to 3.20X today.

VTRS Q1 & Q3 2022 Presentations

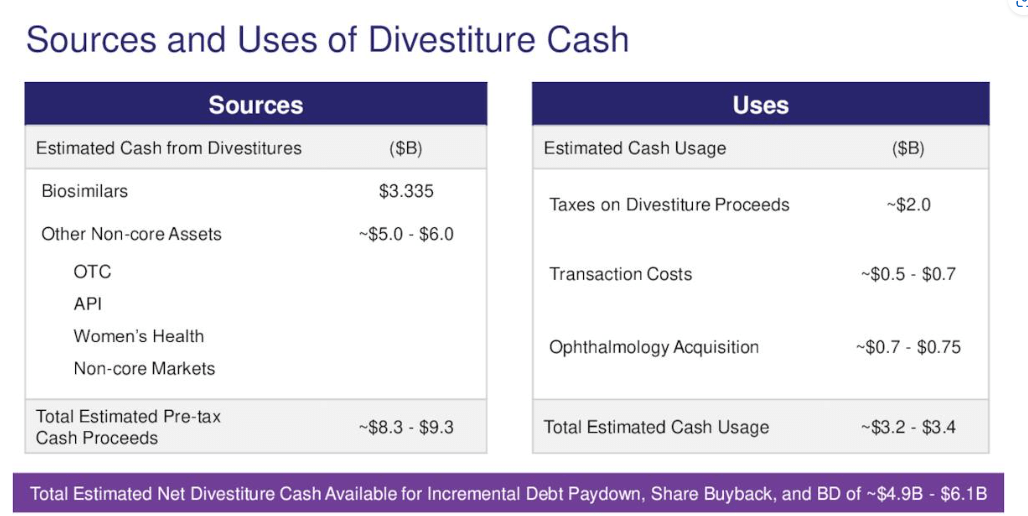

The committed and planned asset sales should bring the leverage ratio comfortably under 3.0X.

VTRS Q3-2022 Presentation

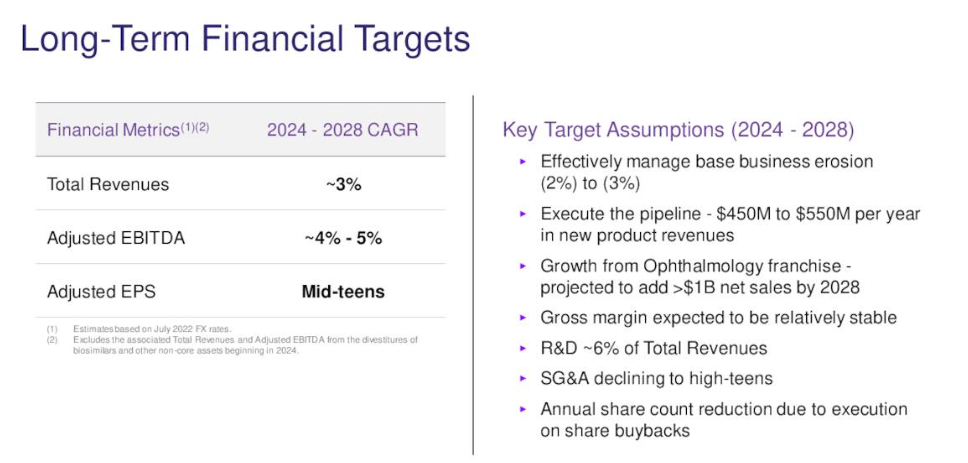

While VTRS mentions stock buybacks, we doubt those will occur unless organic sales stabilize. VTRS revealed its long-term plan for that, which begins in 2024.

VTRS Q3-2022 Presentation

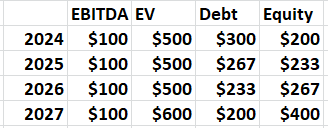

If VTRS delivers a 3% annual sales growth and 4-5% adjusted EBITDA growth, the stock should double, at a minimum. The math is pretty straightforward here as the company should be trading at close to 5.0X EV to EBITDA when all these divestitures are done. If that revenue base starts moving up, you can get the doubling within three years just debt reduction and a slight multiple expansion to 6.0X EV to EBITDA. In the figure below, we have assumed that EBITDA stays flat and debt is reduced over three years. In the third year, we have expanded EV to EBITDA by one multiple.

Author’s Calculations

We can actually extrapolate this outcome even if sales stay flat, and they execute buybacks near this multiple.

