Ekaterina Klishevnik/iStock via Getty Images

United-Guardian (NASDAQ:UG) is an American manufacturer of chemical components used in cosmetics, pharmaceutical and medical applications.

The company sustains high margins on a few core products sold through marketing partners. Recent revenue drops, added with losses on its securities portfolio, made the stock price fall.

Although the company might be able to recover its profitability, I believe its core business is under threat. Even considering a return to normal profitability, current prices imply a high multiple for a business that has remained stagnant for a long time.

Note: Unless otherwise stated, all information has been obtained from UG’s filings with the SEC.

Business description

UG’s star products: The company obtains 60% of its revenues from different lines of the cosmetic/pharmaceutical chemical Lubrajel. It is used by manufacturers as a moisturizer, and can be created using different ingredients (more industrial, more natural, etc.).

Another 34% of revenue is obtained from Renacidin, a prescription drug used to prevent calcification in urethral catheters and the urinary bladder.

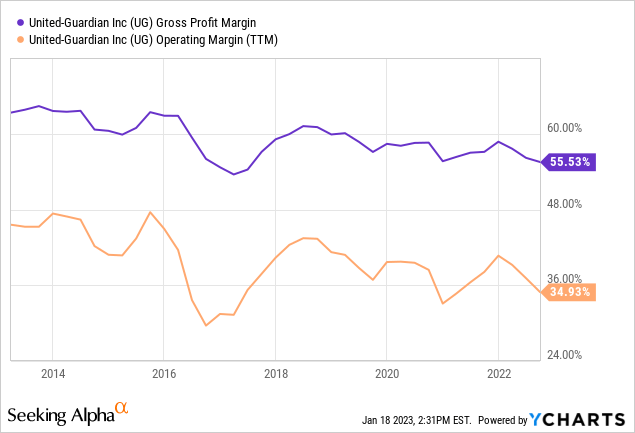

High margins on a lean structure: UG commands a high gross and operating margin that has been maintained for a long time.

These margins account for the strength of the Lubrajel brand. Despite being an unpatented (since 2019) chemical component, it is listed in several websites specialized in makeup and skincare.

Another evidence of UG’s product competitiveness is the fact that almost 50% of its sales are directly or indirectly generated in foreign countries, including 15% coming from China (according to the company’s 10-K for FY21). Again, this is despite the fact that UG does not have patents on the products it sells.

On top of the product’s strength, UG has a small, lean structure. It only has 24 employees, 16 of which work in R&D and manufacturing. The company sells through wholesalers and distributors. One of those distributors, Ashland (ASI) accounts for 40% of its revenues.

Competition from cheaper competitors: UG comments that it has faced competition from lower cost competitors, particularly from Asia. This situation is not easily seen at the margin level, although it might have something to do with the recent fall in revenue.

Financially strong: UG has no debts, $7.5 million in securities (mostly bond mutual funds) and a 50 thousand square building in Hauppauge, New York, that is completely depreciated.

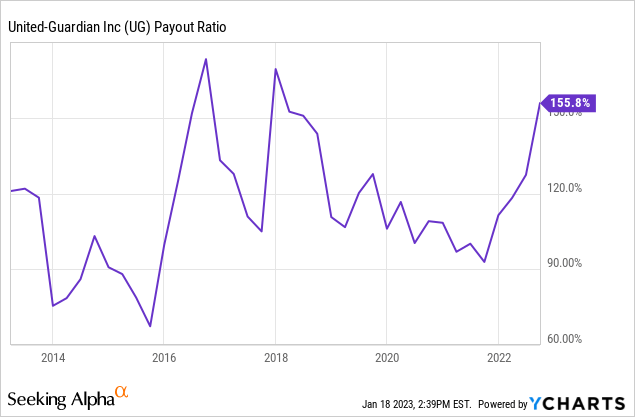

High dividend payout rate: Without much investments in capacity or expansion, the company has returned most of its net income in the form of dividends. On many occasions, its dividend payout rate has been above 100%.

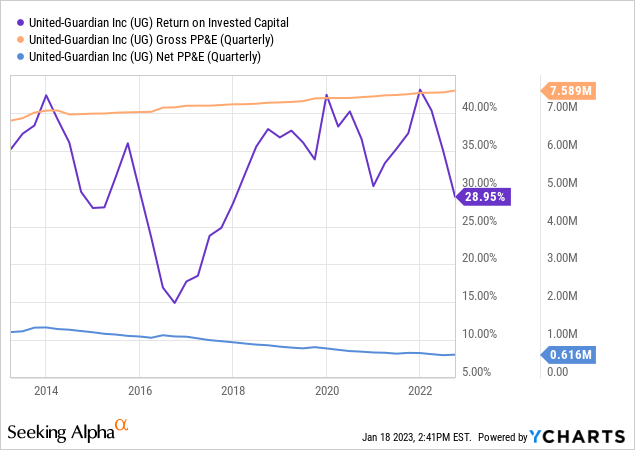

High although overstated ROIC: With high margins, a lean structure, and consistently returning capital, the company generates a high ROIC. This figure is somewhat overstated though, because the company’s assets are almost completely depreciated.

Recent developments

The securities portfolio takes a dive: UG’s securities portfolio, mostly invested in bonds, took a severe hit in 2022. For the 9M22 period, the company posted $1.15 million in FV losses, against none during 9M21. In my opinion, this is noise, given that the company did not take an aggressive investment strategy and that this is non-operating income.

Revenues in cosmetics down: For most of 2022, the company did ok. Revenues were up and operating profits a little down. However, for 3Q22, the company posted a significant fall in cosmetic sales, its biggest line. Revenues were 50% lower than one year ago.

The company argues that the reason was a temporary oversupply of its distributor in China, ASI. However, sales to other distributors in other regions also fell, even more, 65% cumulatively. Also, ASI sales in Asia-Pacific grew during 3Q22 (although not everything ASI sells is produced by UG).

Change in historical management: Just two weeks before posting the 3Q22 results, UG announced the resignation of its CEO, Chairman and largest shareholder. He had been with the company since 1983, and is the son of the company’s founder. He was replaced by an external manager with experience in cosmetics.

The 2016 experience: The change in CEO, added to the fall in revenues, plus the active search for strategic opportunities, may all signal problems at the business level.

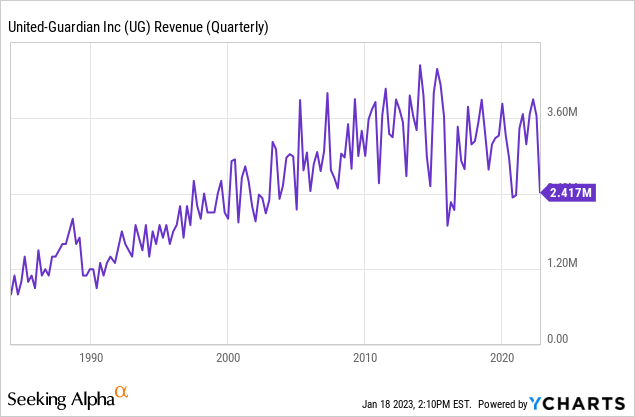

Interestingly, UG’s profile changed after 2016, as can be seen in the chart below. The company’s revenues fell sharply, never to return to the same level, and indeed losing its previous growth trend.

A reading of the 10-K for FY16 reveals that at the time the company also blamed the fall in revenues on slower demand from China through its distributor ASI. However, cosmetic revenues, which had reached $10 million in FY15, never returned to the previous level.

Valuation

We have seen that UG has some very desirable characteristics: financial strength, high returns on capital, and high margin. It also shows deteriorating conditions and difficulties to sustain its revenues.

The company may start implementing significant changes in the following quarters given its change of leadership. This adds volatility to future earnings.

I believe UG is overvalued at current prices, because its business quality is deteriorating, its future developments are highly uncertain and it trades at a high current or historical multiple.

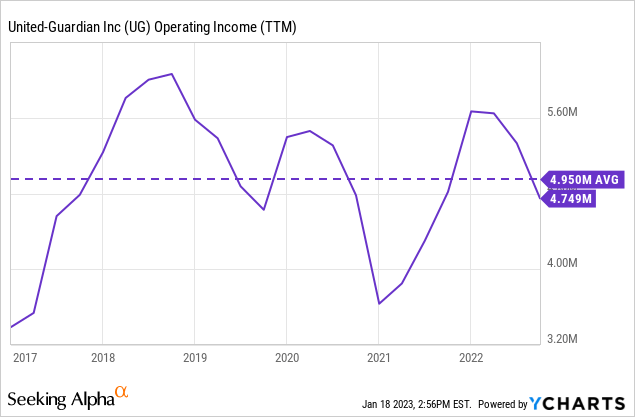

Even if the reader considered that UG can return to normal operating income (considered for the after FY16 period), then the company promises $4 million in net income (the average $4.95 by 80% to account for taxes). At current prices that is a multiple of 13 on earnings.

Considering that the return to the average is uncertain, and that even with a return to averages the business is still threatened, I prefer to pass on UG.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment