peterschreiber.media

Investment Summary

We continue expanding our specialist healthcare, med-tech, and biotech investment universe by identifying selective opportunities positioned at multiple points along the treatment paradigm. Our recent follow-up publications on EDAP TMS S.A. (EDAP) and Profound Medical Corp. (PROF) [see: here, and also here] reinforced our bullish theses in the prostate cancer treatment paradigm. Extending from this, it is prudent to share observations we made from our concurrent analysis of Veracyte (NASDAQ:VCYT). With the stock trading at 1.75x book value and 5.7x forward sales, we believe this is still expensive relative to other names in the sector. Net-net, we opt to rate VCYT neutral until we have more clarity from its upcoming FY22 numbers.

Added exposure to prostate cancer and BPH diagnosis, prognosis

Our theses on PROF and EDAP concentrate on procedural modalities to address the nexus between prostate disease [either prostate cancer or benign prostatic hypertrophy (“BPH”)]. Both are meaningful differentiators from the current standard of treatment and care, where post-operative outcomes are typically poor for patients.

In this vein, it should be known there are inherent difficulties in the accurate diagnosis of both conditions, notwithstanding the ability to differentiate between benign and malignant versions of the lesions. One of the major hurdles in accurately diagnosing prostate cancer is the lack of specificity of existing diagnostic modalities, such as prostate-specific antigen (“PSA”) testing, and digital rectal exams (“DRE”). The PSA test, despite its widespread usage, has a relatively low positive predictive value [21-30% in various studies] and often results in false-positive results. Furthermore, the PSA test is not capable of differentiating between BPH and clinically significant prostate lesions. Similarly, the DRE, although useful in detecting prostate enlargement and abnormalities, is highly subjective and can be influenced by patient and operator factors. Moreover, its predictive value is mostly seen in symptomatic patients.

Another challenge in accurately diagnosing prostate disease is the heterogeneous nature of the disease itself. Prostate cancer can present in various forms, ranging from indolent, slow-growing tumors to more aggressive, rapidly growing lesions. This variance in presentations can make it challenging to determine the appropriate diagnostic approach, particularly in the case of low-risk prostate cancer, where active surveillance is a viable option.

Finally, biopsy accuracy is a significant concern in the diagnosis of prostate cancer. The current standard of care, transrectal ultrasound (“TRUS”) guided biopsy, can miss clinically significant prostate cancer when used on its own, particularly in the peripheral zone where the majority of prostate cancers arise. Data on its accuracy varies, yet ranges from 39%-75% in various publications. Furthermore, the inter-observer variability in biopsy interpretation and the potential for sampling error further complicates the accuracy of biopsy results, although this isn’t unique to TRUS imaging.

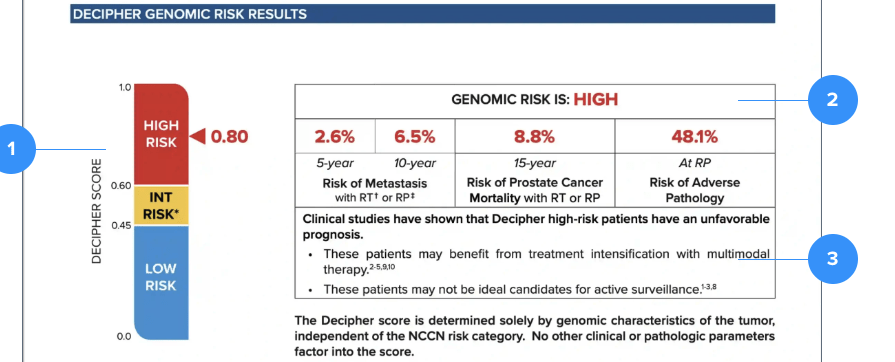

This is where we are attracted to VCYT’s offerings in this domain. In particular, the Decipher prostate biopsy (“DPB”) and Decipher radical prostatectomy (“DRP”) are diagnostic modalities employed in the identification of prostate cancer. Collectively, they form VCYT’s Decipher prostate genomic classifier. VCYT acquired Decipher Biosciences in FY21′ on a $600mm, and we believe this is a long-term cash compounder for the company. It is a 22 gene, whole-transcriptome-developed test that puts out a ‘Decipher score’ out of 22, to provide risk estimates and specific outcomes. Net-net, it provides clinicians and patients with distinguishing guidance to identify what patients are candidates for surgery, active surveillance, or combined therapy. DPB involves obtaining a tissue sample from the prostate gland through a biopsy needle to be analyzed for the presence of cancerous cells. The procedure typically employs TRUS guidance to visualize the prostate and locate the area of interest. It is well supported in over 75 studies reliability studies and does indeed outperform standard markers like PSA.

Snapshot of DPB, retrieved from Decipher Bio

Data: Image retrieved from Decipher Bio website, see: “Decipher Prostate Biopsy”

VCYT reported >11,000 DBP tests in Q3 FY22, a double-digit sequential growth, helping drive total testing revenue for the quarter to $64.6mm. We were pleased to see that management foresee headroom in the marker for the Decipher platform. Management also increased full-year guidance for total revenues to $293mm at the upper end of range, calling for 33% YoY growth at the upper end of range. We will be heavily scrutinizing these numbers when the company is due to report at the end of this month.

Valuation and conclusion

Profitability is a key issue to recognize in the current macro-landscape where investors are rewarding profitable names with higher multiples versus their unprofitable counterparts. We’d note the stock is trading at ~5.7x forward sales and 1.75x book value. Depending on one’s time horizon, these could be attractive or not. Assume a 5-year horizon, we’d need to see VCYT’s top-line 5x in growth over this time to justify a fair valuation at this multiple today. Question being, can it get there? We believe it can achieve this kind of growth. However, its upcoming FY22 earnings will be the major telling point, and so we are looking forward to providing further clarity after its numbers.

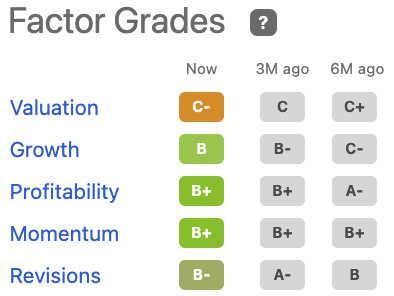

Despite the optimism discussed in our analysis, quant gradings around its valuation are a concern. The stock hasn’t been rated highly with Seeking Alpha’s quant factor grades in this domain, as it expensive relative to the sector. Shares would need to pull back to a more reasonable range to trade at ~4.2x forward sales to be in line with the sector.

Exhibit 1. VCYT Seeking Alpha factor grades – average grade for valuation

Data: Seeking Alpha, VCYT, see: “Factor Grades

Net-net, we are constructive on VCYT, but shares look to be expensive at this point in time without further earnings data to work by. We are opting to remain neutral heading into its FY22 earnings and look forward to providing additional coverage afterwards.

Be the first to comment