imaginima

After seeing a 340% rally in total return terms from the Covid lows, the Vanguard Energy ETF (NYSEARCA:VDE) has closed most of its valuation discount. I still expect the VDE to outperform over the coming years as it continues to trade at a discount to the SPX. However, the high degree of volatility and exposure to global economic weakness suggests caution is warranted at present.

The VDE ETF

The VDE seeks to track the performance of MSCI US Investible Market Energy Index. The VDE is slightly more diversified than the larger Energy Sector Select SPDR ETF (XLE), which tracks the S&P500 Energy Sector. The two largest companies, Exxon (XOM) and Chevron (CVX), comprise 38% of the index versus 42% for the XLE. Meanwhile, the top 10 companies make up 67% of the index versus 74% for the XLE. The expense ratio for the VDE is minimal at 0.03%, versus 0.1% for the XLE, while the dividend yield is the same at 3.6%. This yield looks set to decline over the coming months as analysts anticipate a sharp drop in payouts, which puts the forward dividend yield on the underlying index at 3.0%, a far cry from the 17% figure seen at the height of the Covid crash.

VDE Top 10 Holdings (Bloomberg)

Valuation Discount Has Closed Significantly

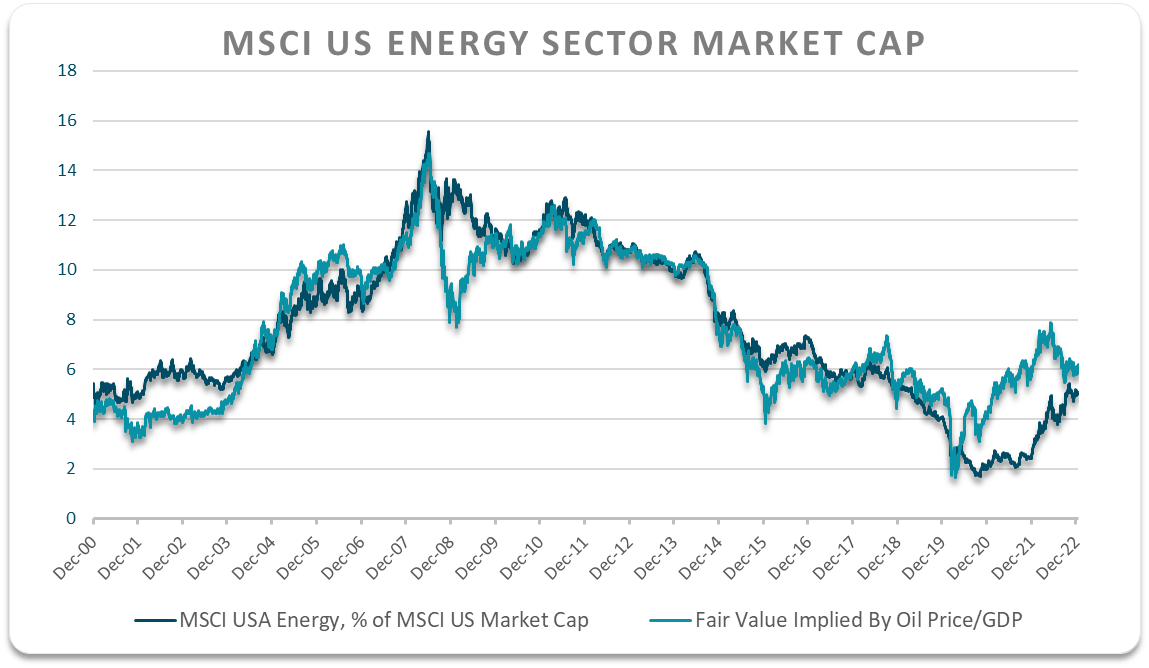

Even as oil prices have risen significantly over the past few years, the outperformance of the VDE has been even more impressive. That has resulted in a narrowing in the VDE’s valuation discount relative to the broader market. This can be seen in the chart below which shows the price of oil relative to US nominal GDP against the energy sector’s share of the MSCI US.

