Mihaela Rosu/iStock via Getty Images

Thesis

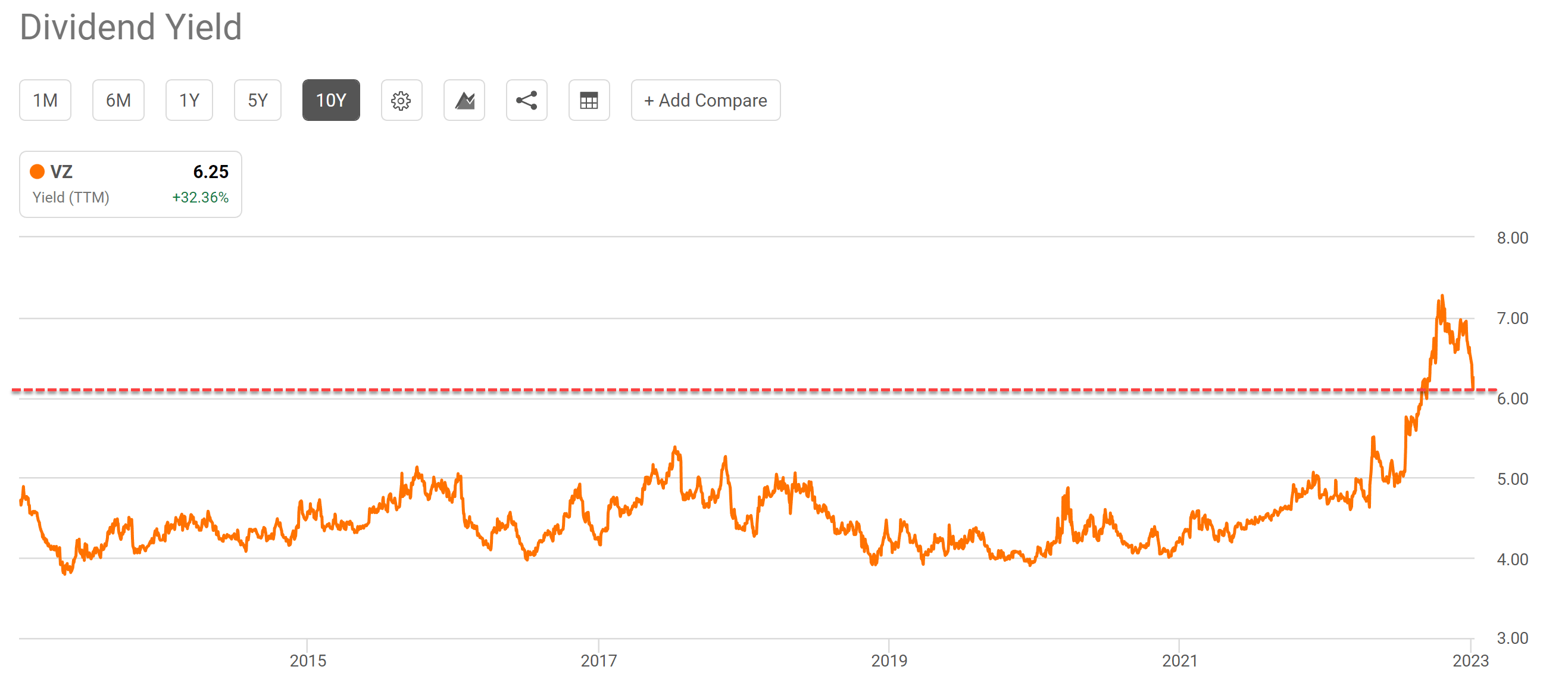

I have become bullish on Verizon (NYSE:VZ) and also have been holding its shares since its dividend yield surged above 6% last year. Currently, it is trading in a valuation range not seen in at least 10 years as you can see from the following chart. To wit, its current dividend yield sits around 6.25% on a TTM basis and 6.31% on an FW basis. Such a level of dividend yield is not only above its 4-year average (about 4.6%) by a whopping 37% but also among the highest level in a decade as seen. A bit later, we will confirm its valuation discount by other metrics as well.

