JayLazarin/iStock Unreleased via Getty Images

Union Pacific (NYSE:UNP) is the largest railroad in North America. It controls more than 22,000 miles of track and has a dominant position across much of the western United States.

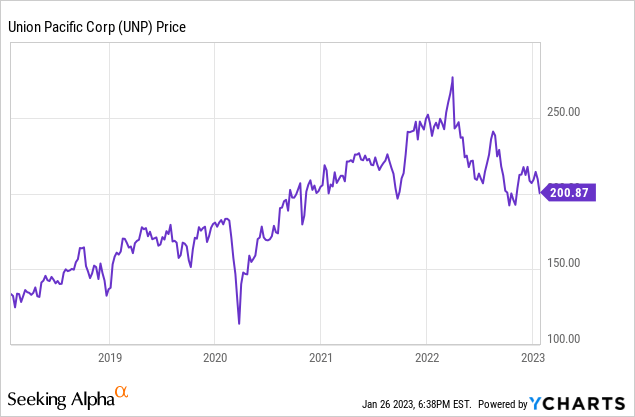

Shares have historically performed exceptionally well. However, the stock has now been flat to down for the past couple of years, with shares now sitting just slightly above where they were prior to the onset of the pandemic:

Sentiment also seems to be fairly muted on Union Pacific. Some investors are understandably nervous about a variety of factors including both macro concerns such as an economic slowdown and more industry-specific worries such as labor problems.

As of the time I’m writing this, the last eight articles on Seeking Alpha about Union Pacific stock have either come with hold or sell ratings. Not a buy to be found among them. I take an opposite stance. I’m of the view that UNP’s stock price has now fallen far enough that shares are likely to outperform the S&P 500 going forward. Here’s why I’m more upbeat on Union Pacific stock for 2023 and beyond.

Growth Won’t Be As Strong As In The Past, But That’s Okay

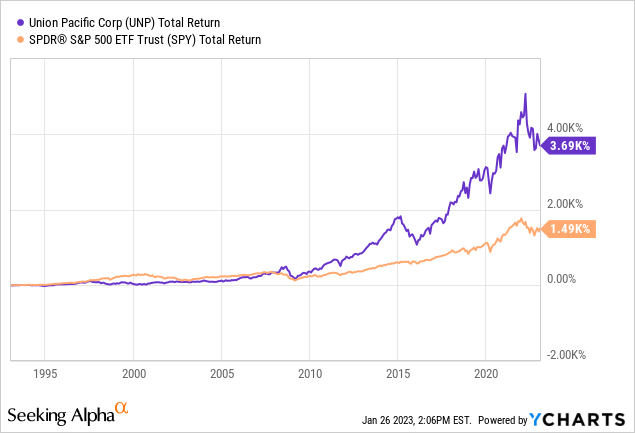

Looking at a long-term chart of Union Pacific (or the other publicly-traded railroads for that matter) gives us the idea that railroads are simply a tremendous industry:

Over the past thirty years, Union Pacific has produced a total return of 3,690%, compared to a rise of 1,490% for the S&P 500 over the same period. Aside from a brief period of underperformance in the late 1990s, Union Pacific has tracked or beat the S&P 500 in almost all subsequent market periods.

The industry bull case is easy to arrive at. Railroads serve as functional monopolies. In many cases, only one rail line offers frequent service to any given city or region, allowing the freight hauler a significant amount of bargaining power with its customers. There are also massive barriers to entry, as there are numerous environmental, regulatory, and capital constraints to launching rival railroad or transportation services.

Railroads also have other advantages such as fuel efficiency. In the year 2000, when gasoline and diesel prices were dirt cheap, this didn’t matter much. However, as the price of oil has soared, railroads have gained a key advantage against trucks. This also plays out on an ESG perspective as railroads have historically been much easier to electrify than the trucking industry and have a smaller proportional carbon footprint.

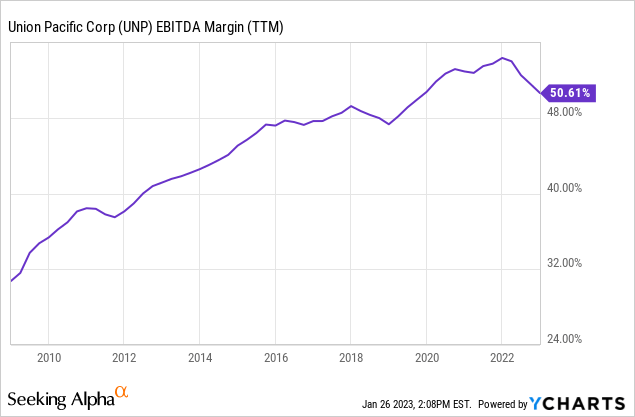

Add these factors up, and railroads might seem like an inevitable long-term winning industry. And there’s some truth to that. However, much of the recent uplift in the railroad industry has come about from rising profit margins. Here’s Union Pacific’s EBITDA margin since the 2008 financial crisis:

You’re reading that right. Union Pacific’s EBITDA margin has soared by a jaw-dropping 2,000 basis points over the past 15 years. Needless to say, regardless of how well management runs the company, it’s unlikely that they will be able to achieve such similar margin gains for all that much longer into the future. If anything, it appears railroad margins may have peaked in the short-term, with a significant decline being noted since the start of 2022.

In late 2022, it appeared that the railroad industry workers might be set to go on a prolonged strike. Workers complained of long hours, insufficient vacation time, and a lack of enough sick leave, among other matters.

The strike was avoided at the last minute, as Congress and the Biden Administration stepped in with legislation to head off a potential strike. Railroad workers will get a 24% pay raise over the next few years along with an additional paid day off among other benefits. This came up well short of workers’ initial demands, however, and it wouldn’t be surprising if the unions try to organize another strike in the not-too-distant future. That’d be especially true if railroad profit margins resume trending upward and workers feel like they should get more of the pie.

All this to say that railroads enjoyed a tremendous stretch of increasing profitability over the past decade or two. However, operations have already been optimized. Advantages over trucks have been utilized to full effect. And labor costs will probably go up, rather than down, as a proportion of revenues. So, investors should mentally prepare for slower growth out of railroads going forward than we saw in the past.

That said, I believe the starting valuation — especially on Union Pacific — is reasonable enough to justify an investment at today’s price despite the more modest longer-term growth outlook. Union Pacific, in particular, has an ace up its sleeve.

Union Pacific’s Mexican Upside

Union Pacific de Mexico logo (Corporate website)

A huge theme I’ve been hammering over the past few years is upside for companies with exposure to Mexican manufacturing. Now that companies are more wary of putting their manufacturing in China and other farflung locales, we’ve seen a significant rise in the amount of new manufacturing investments in North America. Mexico, as the low-cost labor option on the continent, is a natural hub for more labor-intensive manufacturing operations.

Union Pacific is set to be one such company that benefits from this wave. That’s because it owns 26% of Ferromex, which is one of Mexico’s two primary railroads.

Union Pacific has now been in the Mexican market for 31 years, as it wisely got involved right around the passage of the original NAFTA free trade agreement. Over the ensuing decades, countless auto, aviation, medical device, food & beverage, etc. factories have sprung up in Mexico, giving Union Pacific and its affiliate Ferromex more goods to haul.

Here’s Union Pacific Mexico VP Beto Vargas Garcia:

Looking back to 1992, we see the economic revitalization and growth Mexico has experienced since the reshaping of the rail network and are very proud to have been part of the success and transformation of this great country. We believe the region will continue to benefit from our continued combined efforts to grow and build a solid region, creating transportation solutions that meet industry needs on both sides of the border.”

Ferromex’s parent, Grupo Mexico Transportes (Mexico:GMXT) has a market cap of around $9 billion, suggesting that the 26% stake in Ferromex isn’t worth all that much in comparison to Union Pacific’s overall valuation. That said, I expect Ferromex’s revenues to grow tremendously throughout the 2020s, which should give Union Pacific a nice higher-growth element to its overall structure, particularly if much of Ferromex’s cargos end up routed on Union Pacific rails once they enter the United States.

Union Pacific Stock’s Bottom Line

I don’t believe the next ten or twenty years will be quite as sensational as the last few decades have been for railroads. Taking a company’s EBITDA margin from 30% to 50% is a simply breathtaking accomplishment, and it’s hard to imagine being able to duplicate that level of margin improvement again anytime soon.

That said, the rails still have a lot of favorable qualities to them, such as being monopoly-style assets with limited current or future competition. And now, with UNP stock at a starting multiple of just 17x forward earnings, the price certainly isn’t too demanding. Analysts forecast high single-digits annualized earnings growth from here over the next few years, and that should be more than enough to generate decent total returns for UNP shareholders.

Throw in the benefits of reshoring and the ownership in Ferromex, and that builds the case for Union Pacific in particular as well. The 2.6% dividend yield, while not huge, is an additional perk compared to the S&P 500’s lower current yield. With Union Pacific shares down 18% over the past 12 months, this dip is deep enough to offer significant value for potential Union Pacific investors today.

Be the first to comment