Bloomberg, Author’s calculations

The two lines have been extremely closely correlated in data going back to 2000 as one would expect. The higher the price of oil relative to the overall economy, the higher the profitability of the energy sector relative to the broader market, and therefore the higher its share of the market should be. After being more than 60% undervalued on this metric back in September 2021, the figure is less than 20% today.

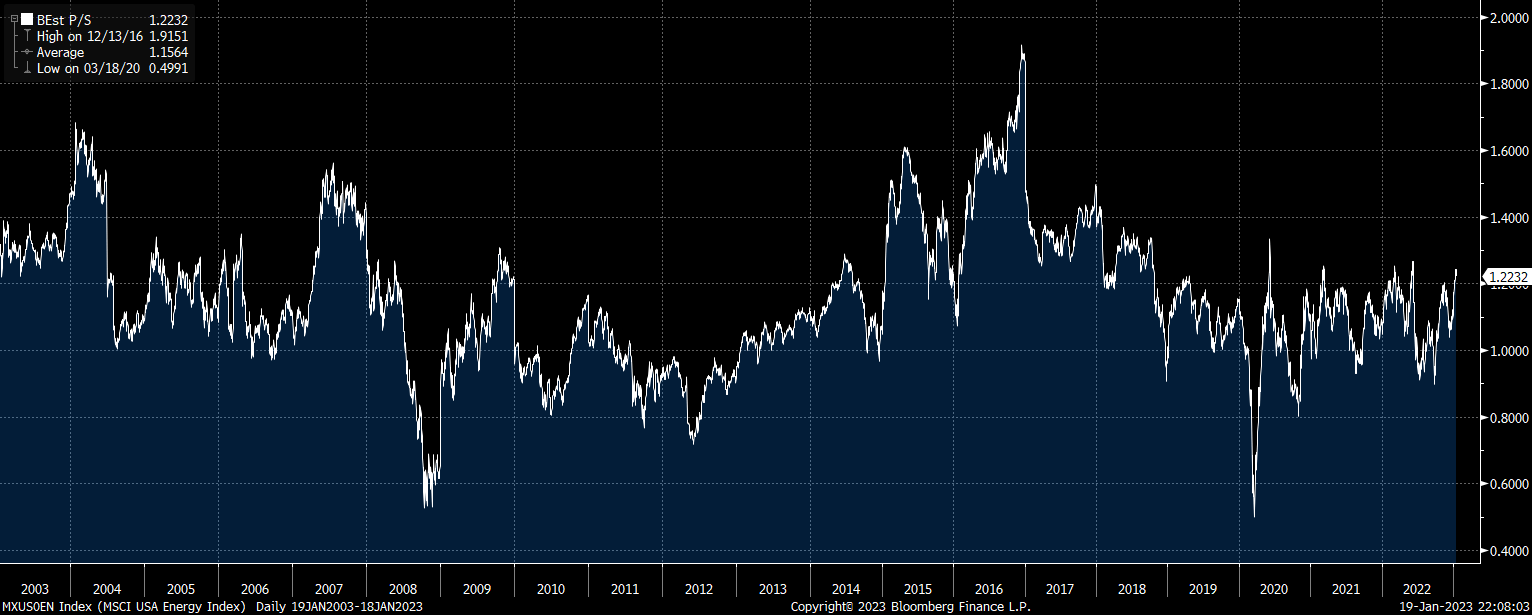

The rise in the VDE’s valuations can also be seen in its forward P/E ratio, which has risen to 9.9x from its September low of 7.0%. This figure reflects record profit margins which should be expected to mean revert lower over the coming years as capex spending picks up. If we look at the forward price-to-sales ratio, the current figure is actually in line with its long-term average. Nonetheless, the discount versus the broader market remains intact regardless of the valuation metric used and suggests that the VDE should outperform the SPX over the long term.

