Tanarch

As our readers know, we have been discussing for some time now how investors need to pay attention to what they have in their portfolios as it relates to fixed income funds to avoid losses and manage risks. In 2022 we had a number of people asking us about losses they had in retirement portfolios or do-it-yourself brokerage accounts caused by what they perceived to be safe, healthy-yielding bond funds. We have tried to help readers avoid some of these issues by pointing out how we believed one should position their cash and short to intermediate fixed income holdings moving forward.

Our belief was that there was a lot more pain to come as the U.S. Federal Reserve was going to have to be aggressive in raising rates and that reaching for yield by taking on duration was a risk not worth engaging in. Instead, we believed that shifting to short-term holdings such as money market mutual funds or floating rate securities would protect capital more efficiently while also generating more interest income; essentially creating outperformance via both metrics (you have no capital losses while benefitting from rising rates, and thus greater interest income). We recommended ETFs such as the Goldman Sachs Treasury Access 0-1 Year ETF (GBIL) and the WisdomTree Floating Rate Treasury ETF (USFR) which have done great jobs of preserving capital while also delivering interest income.

Last month we discussed how some ultra-short duration funds were beginning to look attractive vs their floating rate counterparts and how investors should start to rotate into fixed coupon ETFs with longer maturities in a planned way.

One Interesting Play

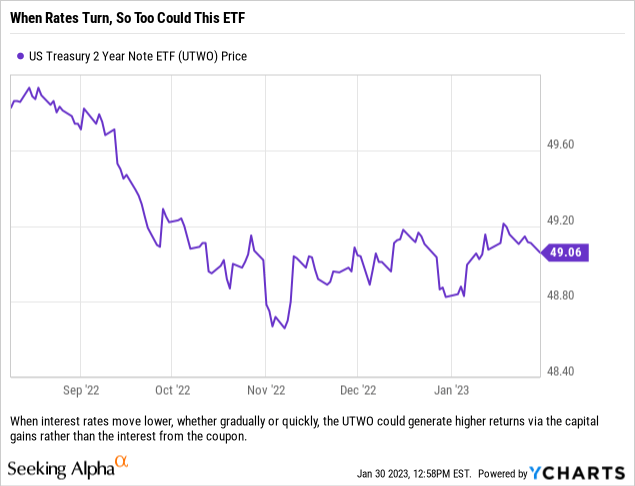

As we look for ways to gradually extend out and rebuild fixed income sleeves that actually make sense, we stumbled across the US Treasury 2 Year Note ETF (NASDAQ:UTWO). This is a new ETF, which has an inception date of August 9, 2022, and is on the small side with only around $225 million in assets but it does have a respectable expense ratio of 0.15% and thus could serve a purpose in certain investors’ portfolios.

The 2-year portion of the treasury curve is historically the most volatile, so when the Fed does finally move, or pivot, investors could benefit by holding this in their portfolio. This is not a laddered portfolio, instead the ETF owns the current on-the-run 2-year which generates performance via the price swing in the bond plus the interest income from the coupon. While this is not a stable NAV security, this fits into our thesis of not chasing yield and managing one’s fixed income in a prudent manner so as not to be crushed when rates or spreads move against you.

With rates having moved higher over the last few months, the US Treasury 2-Year Note ETF now has a net indicated yield of 4.31% – which is very important for investors to understand. While many bond ETFs are currently seeing their yields move higher as they add higher coupon bonds and/or bonds trading at a discount to par, this particular ETF has one holding (each month) and rolls that position into the next on-the-run US 2-Year Treasury. So the net indicated yield will move around on this one and while investors will be able to collect decent coupons in the interim, the volatility of the bond will be key as any downward movement can eat away at returns over the long run.

We think that rates are topping out, so while we are giving up the ability to lock in attractive coupons, we will be able to collect interest income on a monthly basis while also benefiting from potential capital gains.

Why We Like This Play

We think that there are a few ways to benefit here. First, if the speed at which rates are increasing slows (which appears likely) then the interest income could serve as a buffer to losses on the price of the Treasury that the ETF holds at that time. If we move to a period where the Federal Reserve pauses and decides to take inventory of where the economy is, investors would be able to benefit from what could be a relatively stable (or even positive) price environment for the underlying 2-Year Treasury and benefit from capital gains and the higher coupon (and when the bond is sold in a month’s time, the accrued interest is earned). Lastly, there would also be solid returns in an environment where the Fed was easing and the coupon gradually came down on the 2-Year Treasury which would result in less interest income but higher capital gains as investors tried to lock in rates. Note: It is important to remember that a $1 move higher on the price of the Treasury would be a rather significant annualized gain.

What makes this really attractive in our view is that it might be a little early to go all in on a bet for lower rates and higher bond prices across the yield curve, but with this ETF you are able to bet on a specific on-the-run maturity as you gradually rebuild fixed income allocations and add duration to your portfolio. You are not going too far out to get crushed if too early, and not adding corporate exposure so avoiding the risk of spreads widening.

Final Thoughts

We are not one to make huge bets when it comes to interest rates, especially with this Fed and their attitude of having to prove themselves in order to establish credibility. ‘Fighting the Fed’ is usually a losing battle, however, redeploying capital when reallocating by taking baby steps is prudent and could position investors to benefit once the Fed finally does decide that it is time to pivot. And not knowing at this time whether the Fed will wait too long to make that move, leads us to believe that investors are best served by utilizing ETFs with US Treasury exposure rather than corporates – which enables one to avoid risks associated with spreads.

Be the first to comment