SolStock/E+ via Getty Images

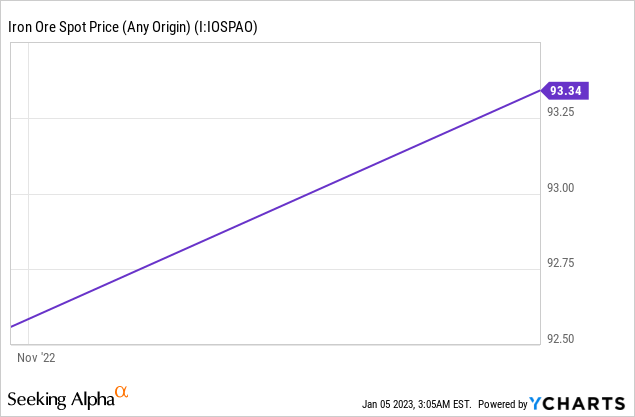

Vale S.A. (NYSE:VALE) is the world’s largest iron ore miner. Iron ore demand is primarily driven by Chinese demand. China only recently is lifting Covid restrictions, which seems to be a positive factor in demand. Meanwhile, its real estate sector is still in the doldrums and going through a very tough period. In the aggregate, the result is that iron ore prices appear on the rise once more after coming down from summer highs.

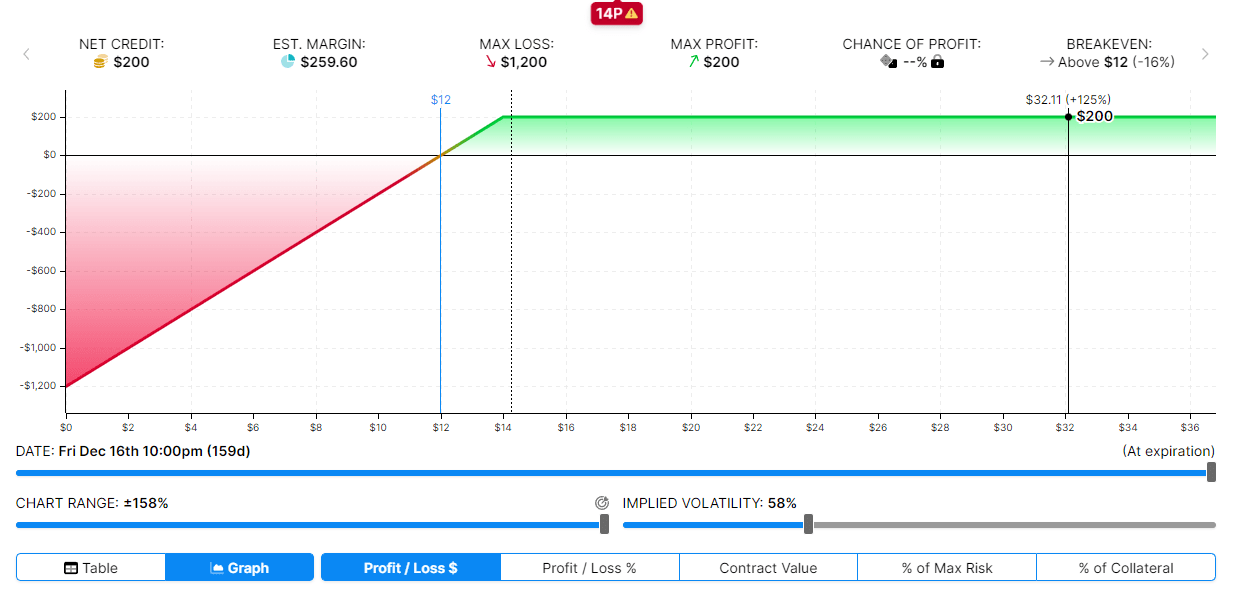

In a previous article, I’ve talked about an option position that I liked for Vale:

What I did, and keep in mind this is very risky, is to sell a December $14 put. These trade around ~$2. This means my maximum loss is $1200 per contract. My maximum upside on the trade is $200. At $12 the contract breaks even at expiration. Graphically, the exposure looks like this:

put exposure Vale (Optionstrat)

The buyback program and management confidence it is happening at attractive prices add to my conviction the buyback is likely strong whenever Vale’s share price is stalling or falling. That should strongly decrease the odds the share price ends up substantially down over the next few months. I’m not sure if commodity producers are going to be in high demand with a potential looming recession, but I like the premium on this contract vs. the risk of a sustained share price decline.

