DouglasOlivares/iStock via Getty Images

Back in October, Verastem (NASDAQ:VSTM) updated investors on their RAMP clinical trials for recurrent low-grade serous ovarian cancer “LGSOC”, KRAS G12V-Mutant non-small cell lung cancer “NSCLC”, KRAS G12C-mutant NSCLC, and frontline metastatic pancreatic cancer. The update was not entirely positive, with the company reporting that the combination of avutometinib and defactinib “did not meet the pre-defined criteria to continue in the RAMP 202 trial.” In response, the market hammered VSTM down roughly 70% and is now trading around $0.40 a share with a market cap of around $84.5M. It appears as if the market believes the RAMP 202 data is indicating that avutometinib might be a dud in NSCLC, and might not be as operative in other cancer types. Admittedly, I was disappointed with the update and decided to mothball my VSTM until fresh data can revitalize my thesis. However, I will consider adding to my position for a potential snap-back reversion trade if the conditions arise.

I intend to provide a brief background on Verastem and its pipeline programs. Then, I review the company’s update on their RAMP trials and the lackluster RAMP 202 data. In addition, I will discuss why I mothballed my VSTM position and will attempt to highlight some key downside risks that investors need to consider when managing their VSTM position. Finally, I will take a look at the company’s valuation and charts to see if I can find any signs of a turnaround or buying opportunities.

Background on Verastem

Verastem Oncology is a biopharma company that focuses on the development and commercialization of small-molecule drugs for the treatment of cancer. Their pipeline drugs attempt to inhibit critical signaling pathways that stimulate cancer cell growth and survival. At the moment, the company is focusing on RAF/MEK inhibition and focal adhesion kinase “FAK” inhibition.

Verastem Oncology Pipeline (Verastem Oncology)

Avutometinib (VS-6766) is an RAF/MEK clamp that attempts to create maximal RAS pathway inhibition involving MEK with ARAF, BRAF, and CRAF theoretically improving the anti-tumor response. avutometinib is unique to other MEK inhibitors due to its ability to block both MEK kinase activity and RAF’s ability to phosphorylate MEK, but with the compensatory activation that is seen in other MEK inhibitors.

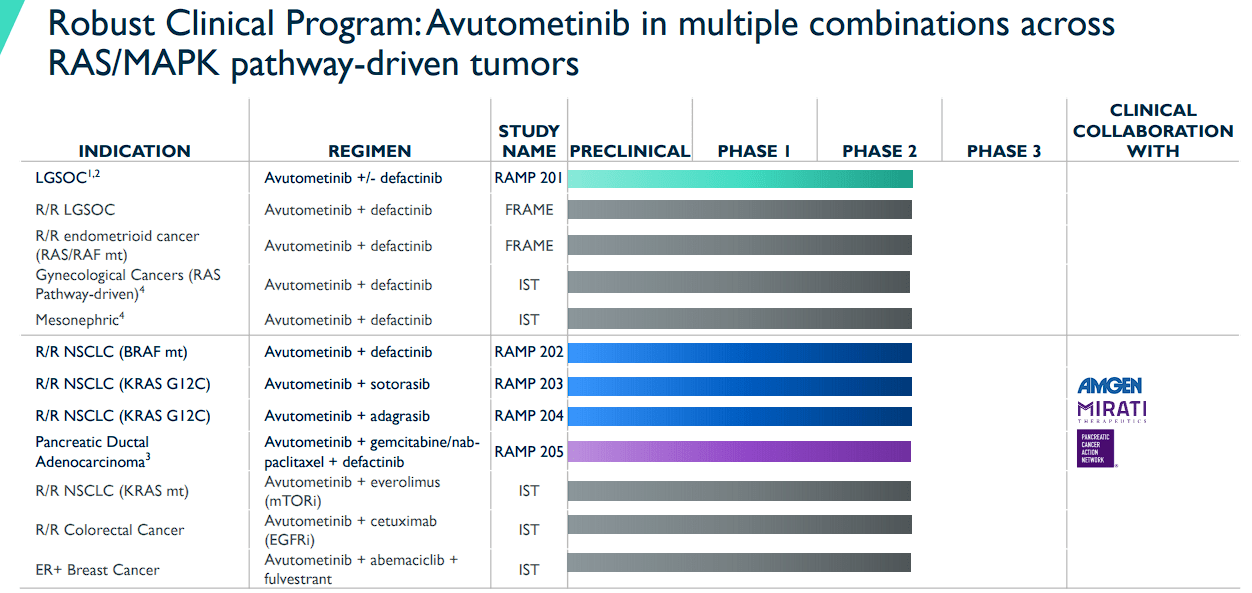

Verastem Oncology’s Raf And Mek Program “RAMP” is currently conducting clinical trials with avutometinib and defactinib. RAMP 201 is a registration-directed trial of avutometinib alone and in combination with defactinib in recurrent LGSOC. The FDA granted Breakthrough Therapy designation for the combination in LGSOC regardless of KRAS status after one or more prior lines of therapy, including platinum-based chemotherapy. The RAMP 202 trial is for the combination of avutometinib and defactinib to treat KRAS G12V NSCLC.

Verastem Oncology does have partnered RAMP programs with clinical collaborations with Amgen (AMGN) and Mirati (MRTX). Verastem is combining Amgen’s LUMAKRAS and avutometinib in KRAS G12C mutant NSCLC in the RAMP 203 program. In addition, they are employing adagrasib in combination with avutometinib for KRAS G12C mutant NSCLC in RAMP 204. Verastem Oncology is working with the Pancreatic Cancer Network “PanCAN”, in RAMP 205 to test avutometinib and defactinib with gemcitabine/nab-paclitaxel in front-line metastatic pancreatic cancer.

Regarding IP, the company has patent coverage for avutometinib alone up to 2038, and 2040 in combination with defactinib.

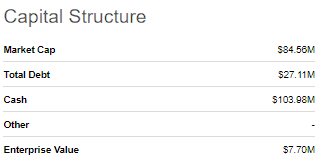

In terms of cash, the company finished Q3 with about $104M in cash, cash equivalents, and investments with about $27M in debt.

Verastem Oncology Capital Structure (Seeking Alpha)

The company’s market cap is roughly $84.5M with an enterprise value of around $7.7M.

RAMP 202 Falls Short

As I mentioned in the introduction, Verastem provided a mixed update to investors on some of their RAMP programs. The big concern was from the company’s Part A data from the RAMP 202 trial with the combination of avutometinib and defactinib for KRAS G12V NSCLC. The company reported 11% ORR (2 of 19) with a disease control rate of 37% in KRAS mutations. The ORR with non-G12V KRAS mutations was 5% with a disease control rate of 54%. This data revealed that the combination “did not meet the pre-defined criteria to continue in the RAMP 202 trial.” Verastem intends to present the Part A results at an upcoming medical congress.

An 11% ORR and a 37% disease control rate is not what the market was hoping for from this combination. Indeed, the data did show that the combination did perform better in the KRAS population vs. non-KRAS, so there is some hope the company will be able to find an opportunity for this combo. However, the lackluster data appears to have cast a shadow over the RAMP programs and avutometinib.

RAMP 201 In LGSOC Is Still A Go

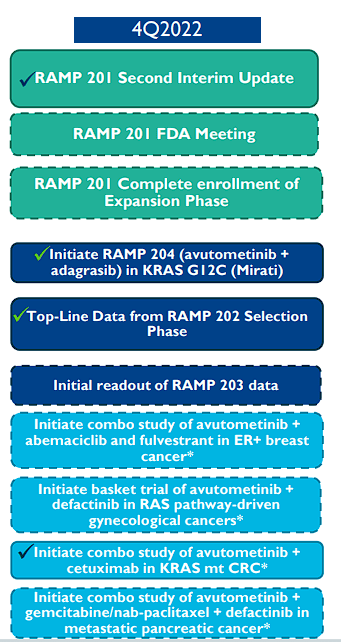

Verastem also reported the results of a second planned interim analysis for RAMP 201 trial for recurrent LGSOC. The trial is ongoing with all four cohorts of avutometinib alone and in combination with defactinib in KRAS mutant and KRAS wild-type patient populations. Verastem expects full enrollment by the end of 2022 and plans on meeting with the FDA in Q4 of 2022 about a regulatory path forward.

The company did provide any data points because the study is still ongoing, however, the company’s decision to keep pressing forward with the FDA does suggest they are seeing some promise from at least one of the cohorts. Hopefully, we will get an update after the meeting with the FDA about the timing of a potential data readout.