Usually, when valuation discounts of such magnitude happen – especially for a staple stock like VZ, there must be serious red flags for dividend safety or balance sheet strength. However, in the case of VZ here, I see no such signs at all. What I see is peak dividend safety and balance sheet strength as to be elaborated on next.

Source: Seeking Alpha data

Valuation discount unseen in at least 10 years

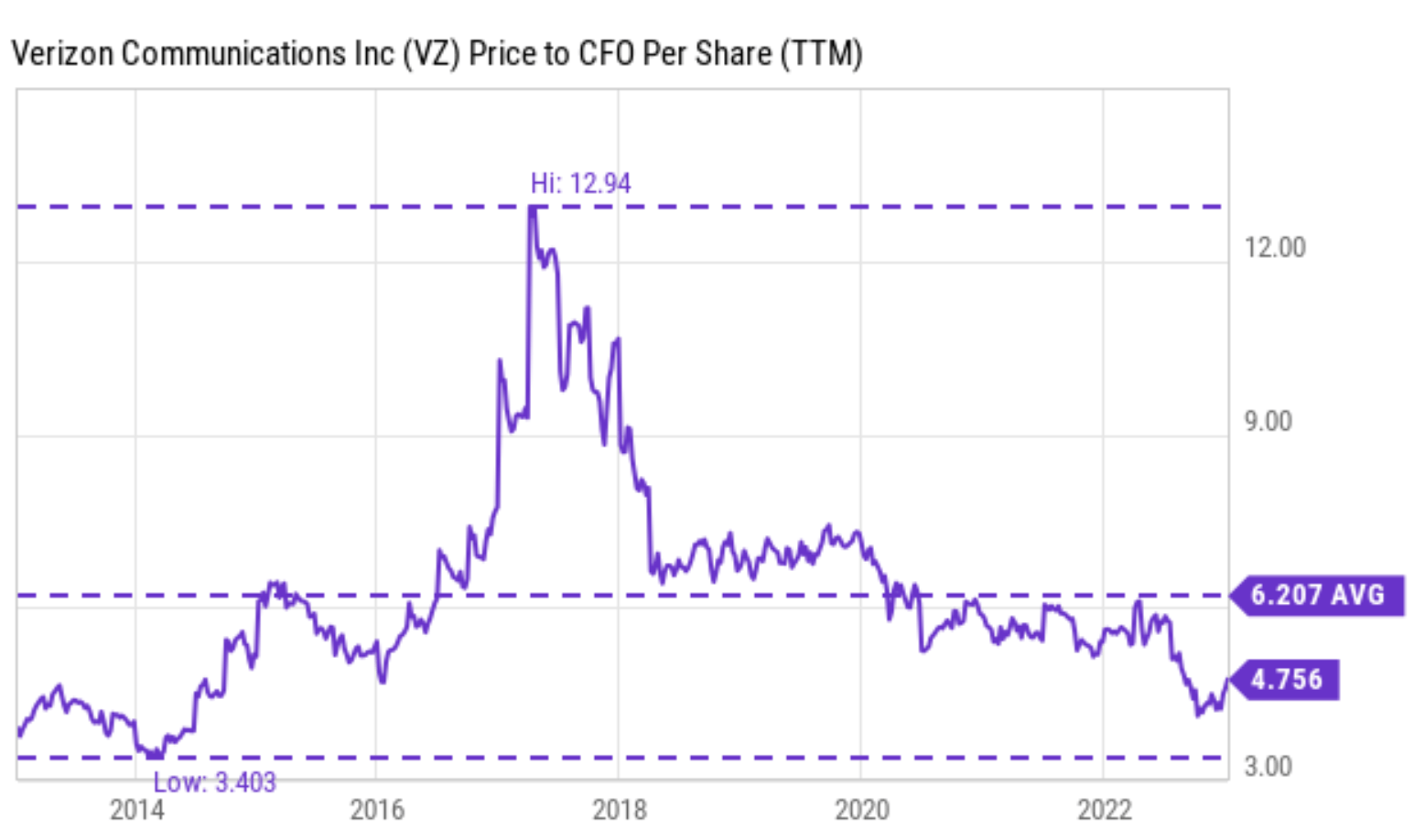

First, let’s quickly confirm its valuation discount by other metrics before we move any further just in case dividend yield paints a biased picture. The next chart shows its price to CFO multiple (cash from operations).