MSCI US Energy Sector Forward PS Ratio (Bloomberg)

Downside Volatility Suggests Caution Warranted

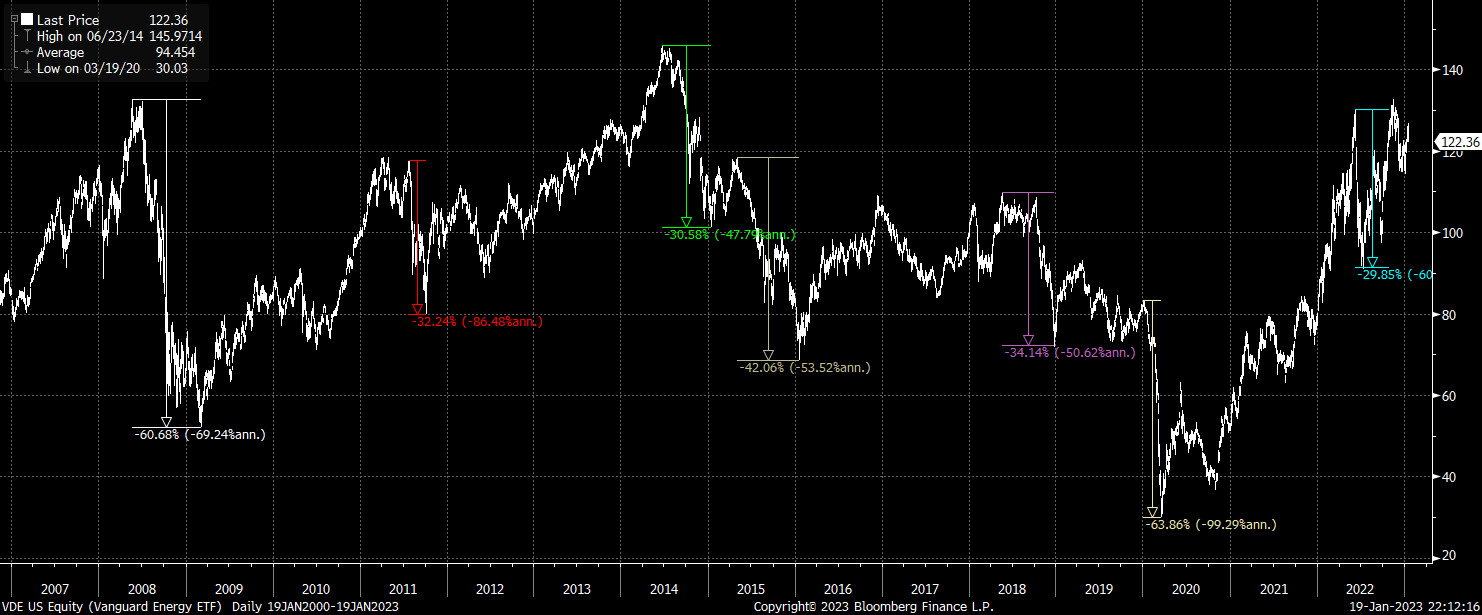

While the VDE is likely to outperform over the coming years, there are other factors to consider when investing in energy majors, most notably their higher degree of volatility relative to the broader market. 30% declines, the last of which occurred as recently as June last year, are the norm rather than the exception.

VDE Share Price (Bloomberg)

This high degree of volatility reflects the volatility nature of oil prices themselves, which have the ability to drive major swings in profitability for the sector. Investors should be compensated with higher long-term returns as a tradeoff for this higher volatility, and this is what we see today. With this in mind, investors should exercise caution towards the VDE at present, particularly with oil prices under downward pressure and the downtrend in the SPX looking set to resume.

Summary

The VDE has had a remarkable run over the past few years and after such strong gains the valuation gap relative to the broader market has narrowed. While valuations remain attractive relative to the SPX, which should result in stronger long-term returns, this will come at a cost of higher volatility, which suggests caution is warranted in the short term.

Be the first to comment