RAMP 203 and RAMP 204 in KRAS G12C-Mutant NSCLC Are Still Intact

Verastem has two partnered RAMP programs that are targeting KRAS G12C-mutant NSCLC. RAMP 203 is in a Phase I/II trial of avutometinib in combination with Amgen’s KRAS G12C inhibitor LUMAKRAS. The company expected the initial results in Q4 of 2022. The RAMP 204 Phase 1/2 trial is open and enrolling of avutometinib and Mirati’s adagrasib “Krazati”. This study is expected to determine the maximum tolerated dose and the optimal dose to be used in the Phase II dose.

The partnered programs could be critical for avutometinib development and possibly its meal ticket to getting on the market considering both drugs are already approved. It would be a big win for Verastem if data shows that the addition of avutometinib to these drugs improves outcomes. We should see initial data from RAMP 203 in the first half of this year.

Eyes On RAMP 205 in Frontline Metastatic Pancreatic Cancer

Verastem is partnering with PanCAN to test avutometinib with defactinib in frontline metastatic pancreatic cancer. RAMP 205 is a Phase Ib/II clinical trial of avutometinib with defactinib in addition to gemcitabine/nab-paclitaxel regimen. The company planned to open RAMP 205 in Q4 of 2022.

This trial could be a game changer if avutometinib with defactinib is able to blockade KRAS signaling, which is “mutated in more than 90% of pancreatic cancer tumors.” If the avutometinib with defactinib combination can improve the standard of care, Verastem might have one of the most important developments in pancreatic cancer treatment in recent history.

Mothballing VSTM

Regrettably, I decided to put my VSTM position following the sell-off due to some concerns that avutometinib could be a dud. I was expecting the RAMP 202 data to show much better results in the KRAS population, but the data was disappointing. Typically, I would take the contrarian approach and focus on the trading opportunities that follow an overblown sell-off, but the current market conditions are not favorable for this method. So, my VSTM position is currently sitting in mothballs and is out of the Compounding Healthcare “Bio Boom” Portfolio for the time being.

Make note that I did not sell my position because I still believe there is a possibility that future data readouts vindicate avutometinib. Therefore, I will keep an eye out for company updates and will consider reviving the position and adding it back to the “Bio Boom” Portfolio.

Verastem Oncology Pending Q4 Updates (Verastem Oncology)

Downside Risks

Like most small-cap speculative healthcare tickers, VSTM has multiple downside risks that investors need to consider when handling their positions. First, Verastem has significant regulatory risk at this point in time. As I mentioned above, avutometinib needs to prove it is operative and can be deployed across a broad range of KRAS cancer types. Failure in one or more programs would most likely have a prolonged impact on the share price.

Another concern is the company’s cash position, which is healthy at this time. However, we have to anticipate that the cash position will decrease in the coming quarters and years as the company attempts to move their pipeline into larger trials. It is possible that the company will have to perform some form of dilutive funding or take on additional debt to keep the pipeline moving and the lights on.

Investors also need to consider there is a strong likelihood the company will have to perform a reverse split to get the share price back above $1.00 per share in order to maintain their NASDAQ compliance. It is possible the company could report positive data that could rally VSTM above $1.00, but the high volume of trading occurring at these current levels might keep the ticker stuck in the mud. A reverse split by itself is not the issue… but the reduced number of shares often makes a stock a target for short sellers trying to cut the share price down through a thin order book on low volume. Once in a while, it works in the other direction, but investors should see a reverse split as a negative event in the immediate term.

Overall, VSTM is a very speculative ticker at this time. Therefore, I am lamentably assigning the ticker a conviction level of 1 out of 5.

Finding An Opportunity

I might not be looking to take my position out of mothballs, but that doesn’t mean that there isn’t an opportunity for investors to manage or possibly initiate a VSTM position. I would like to point out that VSTM is trading with an enterprise value of ~$7.7M, so the ticker is not trading at a premium valuation. In fact, VSTM is trading at a 1.3x price-to-book, which is under the sector median of roughly 2x. Therefore, one could say that VSTM is trading at a slight discount for its current intrinsic value. Then, if you consider the company’s potential future revenue and growth, we could say VSTM is trading at a heavy discount.

