Bloomberg/Bloomberg via Getty Images

Introduction

It’s time to dive into Union Pacific’s (NYSE:UNP) fourth-quarter earnings. These matter for at least two reasons:

- They tell us a lot about how Union Pacific is doing, which is important for traders and investors buying UNP for capital gains and dividends.

- As UNP is America’s largest stock-listed railroad, its outlook and comments reveal a lot about the state of the US economy, as well as global trends impacting US imports and exports.

There is both bad and good news. The bad news is that the company missed both revenue and EPS estimates, as economic weakness and high costs weakened shipments and operating profitability. The outlook also remains highly uncertain as the company sees industrial contraction and other headwinds.

Moreover, operating efficiency ratios were weak as the company continued to adjust to post-pandemic volumes.

The good news is that the company remains in a good spot. It has a healthy balance sheet, it is highly dedicated to shareholder returns, and stock price weakness provides buyers like me with new opportunities. While I believe that downside risks remain high, I’m eagerly waiting to pull the trigger this year.

Now, let’s dive into the details!

4Q22 Was Not Great – As Expected

In one of my last (Union Pacific) articles of 2022, I wrote that 2023 would be a weaker year in terms of economic growth. However, this would also come with new opportunities.

[…] we discussed the high likelihood of more economic weakness in 2023. The Fed will have to keep fighting inflation, even as we have already entered an economic downswing with an almost certain recession.

While that won’t be a lot of fun for my portfolio, it is great news for long-term investors looking to buy value in 2023.

Unfortunately, Union Pacific’s earnings confirmed all of this.

