supersizer/E+ via Getty Images

Thesis highlight

Utz Brands (NYSE:UTZ) has 19% upside. UTZ is a company that produces a wide variety of packaged foods. The market for salty snacks is a lucrative one, valued at $26 billion within the larger $93 billion U.S. snack foods market. With consumers snacking more often, both on the go and at home, the demand for easy to prepare and satisfying snacks is on the rise. UTZ is well positioned to take advantage of this trend, with a pure-play salty snacking portfolio and a focus on innovation and marketing.

Company overview

A variety of packaged foods are available from Utz Brands. The Company produces a full line of salty snacks such as potato chips, veggie snacks, pub and party mixes, tortilla chips, and other snacks.

Attractive and resilient market

Within the larger $93 billion U.S. snack foods market, UTZ operates in the lucrative and expanding $26 billion salty snacks category. It seems to me that people are more likely to snack these days, and that they are more likely to snack on the go or at home, so they need snacks that are both easy to prepare and satisfying to eat. And there are numbers to back up this theory. As an illustration, 91% of consumers snack multiple times daily, and snacks account for half of all mealtimes. In addition, the competitive dynamics in the salty snacks market have historically favored manufacturers and consumers. This is so because the market share of private labels is relatively low, and the dominant firms in the industry rely heavily on advertising and new product development to stay ahead of the pack. These consumer and market movements should keep boosting sales of salty snacks at stores.

My impression is that demand for staple foods is generally stable, and that their supply chain is primarily domestic. As evidenced by its unabated expansion throughout the Great Financial Crisis and COVID, the salty snacks category appears to be relatively immune to the effects of economic uncertainty.

UTZ is well-positioned to capture share

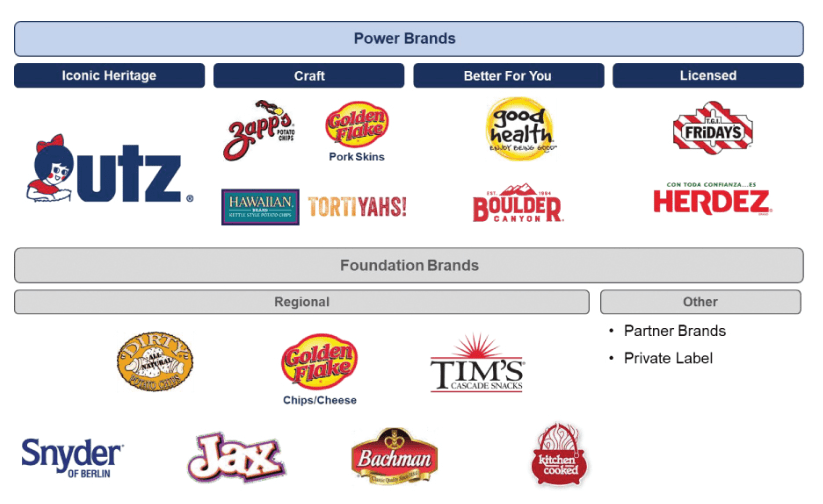

I think UTZ’s pure-play salty snacking portfolio puts it in a good position to gain market share in the salty-snack industry. UTZ actively manages their brand portfolio by separating it into two categories: Power Brands and Foundation Brands. In my opinion, the Power Brands market is the most promising one. The Power Brands have higher growth and margins, more room for innovations, and better marketing responsiveness than the Foundation Brands. In addition, given the increased marketing support from UTZ and the new product innovations made possible by utilizing Collier Creek’s expertise, I think there is still a sizable window of opportunity for Power Brands to expand both in terms of sales and distribution.

S-1

To provide some background, UTZ has historically lost ground in the salty snacks market, while larger competitors like PepsiCo (PEP), Grupo Bimbo, and Hershey (HSY) have gained ground. But the company has been turned around by management, as evidenced by the increase in market share since 2019. According to the company’s 3Q22 earnings presentation slides, UTZ has increased its market share from 3.8% to 4.6%, moving it up to the #3 spot from the #4 spot. I believe UTZ’s savvy execution has led to its current growth trend, as the company has increased production to keep up with demand and has accelerated shelf restocking to reduce stock-outs.

Another positive point to note is UTZ is not overly exposed to any one brand or product sub-category. This is thanks to its diversified portfolio and offerings throughout various salty snack sub-categories, which I believe reduces business risk and leads to more stable financial performance.

2Q22 earnings

Strong manufacturing and distribution network

In my opinion, as a manufacturer and distributor, UTZ has a leg up on some of the other players and new entrants in the salty snacks market in the United States.

UTZ is able to produce a diverse range of premium salty snacks thanks to its extensive manufacturing capabilities. In my opinion, UTZ’s ability to supply a wide variety of salty snacks is a selling point for retailers, leading to increased sales and more shelf space for the company’s products. It’s worth noting that UTZ factories cover a large area and have plenty of room to expand. In addition to this, UTZ is able to innovate products more quickly and adapt to shifting consumer preferences because of its in-house expertise and experience with a wide range of manufacturing methods, ingredient flavours, and packaging formats.

In addition to UTZ’s impressive production capacity, I think the company’s distribution network is particularly noteworthy. UTZ maintains a hard-to-replicate, atypical model of distribution by:

- Direct shipments to hundreds of customer distribution centers serving over 10,000 retail outlets

- Distributors reaching over 10,000 retail stores, and

- UTZ extensive direct-store delivery [DSD] network of more than a thousand routes reaching over 70,000 retail stores.

The latter is the most distinctive of the three channels. In my opinion, UTZ’s DSD capabilities give it a distinct advantage in the salty snack category by allowing for wider distribution, more shelf space at retailers, quicker resupply for significantly greater in-stock levels, and better merchandising opportunities. From what I’ve gathered, UTZ extensive DSD capabilities give the company a competitive edge and make the salty snack industry in which it operates more appealing than those of its competitors.

Moreover, this distribution system is highly scalable from a profit and loss perspective, which means that UTZ can increase margins on new revenue streams and save a lot of money as it incorporates newly acquired brands into its platform.

In my opinion, UTZ has spent many years and a great deal of resources cultivating and improving its hybrid distribution system through both internal growth and external acquisitions. To build a distribution network with the same reach and functionality as this one would be difficult and time-consuming, in my opinion.

M&A expertise

UTZ has demonstrated successful acquisition and integration thanks to their highly disciplined approach to M&A. UTZ’s highly scalable operating platform allows for the swift and seamless incorporation of newly acquired businesses into its existing framework, resulting in significant cost savings and distribution efficiencies. In most cases, UTZ has found ways to cut expenses that can be incorporated within the first 1 to 1.5 years post acquisition.

In my opinion, there are numerous benefits to employing an M&A strategy that is designed to increase value. UTZ’s growth rate, geographic reach, and distribution channels can all be improved through M&As, giving the company immediate benefits as well as longer-term benefits.

For me, UTZ has all the right ingredients to keep up its M&A strategy: a solid customer base, a scalable business model, a seasoned leadership team and directors, and a steady stream of cash flow. In terms of acquisition targets, UTZ has a large potential customer base and a wide range of companies to acquire thanks to its established platform in the salty snacks market. UTZ’s size, management, and ability to raise capital should also make it possible for the company to consider and successfully integrate future acquisitions of varying sizes.

Yet another strong quarter delivered

During the 3Q22, UTZ reported revenue growth of 16.0%, which was above market expectations due to higher-than-expected organic sales growth of 12.6% and smaller-than-expected volume declines. Management claimed that a drop in volumes was caused by a reduction in stock keeping units by 300 to 400 basis points, implying that volumes were up by a low single digit. Improved price versus mix and productivity gains led to a gross margin that was in line with expectations at 33.7%. Adjusted EBITDA of $47.7 million was above expectations, driven by this factor and slightly higher than expected SG&A expense.

The guidance that was given in the earnings report for the 3Q22 was good news. The company expects revenue growth of 17–19% for FY22, up from the previous projection of 13–15%. The company also increased its sales and EBITDA guidance for FY23. For the full year, they anticipate input cost inflation in the mid- to high-teens and adjusted EBITDA growth of 6-9%.

Valuation

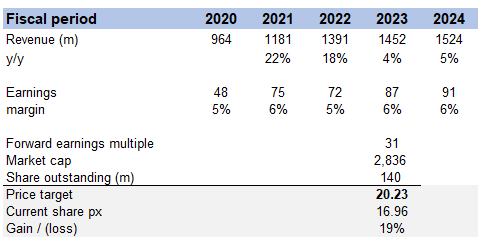

My model suggests that UTZ is worth $20.23 in FY23. The core part of my thesis is that UTZ can continue to capture share and grow along within this large category. Also, margin should continue to expand as it scales and enjoy better economies of scale. Of course, as I mentioned, UTZ ability to conduct value accretive M&As should also further enhance growth rate, if any deals are done.

Suppose UTZ grows as I modelled, it should generate around $1.5 billion in revenue and $91 million in earnings in FY24. Attaching the current forward earnings multiple here would suggest a 19% upside.

Own valuation

Risks

Change in consumer taste preference

Just like other players in the food and beverage industry, the provider will be affected by shifts in consumer preferences. UTZ’s organic growth could be hindered if consumers began eating fewer salty snacks (consistent with the current trend toward a healthier diet). This would force leadership to increase its reliance on mergers and acquisitions to expand, which has the potential to significantly slow the company’s long-term growth rate.

Conclusion

In summary, UTZ is a strong investment opportunity in the snack food industry. The market for salty snacks is attractive and resilient, and UTZ’s market position and execution have led to growth in market share and financial performance. The company’s diversified portfolio, active management of their brand portfolio, strong manufacturing and distribution network, and focus on innovation and marketing all make UTZ an attractive investment.

Be the first to comment