TERADAT SANTIVIVUT

This article was first posted in Outperforming the Market on February 3, 2023

Investment thesis

For those who bought Upstart (NASDAQ:UPST) at what I think are insane valuations in late 2021 when its stock price was $390, this seems like a bad idea given that you would have lost 96% of the value of your investment if you bought at the top.

This is why I emphasize repeatedly that valuation is key, and it should be a focus for everyone picking their own stocks and those involved in the active management of stocks.

However, when sentiment is this bad given the massive selloff, I think that at some point, Upstart will look attractive again given the attractive valuation it is currently trading at, along with its improving fundamentals.

This, in my view, would present itself as a perfect contrarian or value opportunity.

In an earlier article, I shared with members of Outperforming the Market my deep dive research on Upstart and recently bought Upstart stock earlier in January.

I think that there is a perfect contrarian opportunity presenting itself for Upstart, in my view, given that valuations have reached somewhat cheap levels, at a time when business fundamentals are improving.

Today, in this article, I aim to share more with you about this opportunity that I see with Upstart and why I am buying Upstart.

Brief introduction to Upstart

Upstart is a leading cloud-based AI lending platform.

As an AI lending platform, it ultimately seeks to use the power of AI to more accurately quantify the true risk of a loan. Through the use of AI, Upstart aims to target the millions of creditworthy individuals that are left behind by the traditional legacy credit systems, as well as those who are paying more than they should to borrow money.

At the heart of Upstart’s business is innovation. This innovation is a much needed one in the United States credit market given that traditional legacy credit systems have not seen much change for decades. For example, the FICO score was invented in 1989 and continues to be the gold standard for banks to decide who to approve for loans and at what interest rate they should approve it for. As a result of the lack of innovation, affordable credit has not been made available to millions of consumers in the United States as a result of using legacy credit systems that use limited number of variables to identify and quantify risk.

Upstart’s AI lending platform

The central value proposition for Upstart is its AI models and this, in my opinion, is what differentiates Upstart from all other players in the industry.

At the end of the day, as an AI lending platform, its AI models need to bring performance better than the traditional models or at a lower cost.

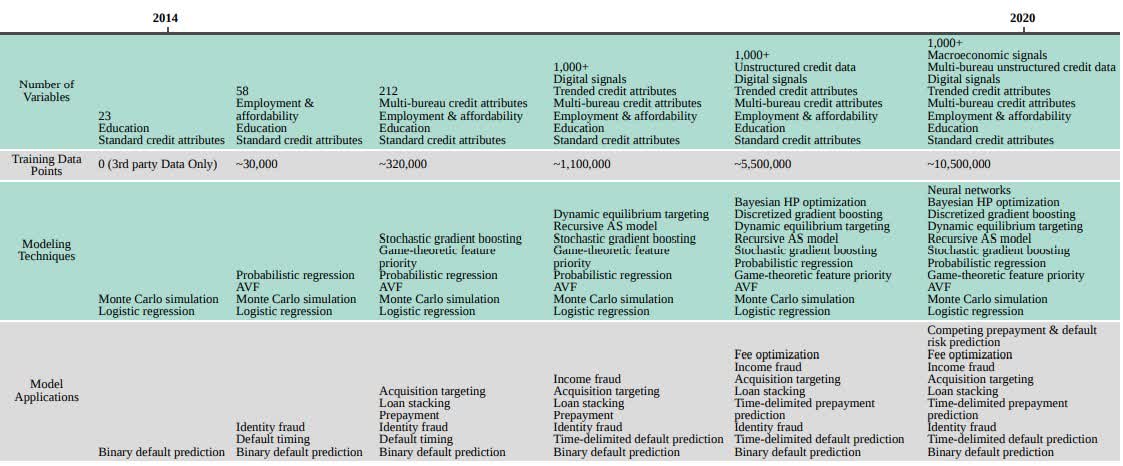

Evolution of Upstart’s AI models (Upstart IR)