Union Pacific

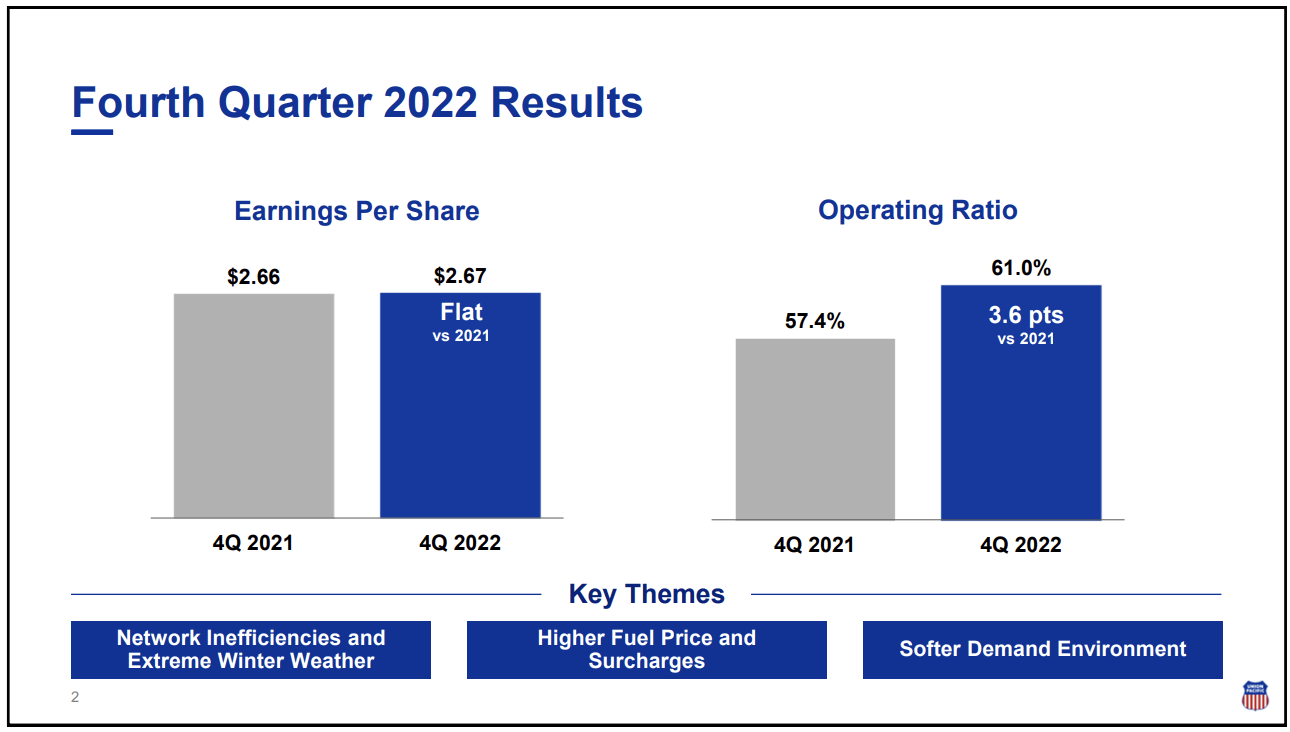

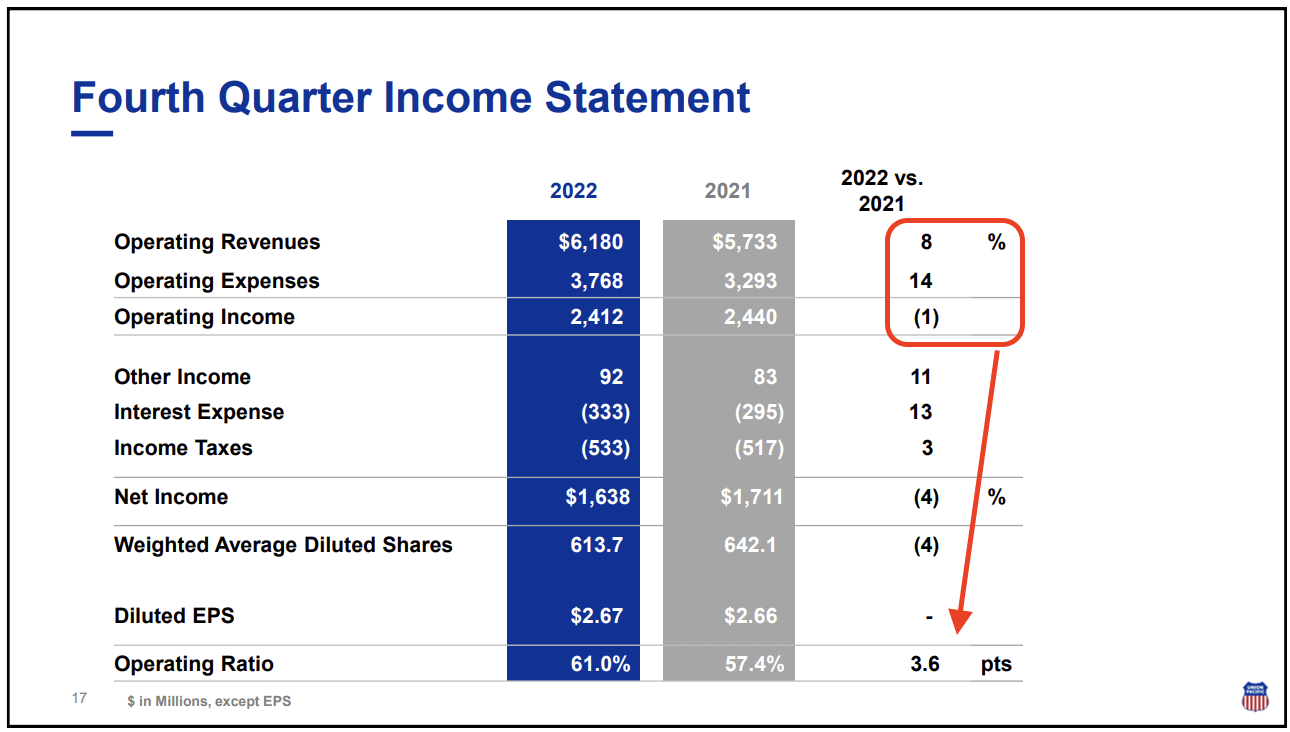

The company reported $6.2 billion in 4Q22 revenues, which is 8.2% higher compared to the prior-year quarter and slightly ($60 million) below estimates. GAAP EPS came in at $2.67, which was $0.11 below estimates.

On a side note, we’ll also discuss freight revenue in this article. That number is slightly higher than total revenues due to the “other” segment. So, please don’t let that confuse you when you see two different revenue growth numbers.

Total Shipments Were Weak

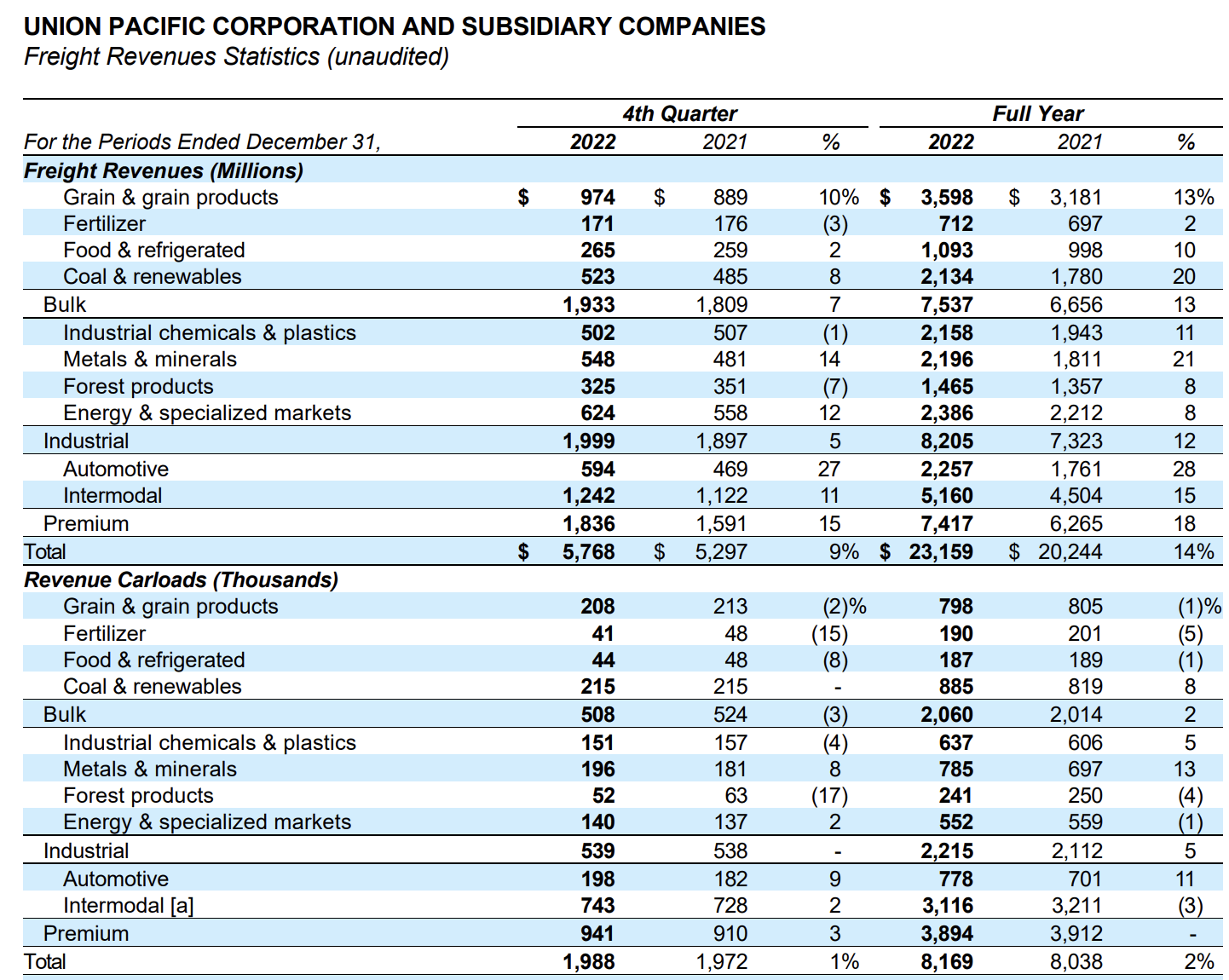

8.2% revenue growth doesn’t scream weakness. However, we do see some weakness in total shipments. The company reported a 1% increase in its total carloads. This is down from 3% growth in the third quarter.

Union Pacific

In bulk, the company faced headwinds due to service and weather challenges and weaker potash shipments. I expect shipments to pick up due to increasing production in Canada and high export demand. Moreover, the company continued to benefit from coal tailwinds, which caused shipments to remain flat despite economic weakness.

Industrial shipments were flat as metals and energy more than offset the weakness in industrial goods and energy. Much weaker economic growth pressured industrial demand, while construction growth supported metals. Housing construction, however, did not see growth, as lower demand pressured forest product shipments.

Premium shipments were up 3% thanks to growth in both automotive and intermodal. Automotive shipments continued to benefit from easing supply chain bottlenecks allowing producers to turn backlog into finished vehicles. Higher international intermodal shipments more than offset softening intermodal demand.

Higher Operating Costs Offset Pricing Gains

As the overview above shows, the company generated 9% higher freight revenues. All segments generated growth led by premium, which benefited from both higher shipments and strong pricing.

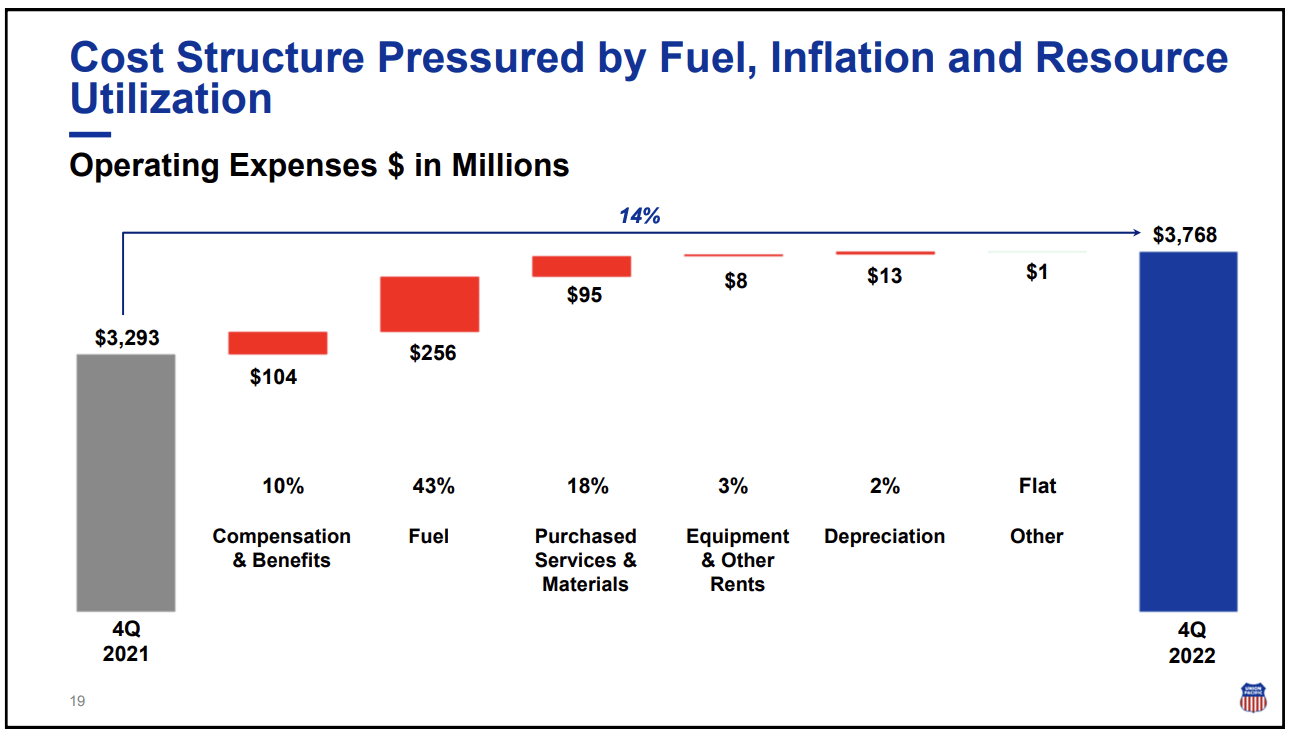

Unfortunately, these gains were more than offset by a 14% increase in operating expenses. This pushed the operating ratio to 61.0%, an increase of 360 basis points.

Union Pacific

So, what happened?

First of all, this is the breakdown of the 9% freight revenues growth rate:

- Volume: +0.75%

- Fuel surcharges: +8.5% (revenue growth is almost entirely based on fuel surcharges).

- Price/mix: -0.25%.

This is what the breakdown of operating expenses looks like:

- Compensation & benefits: +10%

- Fuel: +43%

- Purchased services: +18%

- Equipment & other: +3%

- Depreciation: +2%

Union Pacific

These prices were also impacted by network inefficiencies in the form of higher overtime and borrow-out costs, which brings me to the next topic.

Network Inefficiencies

One of the things we discussed last year is railroad network inefficiencies. This started during the pandemic when railroads responded to imploding transportation volumes by laying off employees and taking equipment offline. It was the right thing to do. After all, nobody knew when demand would rebound again.

Fortunately, demand rebounded quickly when the first wave of lockdowns ended. The problem is that railroads (and almost all companies in every supply chain) were not prepared. They had to bring back equipment and accelerate hiring. Unfortunately, the labor market was tight, and demand growth was much higher than anticipated.

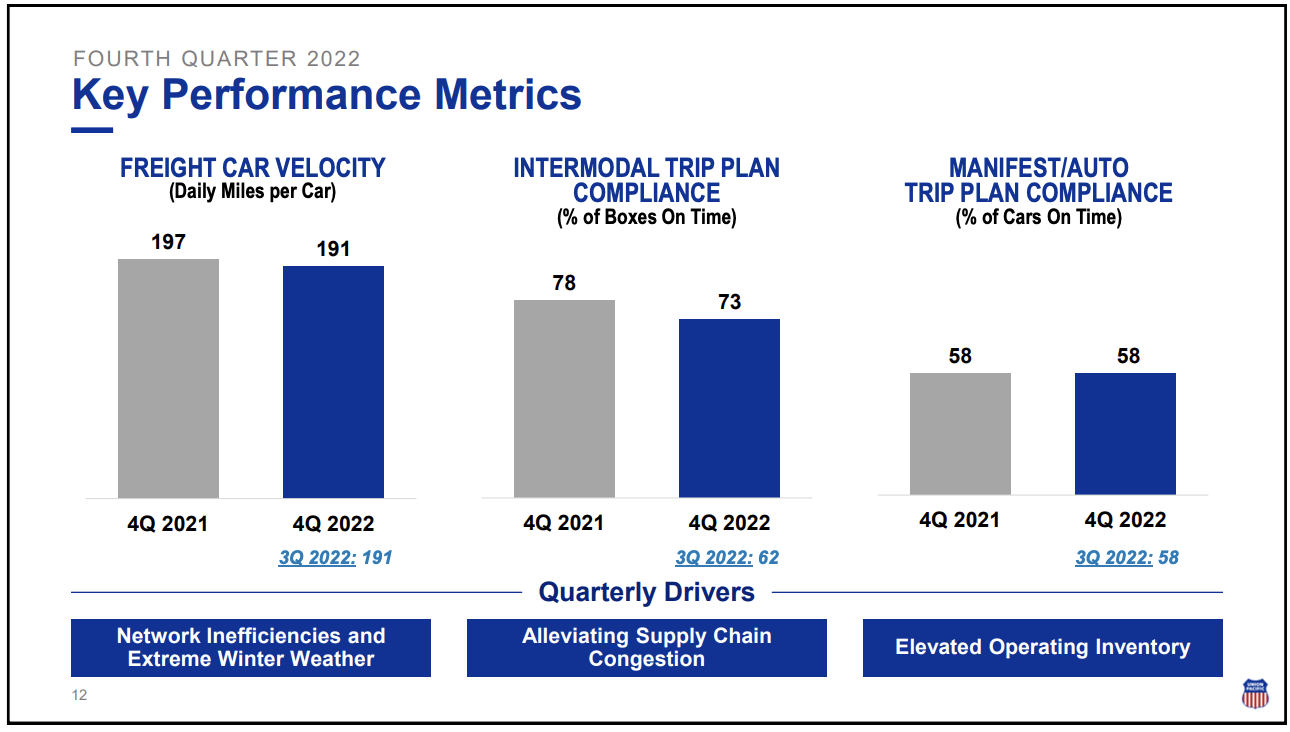

Union Pacific is still struggling with these issues. The fourth quarter wasn’t much different.

- Quarterly freight car velocity fell by 3%.

- Quarterly locomotive productivity declined by 5%.

- The average train length declined by 1%.

- Quarterly workforce productivity declined by 3%.

Union Pacific

The good news is that the company did not see a deterioration in its on-time performance. Intermodal trip plan compliance improved by 11 points versus 3Q22 as supply chain congestion alleviated. This resulted in fewer stacked containers at inland ramps.

Union Pacific

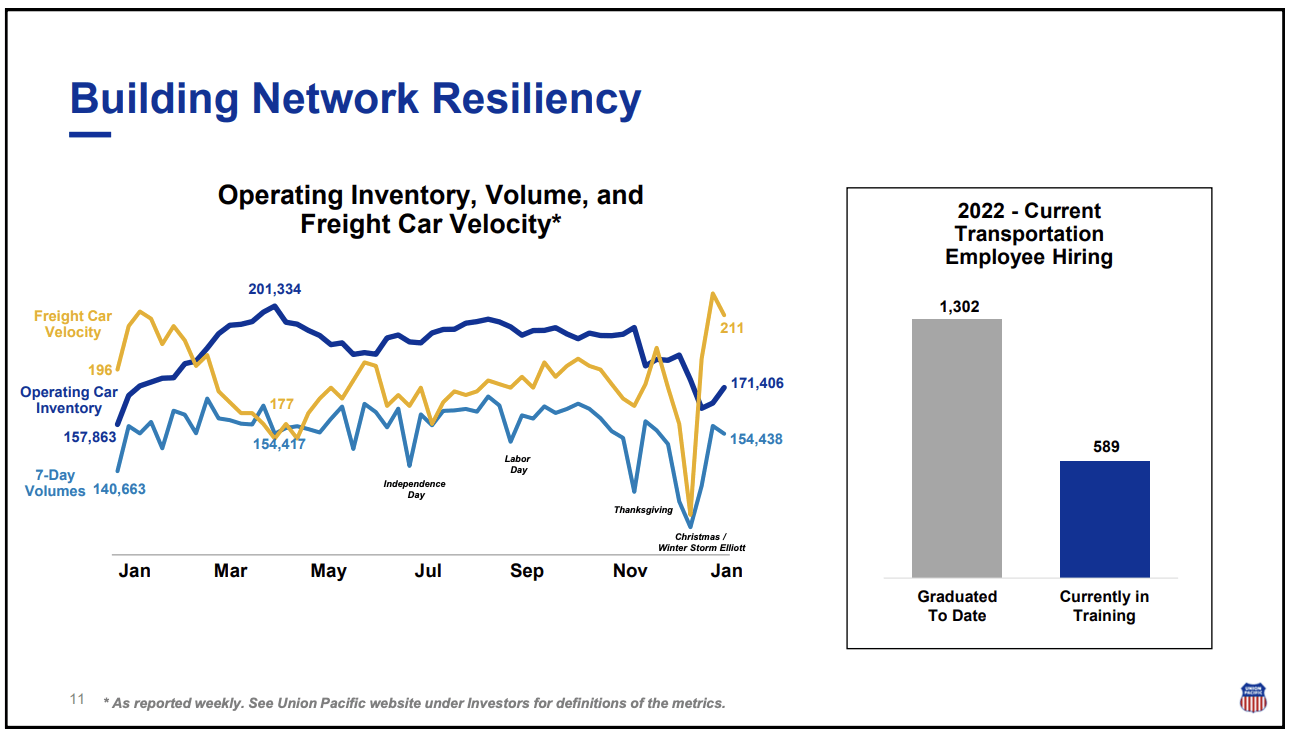

Our attention throughout 2022 was focused on onboarding the necessary crew resources to operate a fluid network and meet customer demand.

[…] We currently have around 600 employees in training as our pipeline is significantly stronger than it was a year ago. That being said, our hiring efforts will continue in 2023 as we backfill for attrition and target locations across the northern region, where crude challenges persist. In the near term, we will continue to utilize borrow outs to supplement crew shortfalls. – Union Pacific

Cash Generation, Capital Spending & Dividends

In 2022, UNP generated $9.4 billion in operating cash flow. While this is up from $9.0 billion in 2021, the cash conversion rate dropped by 9 points to 82%.

Free cash flow dropped to $2.7 billion. This decline of roughly $700 million was caused by higher spending requirements as a result of the aforementioned challenges.

The company used its balance sheet as well to distribute cash, as $9.4 billion in cash was distributed to shareholders.

- Dividends: $3.2 billion, +10% versus 2021.

- Buybacks: $6.3 billion, 5% of shares outstanding.

Adjusted debt rose from $31.5 billion to $35.0 billion. The leverage ratio rose from 2.7x to 2.9x. The company remains A-rated by all major rating agencies.

While using debt to buy back debt isn’t sustainable, the company knows it has a healthy balance sheet. It wants to use this to its advantage. This means that the company will cease buybacks the moment it runs into bigger headwinds.

