cveltri

One thing that I have discovered to be true about the market is that, over time, it can be harsh to companies that are experiencing pain but gracious to those firms that are making an effort to turn themselves around. Sometimes, that can even result in the companies in question seeing their share prices trade at levels that you would not normally anticipate. A great example of this can be seen by looking at Utz Brands, Inc. (NYSE:UTZ), a producer of chips and other snack items. In the past, I turned rather bearish on the business. In an article published in June 2022, I even went so far as to rate it a ‘sell’ because of its financial trajectory and how expensive the stock was. Since then, the enterprise has exceeded my expectations rather significantly. While the S&P 500 is up 26.8%, shares of Utz Brands have seen an upside of 31.8%.

Clearly, I got this call wrong. It happens from time to time. Part of this is because of some improvements that management has been pushing for. Already, we have seen some progress on that front. But in addition to that, on January 31st, the management team at the company announced some major changes aimed at improving operations even further. From what I can see, these maneuvers should be a net positive for the enterprise. But that doesn’t make the stock attractive enough to buy into just yet. Shares are still very expensive, though if the company can achieve its longer-term objectives, the end result could be positive. It is with this hope in mind and in response to management’s own hard efforts leading up to this point, that I have decided to upgrade the stock to a ‘hold’.

Some big changes

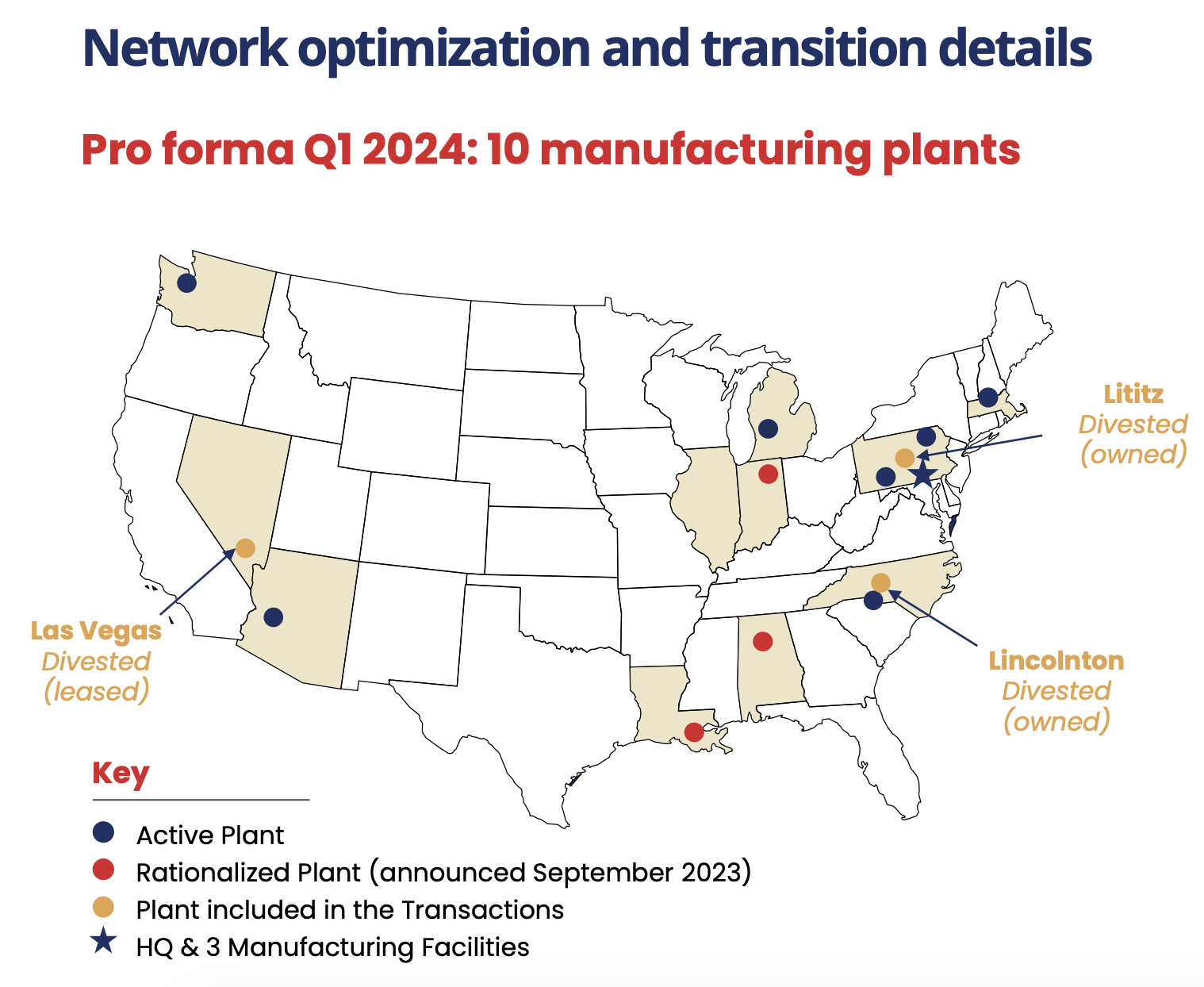

Times have not been particularly pleasant for Utz Brands. Even in the 2022 fiscal year, the business generated a net loss of $0.4 million. However, on January 31st of this year, the firm did announce some major developments. For starters, management decided to sell off certain assets, including three manufacturing facilities and its Good Health and R.W. Garcia brands. Collectively, the two brands that the company has decided to sell generated about $65 million in revenue for the business in 2023. That’s less than 5% of its overall anticipated sales. And yet, in exchange for all of these assets, the company is receiving consideration of $182.5 million. After factoring in taxes, it should be around $150 million.