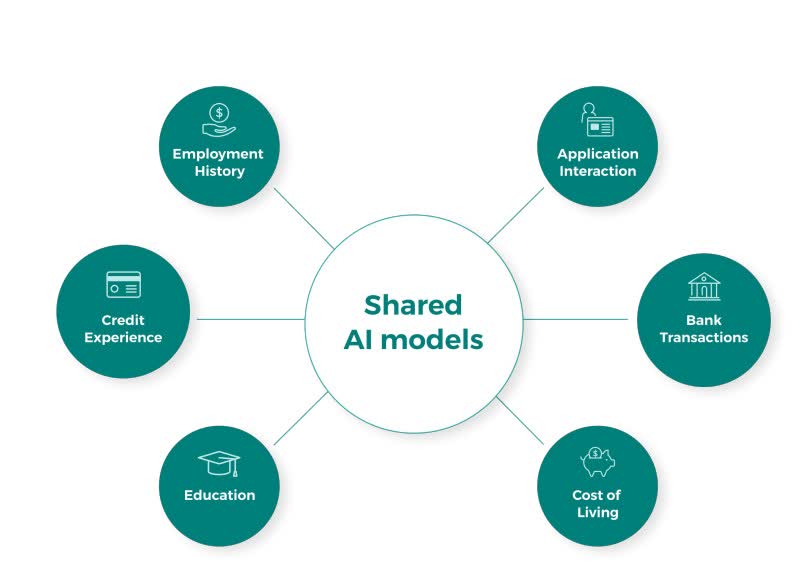

To understand the complexity and depth of Upstart’s AI models, we need to know what goes into the models. More than 1,500 variables are incorporated into Upstart’s AI models, and they have been trained by more than 21.6 million repayment events. Apart from these, Upstart also incorporates interactions between variables through use of sophisticated machine learning algorithms, using large volumes of training data to improve on the accuracy of the model. As time goes by, Upstart continues to upgrade and improve on its modeling techniques to improve on the overall accuracy of the model. For reference, Upstart started with only 23 variables in 2014 and subsequently increased the number of variables to more than 1,500 in 2021. These variables include things like credit experience, educational history, cost of living, employment, amongst other things. This differentiates Upstart as many other incumbent lenders lack the depth of variables that powers Upstart’s models.

Upstart AI models (Upstart IR)

For Upstart’s bank partners, the company allows for customized solutions based on the bank partner’s needs and policies. For example, some of Upstart’s bank partners may look to set certain constraints on Upstart’s AI models by setting a minimum credit score or a maximum debt-to-income ratio. As a result, each bank will have their own self-defined lending program that will lead to the origination of loans that meet those requirements and constraints at a low cost per loan.

At the end of the day, through the use of Upstart’s AI platform and technology, the resulting innovation brings strong competitive advantages to Upstart as it has a strong value proposition to both consumers and banking partners.

Benefits to consumers

At the end of the day, Upstart is a platform, and it serves two parties: consumers and banking partners.

Upstart’s value proposition to consumers is very clear. As a company focused on the underserved, it ultimately aims to bring access to credit to those it is not available to and to provide this access at a lower cost. As a result, the first value proposition to consumers comes in the form of a higher approval rate and lower interest rates. According to Upstart in its 2021 Annual Report, the CFPB reported that Upstart’s AI models approves 27% more borrowers compared to other high quality traditional lending models while providing a 16% lower average APR for approved loans. Upstart’s own analysis found that its loan offers have improved significantly over time when compared to those of its peers.

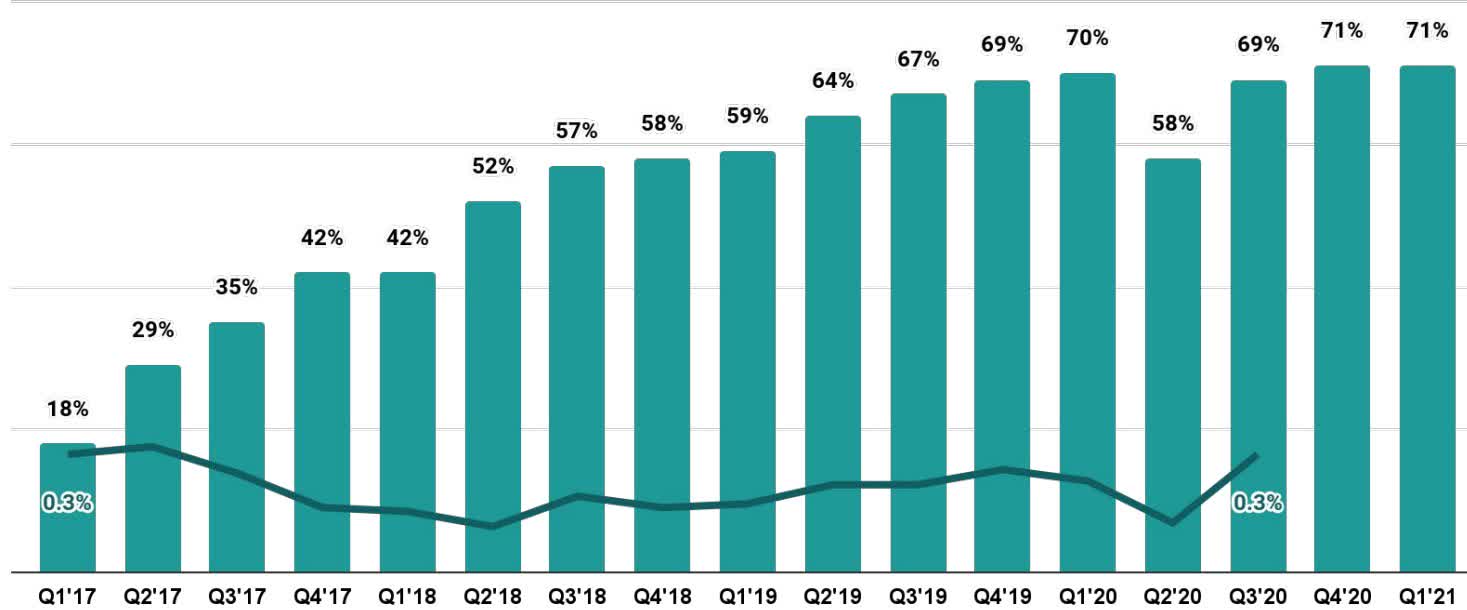

The other benefit that consumers get when applying for a loan through Upstart is the highly automated and digital experience. As of the latest third quarter 2022 results, Upstart has continued to push automation to record levels at 75% of loans being fully automated. For those following the Upstart story for the first time, their focus and progress on automation has been stellar, in my view, as can be seen in the figure below (18% fully automated loans in the first quarter of 2017 compared to the 75% fully automated loans as of third quarter of 2022). This high level of instant approvals through a highly automated process have been a result of continuous improvements to the AI models and the loan process, which has resulted in a better customer experience.

Improving automation levels of Upstart (Upstart IR)

Benefits to Upstart’s bank partners

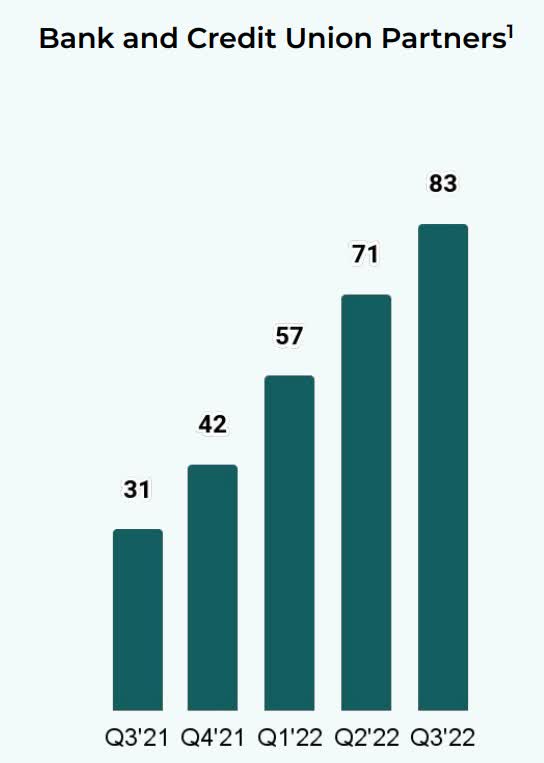

The one validation and evidence of how Upstart really does bring real benefits to bank partners is through the number of bank partners Upstart has managed to attract and retain over the years. In the third quarter of 2022 alone, Upstart added 17 new banking partners, compared to the 17 banking partners Upstart added in the whole of 2021.

Upstart’s 3Q22 banking partners (Upstart IR)

The first benefit for Upstart’s bank partners is really a cost-efficient way to provide a digital lending experience. At the end of the day, there are many regional banks and credit unions that are looking to remain competitive against their larger peers. However, larger banks typically have a huge technology budget, and these smaller regional banks and credit unions often only have a small fraction of this to spend on technology. As a result, Upstart provides this competitive digital lending experience without the need for heavy spending or to match the technology budgets of larger banks.

Secondly, Upstart helps to expand its bank partner’s customer base by referring customers that apply for loans through its platform to its bank partners. At the end of the day, this helps bank partners gain and expand their customer list and also grow loan volumes over time.

Lastly, Upstart claims to have a lower loss rate on its own model when compared to other large United States bank models. The results of Upstart’s own internal study found that its own AI model could help these banks lower loss rates by almost 75% while still maintaining approval rates. This is an internal study, but if true, this shows what kind of improvements its bank partners can expect compared to their own models.

Marketplace model drives network effect

At the end of the day, Upstart’s AI models continue to use data and information from each of its bank partners. With each Upstart-powered loan, I think that we will see improving network effect benefits as Upstart’s AI models continue to improve as it gets trained on ever increasing volumes of data. With each Upstart-powered loan, Upstart’s model accuracy should theoretically improve as more data incorporated helps Upstart’s AI models to reflect the true risk of a loan.

With more consumers and banking partners entering the ecosystem, Upstart’s network effect grows, and the company’s competitive advantage improves, differentiating itself from competitors.

The marketplace model has enabled Upstart to grow rapidly and scale up quickly. For loans that exceed Upstart’s bank partners risk objectives and capacity, these are typically then sold to Upstart’s network of institutional investors. As a result of this marketplace model, Upstart did not need to take balance sheet risk and this enabled Upstart to grow at a rapid pace.

As of the 2021 annual report, 16% of loans that were funded through the Upstart platform were retained by the originating bank while 80% were purchased by Upstart’s network of institutional investors. These investors invest in Upstart-powered loans through multiple ways, including investments in asset-backed securitizations, whole loan purchases or purchases of pass-through certificates. Cross River Bank originated loans have been known to take up a large part of whole loans that are sold to institutional investors, representing 55% of loans on the Upstart platform, while another bank partner accounted for 36% of loans on the Upstart platform. This does highlight some form of concentration risk given that these two partners made up almost 90% of loans on the Upstart platform in 2021. With a growing number of bank partners and new bank partners added each year, we will likely see further diversification of Upstart’s loan mix in the future.

Upstart’s strategy for growth

For Upstart, while valuations may appear relatively inexpensive, the fact remains that it is in growth mode and as a company with a market capitalization of only about $1 billion, the management team continues to look to the long term to grow the business. I think that we need to understand Upstart’s growth strategy to appreciate how Upstart will eventually be a much bigger company than it is today.

The first way that Upstart seeks growth is through improving its technology and AI model. This has been its traditional way of growing since inception, particularly for the personal loans segment. By driving improvements in the AI model and bringing technological upgrades, the company managed to drive growth this way in the early years. The improvements in the AI model leads to things like increasing levels of automation, higher rates of approvals and improved loan offers. What these improvements do is to increase the total number of funded loans and as the accuracy of Upstart’s models improves, Upstart is able to re-target and approve these consumers who were not previously eligible for a loan.

The second way is for Upstart to grow is to increase the efficiency of funding. One way of reducing the cost of funding for Upstart is to improve the confidence that bank partners have in Upstart’s models. This will in turn result in loosening of some of the constraints that Upstart’s banking partners have chosen to put in their lending program. Another way to increase the efficiency of funding is by attracting more banks into the Upstart platform or by increasing the budgets of existing partners for Upstart-powered loans, this can drive a reduction in the cost of funding for Upstart-powered loans. Lastly, cost of funding can also improve as the credit performance of Upstart-powered loans shows relative strength in different market conditions.

The third strategy for growth for Upstart is for its bank partners to offer Upstart-powered loans on their own websites instead of being referred via Upstart.com. Over time, as more banks distribute Upstart-powered loans, this will help the company have a broader reach and extend its offerings to more customers.

Lastly, Upstart’s long-term growth strategy is to expand into new products outside of personal loans. While the personal loans segment may be one of the fastest growing segments in consumer credit in the United States, this is only the first market in which Upstart seeks to bring innovation to. As Upstart reaches maturity and scale in the personal loans segment, it can then use its learnings from the segment to penetrate into new credit verticals, using its AI models and technology to bring innovation to these new credit verticals. As mentioned earlier, Upstart is looking to expand from its current personal loans segment into other segments like auto loans, small business loans, mortgages and other segments in the future. These segments will be rolled out at full steam at different stages, with auto loans being the next likely growth driver after the personal loans segment.

Final thoughts

I am buying Upstart for The Barbell Portfolio.

Do I know if this is the absolute bottom for Upstart? I think that when valuation for the company is this cheap given the company’s forward P/E multiple is at 10x, I am of the view that investors have sufficient margin of safety going into Upstart today.

The company remains a fundamentally strong business in my view. Management continues to execute on its long-term growth strategy, while maintaining its emphasis on a marketplace model. Upstart’s value proposition remains strong even in a downturn and when the macro backdrop improves and funding is no longer a constraint, Upstart will be like a coiled spring ready to bounce once again.

Be the first to comment