As we near the expiry date, I’ll be more likely to roll over the contract to avoid holding an extremely volatile position. This is especially true if the contract is still near the money.

The December $14 put options have now expired and the position worked out fine:

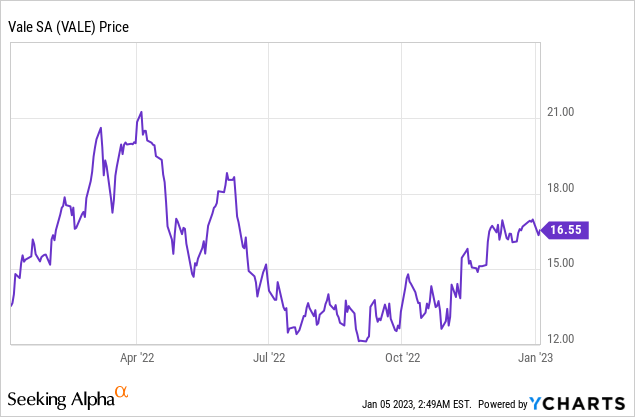

Going forward, I’m less interested in Vale, as the risk of a recession continues to increase. As long as there is no recession, I expect the Fed to continue pumping the brakes (increasing interest rates and continue QT).

However, Vale plans to separate its base metal assets from its iron ore operations. It is also talking about unveiling a strategic partner in H1 next year. It seems weird to me that Vale is so excited about a strategic partner. Except – keep in mind this is speculation – it could be Elon Musk’s Tesla (TSLA).

Musk has been very worried for years about the supply of Nickel and other base metals needed for electric vehicles (“EVs”). He even tried to buy a stake in Glencore (OTCPK:GLCNF), which ultimately failed because Tesla didn’t want the coal exposure.

If Vale separates future oriented battery powering metals into a separate company, that could make a lot of sense for Tesla to be a part of.

Regardless of whether Tesla will be the partner, the split of assets makes sense. A battery metals-focused company is very much something that interests ESG investors. These types of miners are more sought after and receive higher multiples. Instead of Vale’s many base metal assets being viewed as an afterthought to the iron ore business they will become the highlights in a new structure. I think it is a credible idea a separation will unlock shareholder value.

If it happens through a Tesla/Musk partnership that will draw all the more attention. If you read my stuff regularly, you’ll known I’m definitely not a fan of Musk but many people are. The number could be dwindling given his chaotic strategy to fix Twitter. Tesla is also rapidly decreasing in value which may make it more difficult to finance a partnership. On the other hand, Tesla would probably be delighted to use its cost of capital to tap into the tangible Vale cash flows.

Vale commented on a potential separation on the latest earnings call as well:

Hey Caio, thanks for your question. Let’s see. Well, that’s true. We’ve been very clear on the path to unlock value in base metals, as I mentioned in the previous question has exactly where we see enormous how can I say that amount of value to be delivered. What the execution path that we’ve been discussing. And again, as we mentioned, the IPO I’m going to get back to you tonight in a minute. We’ve been very disciplined on that. We’ve been communicating to you. First of all, no decision has been taken within our board. But we were going to segregate on our assets. We did that.

So we just announced that there recently. Because, yes, we say avenues, but the avenues they have a path to that. And the best goes back to the execution of our operating assets, the execution of a growth plan. With being that we could see a partnership being built, I think this is the most natural, and it has been as again voiced by us even in the event that you mentioned in our calls. So we have engaged advisors to help us on that if we are able to find partners because one very strong point here for you and for everybody we not selling base metals. Base metals is the best assets in the world value, it will keep it. So what we want is a partnership events to look at these values that you just mentioned.