Utz Brands

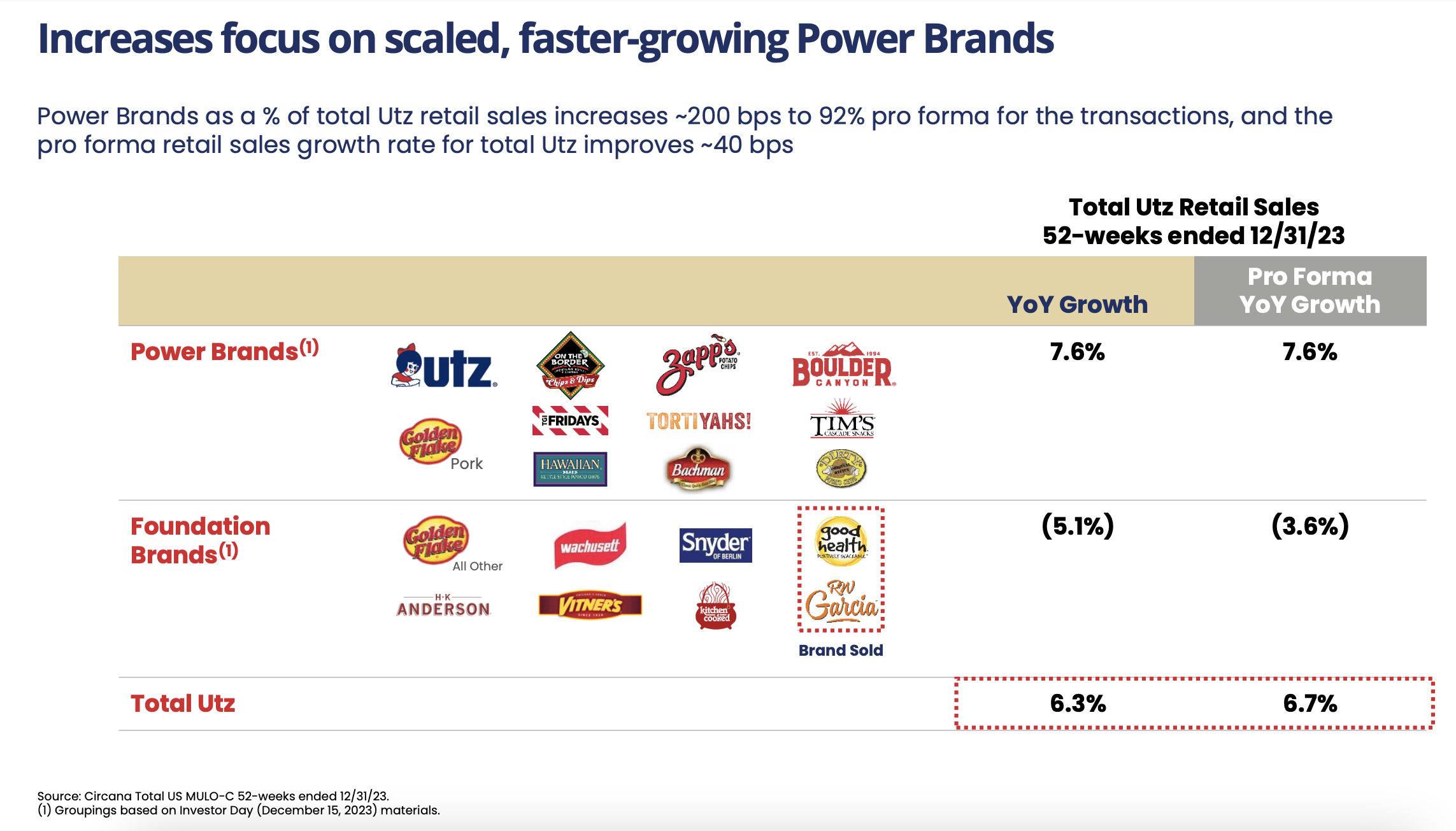

These proceeds will be allocated toward reducing long-term debt that management believes will reduce interest expense by $12 million on an annual run-rate basis. It also seems likely that these were unprofitable brands, especially because they seem to be in a state of decline. I say this because management said that year-over-year revenue growth for 2023 was around 6.3%. But when we strip these out of the equation, that growth increases to 6.7%. The decision to include in the mix some manufacturing facilities does reduce the company’s overall capacity. However, management has been working hard on reducing its physical footprint. At one point, it had 16 different manufacturing plants. It was announced in September of last year that three of these would be ‘rationalized’. Add on top of this the other three being sold as part of this deal, and the company should have 10 manufacturing plants, plus its global headquarters when all is said and done.

Utz Brands

I think it’s also important to note that the brands being unloaded are not part of the company’s major growth plans. The ‘Power Brands’ as management calls them are the true growth initiatives for the business and managed to grow by 7.6% in 2023. The decision to get rid of certain manufacturing facilities does not look to have any impact on growth for these brands moving forward. Instead, the brands sold came from the company’s ‘Foundation Brands’ that have historically been some of the more well-known names in its portfolio, but that might not be achieving any real growth.

Author – SEC EDGAR Data

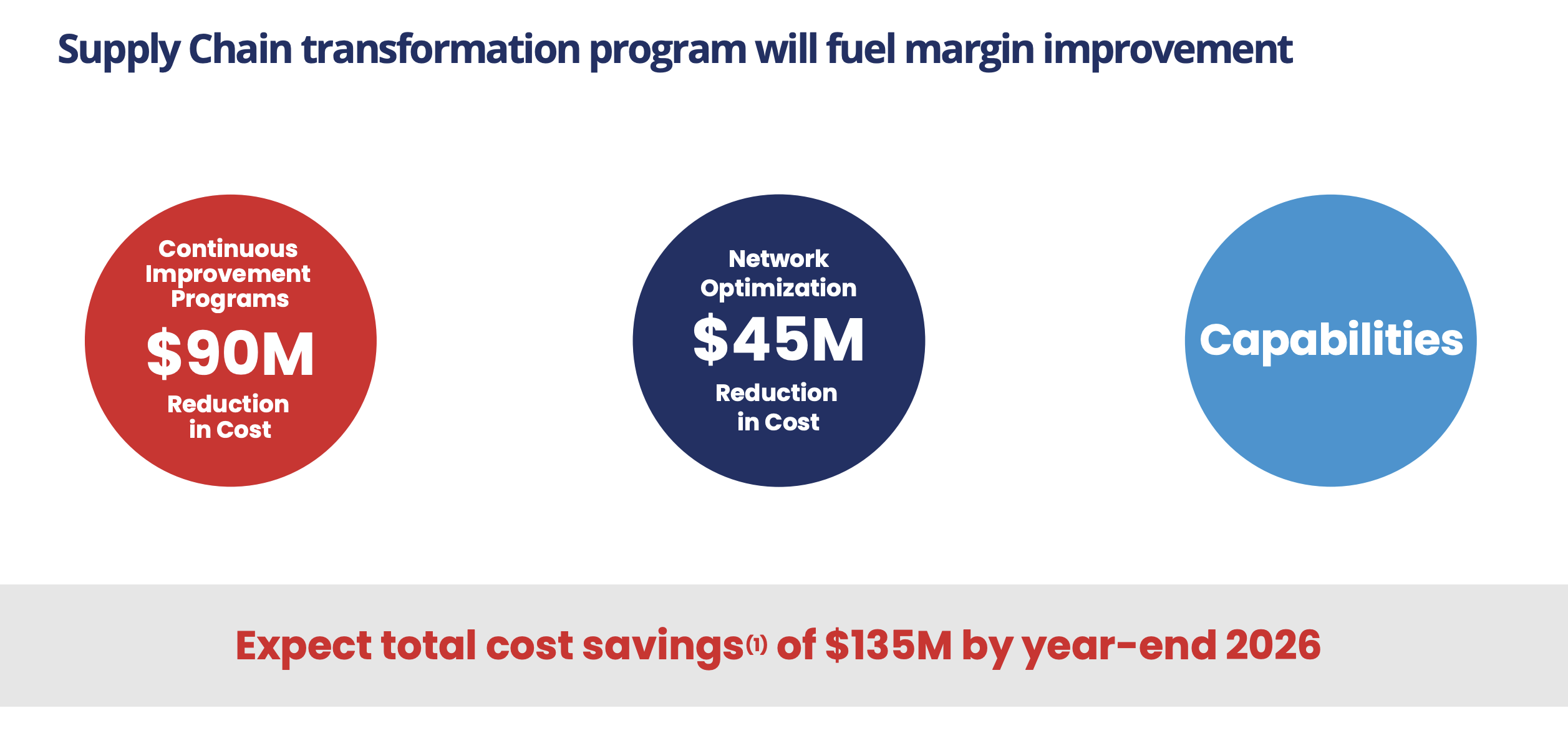

The company is currently working toward a cost-cutting program that will involve evaluating how it utilizes its assets, and will also involve scaling its mixing centers and focusing on costs across the board. This plan was initially presented on December 15th of last year. The ultimate goal is to cut costs by $45 million. There is no reason to believe that the interest reduction has been factored into this figure. But management did say that the decision to divest the three manufacturing facilities does help to accelerate this plan. This, combined with the $90 million cost reduction plan associated with other areas of the business that management is seeking to make will ultimately help to reduce costs, in addition to the interest reduction, by $135 million no later than the end of 2026.

I am hopeful that these initiatives will prove successful. However, it’s always risky to bank on multiyear cost-cutting programs. I do think factoring in the interest savings for the business is appropriate at this time. But I would not factor in any other aspects of its plan until they have been achieved. The good news is that we have seen some progress from a profitability perspective. As an example, we need only look at data covering the first nine months of the 2023 fiscal year compared to the same time in 2022.