Currently, the P/CFO multiple for VZ is only about 4.75x. To further contextualize it under a historical perspective, the P/CFO ratio for VZ has fluctuated in the decade between a bottom of 3.4x and a peak of 12.9x with an average of 6.2x. Therefore, its current P/CFO ratio is not only cheap on an absolute basis, but also below its historical average of about 24%, consistent with the large discounts revealed by the dividend yield analysis above.

Now, as just mentioned, the next logical step is to examine if there are red flags that can justify such large valuation discounts.

Source: Seeking Alpha data

VZ’s dividend safety

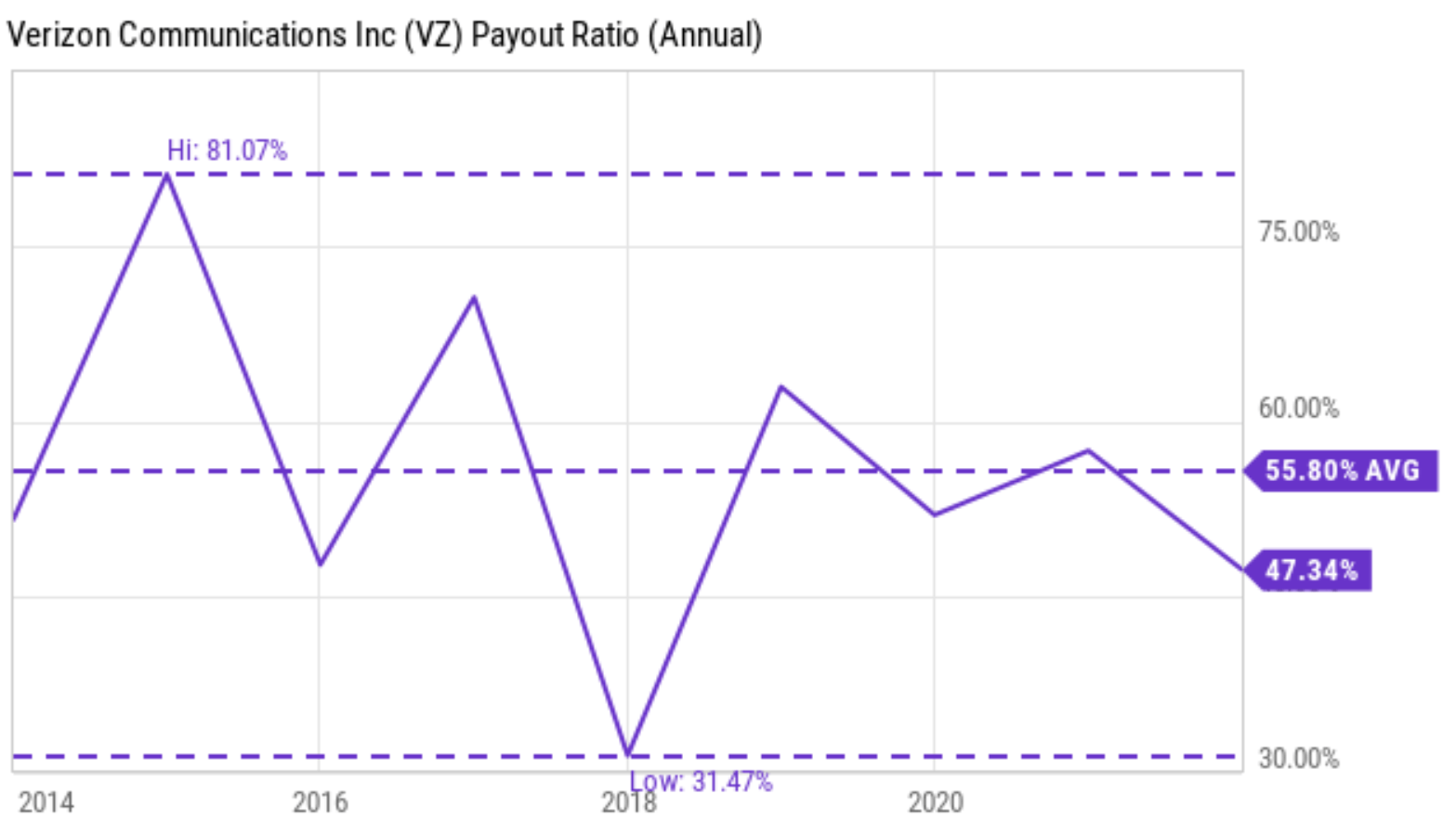

Let’s start with the obvious place for a staple stock like VZ: dividend safety. As illustrated from the next chart, its dividend safety is actually among the most conservative levels in a decade. To wit, its dividend payout ratio has been fluctuating in a range between about 45% to 70% most of the time in the past (if you ignore the few outlier data points). The long-term average payout ratio is 55.8%. Its current payout ratio hovers around 47.3%, not only far below its long-term average but also near the lowest end of the historical spectrum.

Looking ahead, thanks to its scale and pricing power, I expect VZ’s dividend safety and dividend raises to continue. And the management is also very committed to dividend safety and sustainability as confirmed by its CFO Matt Ellis in the recent Q3 earnings report. His comments were quoted below (slightly edited with emphases added by me):

Our guidance for 2022 remains unchanged. We are building momentum and remain confident that our strategy will deliver strong cash flow growth into the future. It is this confidence, combined with the health of our balance sheet, that enabled us to recently increase our dividend for the 16th consecutive year. We recognize the importance of the dividend to our shareholders, and we intend to continue to put the Board in a position to approve annual increases.