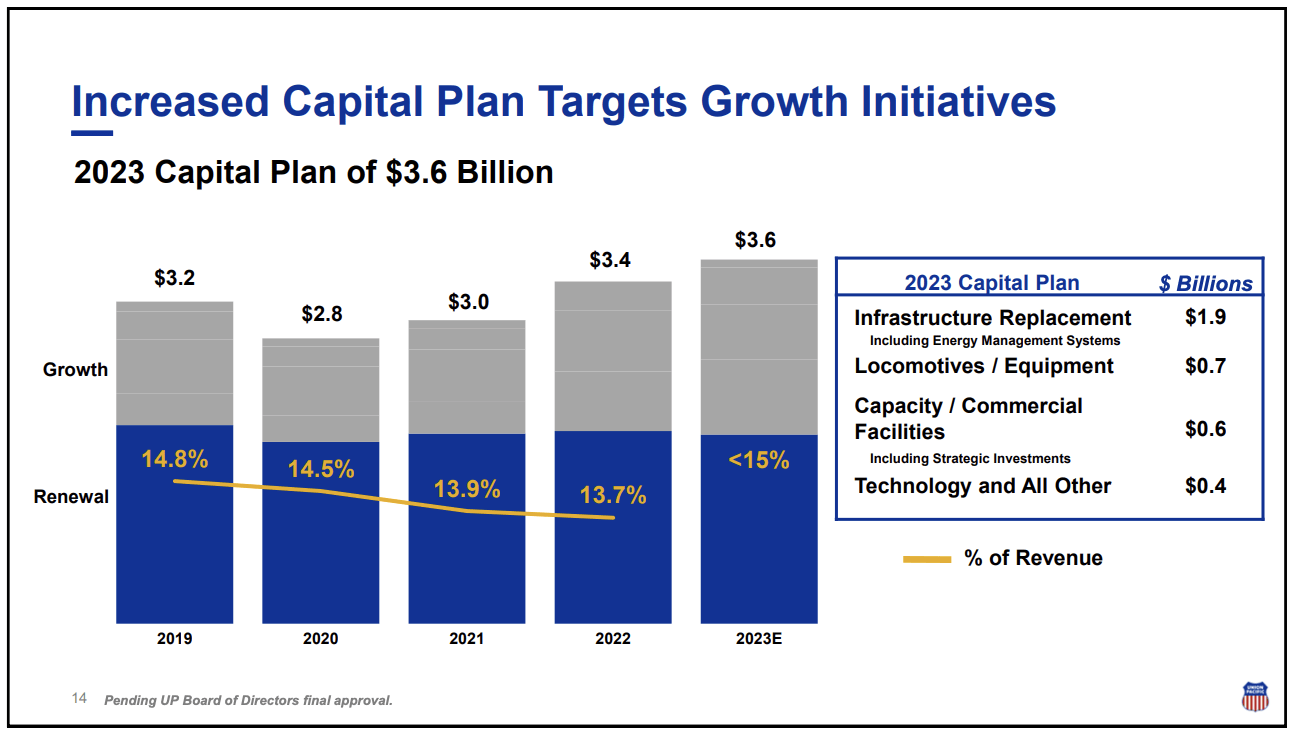

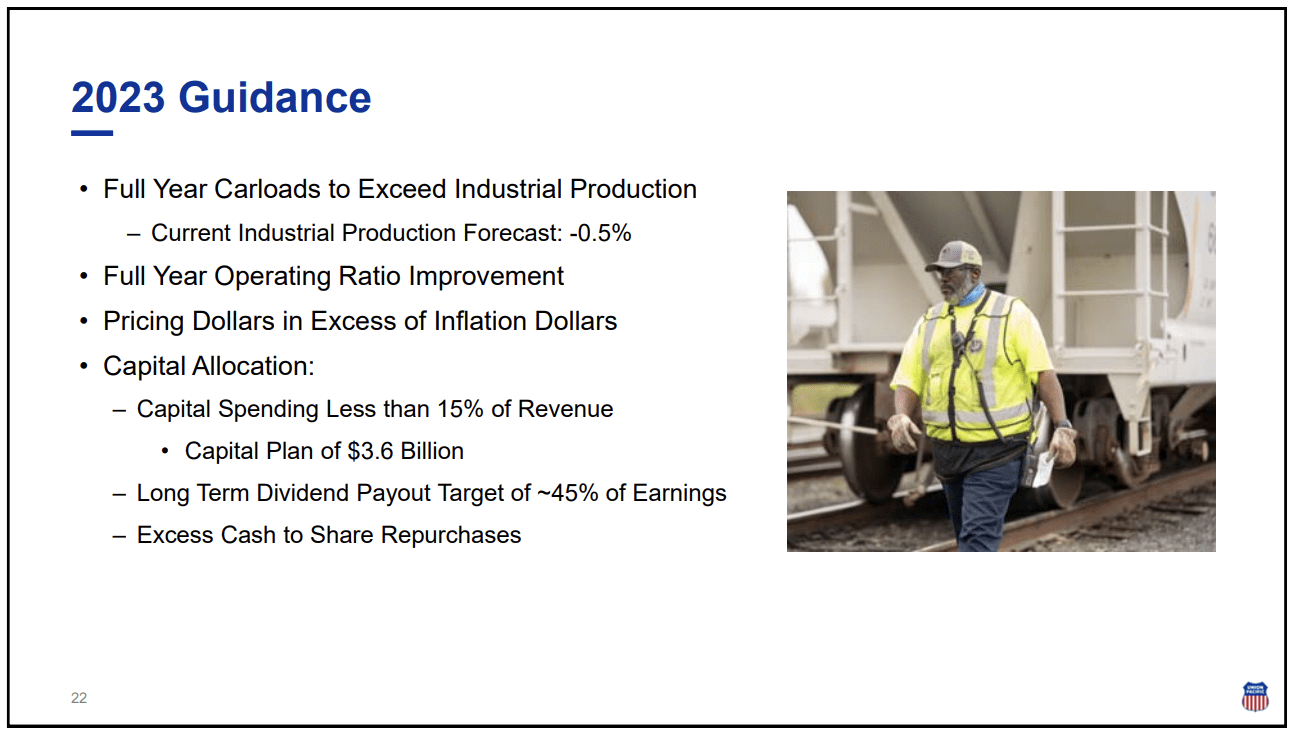

In 2023, the company plans on boosting capital spending to $3.6 billion. Roughly half of this will flow toward growth projects.

[…] in addition to a higher inflationary environment, the elevated capital spending will be driven by increased locomotive spending of $175 million. With 430 modernized locomotives currently in the fleet, we will bring the total modernized to over 1,000 by the end of 2025. These modernizations not only help build resiliency into the network through enhanced reliability and productivity, but also further the progress towards our carbon emission reduction goals.

Union Pacific

The good news is that the company expects to maintain CapEx spending of less than 15% of revenue.

Outlook – Embracing Weakness

Are we going to get a soft landing? Are we going to get a full-blown recession?

Like most, I don’t know. Even the ones who claim to know the answer don’t know.

However, I’m assuming that a soft landing will be hard to achieve. I don’t see how the Fed can reduce inflation to 2% and keep it at 2% without hurting economic demand. After all, the only way to get sticky inflation down is to do some serious damage.