Author – SEC EDGAR Data

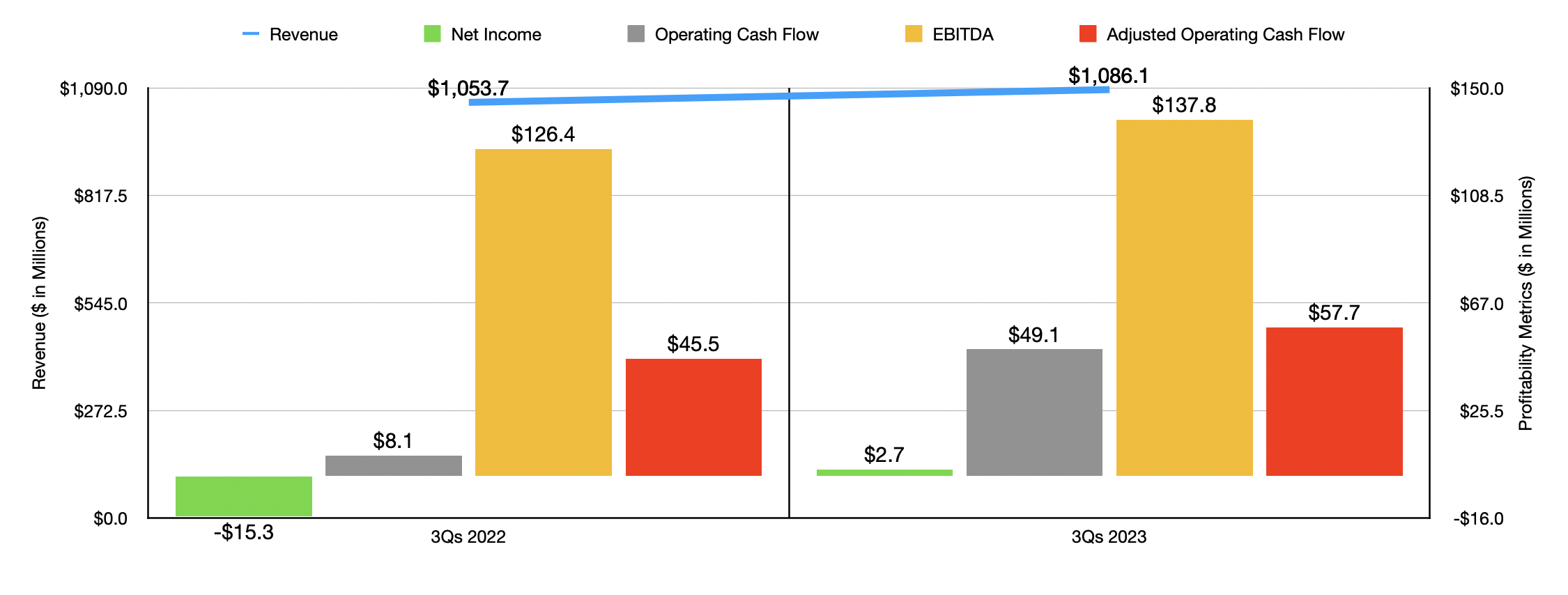

Revenue for the company during this window of time rose from $1.05 billion to just under $1.09 billion. But the really exciting stuff is not on the revenue side. It’s on the cost side. The company went from generating a net loss of $15.3 million to generating a modest profit of $2.7 million. Most of these savings came from the company’s selling and distribution category of expenses. These dropped from 21.5% of sales down to 18.7%. While this might not sound like much, when applied to the revenue generated in the first nine months of 2023, it translates to an extra $30.4 million in pretax profits for the business. Unfortunately, some things such as higher interest expenses and a growth in the cost of goods sold, offset some of this reduction.

The improvement in net profits also resulted in an improvement in cash flow. Operating cash flow surged from $8.1 million to $49.1 million. If we adjust for changes in working capital, it rose more modestly from $45.5 million to $57.7 million. And over that same window of time, EBITDA for the company expanded from $126.4 million to $137.8 million. Although management has not provided concrete data for the final quarter of the 2023 fiscal year, they did say that EBITDA would end up being between 9.5% and 10% higher for the year as a whole relative to what was seen in 2022. This would imply an EBITDA of approximately $187.1 million. But then if we make a similar assumption for adjusted operating cash flow and add onto it $12 million in interest savings moving forward, we would get a reading of $187.1 million.