Source: Seeking Alpha data

VZ’s balance sheet strength

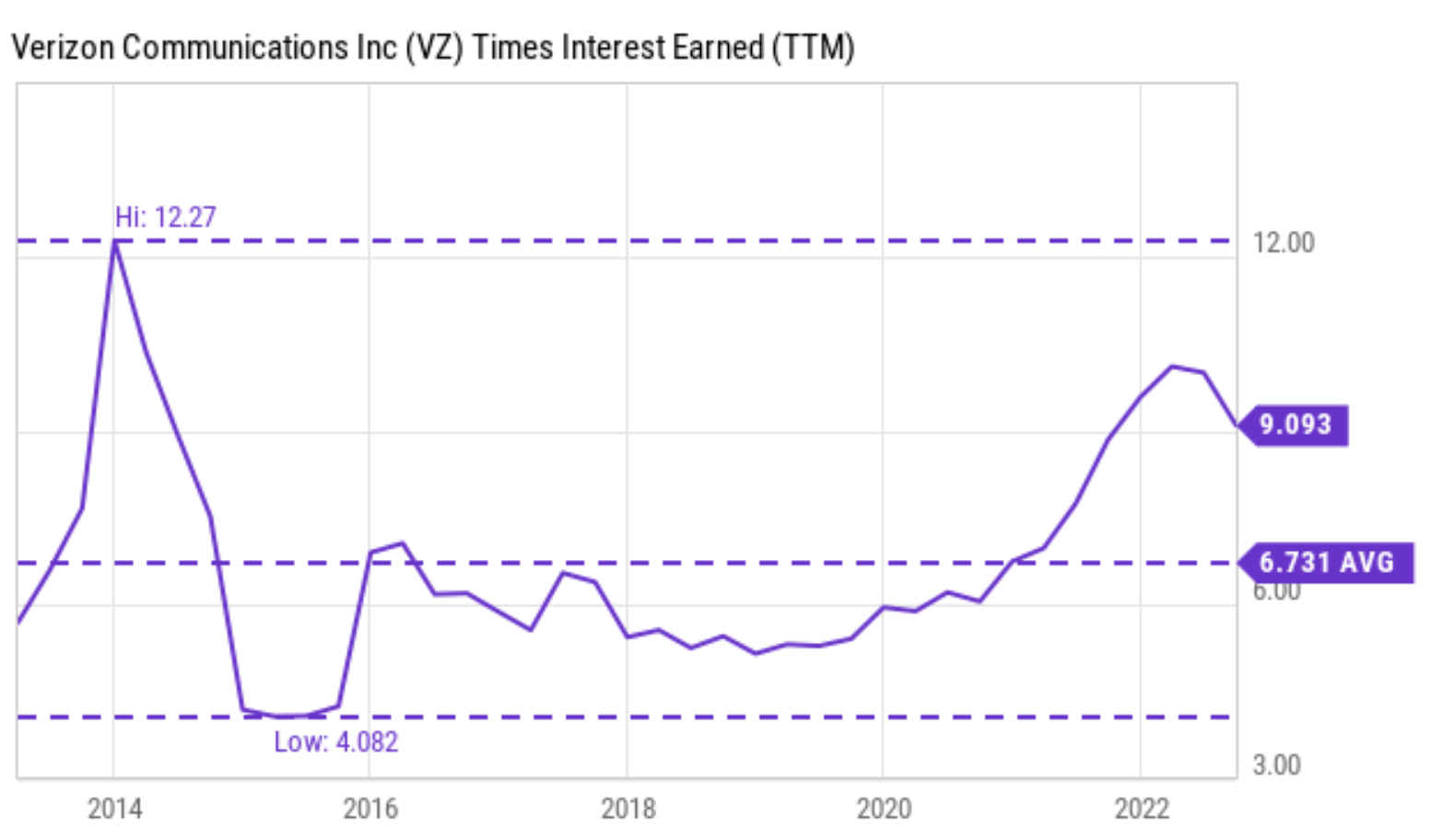

The CFO’s above comments also naturally leads me to the next item to check: its balance sheet. And I am not seeing any signs of balance sheet deterioration. On the opposite, its balance sheet now boasts the strongest position in a decade also as you can see from the interest coverage ratio data below. In the past 10 years, VZ’s interest coverage (in terms of Times of Interest Earned) has been quite stable between a range of 5x to about 10x with an average of 6.7x. The current coverage is at 9.09x, again not only far above its historical average but also near a peak level in a decade. VZ ended the September interim with a healthy cash position (with ~$2.1 billion in cash on its ledger) and a sizable debt reduction. Its long-term debt sits around $132.9 billion, down from $143.4 billion a year ago.

Source: Seeking Alpha data

As such, going forward, I see the company well-positioned to not only keep raising its dividend payout but also make additional acquisitions. And indeed, management has made it clear that it is committed to enhancing VZ’s strategic capabilities and its multi-spectrum assets. And the latest comments from CEO Hans Vestberg (made during the 2022 Q3 earning report) on these strategies are quoted below. These comments are again sightedly edited with emphasis added by me. VZ has been pursuing these strategies for several years, and I share management’s view that is working.

Our mission has always been to build and operate the best, most reliable, highest performing network. Our use of advanced technologies, our spectrum portfolio and our expansive own fiber footprint, are critical to achieving that goal. Where we deploy our C-band, we see direct correlation to customer growth on both mobility and fixed wireless access.

… we are confident about the strategy, and it’s working. We have talked about for several years. We come out with new products, that’s going to be multi-spectrum. That’s going to handle everything from 4G, C-band, 10-millimeter wave. So the resilience and the performance and quality of the products is even getting better.

