Galeanu Mihai

Investment Thesis

USA Compression Partners (NYSE:USAC) is predominantly focused on natural gas compression services. While the business provides processing and transportation for both natural gas and crude oil, it’s overwhelmingly focused on natural gas compression and transportation.

The bearish aspect facing the stock is that USAC carries a significant amount of debt. And that debt carries a high coupon.

On the other hand, USAC continues to distribute its cash flows, and Q4 2022 is expected to reach a high for the year.

Assuming that for 2023, its distribution remains flat with 2022, that would mean a cash yield of 10.5% from current prices.

Particular Tax Status For Foreigners

Before we go further, note that USAC is an LP. That means that as part of its structure, it distributes the majority of its cash. But at the same time, it has a schedule K-3.

This means 10% of the amount of funds that would settle resulting from any transaction or distribution, not just 10% on any calculated profit, are taxed.

This affects anyone that’s not in the US. Read here for more details.

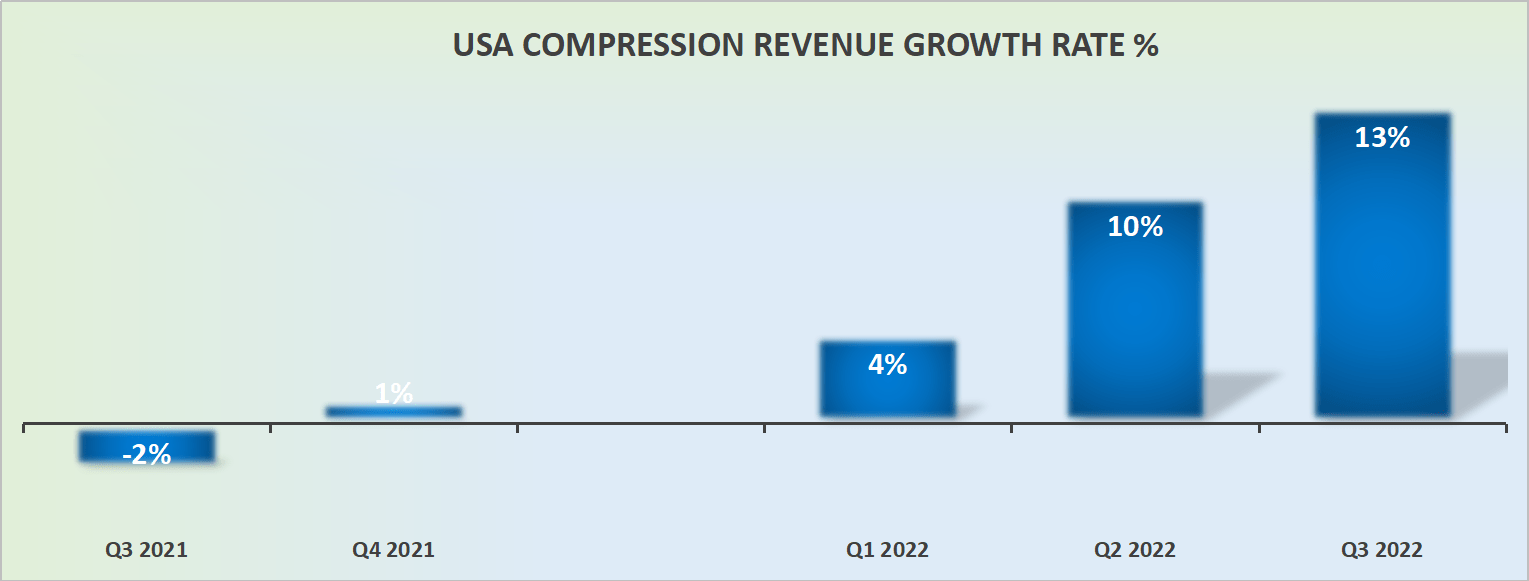

Revenue Growth Rates, Now Compelling

Moving on, as you can see below, USAC’s revenue growth rates are not particularly strong. But that’s a good thing. It goes to the heart of the bull case.

USAC revenue growth rates

USAC’s business model isn’t directly related to natural gas prices. USAC participates, indirectly, by providing compression services to natural gas.

That means that if one has a view that there’s going to be continued increased global demand for natural gas, that will mean that USAC will continue to benefit from this tailwind.

Put another way, USAC operates in the midstream. It’s not likely to have the volatility of downstream players.

And now we get further into the heart of the bull case.

Capital Distribution Program

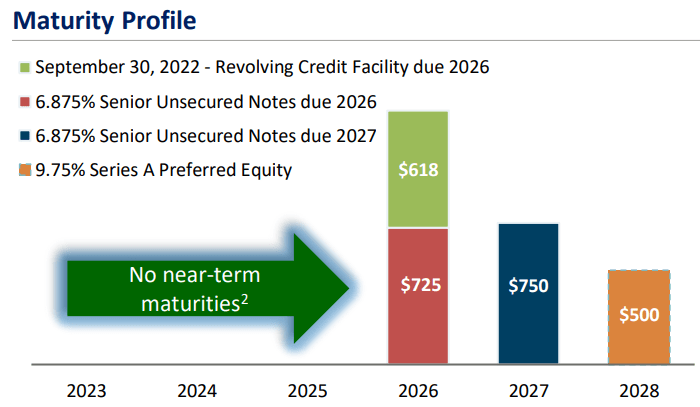

Before going much further, consider USAC’s balance sheet.

USAC December presentation

What you don’t see here is that borrowings under the revolving credit facility were approximately $620 million. Put simply, USAC carries some debt, but in the near term, it does not have maturities.

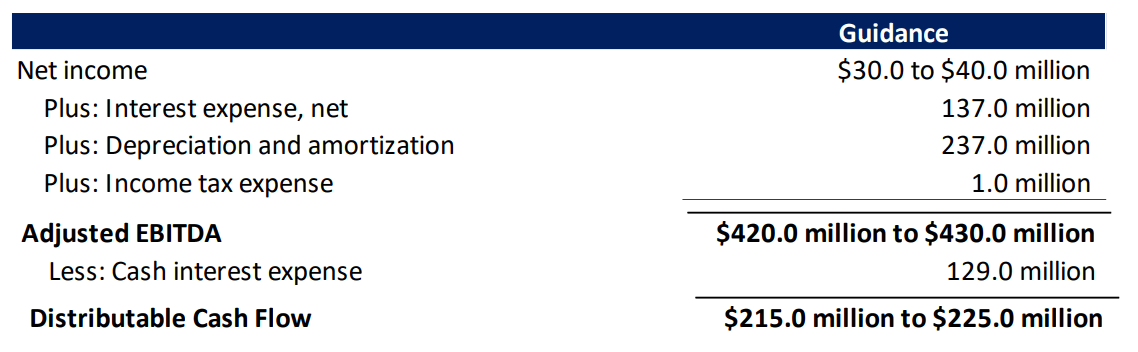

That being said, this doesn’t get in the way of USAC’s strong capital distribution program.

USAC December presentation

As you can see above, USAC guides to finish 2022 by distributing approximately $220 million. Having already distributed $154 million for the first 9 months of 2022, one can infer that Q4 could potentially see $70 million of distributable cash flows.

Furthermore, as you can see in the table below, even though Q1 2022 saw its distributable cash flow ratio fall below 1x, the subsequent quarters climbed above 1x.

USAC December presentation

Thus ensuring that USAC has the wherewithal to distribute approximately $70 million in Q4.

What does this mean in practical terms?

USAC Yield for 2023?

Let’s assume that for 2023, USAC’s cash distribution per common stock remains level with the prior years at $2.10.

That would mean that investors getting into the stock now would get a 10.5% yield on the stock.

The Bottom Line

The main risk aspect overhanging the stock is that USAC carries a significant amount of debt. That debt doesn’t have to be attended to today, but it absolutely has to be attended to sooner rather than later. Also, on top of the debt, there’s also the outstanding revolver.

What’s more, given that the coupon on its debt ranges from 6.9% to just under 10%, that just speaks of the doubt that creditors have over USAC’s long-term prospects.

Moreover, keep in mind that USAC’s debt was issued in 2018 and 2019, at a time when rates were abnormally low. When USAC comes to refinance its debt, which it must start doing so in 2024, if not sooner, it will be more onerous terms, given that interest rates will have gone from close to 0% to somewhere close to 5% by the time 2023 is done.

All that being said, despite shining a light on some negative considerations investors should be aware of, for anyone that believes that natural gas will continue to play a crucial role in our great energy transition, USAC is well-positioned to benefit.

As evidence that USAC’s services continue to increase, keep in mind that Q3 utilization exit rate was 91% and up from 89% in Q2 2022, as well as up from 83% in Q3 2021.

Once again reinforcing the view that if natural gas demand continues to be strong, USAC has got the fleet to service this demand.

Be the first to comment