Rex_Wholster

The launch of recreational cannabis sales in Connecticut got limited attention from the stock market due to the market focus on the wrangling in Congress over the SAFE+ banking bill. Verano Holdings Corp. (OTCQX:VRNOF) is a sneaky way to play the market opportunity in the state as the Connecticut license structure turns off aggressive investors. My investment thesis remains ultra-Bullish on a cannabis space thrown away by the market in late 2022 due to political issues not impacting the true value of businesses over time.

Connecticut Launch

The Connecticut market launched on January 10 with 9 retail stores open, including the Zen Leaf Meriden dispensary from Verano. As with New York, the regulators have tried to shift the market focus away from the multi-state operators (MSOs) to social equity retail licenses.

The problem the states will face is that current funding is limited and social equity license winners aren’t necessarily equipped to operate competitive retail locations. As a medical cannabis license holder, Verano will be able to supply wholesale product from the CTPharma 217,000 square foot cultivation and processing facility along with eventually open up recreational sales at the Caring Nature dispensary in Waterbury.

On the Q3’22 earnings call, CEO George Archos specifically discussed the opportunity in the wholesale market in Connecticut:

We’re one of the largest wholesalers currently in the state. We brought in some additional supply. We also will be opening some additional retail services and JV structures. So we’re anticipating pretty good wholesale growth and retail growth in Connecticut.

From a timing perspective, we’ll see should happen in the pretty near-term. So it will probably be mostly wholesale growth as we continue to build out and find these new store locations. But we’re excited about CT. It’s a pretty tight market. And we traditionally, CTPHARMA has done very well there, and we anticipate good growth in that market.

The Connecticut regulator is reviewing 100s of retail licenses setting up a scenario where retail stores lack supply. None of the additional cultivation licenses appear ready with product and the current capital situation in the sector works in the favor the MSOs with existing cultivation assets.

In fact, the one cultivator that isn’t a major MSO is struggling financially. Greenrose (OTC:GNRS) went public via a SPAC in late 2021 with the acquisition of Theraplant, LLC in Connecticut and the company is struggling financially. A recent SEC filing disclosed the company missed a quarterly financial reporting deadline, broke credit agreements and needs “substantial additional capital” to fund ongoing operations.

The Connecticut market was recently estimated by MJBizDaily with a market size of up to $800 million by 2026. The problem facing these new recreational cannabis markets trying to bypass the large MSOs is the lack of capital in the cannabis space after every investment over the last few years failed miserably. The issues with Greenrose highlight the problem in the sector that are providing Verano with a clear path to being a leader in the wholesale space.

Priced For Disaster

Despite another Northeastern state launching a recreational cannabis program with Verano having only 1 of 9 stores open on launch, the stock has fallen all the way to $3. The MSO now has a market cap of only $1 billion while the 2023 sales target is a similar $1 billon.

The market has pretty much ignored the opportunities ahead in the cannabis space as competition should die down just when states like Connecticut and New York plan to open up recreational sales with 100s of retail licenses.

Verano’s reported Q3’22 revenues increased 10% to $228 million, making the MSO one of the largest in the cannabis space. The company is very profitable on an adjusted EBITDA basis, with $82 million in the quarter on 36% margins.

The MSO now has operations in 13 states with 120 dispensaries and 14 cultivation and processing facilities. Verano is cash flow positive from operations, but the MSO plans to spend anywhere from $25 to $50 million on capital spending in 2023.

Verano Holdings Corp. stock only trades at 1x sales versus other MSOs still maintaining P/S multiples closer to 2x. Verano is difficult to value, but the company appears a winner in a market sure to consolidate where possible with social equity license holders unlikely able to prosper without the necessary funding in a difficult time.