Risks and final thoughts

In terms of risks, as a popular stock, VZ’s risks have been thoroughly discussed by many other SA articles including my own articles.

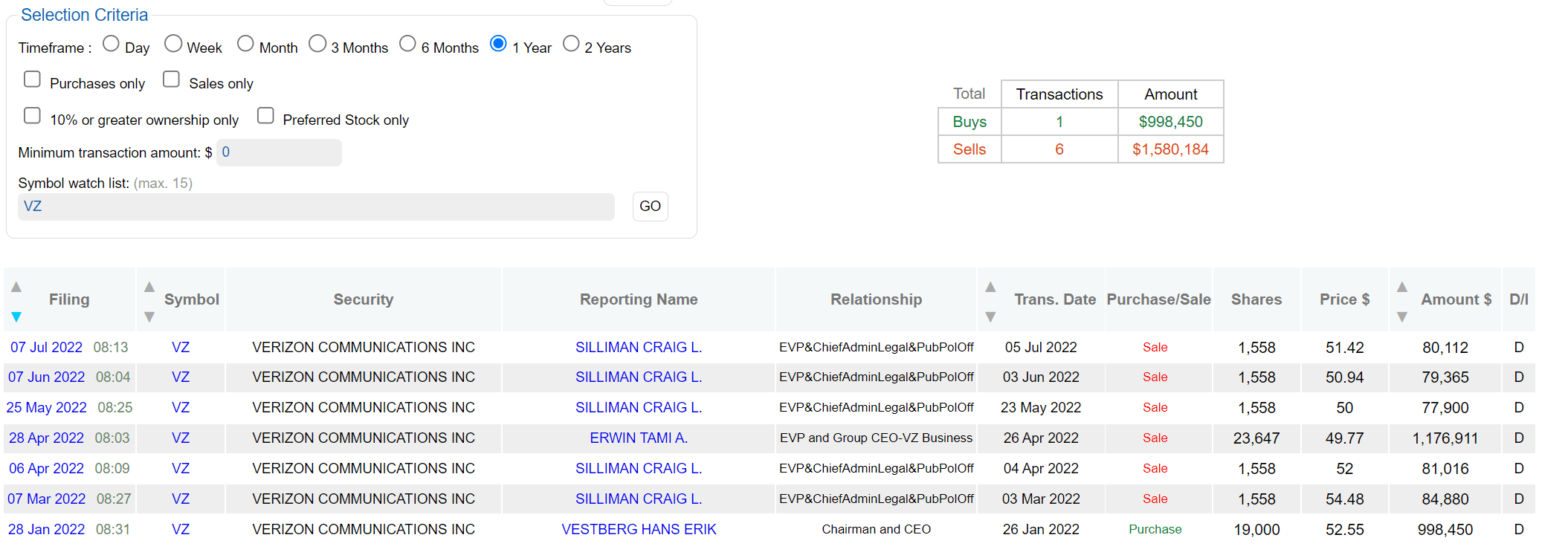

These risks include macroscopic risks such as interest rate hikes, competition risks, and also the heavy capital investment involved in the telecom space. I won’t further add to these topics anymore here. Instead, let me point out something that is less often discussed: the inside activities. As seen in the following chart, in the past year, VZ’s inside activities have been dominated by two transactions only: a large purchase from its CEO in January 2022 (with a total sum of around $1M) and a large sale by one of its EVPs in April of 2022 (also with a total sum of $1M). Such opposite insider actions could signal some divergence of opinions among its senior management. Although I myself usually pay more attention to insider buying and less attention to selling. Buying has one explanation only: the buyer is bullish on the stock. But selling can be triggered by many other reasons.

Source: Dataroam.com data

To conclude, the market is overthinking the VZ case in my view. The current dividend level and valuation discounts are suspiciously large for a stable dividend stock like VZ. However, when examined closely, I do not see any red flags to be suspicious of. What I see are the opposite: peak dividend safety, good prospects for continued dividend raises, and peak balance sheet strength.

Be the first to comment