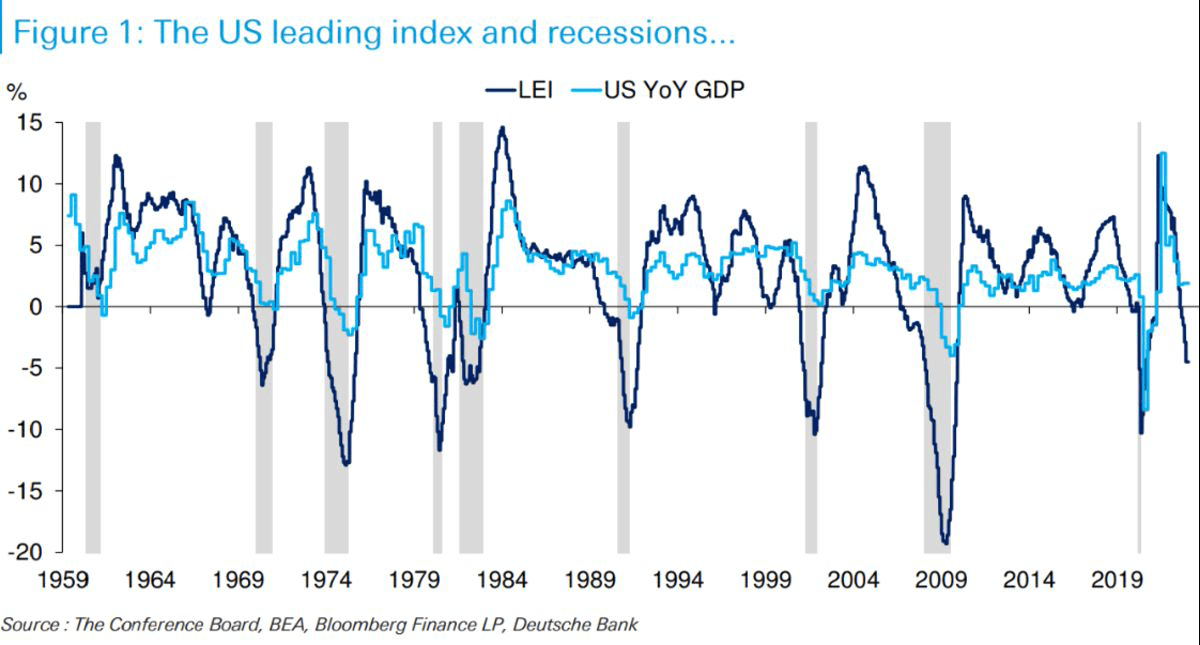

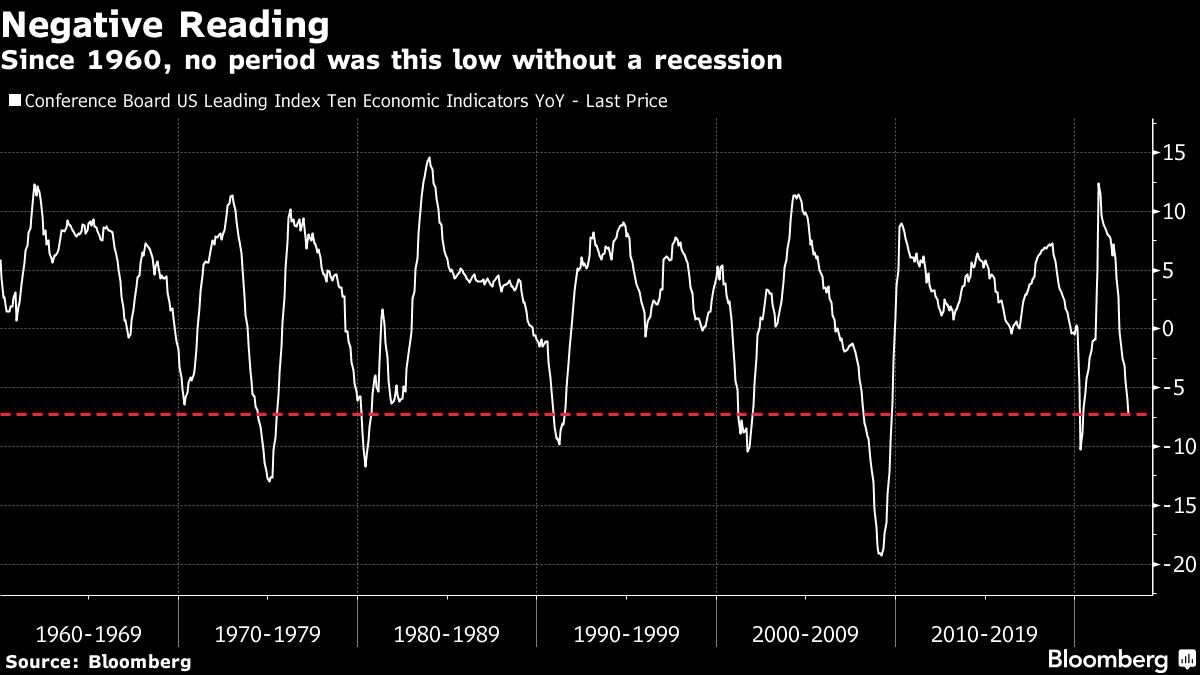

For now, leading indicators like the Conference Board’s LEI indicate a very high likelihood of a recession.

Deutsche Bank

As Bloomberg writes (based on the chart below):

All the points below the dashed red lines were moments of extreme distress for the US: the Yom Kippur War and the oil embargo in the early 1970s, Iran–Iraq war in 1980, Gulf War in 1990-91, dot-com bubble in 2000, the Great Financial Crisis and then Covid-19. Those aside, December’s reading was weaker than more than 92% of all data-points since 1960, Bespoke noted. This may be a lagging indicator, but it doesn’t lag by all that much, and it seems dangerous to ignore it or try to explain it away.

Bloomberg

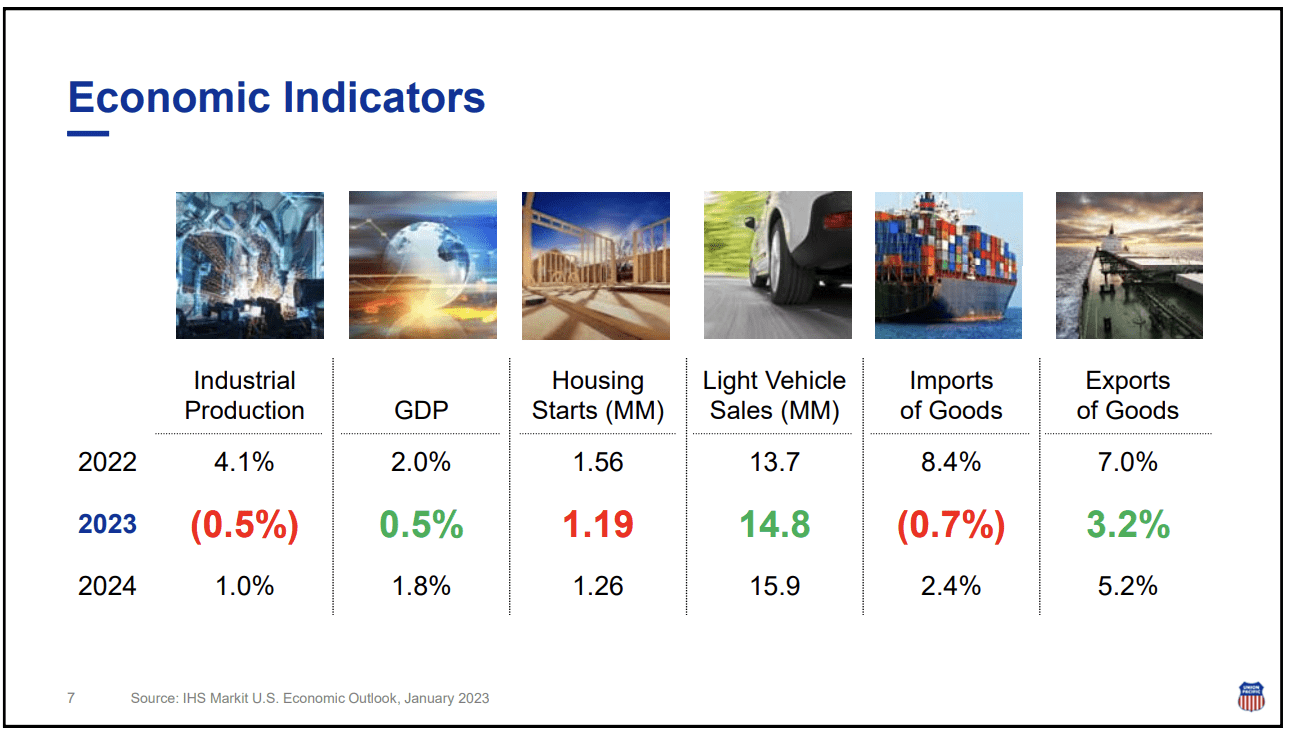

Based on this context, Union Pacific isn’t very upbeat. It did not give a volume outlook. The company expects growth in coal, biofuels, metals, domestic intermodal, and automotive. It sees flat demand in international intermodal and a contraction in grains, industrial production, and forest products.

This is based on the following macro assumptions:

Union Pacific

As the data above shows, the company does not see a full-year GDP contraction. In this case, it’s in line with estimates from major banks.

The company also expects to outgrow industrial production, improve its operating ratio, achieve above-inflation pricing, and maintain a dividend payout ratio of roughly 45% of its earnings. Excess cash will be spent on buybacks.

Union Pacific

According to the company:

[…] we have some challenges with industrial production, imports and housing starts. However, we remain optimistic that we will be industrial production with our strong focus on business development.

[…] we expect the entire intermodal market to be challenged, both international and domestic by high inventory levels, lower truck rates and temper consumer spending. We expect to outperform that market, however, through our new business with Schneider as well as opportunities to grow with other private asset owners and our strong IMC partners.

As I wrote on Twitter, it looks like the company’s outlook follows the soft-landing thesis. I think that is a major risk, as it would warrant adjustments if the growth-slowing trend does not reverse soon.

So far, the trend is ugly and indicative of more weakness in the industrial sector.

Wells Fargo

However, there are two things worth mentioning:

- Union Pacific has priced in a lot.

- Long-term investors should embrace weakness.

Valuation

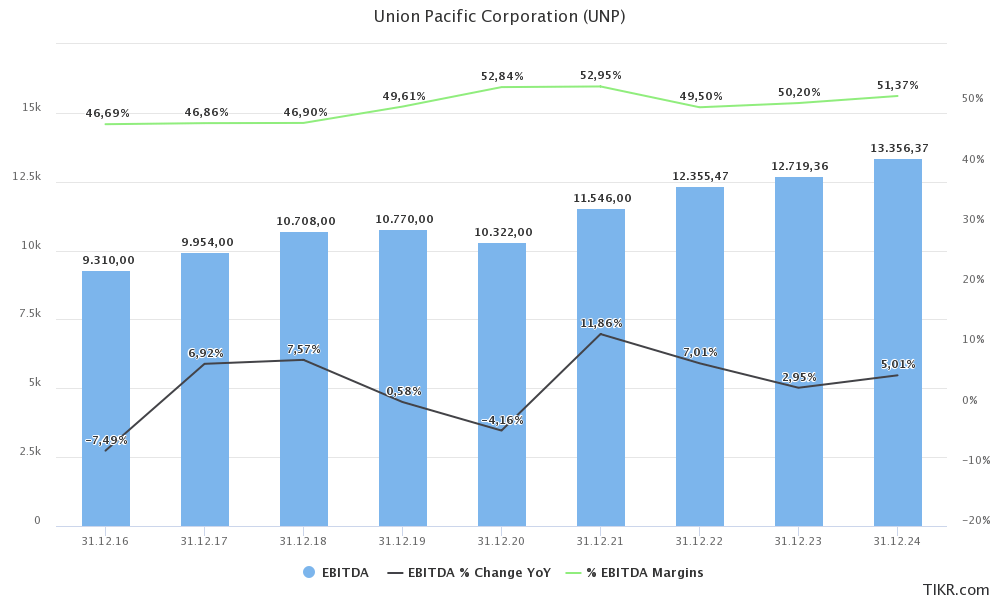

Analysts expect Union Pacific to generate $12.7 billion in EBITDA this year. This would imply a 3.0% growth rate and a 50.2% EBITDA margin. This is in line with above-inflation pricing, a mild industrial downturn, and improving operating efficiencies.

TIKR.com

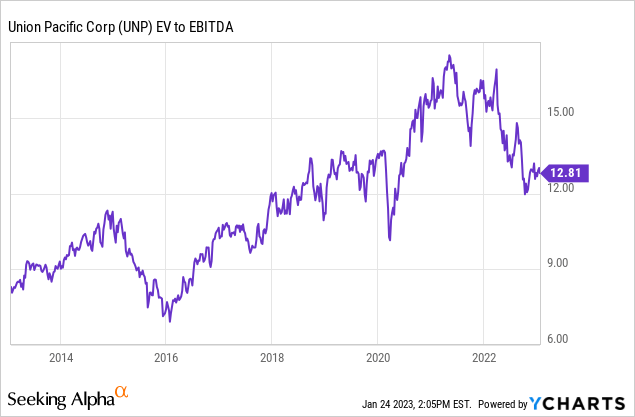

Using 2023E EBITDA estimates and UNP’s $159 billion enterprise value ($125.9 billion market cap, $33.1 billion in 2023E net debt), we get an EV/EBITDA multiple of 12.5x.

As I wrote in December, this valuation is fair, but I think we can get a better valuation.

To quote from my December article:

I will likely buy more aggressively if the stock falls to the $180-$190 range. The only reason I didn’t buy more UNP shares in October is the fact that UNP is already a large part of my portfolio, which required some diversification.

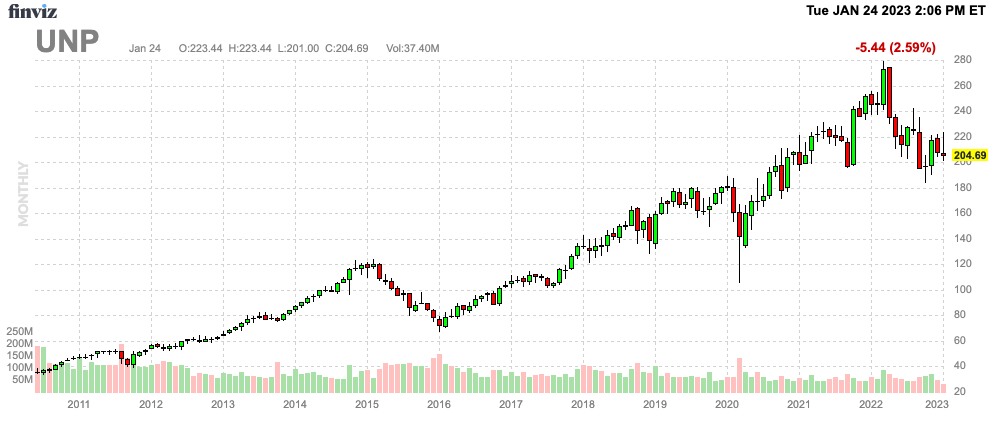

Currently, the stock is 27% below its 52-week high.

FINVIZ

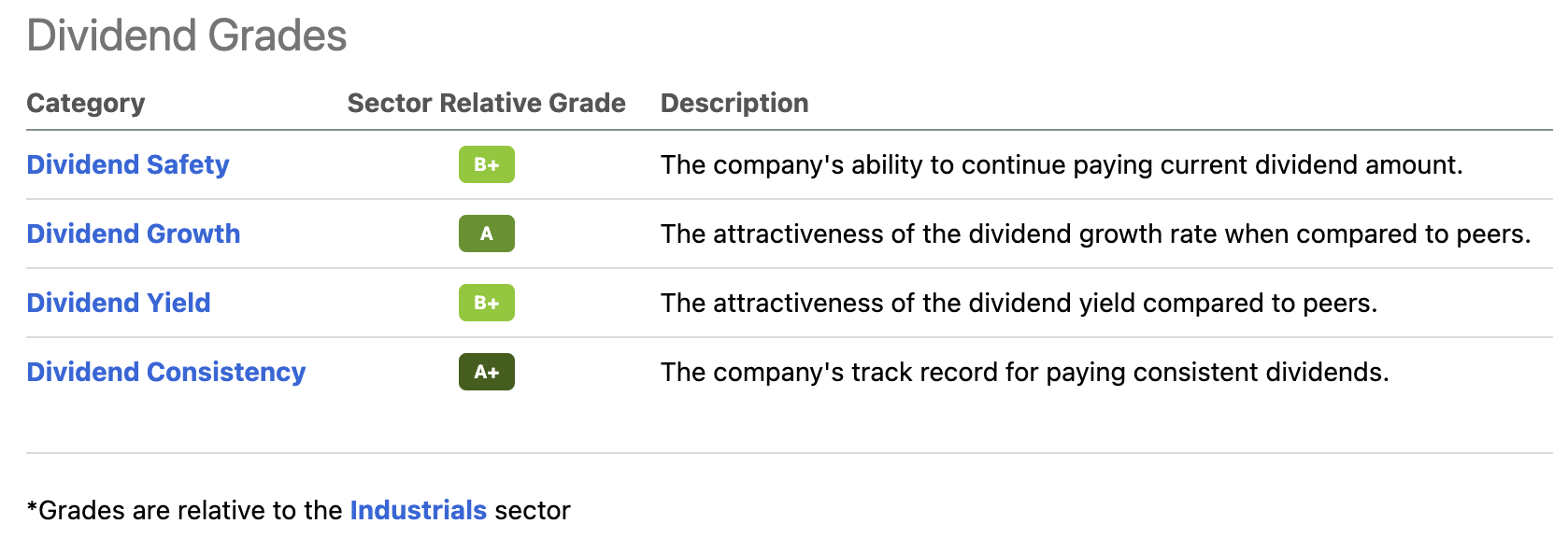

I started buying UNP for my dividend portfolio in 2020. It has been one of my largest holdings ever since.

The company’s qualities as a dividend stock are impressive. UNP yields 2.5% and has had 15.1% average annual dividend growth over the past ten years. That number will slow if the US economy weakens, but as management keeps confirming, shareholders will benefit greatly from the company’s long-term growth.

Seeking Alpha

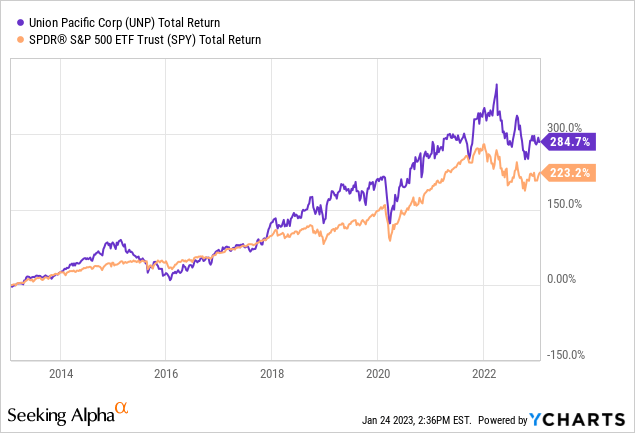

UNP also has a long history of outperformance, despite regular drawdowns during (manufacturing) recessions.

With that said, here are my final thoughts.

Takeaway

Union Pacific’s fourth-quarter earnings were somewhat poor. The company missed revenue and EPS estimates, as rising operating costs outperformed slowing revenue growth.

However, the company maintains a healthy balance sheet, it is dedicated to maintaining dividend growth and buybacks, and operating efficiencies are improving, albeit somewhat slowly.

Going forward, the company expects moderate economic weakness, improving margins, and subdued capital spending growth.

While UNP is already fairly valued, I believe we could see more downside. I even embrace it, as I cannot wait to aggressively add to one of my all-time favorite stocks.

Needless to say, I’ll keep you up to date!

(Dis)agree? Let me know in the comments!

Be the first to comment