And then the word that I use there was eventually and might be a confusing word for English investors and Portuguese, I feel it’s an optionality is not the one that we believe that’s going to be happy now because of the previous question. We need to fix the asset still, partnership can be done now because we can find partners that see this value that we see in this business. Help us deliver the growth, help us deliver the execution, help us with creating a new current. Yes. To go after these avenues when timing wise, I’ll pass to Gustavo, because he can give you more color on that and then Spinelli can comment on the value of volume question.

It appears an IPO or spin-out is less of a thing then the partnership. That’s unfortunate and definitely puts a bit of a damper on my excitement for Vale’s 2023.

To get a clear picture of where Vale is at, I also wanted to look at its relative valuation compared to other major miners. For what it is worth I think the entire group is on the cheap side of things compared to the rest of the market. I pulled up the valuation statistics on Seeking Alpha for a number of major mining peers:

|

Vale |

BHP |

Rio Tinto |

Anglo-American |

Glencore |

|

|---|---|---|---|---|---|

| P/E Non-GAAP (FY1) |

4.75 |

12.24 |

8.05 |

– |

– |

| P/E Non-GAAP (FY2) |

6.81 |

12.58 |

9.88 |

– |

– |

| P/E Non-GAAP (FY3) |

7.11 |

34.68 |

10.08 |

– |

– |

| P/E Non-GAAP (TTM) |

3.85 |

– |

– |

– |

– |

| P/E GAAP (FWD) |

4.65 |

14.02 |

8.97 |

– |

– |

| P/E GAAP (TTM) |

4.29 |

7.64 |

6.45 |

6.86 |

5.49 |

| PEG Non-GAAP (FWD) |

0.68 |

NM |

NM |

– |

– |

| PEG GAAP (TTM) |

NM |

0.10 |

NM |

1.29 |

0.01 |

| Price/Sales (TTM) |

1.75 |

2.36 |

1.89 |

1.26 |

0.35 |

| EV/Sales (FWD) |

1.98 |

2.95 |

2.64 |

1.57 |

0.40 |

| EV/Sales (TTM) |

1.94 |

2.43 |

2.39 |

1.54 |

0.44 |

| EV/EBITDA (FWD) |

4.06 |

5.19 |

5.46 |

3.93 |

3.15 |

| EV/EBITDA (TTM) |

3.74 |

4.22 |

5.13 |

3.70 |

4.05 |

| Price to Book (TTM) |

2.23 |

3.43 |

2.24 |

1.66 |

1.79 |

| Price/Cash Flow (TTM) |

6.82 |

4.80 |

5.12 |

3.60 |

9.14 |

It is especially interesting to look at p/b, EV/EBITDA ((forward and TTM)), and of course price to cash flow. Vale definitely appears attractive compared to BHP (BHP) and Rio Tinto (RIO). However, Glencore and Anglo-American appear slightly more attractive than Vale.

Conclusion

As a special-situation investor, I’m very interested in the separation of the businesses and the potential for a big name partner to bring attention to underestimated Vale assets. However, Vale’s valuation is sort of in line with other big majors. The separation looks like it will happen in a very slow way that leaves most of the value within Vale. I’m not as sure a structure like that unlocks value. Vale management seems very excited about a potential partnership. That, together with Musk’s serious interest in battery metals, leads me to speculate Tesla could take a strategic interest.

I think it is highly likely such a high profile partnership would bring lot of eyeballs to Vale assets and highlight their importance in the energy transition. At this point it seems like something of a free option to hold onto Vale until there’s more clarity around the separation. The company trades in line with peers, but clearly there is the possibility for a value unlocking event.

Instead of the option trade I’ve favored in a previous article, I now prefer Vale S.A. shares. I don’t think the opportunity is clear enough to justify a buy based on this special situation angle. If I owned Vale S.A. shares, I’d likely hang on and collect some of that sweet ~9% yield, to see it through but I’m not going to buy to speculate on the event.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment