Sundry Photography

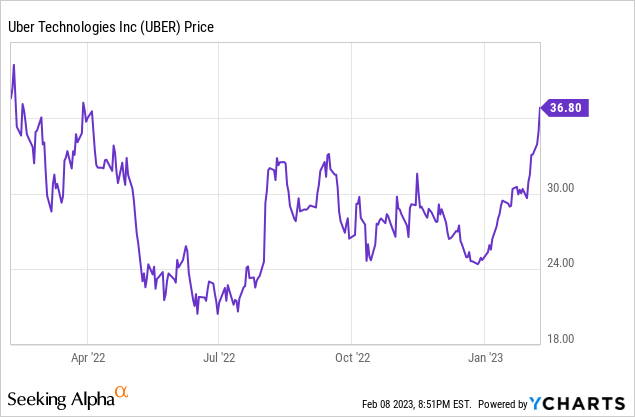

Oftentimes market sentiment is deeply misaligned from underlying business fundamentals, and that was the case with Uber (NYSE:UBER) – the global ride sharing giant. Uber stock spent much of late 2021 and 2022 fighting off bears and taking in criticism over the speed of profitability increases as well as deceleration in bookings growth.

Now, however, those criticisms seem moot. Fresh off a very impressive Q4 earnings print that showed a massive beat to both top and bottom line expectations, shares of Uber jumped ~5% post-earnings, adding to an already-healthy ~45% YTD gain.

Never has the bullish thesis for Uber been clearer

Despite the huge recovery we’ve seen already, I remain very bullish on Uber and retaining the stock as a core holding in my portfolio. I continue to view Uber as a tech mega-cap in the making, especially as 1) Uber reinforces its clout as the world’s leading ride-share company and takes market share from smaller competitors that are struggling to achieve economies of scale, and 2) Uber’s own rising scale gives way to huge gains in profitability.

Here is my full long-term bull case for Uber:

- Huge $13.8 trillion TAM. Mobility and Delivery each carry $5 trillion market opportunities, and nascent Uber Freight is another massive $3.8 trillion market that is heavily underserved and ripe for tech disruption.

- Formidable market leadership. In most of the markets that Uber operates in, the company has a leading market share, and usually by a substantial margin. The company has selectively exited markets where it lost share to a local incumbent (Grab in Singapore is a good example), so it can focus on turf where it has the advantage.

- The sharing economy is gradually taking precedence over ownership. Even pre-pandemic price inflation caused many to rethink buying cars, many consumers were already questioning the wisdom of car ownership over rideshare. Owning a car comes with maintenance costs, insurance costs, and in urban areas, often hefty parking costs. Gradually, I expect car ownership to decline and for rideshare to become the preeminent form of transportation.

- Uber One. Uber introduced a $10/month subscription membership that offers, among other benefits, free deliveries on Uber Eats and a 5% discount on rideshare. In my view, this move will help to boost rider loyalty and frequency on top of generating a new subscription revenue stream.

- “Other bets” are numerous. Uber Freight is the best example of a new initiative to drive growth, but grocery and package delivery are others as well. Uber’s focus on anything involving mobility gives it a massive greenfield market to operate in.

- Profitability is sinking back in. Driven by the uptick in rideshare volumes plus higher take rates in both the rideshare and delivery businesses, Uber is driving tremendous Adjusted EBITDA growth. In addition, the company is close to hitting GAAP breakeven.

Uber enters 2023 with a really strong bookings story

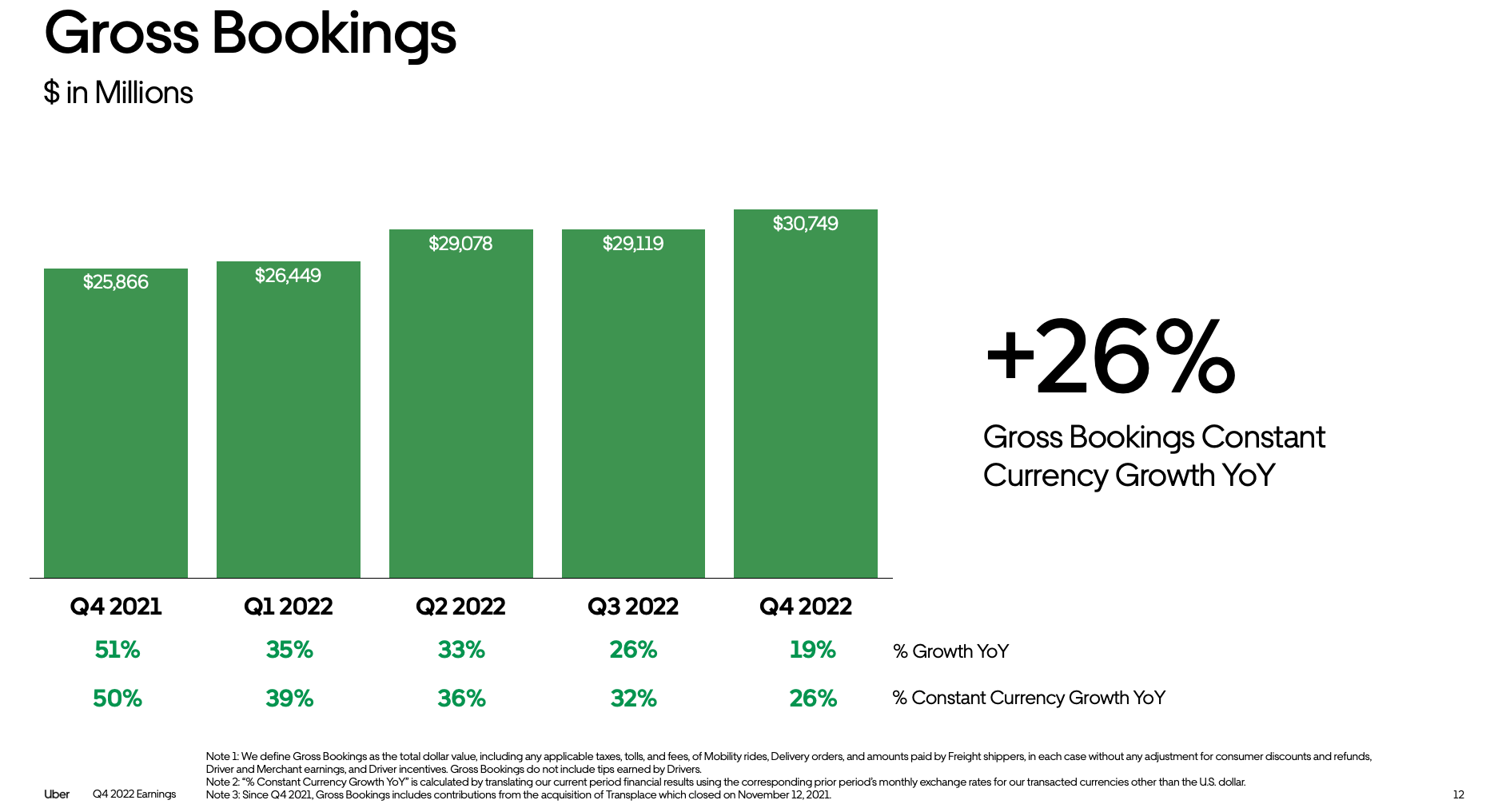

We’ll go through the key highlights of Uber’s fourth quarter, but the first and foremost thing to note: Uber’s bookings are looking really, really strong.

Uber bookings (Uber Q4 earnings deck)

In Q4 (the December quarter), Uber achieved 19% y/y growth in bookings to $30.7 billion. Note that this is already against a fairly tough post-COVID recovery compare last year. Note as well that revenue growth at 49% y/y is coming in much stronger than underlying bookings growth, thanks to Uber’s consistently rising take rates.

The company is even expecting bookings growth to accelerate into Q1, driven in part by easing FX headwinds. For Q1, the company is ranging bookings growth from 20-24% y/y, or 23-27% y/y from a constant-currency basis (implying virtually no deceleration from an FX-neutral standpoint sequentially).

Uber guidance (Uber Q4 earnings deck)

It’s worth noting that Uber One, the company’s $10/month membership, now has more than 12 million members (roughly doubling y/y in the fourth quarter), and the company’s 131 million monthly active users are also at an all-time high.

Segment highlights

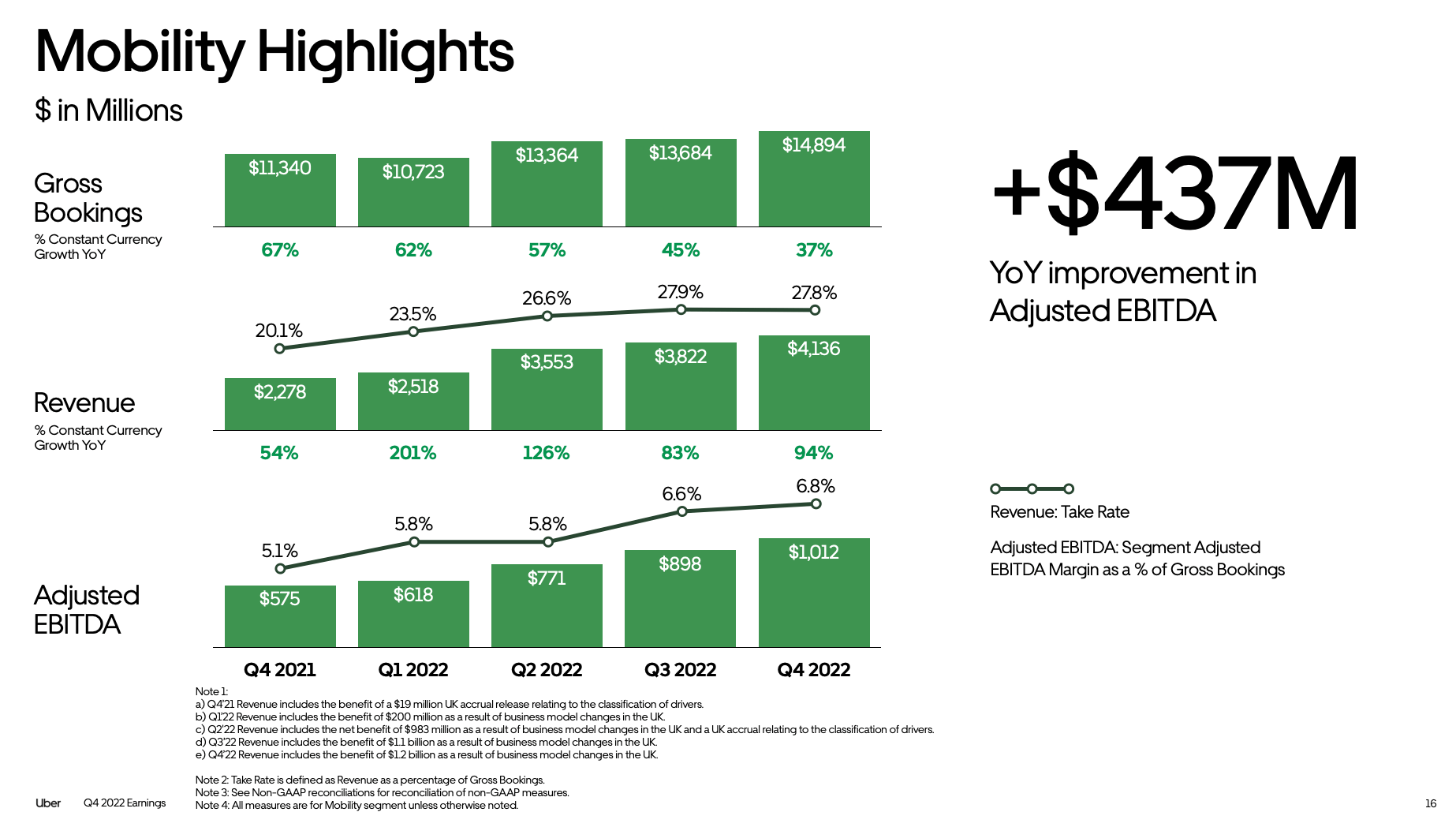

To dig into these trends, it’s important to understand how Uber’s discrete businesses are doing. The Mobility segment continues to benefit from a consistent pickup in rideshare demand, with bookings growing 37% y/y and revenue growth even accelerating to nearly 2x y/y.

Uber Mobility (Uber Q4 earnings deck)

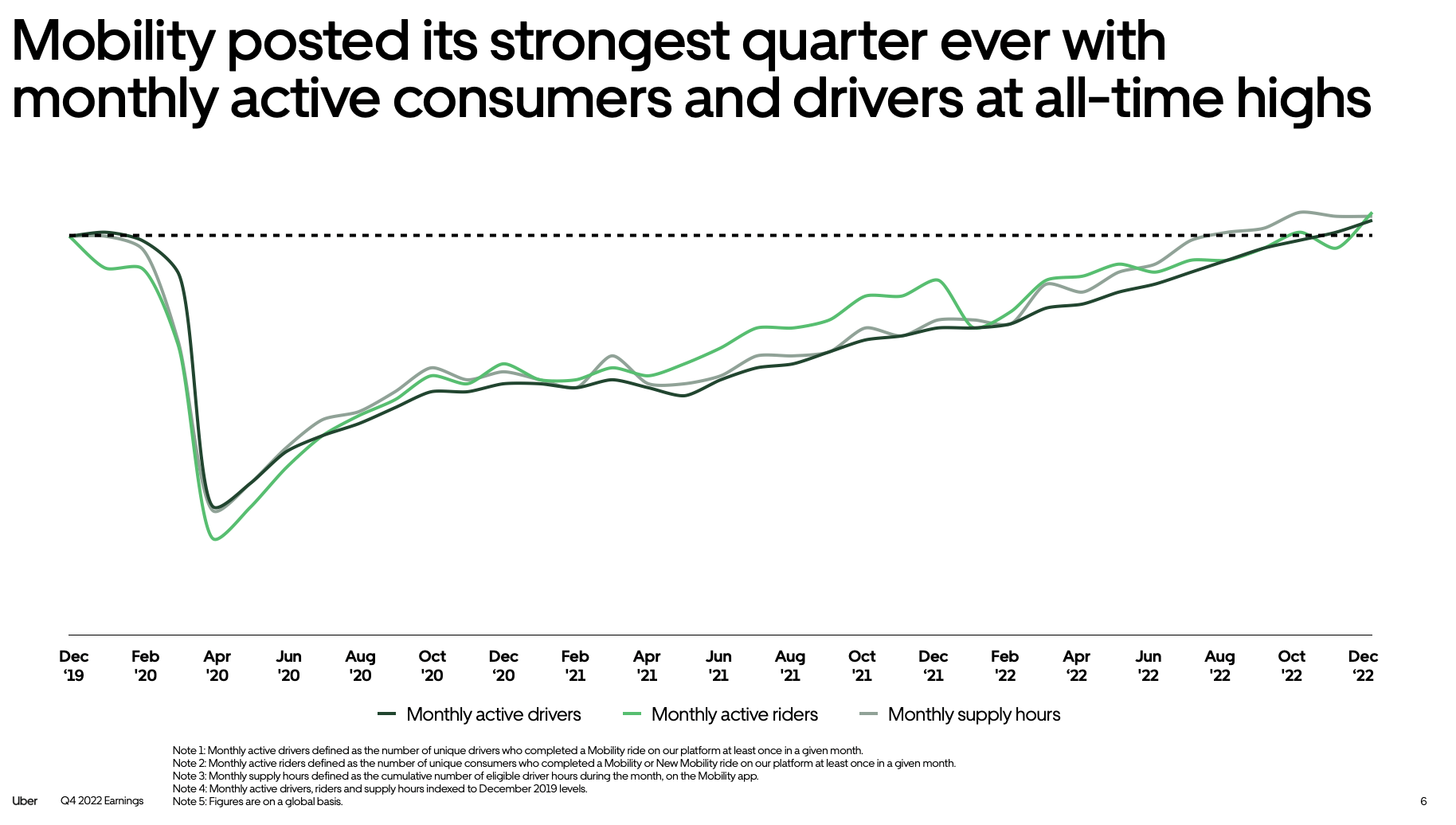

And as seen in the monthly trend chart below, we note that Uber has enjoyed growth in both rider demand as well as driver supply:

Uber monthly Mobility metrics (Uber Q4 earnings deck)

It’s also key to note that it appears Uber riders are tilting toward higher frequency. The average amount of trips per monthly active user has increased to 5.4, up from 5.0 in the year-ago Q4.

Under the hood, Uber notes that new features are helping to capture more rideshare demand. The ability to reserve an Uber in advance, in particular, has seen strong traction per CEO Dara Khosrowshahi on the Q&A portion of the Q4 earnings call:

So I’d say the biggest one for us has been Reserve. If you look overall at the portfolio of new products that we’ve introduced, those new products accounted for about $6 billion of EBITDA — sorry, gross bookings, I wish it were EBITDA, but gross bookings for the quarter, and it’s about 20% of our growth. And that portfolio is growing at about 100% year-on-year. So it will continue to be a larger and larger portion of our overall bookings. And Reserve is the biggest one. We talked about it being over $2 billion. It is a terrific product, especially as travel opens up.

Typically, if you think about traveling to and from the hotel and then coming back, there are about four trips that are available to us. And we capture 1 to 1.5 of those trips. So we think there’s still a significant runway for us to continue to grow Reserve.”

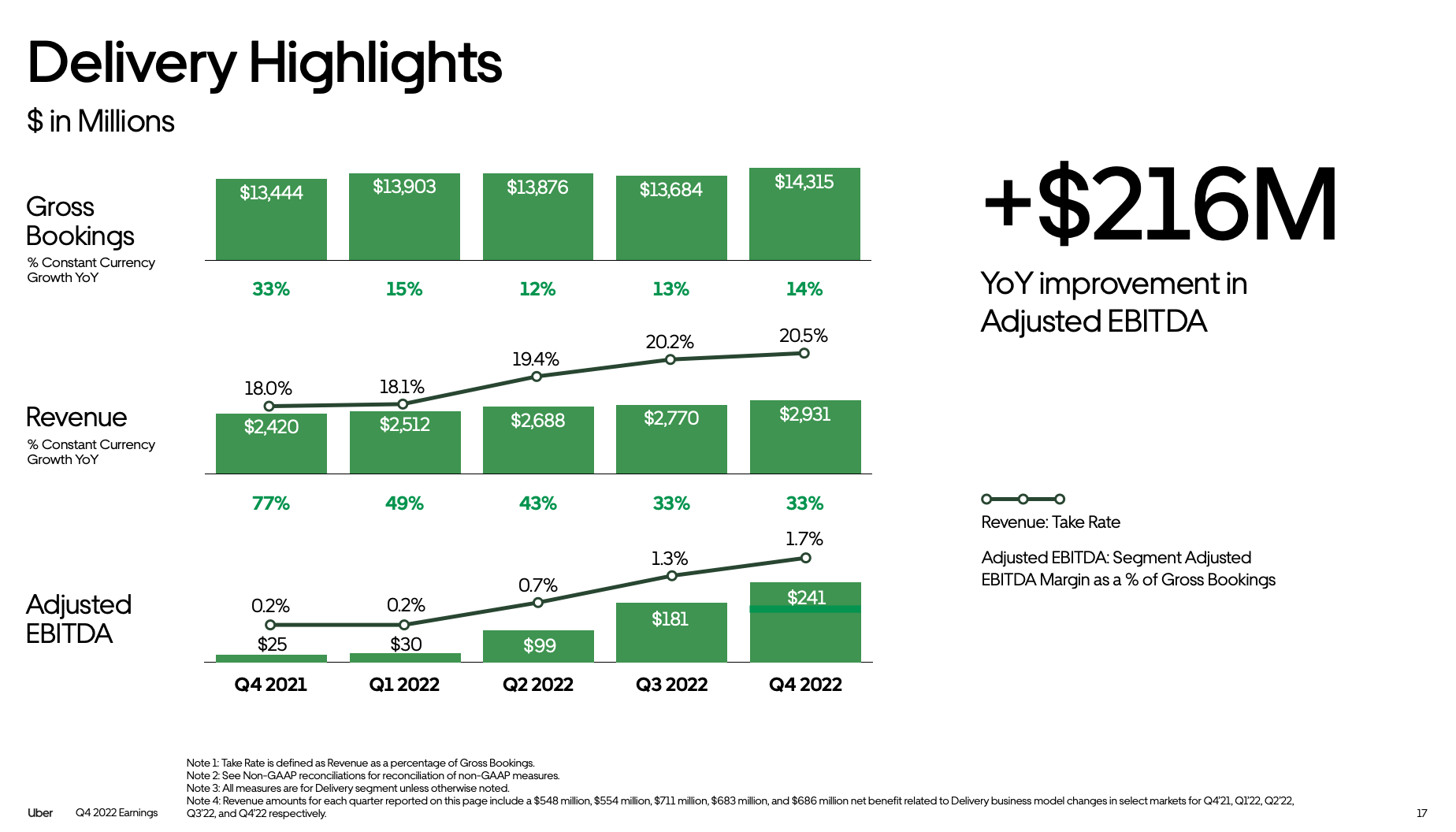

The delivery side of the house, meanwhile, also continues to enjoy double-digit bookings and revenue growth. Much of the pessimism around Uber in the pandemic era was the idea that Uber Eats was a passing fad – and once the pandemic was over, takeout habits would decline.

Uber Delivery (Uber Q4 earnings deck)

This has evidently not been the case. Delivery continued to see strong 14% y/y growth in bookings and 33% y/y growth in revenue – and I’ll emphasize here that we already have a tougher post-COVID compare here, lapping last year’s reopening of stores and restaurants. Evidently, the habits we formed during the pandemic of having takeout delivery more frequently have stuck with us.

Note as well that Delivery, which was heavily unprofitable and killed Uber’s margins pre-COVID (before true scale started to sink in), is now generating adjusted EBITDA profitability and scaling quite nicely.

Uber’s profitability is growing at a nice clip

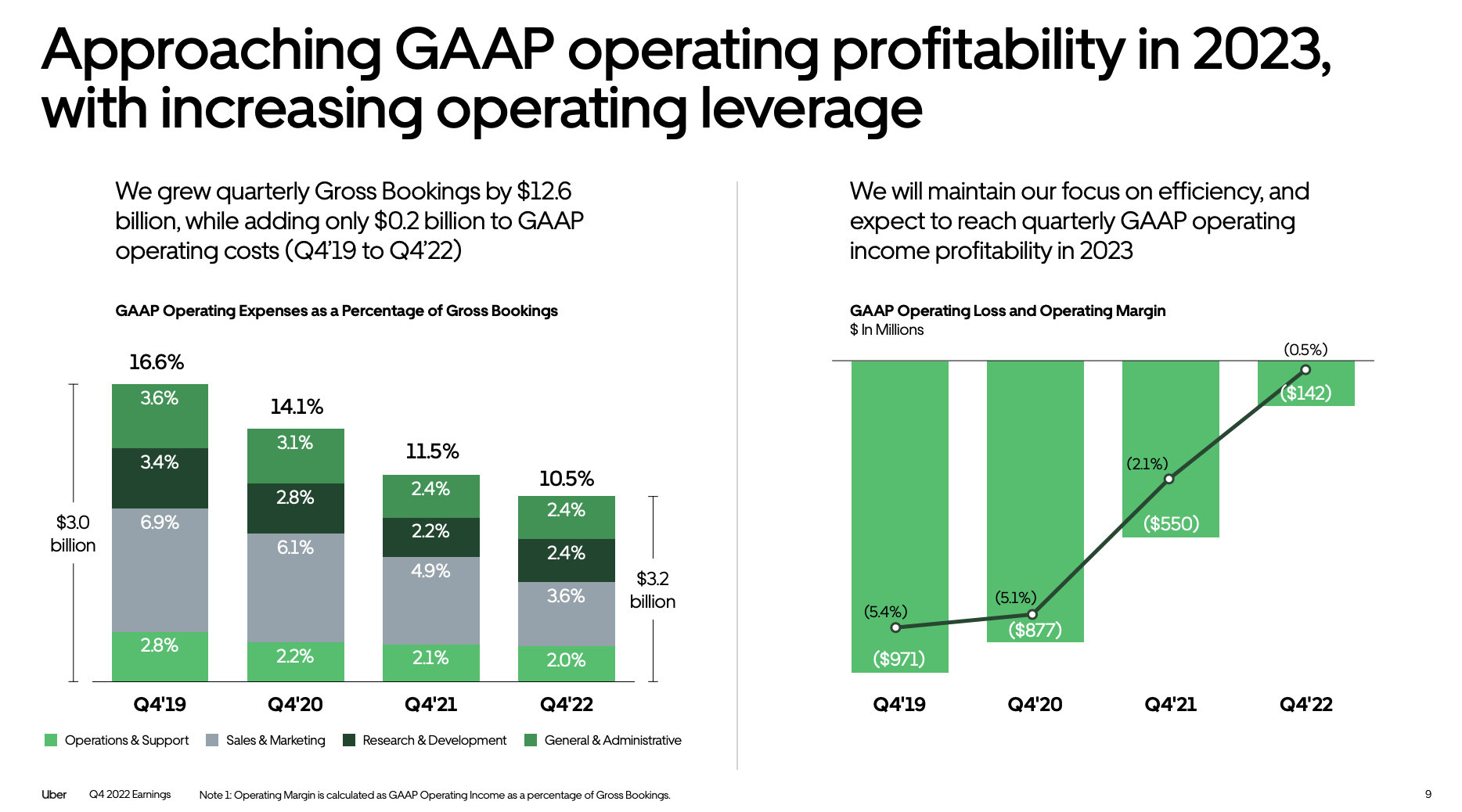

To zoom out at the company-level profitability as a whole: Naysayers once thought Uber was a growth-at-all-costs company that would never reach profitability.

This, evidently, has been proven false. The company reached a -0.5% GAAP operating margin in the fourth quarter, with an eye toward GAAP breakeven/profitability in FY23. Note that the company has managed this without executing any mass-scale layoffs; natural operating leverage has kicked in as the business has grown.

Uber GAAP profitability (Uber Q4 earnings deck)

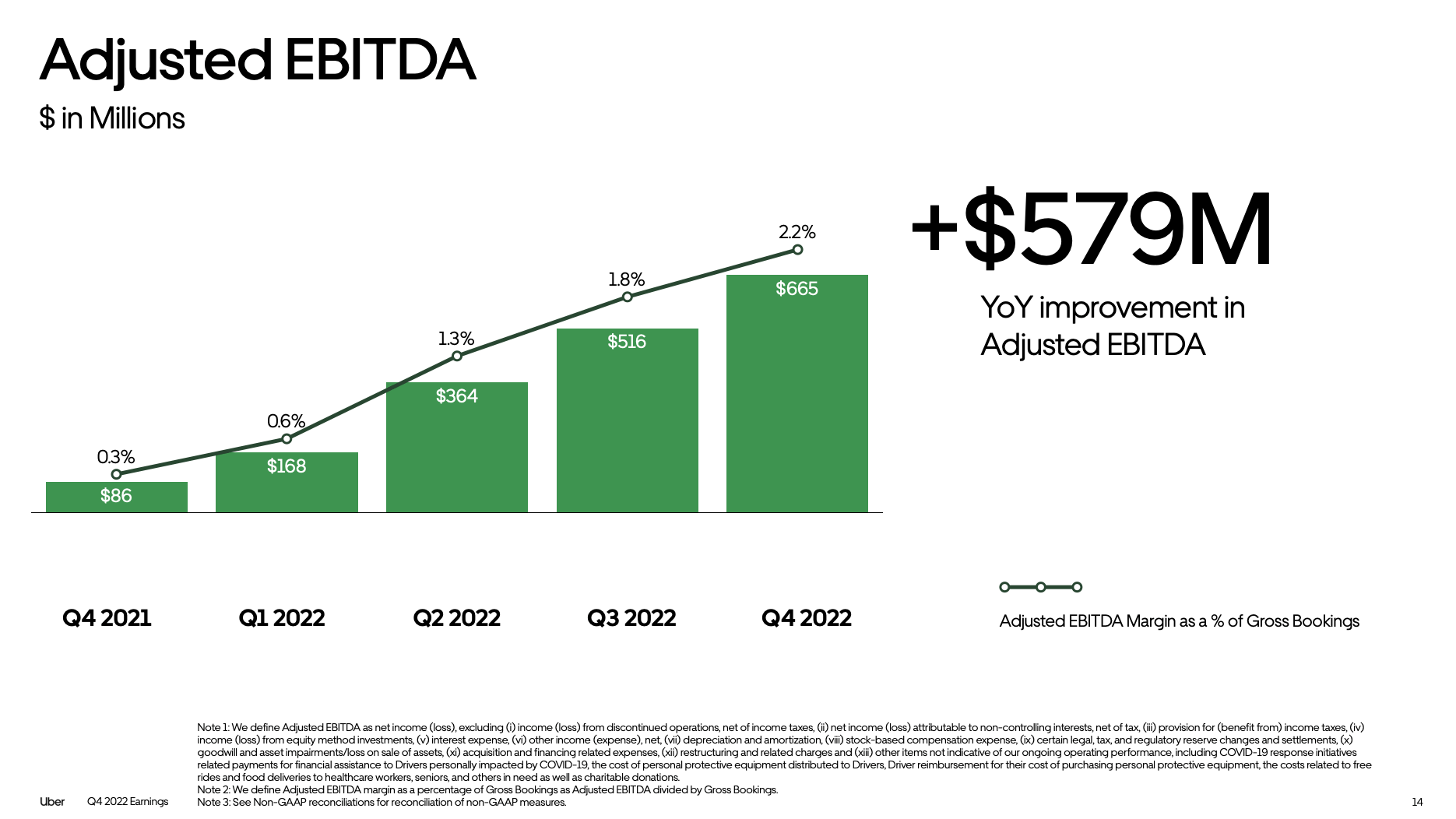

Adjusted EBITDA expanded to a record $665 million in the fourth quarter, representing 2.2% of bookings (a 190bps improvement y/y) and a 7.8% margin of revenue:

Uber adjusted EBITDA (Uber Q4 earnings deck)

Key takeaways

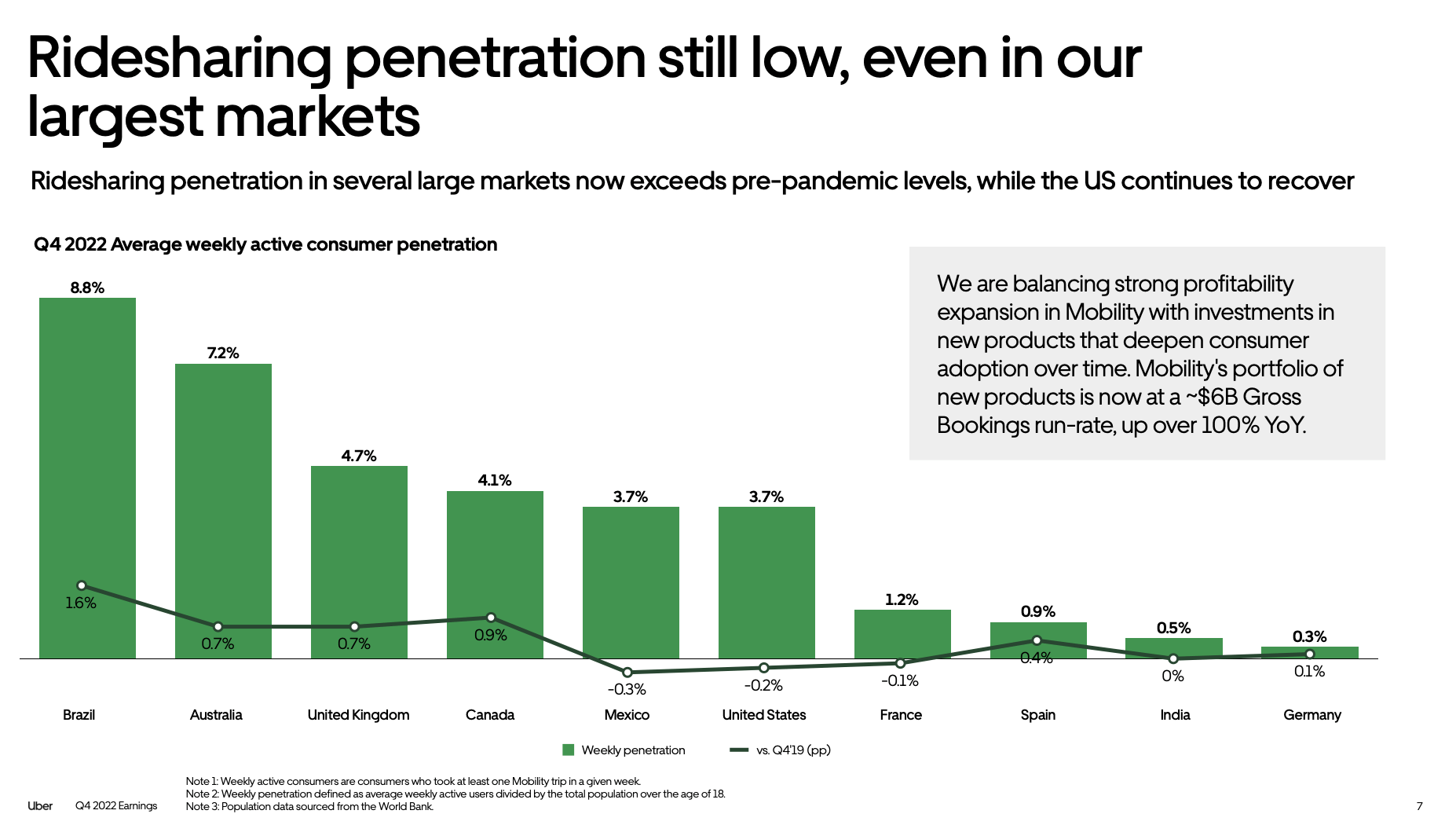

I don’t see any of Uber’s momentum fading. From a long-term standpoint, we should remind ourselves that Uber’s penetration (the percentage defined as weekly active consumers divided by total over-18 population in any given market) remains in the single-digits – and the potential for rideshare (versus car ownership) to grow is quite large.

Uber penetration rates (Uber Q4 earnings deck)

Continue riding the upward momentum here.

Be the first to comment