gawrav

The Quarter

Vermilion Energy (NYSE:VET) reported an amazing operating quarter last week (August 11th) that included earnings of $2.20 and about $400 million of free cash (cash from operations ex w/c minus capital expenditures). This brings year to date for the first six months earnings and free cash flow to $3.96/share and about $670 million, respectively – on a $25 stock and $5.3 billion market cap.

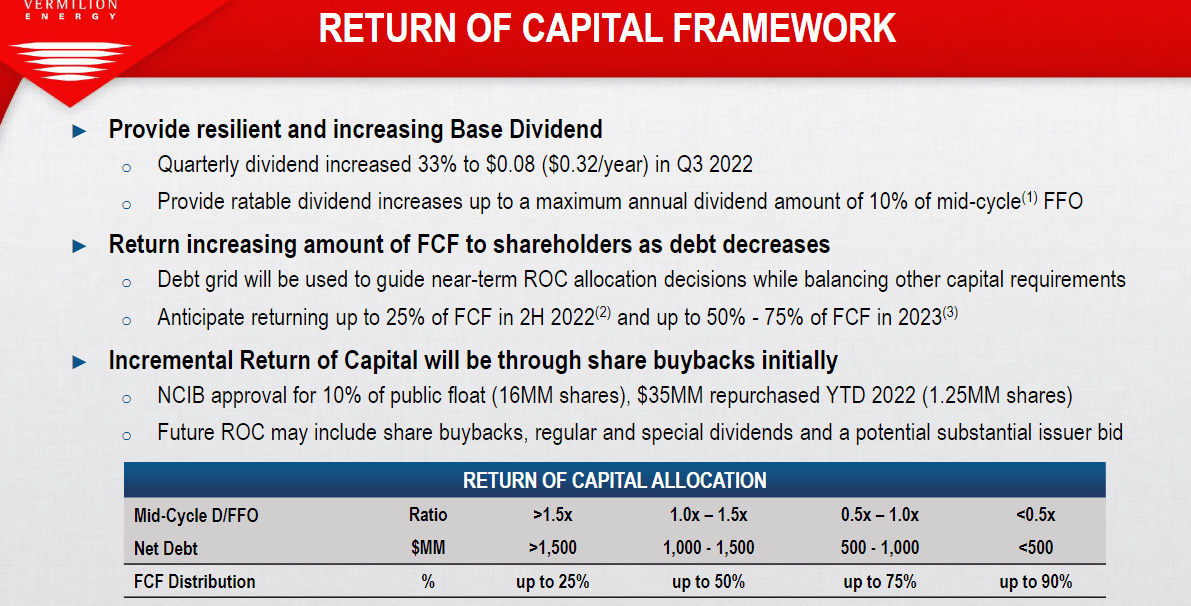

Curiously, the stock fell the day after the report and then again today (Monday the 15th). I think some people were expecting some big announcement about capital return. Oil prices falling didn’t help either. The company didn’t totally disappoint on the company return front. They laid out a grid of what percentage of free cash would be returned given a level of indebtedness.

Capital Return Grid Based on Debt Levels (VET Q2 Presentation)

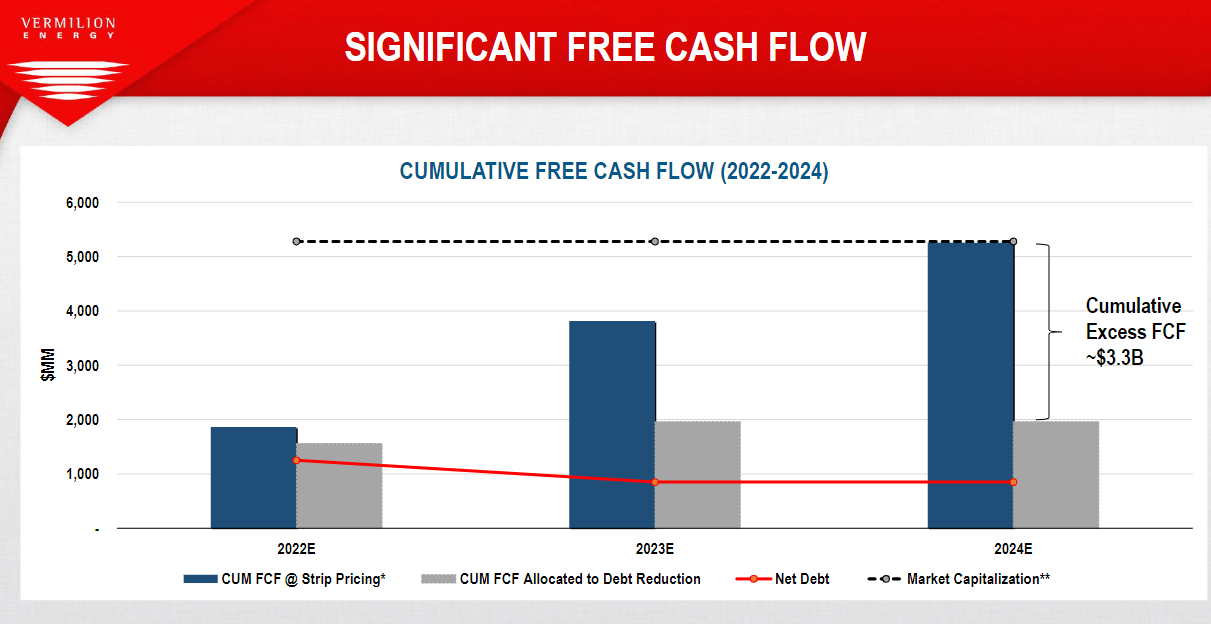

The company finished the quarter with about $1.6 billion of net debt and expects to finish the year with about ~$1.2 billion. So, expect free cash return to pick up meaningfully soon and should continue through at least next year if not 2024.