VTRS Q3-2022 Presentation

The Acquisitions

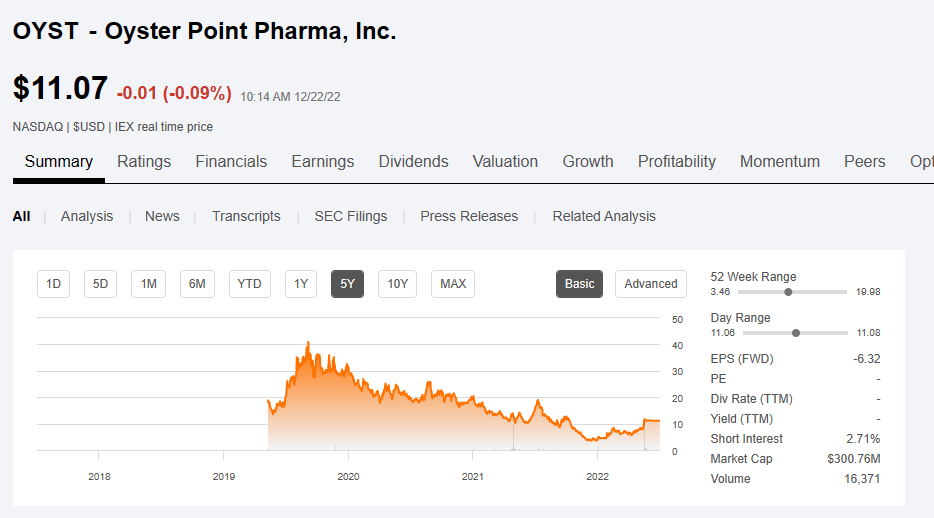

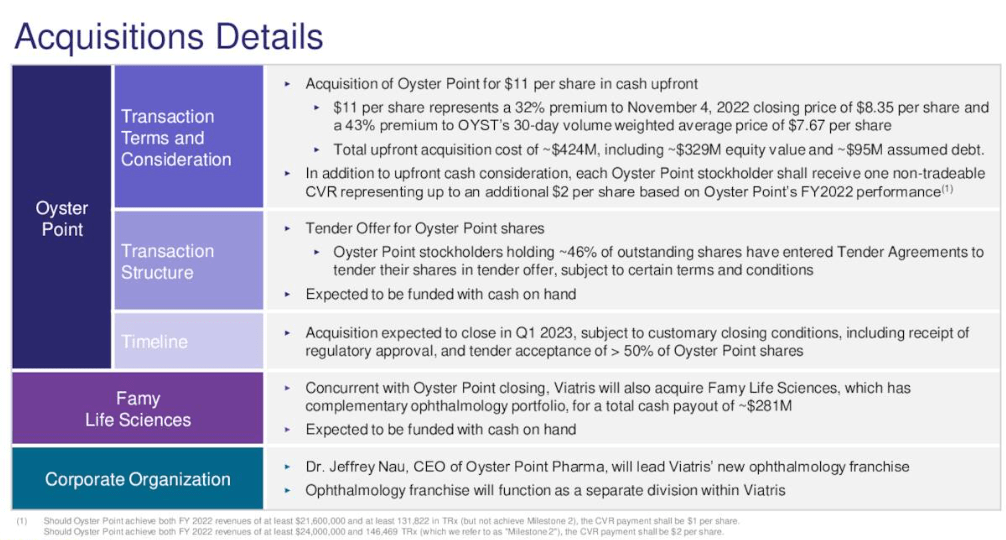

The two recently announced acquisitions were an interesting twist in the old plot. While Oyster Point (OYST) was bought at a 43% premium, this was definitely not chasing a stock at the highs.

Seeking Alpha

VTRS did not want to waste the shock effect of the moment and also added a second acquisition of the ophthalmology department of Famy Life Sciences for $281 million.

VTRS Q3-2022 Presentation

In one fell swoop, VTRS has spent over $700 million. The good part about the Oyster Point acquisition is that it makes VTRS sales declines look great in comparison.

The purchase price at 20X sales definitely hinges on the future being far brighter than the past. The full weight of this expectation comes on Tyrvaya and some development pipeline products.

In addition to that, the Famy Life Science’s acquisition will add five additional Phase III or Phase III-ready front-of-the-eye programs in various indications. We believe Tyrvaya and these front of the eye ophthalmology assets could potentially have combined annual revenue of at least $1 billion by 2028.

Source: Q3-2022 Conference Call Transcript

There was obviously a heavy dose of skepticism on this.

Elliot Wilbur

My first question and only question, I guess, is with respect to the acquisition of Oyster Point and Famy Life Sciences. I know you’ve talked about the ophthalmology portfolio generating around $1 billion in sales by 2028. But if I look at current external expectations, at least for Oyster Point, they seem to embed peak sales somewhere around $400 million, which I assume is Tyrvaya exclusively in 2027. And I know that you’re expecting contribution from some other pipeline assets, but doesn’t seem like many of those would hit before 2025 or 2026. So I’m trying to close the gap there between external expectations and what you are anticipating in terms of contribution from the new broader portfolio. Are you simply more optimistic on Tyrvaya than external expectations? Or am I under appreciating the potential contribution from some of the pipeline assets in that period of time?

Rajiv Malik

Elliot, I will take. And maybe later on, Jeff can add. So first of all, let me just break it. One is that, yes, Tyrvaya U.S. expectations and we are talking about the global expectations. We have take this $1 billion, divide almost 2/3 is U.S. and 1/3 is the rest of the world for us. That’s the first one.

The second one is most and maybe every — all of these products will hit the market within this period of time. Because as you see, there are some Phase III assets and well advanced. And it’s not going to be a long clinical study over there. So, we see more products launched around ’26, ’27 to add on along with Tyrvaya.

Source: Q3-2022 Conference Call Transcript

We think management is taking a bit of a long shot here, and time will tell whether it was worth buying these.

Verdict

The new acquisitions definitely cloud the developing long case. We wish we could be as optimistic as management, but the past has validated our cautious stance. At 20X current sales for Oyster Point, you would need some real breathtaking fireworks in the future to make this work. On the second front, VTRS is probably in a better position to assess the true value.

Let me just address on the Famy assets. I’d like to make a point that we’ve been around these assets for the last five years. We helped set up this company originally. We have a small 13.5% stake. And we’ve watched the development of what this company has done. So we’re very, very familiar with these assets.

Source: Q3-2022 Conference Call Transcript

Nonetheless, one has to wonder whether a straight debt reduction for an enterprise valued so cheaply would be a better alternative. We were very close to actually dipping our toes into the water, with perhaps some out of the money option action (like selling the $9.00 cash secured puts), but with this new information, we decided to take a pass. We maintain our hold rating for now.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment