XH4D

Investment Thesis

Thanks to ChatGPT, AI technology is more popular than ever, but the number of clear investment opportunities is still small. Founded in Romania in 2005, UiPath (NYSE:PATH) develops AI software able to automate boring activities like extracting data, filling documents, or updating databases. But despite its products increasing the efficiency and profitability of other companies, UiPath’s business model is still not able to generate positive returns to investors other than growth in revenues.

Even assuming UiPath will achieve the efficiency and profitability levels of the best software companies, its stock appears to be extremely overvalued at today’s prices if compared to an estimated intrinsic value of $8.76 per share. Nonetheless, the growth opportunities represented by the market UiPath is leading in don’t permit us to completely discard the company.

In today’s analysis, we will assess why UiPath should be kept on our watchlist patiently waiting for buying the company at a great discount.

Business Model

UiPath operates in the robotic process automation (RPA) industry developing robotic software powered by AI technology that is able to emulate human behaviors, eliminating the need for employees to execute boring and repetitive tasks saving time and increasing overall efficiency. UiPath’s robotic software can be easily implemented by companies in their already existing ecosystem and results are immediately visible.

UiPath generates most of its revenues from the sale of licenses for the proprietary software, usually lasting one year, and from maintenance and support services that are offered under a subscription program to customers once they purchase the license to use the software. For a lesser part revenues are generated by non-recurring professional services like training services to get used to the products.

UiPath products are sold worldwide, accounting for more than 10 thousand customers. Their primary go-to-market strategy is relying on established consulting companies, like Accenture (ACN), Deloitte, and EY, which enter a partnership program under which they can promote UiPath’s solutions to their consumers as a tool to improve their operations. The word-of-mouth effect of this strategy permits UiPath’s solutions to be known and adopted by the best companies in the world.

Operating Performance

Looking at UiPath’s operating performance, its revenues grew at a compound annual growth rate (CAGR) of 62.9% from 2020 to 2022 fiscal years, reaching $892 million. UiPath achieved excellent gross margins in the range of 80%, but due to the high operating expenses like R&D, needed to support future growth, its business model is still not able to generate positive operating returns with losses of $500 million in the last fiscal year. In regards to the nine months ended for the fiscal year 2023, revenues grew 24.4% y-o-y, and the gross margin remained at 82%.