Author – SEC EDGAR Data

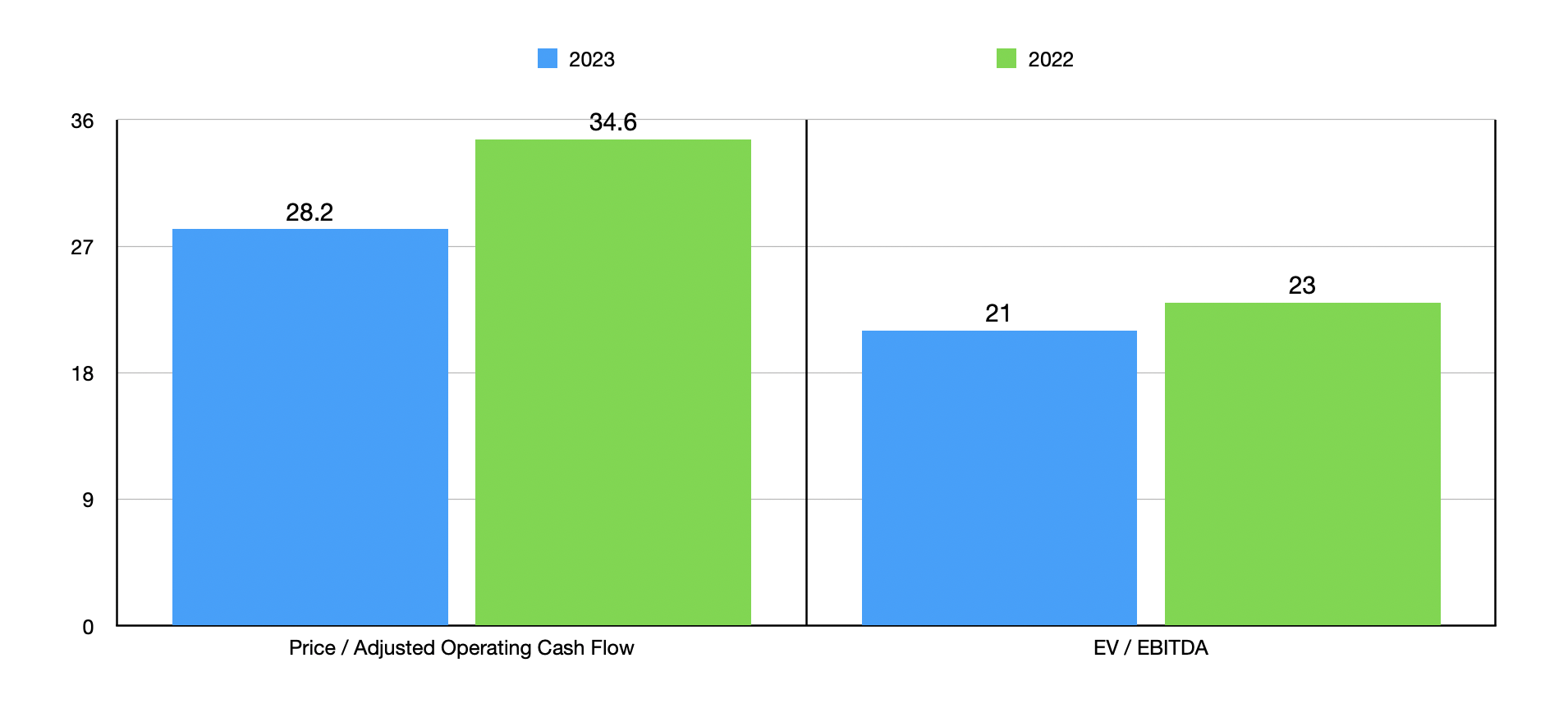

Using these figures, I was able to value the company as shown in the chart above. For a low-growth snack business, these multiples seem awfully high. I say this because, as shown in the table below, four of the five companies I compared it to on an EV to EBITDA basis were cheaper than it, while all five were cheaper on a price to operating cash flow basis. But of course, the market is pricing in potential additional savings moving forward. Given that the cost-cutting plans were announced in December, it’s safe to assume that none of the improvements are being factored into these assumptions. If we assume a 21% tax rate on those additional savings, and assume that management does achieve their goal by the end of 2026, then the price to operating cash flow multiple would be considerably lower at 12.7, while the EV to EBITDA multiple would be 12.6. These are much more reasonable multiples for the business. But it is speculative to bet on them transpiring.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Utz Brands, Inc. | 28.2 | 21.8 |

| TreeHouse Foods, Inc. (THS) | 17.6 | 11.5 |

| Cal-Maine Foods, Inc. (CALM) | 4.6 | 3.2 |

| Sovos Brands, Inc. (SOVO) | 25.3 | 43.8 |

| Nomad Foods Limited (NOMD) | 6.5 | 9.8 |

| J&J Snack Foods Corp. (JJSF) | 17.8 | 17.5 |

Takeaway

At this time, Utz Brands is an interesting turnaround prospect. If the company can show that it is achieving significant cost-cutting, then an upside for shareholders could exist from here. The first step was an easy one, and it should add value to some extent. But given how pricey shares are, I feel as though investors are paying entirely for any potential savings that might lie ahead. I prefer to be more conservative on these matters and see how things pan out. So until we do see some more concrete data, I cannot become optimistic about the firm. But turning more neutral with a ‘hold’ rating is not out of the question.

Be the first to comment