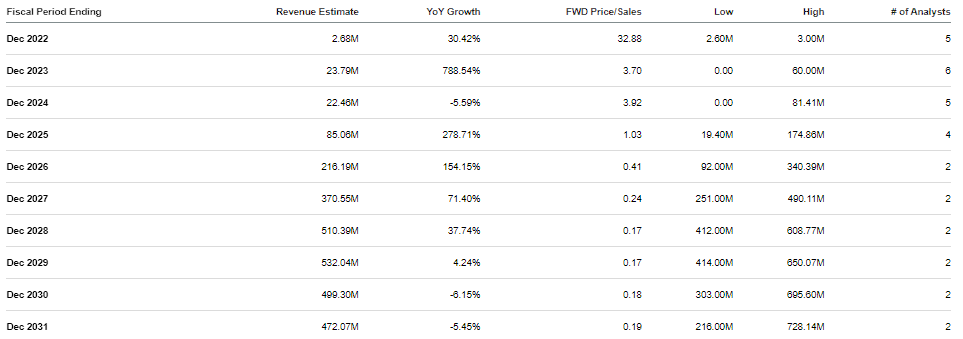

Verastem Revenue Estimates (Seeking Alpha)

The Street expects Verastem to report strong double-digit and triple-digit growth over the next several years. Indeed, these estimates obviously rely upon the company getting multiple programs on the market, so these projections are speculative. However, these revenue estimates do illustrate how Verastem could go from pulling just over $2M to over $200M in just five years, which would be a roughly 0.4x forward price-to-sales. The industry’s average is about 4x-5x, so $200M in revenue would justify VSTM trading at $4-$5 per share in several years. Therefore, we can say VSTM is trading a heavy discount for its potential future revenue… IF everything in the clinic and on the market works out.

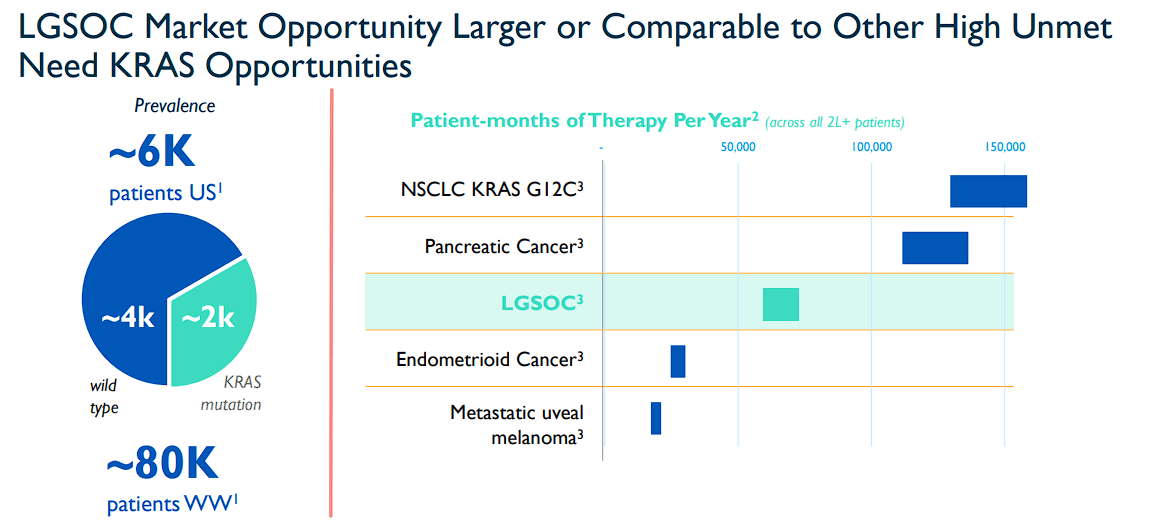

I will point out… at an $84.5M market cap, VSTM would probably only need one of their current pipeline programs to justify a higher valuation. That is something to consider even if some of the pipeline programs do fall short. RAMP 201 in LGSOC is still in play and has a substantial market to keep VSTM in play for the foreseeable future.