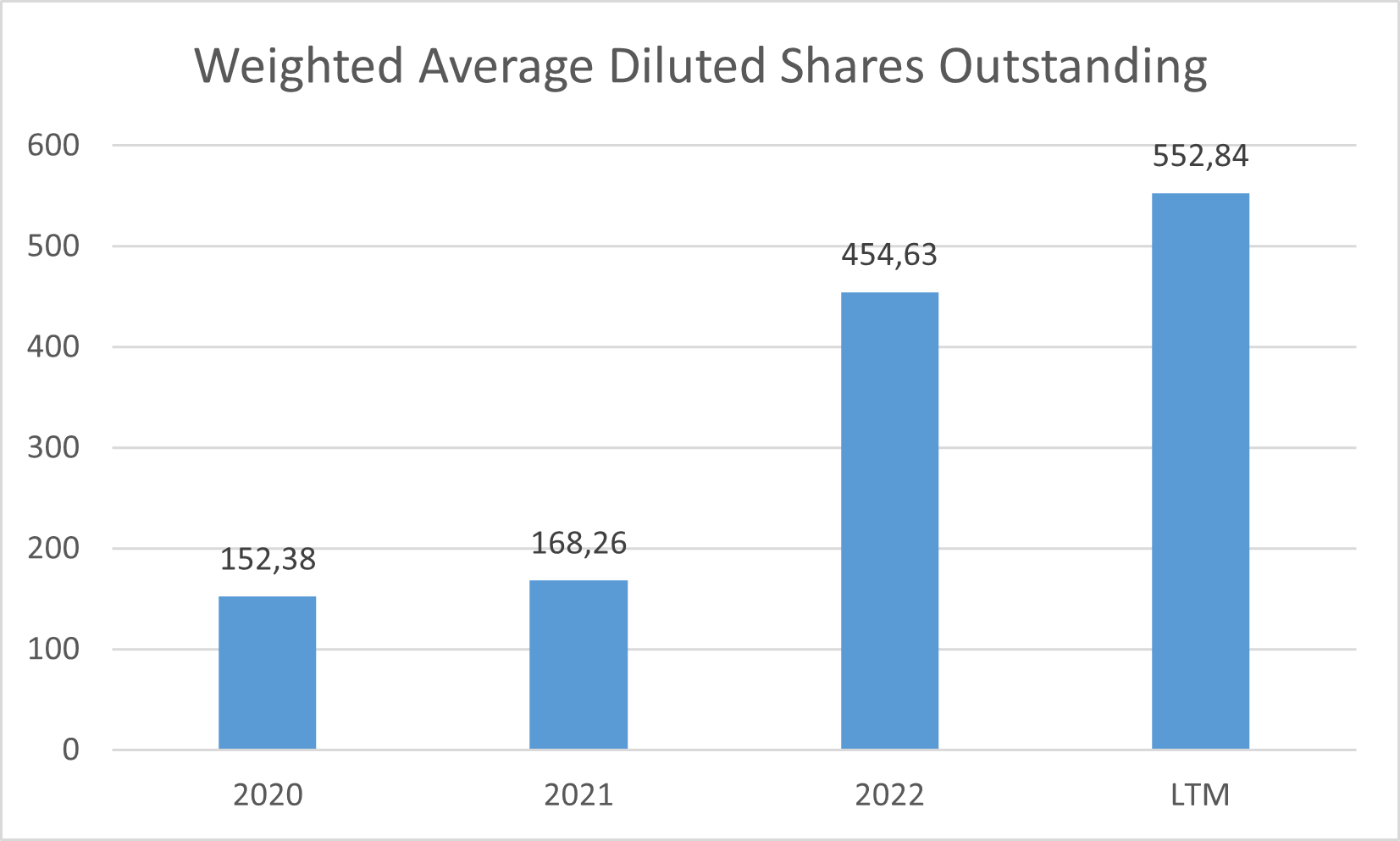

UiPath presents a healthy financial position, with only $61 million in debt outstanding in the most recent quarter, represented by lease liabilities, and $1.38 billion in net cash available. However, UiPath went public not even two years ago, and the management keeps issuing shares to raise capital to fund operations at the expense of investors that see their investment diluted.

UiPath Shares Outstanding (TIKR Terminal)

Market Risks & Opportunities

UiPath’s strength resides in its technology. UiPath has to invest heavily in R&D to keep improving its robotic software and AI technologies adding new features and functionalities to further increase the benefits for its customers and maintain its leading position in the RPA industry.

The current leaders of the RPA industry are UiPath, Automation Anywhere, and Blue Prism and while the latter two offer a more advanced experience, UiPath opted to offer an easy-to-use experience at lower prices. The advantage of UiPath over its two main competitors is the easiness with which employees can start to implement its solution without any particular programming knowledge favoring its mass adoption. On the other hand, when customers need more advanced functionalities, they will rely on UiPath’s competitors. Hence, UiPath is losing a big chunk of revenues from those potential customers that, requiring advanced functionalities, would probably accept paying inflated prices just to get the best products available.

Despite the triad of companies competing for the leading position, the RPA market is still young and has room for growth for every player in my view, since it is expected to expand at a CAGR of 22% by 2033. The recent explosion in the popularity of AI solutions like ChatGPT should make explicit that there’s already high demand and interest in products able to automate cumbersome and time-consuming activities. Enterprise applications would be the first ones to be adopted, with companies looking for the best solution to increase efficiency and gain market shares over their competitors, and UiPath is currently sitting in a privileged spot to benefit from this future trend.

DCF Model

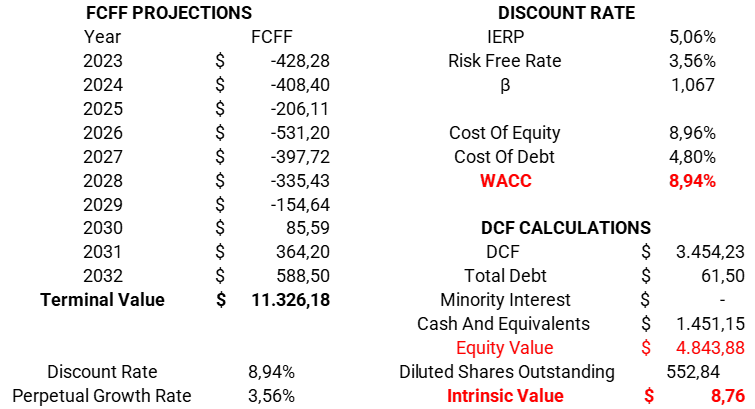

I use the discounted cash flow analysis method to value companies. The aim of a DCF analysis is to determine the present value of expected cash flows generated by the company in the future. The first step is to project the growth rate at which revenues will grow in the future. Secondly, we will need to assume the degree of efficiency and profitability at which the company will turn revenues into cash flows.

Efficiency is represented by the operating margin, and profitability by the return on invested capital (ROIC). Having the revenue projections and future operating margins, we obtain the EBIT and, after subtracting taxes, we get the net operating profit after taxes. The ROIC is used to determine the reinvestments needed to support future growth, determining how much profit the company generates from every dollar reinvested into the company. Future cash flows are calculated by subtracting the reinvestments from the net operating profit after taxes. The higher the growth rate, the higher the reinvestments needed to support it, hence the lower future cash flows will be.

The last step of a DCF analysis is to apply the discount rate to future cash flows, usually calculated using the weighted average cost of capital (WACC).

Projections

Now, trying to project UiPath’s performance, the story we are telling here sees UiPath galloping at the growing trend of enterprise adoption of AI solutions that will boost its revenues growth, permitting the company to reach efficiency and profitability on the same level of the best software companies before entering the maturity phase.

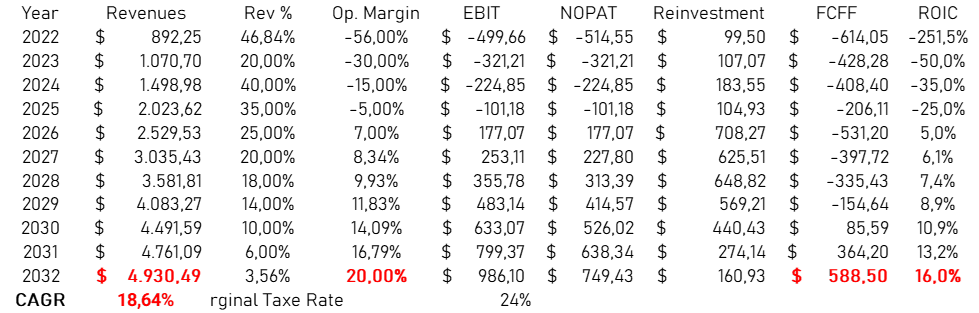

For the fiscal year 2023 we can expect revenues to grow 20%, badly affected by the economic downturn that cut business spending worldwide in 2022, while in the coming years, we can expect growth rates to recover momentum, with growth rates in the rage of 30%-40% as the adoption of AI technologies spread among companies, to then decline slowly as the company reaches maturity. With these assumptions we can expect UiPath’s revenues to quintuple in ten years, growing at a CAGR of 18.6% reaching $5 billion by 2032.

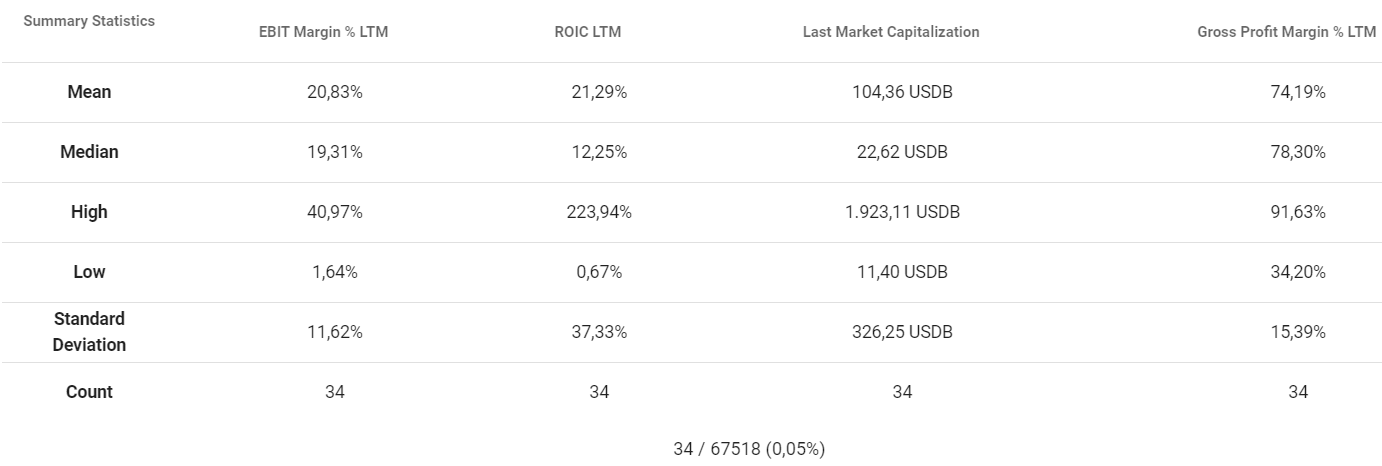

Given the strong assumptions about growth, UiPath will have to invest heavily to support it therefore we cannot expect UiPath to turn profitable in the coming years. Assuming the investments made will start to pay off in 3 years, as the adoption of AI solutions starts to consolidate, and assuming UiPath will still be the market leader, we can expect the efficiency and profitability to reach the level of the best software companies operating at the present. Among the software companies with a market capitalization above 10 billion, the average gross margin, operating margin and ROIC, are respectively 78%, 18% and 12%. Given that UiPath already has a gross margin higher than the current market average we can assume the company to have both an operating margin and ROIC slightly better than its peers by 2032, around 20% and 16% respectively.

Software Industry Average Operating Margin & ROIC (TIKR Terminal)

With these assumptions, UiPath is unlikely to deliver positive FCFF in the short term but by the time the company reaches maturity by 2032, we can expect FCFF to be in the range of $600 million.

UiPath Performance Projections (Personal Data)

Valuation

Applying a discount rate of 8.94%, calculated using the WACC, the present value of these cash flows is equal to an equity value of $4.8 billion or $8.76 per share.

UiPath Intrinsic Value (Personal Data)

Conclusion

Given my analysis and assumptions, UiPath stock seems to be extremely overvalued at today’s price. But even though at these prices UiPath does not represent a good investment opportunity, the growth potential that the RPA industry has in the coming years makes UiPath a noteworthy addition to the watchlist of every patient investor. If UiPath’s stock price declines below its estimated intrinsic value, or if there is any positive development that will make the company’s intrinsic value increase, UiPath would represent a good investment opportunity.

Be the first to comment