Cash Flow Return vs Debt Reduction (VET Q2 Presentation)

For those who might have forgotten, the company already has a 10% normal course issuer bid in place.

Focus on European Natural Gas

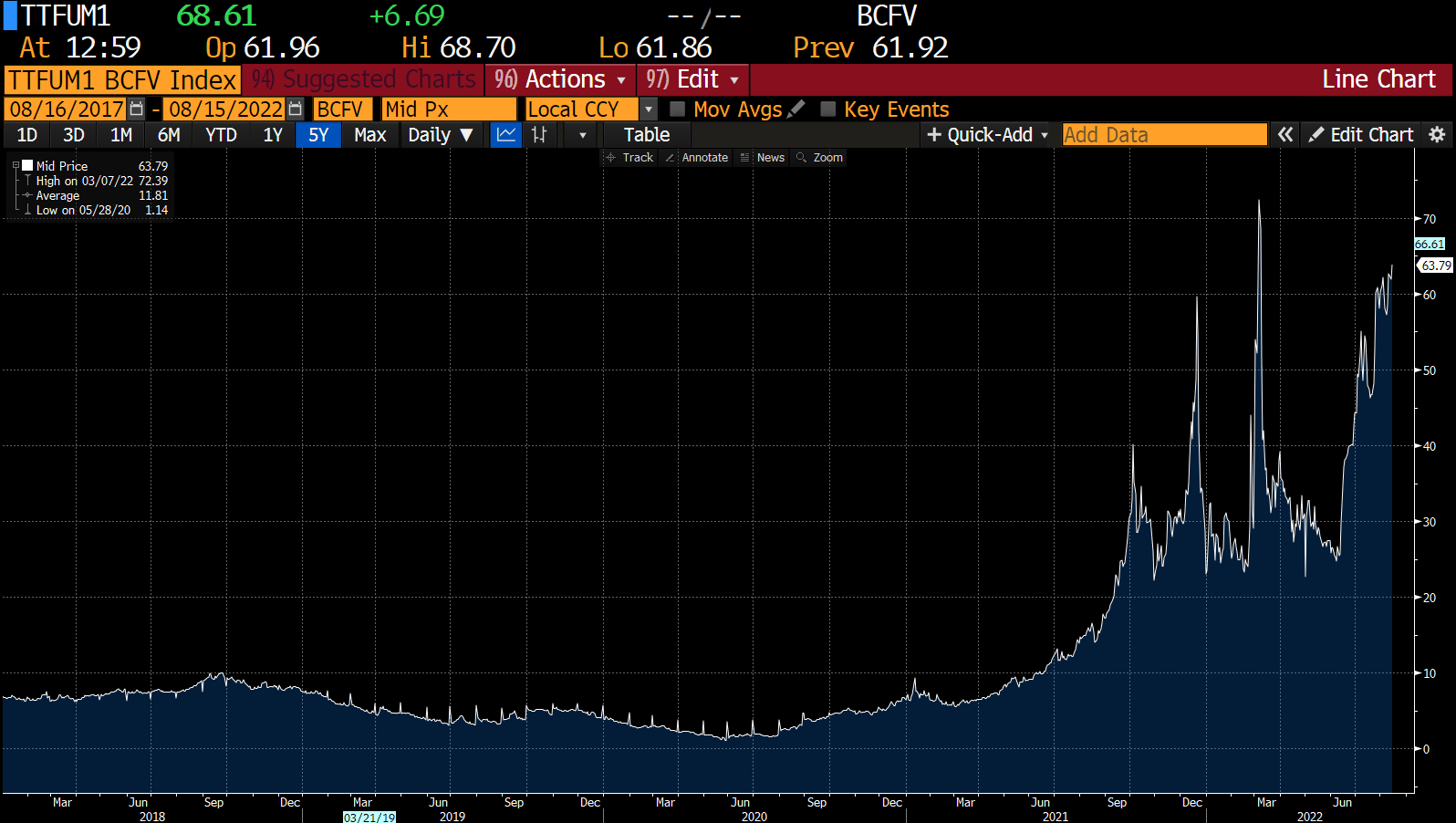

The stock selling off because of oil prices is pretty idiotic in my opinion. As I said in my last piece on the company, VET and Equinor (EQNR) are really the two main ways to play European natural gas shortages. That is still my view and while oil has come off its highs. European natural gas is near its all-time highs and has had outrageously firm seasonal performance (normally winter is the real bid season in Europe).

Dutch Forward Month Natural Gas Prices (Bloomberg)

This bet on VET will become even more important as the Corrib deal closes, which the company said to expect some time in Q4 (I was hoping for this quarter).

That is NOT to say that the company’s other assets are throwaways. North American natural gas prices are extremely firm too and frankly I think one would be hard pressed to find an oil executive who will complain about oil prices over $85/barrel. Just like EQNR, however, the magnitude of the cash flows coming from European natural gas is truly stunning and can permanently transform the balance sheet.

Risks

As we’ve seen the stock trades sensitive to WTI oil prices. The biggest risk in my mind though is a collapse of European or North American natural gas prices. Based on geopolitics right now, I don’t see that happening, but it has to be acknowledged. I suppose there is also the risk of production halts or difficulties. There were some this quarter in France and Australia, but those are temporary and usually pretty minor.

Conclusion

At less than 1 turn of leverage (on current EBITDA), tons of free cash flow generation, potential acceleration of capital return and possessing one of the most strategic fossil fuel assets in the world (Corrib), I think VET is one of the most interesting plays in energy right now. It’s of a size that could easily be acquired as well.

Be the first to comment