Verastem Oncology LGSOC Opportunity (Verastem Oncology)

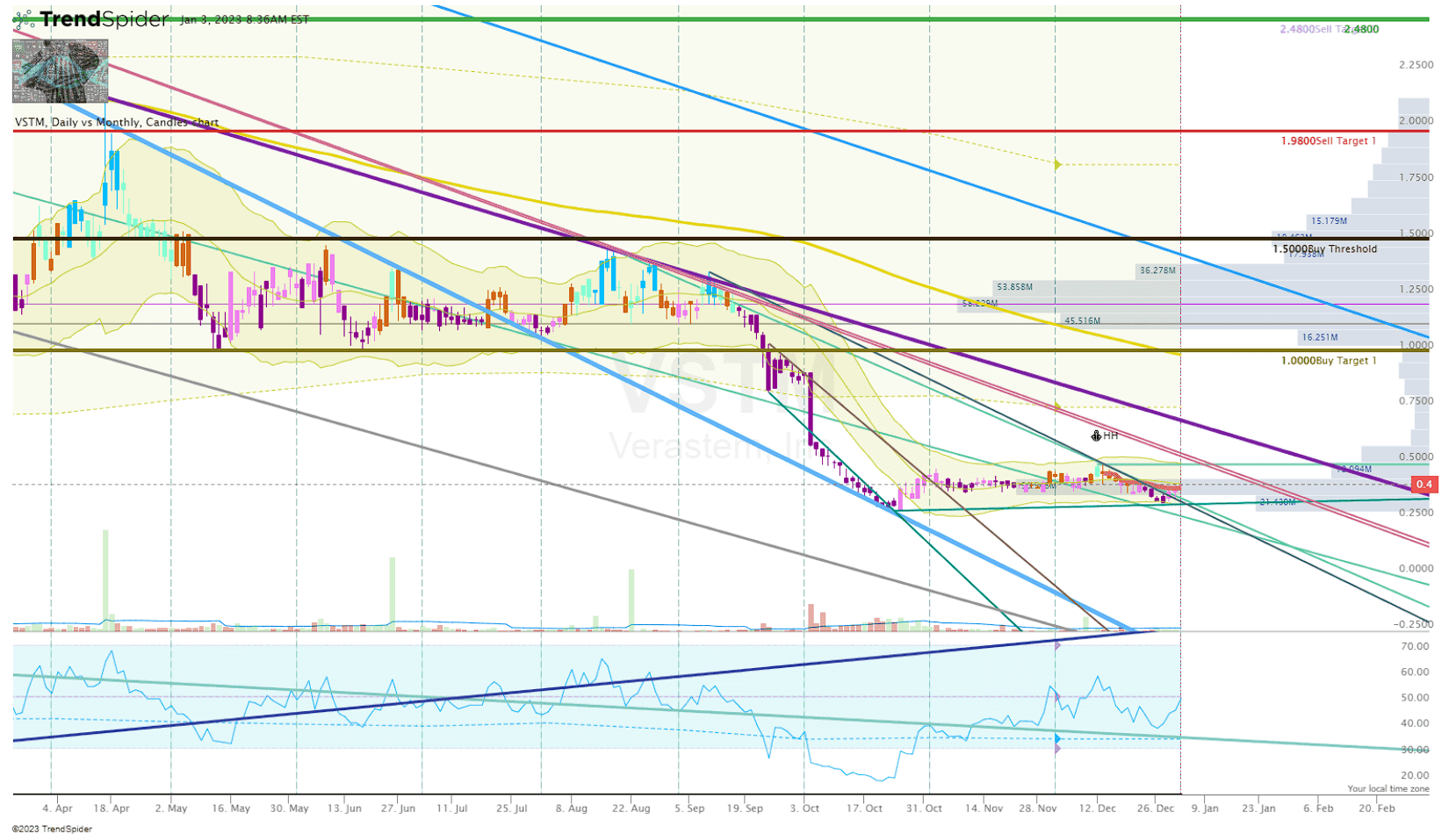

So, one could say that VSTM offers a solid opportunity if you are looking for a speculative investment with substantial upside. Looking at the charts, I would say that a discounted opportunity might be dissipating as the share price continues to “base” and squeeze out of some notable downtrend rays.

VSTM Daily Chart (Trendspider)

A break above $0.50 could trigger a snap-back move inside the monthly Keltner Channel up to potential resistance of ~$0.70, or possibly $0.80. Indeed, a move from $0.40 to $0.80 is not what longstanding VSTM investors want to hear, but it could be a great trading opportunity for those who have been accumulating at these prices.

Then again, the share price could continue to experience selling pressure, especially if the company’s next data readout is lackluster. VSTM is a true speculative play at this time.

Personally, I am sticking to the sidelines with my dormant position at this time. However, I will keep a close eye on the company and the ticker over the first half of 2023 for signs of a turnaround.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment