bloodua

In early July, United Maritime Corporation (NASDAQ:USEA) or “United” completed its spin-off from Seanergy Maritime Holdings Corp. (SHIP) or “Seanergy” to “pursue a diversified business model and greater exposure to different shipping segments“.

The company wasted no time expanding its fleet and just days after the spin-off announced the “accretive” purchase of four second-hand vessels for an aggregate purchase price of $79.5 million:

- two Aframax crude tankers built in 2006 and

- two LR2 product tankers built in 2008

Indeed, charter rates have been decent for both crude and product tankers in recent months which in combination with Russia’s ongoing efforts to accumulate sufficient capacity ahead of a proposed crude oil price cap contributing to further strengthening second hand vessel prices.

While the initial financing was non-dilutive, the company quickly followed the footsteps of peers Imperial Petroleum (IMPP, IMPPP), Performance Shipping (PSHG), OceanPal (OP), Castor Maritime (CTRM) and Globas Maritime (GLBS) and raised $26 million in gross proceeds in a highly dilutive offering of shares and warrants “for additional accretive transactions aimed at strengthening our presence in the tanker sector“.

But in contrast to above-listed peers, United Maritime surprisingly reversed course in early September by announcing a $3 million share buyback plan:

We believe that the share price of United is significantly undervalued considering the solid vessel valuation and earnings environment of the tanker sector. We aim to enhance stockholder value by using our strong cash reserves and the fleet’s robust cashflow generating capacity. We will continue to examine all strategic alternatives and to invest opportunistically, including through buybacks under appropriate conditions.

Within just three weeks, United managed to repurchase 1.86 million or approximately 20% of the company’s outstanding common shares at an average price of $1.61 and immediately authorized an additional $3 million buyback.

Two weeks ago, the company flipped the two Aframax tankers at an estimated 70% gain within just three months:

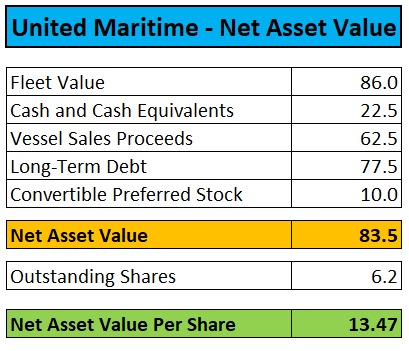

The Company has entered into two separate definitive agreements with an unaffiliated third party for the sale of its two Aframax vessels, the 2006-built M/T Bluesea and the M/T Parosea. The vessels are scheduled to be delivered to their new owners within the fourth quarter of 2022. The aggregate gross sale price is approximately $62.5 million and the transactions are subject to customary closing procedures.

On Tuesday, the company announced the completion of its second buyback program and authorized an additional $3 million repurchase.

So far, United has bought back an aggregate 3.3 million or almost 35% of the company’s outstanding common shares at an average price of $1.81 per share.

Ongoing repurchases in combination with massive appreciation in the second hand tanker markets have resulted in net asset value (“NAV”) per share more than tripling since the dilutive equity raise in late July to an eye-catching $13.47 per share.

Compass Maritime / Company Press Releases

Assuming the company manages to buy back another one million common shares, NAV per share would increase to approximately $15.50.

That said, while the funds from the sale of the Aframax tanker pair will provide United with almost unlimited buyback capacity, I would expect the company’s repurchase efforts to become somewhat less aggressive going forward as the warrant overhang is coming into play.

Remember, the July offering also included 8 million warrant sweeteners exercisable at $3.25. Full exercise would result in NAV per share dropping by more than 40% to approximately $7.70.

With United Maritime having been established as a growth vehicle, it is difficult to see the company buying back shares above the $3.25 warrant exercise price but on the flip side, highly elevated second hand market prices are likely to prevent United from acquiring additional vessels in the near term.

If the company is indeed serious about creating additional shareholder value, I would expect United to redeem the $10 million in outstanding 6.5% Series C Convertible Preferred Stock held by former parent Seanergy Maritime.

Bottom Line

United Maritime’s great fleet expansion timing and aggressive share repurchase efforts have more than offset the dilution suffered from the July offering.

Given elevated second hand tanker markets, I do not expect the company to acquire additional vessels anytime soon which should provide more room for share buybacks and particularly the near-term redemption of its 6.5% Series C Convertible Preferred Stock.

In light of recent equity holder-friendly moves and with shares still trading at an 80% discount to NAV, I am tempted to double-upgrade the stock from “Sell” to “Buy” but with the warrant overhang coming into play, I am raising my rating by one notch to “Hold” for now.

Be the first to comment