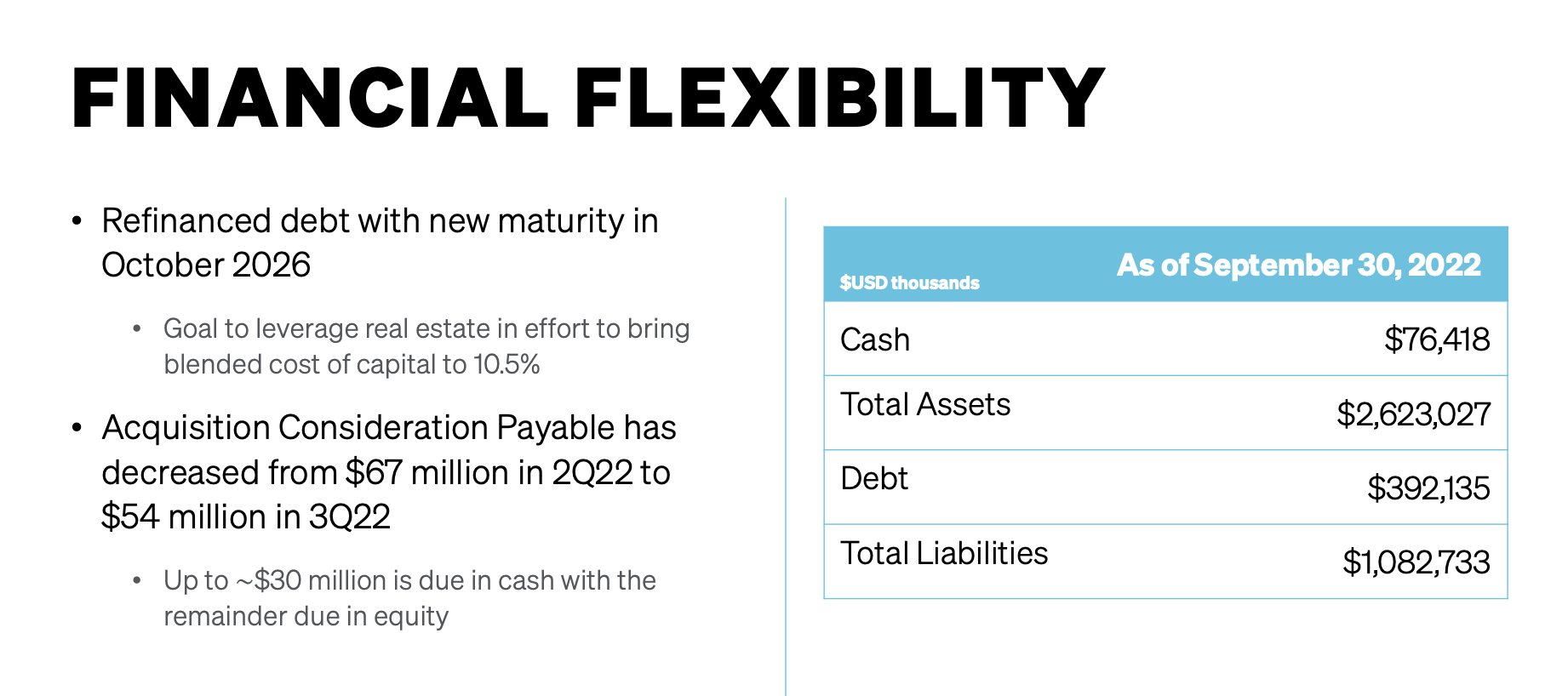

As with other MSOs, the company now has a net debt position from building up retail and cultivation assets in multiple state markets. Verano has a net debt position of over $300 million, but the cannabis company has over $530 million in PP&E and has leverage position below 1x adjusted EBITDA targets.

Source: Verano ’23 ICR presentation

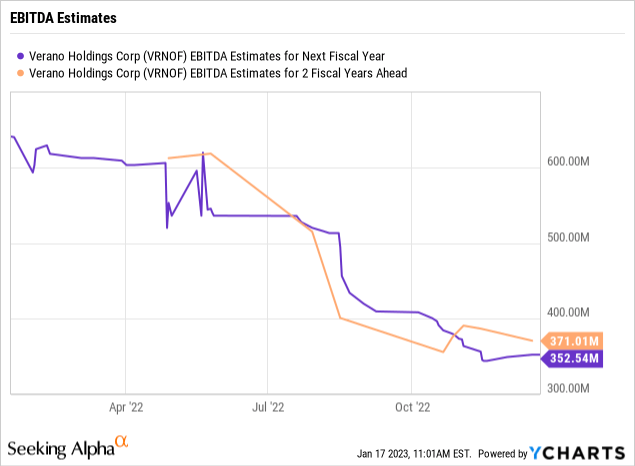

While the new recreational cannabis markets in the Northeast aren’t opening up as friendly to the MSOs as expected, Verano is far too cheap trading at a forward EV/EBITDA multiple of only 4x.

Takeaway

The key investor takeaway is that Verano Holdings Corp. is another cheap MSO. The whole sector has been crushed due to delayed approvals of cannabis by Congress, but investors need to focus more on the expanding market opportunity.

Verano Holdings Corp. is too cheap based on sales and EBITDA targets knowing the Connecticut market is likely to favor the MSOs over time.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment