Kanizphoto

Talking about Government agencies invokes extreme emotions in most people, depending on who is in the office. But one thing that everyone is likely to agree on is the fact that Government systems and processing timelines can use any and all modernization help they can get. Tyler Technologies, Inc. (NYSE:TYL) operates in this enormous yet still largely unnoticed space of providing Software and Services for Public Sector, ranging from small Cities to entire States.

This article dissects the company’s business model and how those have translated into its fundamental situation. I conclude by providing a current technical snapshot and a recommended entry point. Let us get into the details.

Business – Enhance Govt. Productivity

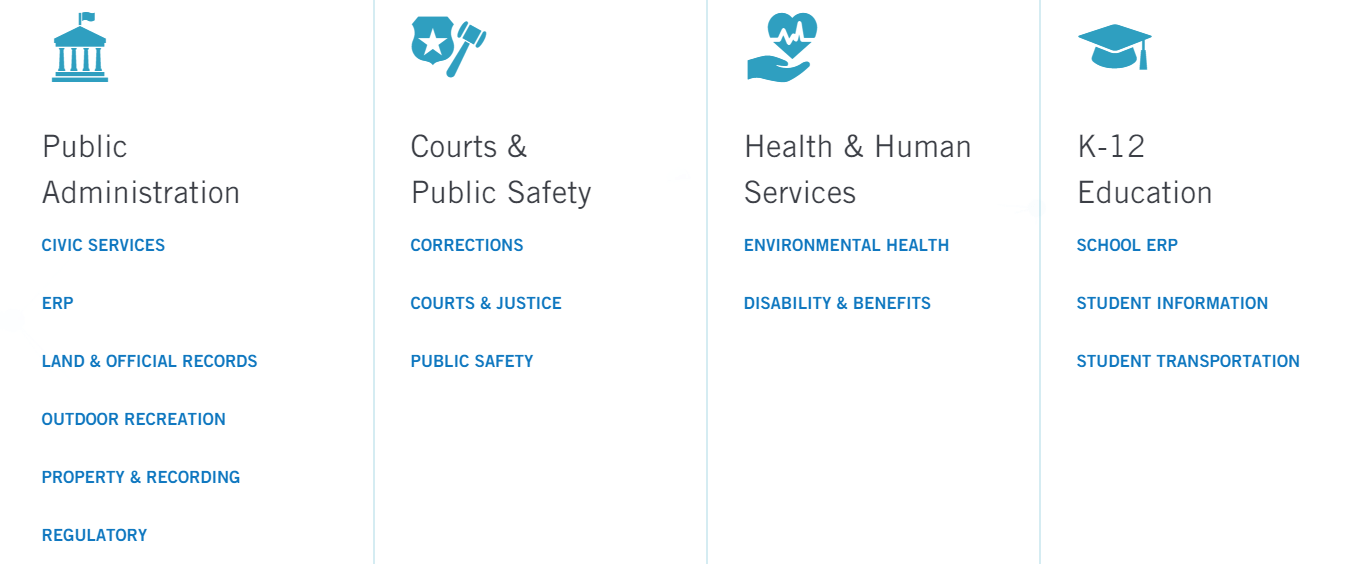

Chances are that if you’ve paid your Water or Electric or Utility bill online, you’ve had some sort of interaction with Tyler’s products. Tyler lists Government and Schools as the two primary areas it serves. While that is short and sweet, we are talking about hundreds of thousands of potential customers and tens of thousands of actual customers. The two pictures below explain better than a two thousand words could, so I am listing out some key bullets below:

- Tyler has been operating as a business for almost 60 years now, with an exclusive focus on Public Sector for 25 years.

- It has products and services that help Government agencies and Schools serve their constituents better. Think of Court case management, Financial management, Utility billing, and Property tax to name a few.

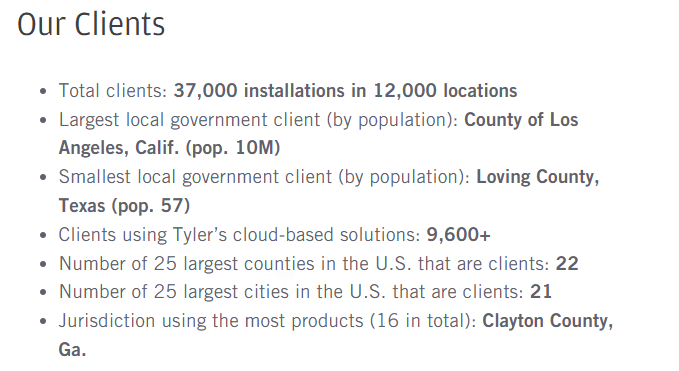

- Tyler’s products are flexible enough to serve governments of all sizes: ranging from one with 57 constituents to another with 10 Million.

- Across the 12,000 locations Tyler serves, there are 37,000 product installations. This means their products can be pieced together to form a portfolio of products that a single customer could use.

The flip side of operating in this space is that at the end of the day, the overall size of the market remains the same. We don’t wake up to the news that a new wing of government has been formed or a new school district has been found every day, week, month, or even year. And by definition and design, these agencies move slowly and are very sensitive to price changes.

Tyler Porfolio (Tylertech.com) Tyler Clients (Tylertech.com)

Business – Stickiness/Contract Length

The fact that Government agencies take a long time to adapt to changes and new technologies, in general, serves as one of Tyler’s biggest strengths. Once a contract is signed, most run for multiple years, with many getting renewed for as much as two decades. Tyler’s target market typically needs to go through an open, expensive, and time-consuming competitive bidding process (RFP, RFQ, etc.) before selecting a vendor and most agencies don’t look forward to repeating this process as long as they are merely satisfied with the services. They are not always on the lookout for the “next big thing” in the Government space.

In addition to contract length and general Government stickiness, Tyler’s products and services are also integrated with each other and served as a platform to the customer. This increases product stickiness as well. For example, when your Financial Management software is also integrated with your Utility Billing software and both are in turn integrated with your own payment processing software, you not only get three revenue streams but also lock in the customer deeper.

Here are some recent Tyler contract extensions and their lengths:

- State of Vermont, 3-year extension, total of 19 years.

- State of Kansas, 2-year extension, total of 33 years.

- Commonwealth of Kentucky, 1-year extension, total of 20 years.

Business – Strategy

I can as well move onto the next section by simply writing this one word: Acquisition. But since SA editors will stop me from doing so, I’ll provide more context here. While the Government Software & Services space may lack big-time competitors, the field is laden with a gazillion small businesses and start-ups. That means there are plenty of acquisition targets and that is exactly what Tyler has been doing for many years as it has both strengthened and increased its portfolio of products. Fortunately and unfortunately for Tyler shareholders, Tyler is already one of the biggest, if not the biggest, fish in this market. That means Tyler is unlikely to get acquired (unfortunately) but still has plenty of targets for revenue growth (fortunately).

Here are some Tyler acquisitions in the last two years alone:

- Quatred, to enhance barcoding solutions for public sector clients, for an undisclosed amount.

- Rapid Financial Solutions, a payment platform, for $68 Million.

- NIC, a digital government solutions and payments processing company, for $2.3 Billion.

There are pros and cons to this strategy. The obvious and almost immediate positive is the bump in revenue from these acquisitions. The medium to long-term positive is the potential synergy by eliminating redundant operations between Tyler and the acquiree. But the cons are that the additional revenue may not necessarily translate into profits and that the acquiree may have their own set of problems that may not be seen until way too late in the game.

The company makes money through many avenues, but the key ones are listed:

- Software As a Service (“SaaS”) fee (Recurring)

- Licensing fee (Typically one-time)

- Implementation Fee (Typically one-time)

- Training Fee (As needed)

- Consulting Services (As needed)

- Payment Processing Fee (Recurring)

Fundamentals – Numbers

Now that I’ve explained the business strengths and weaknesses, let us evaluate how these have translated into fundamentals.

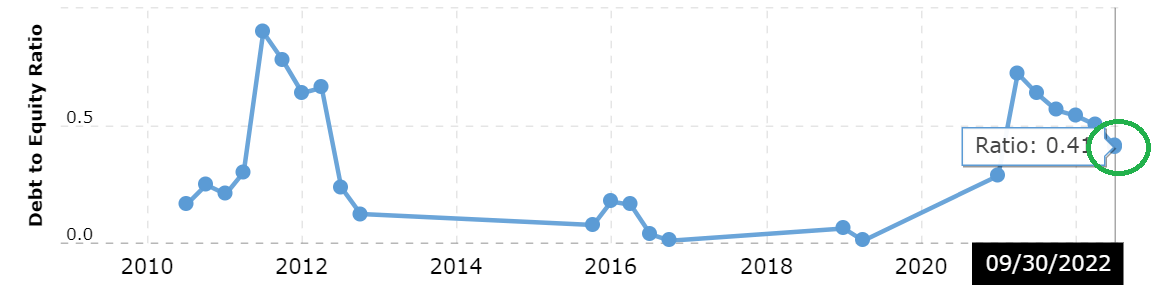

- Tyler’s total long-term debt of $1 Billion may seem high for a company with $13 Billion market cap, but given the fact it acquires more frequently than most companies, it needs quick access to cash.

- But Tyler’s debt to equity ratio of 0.41 indicates that the company is able to finance through equity and is not as reliant on debt. This is a good sign for investors.

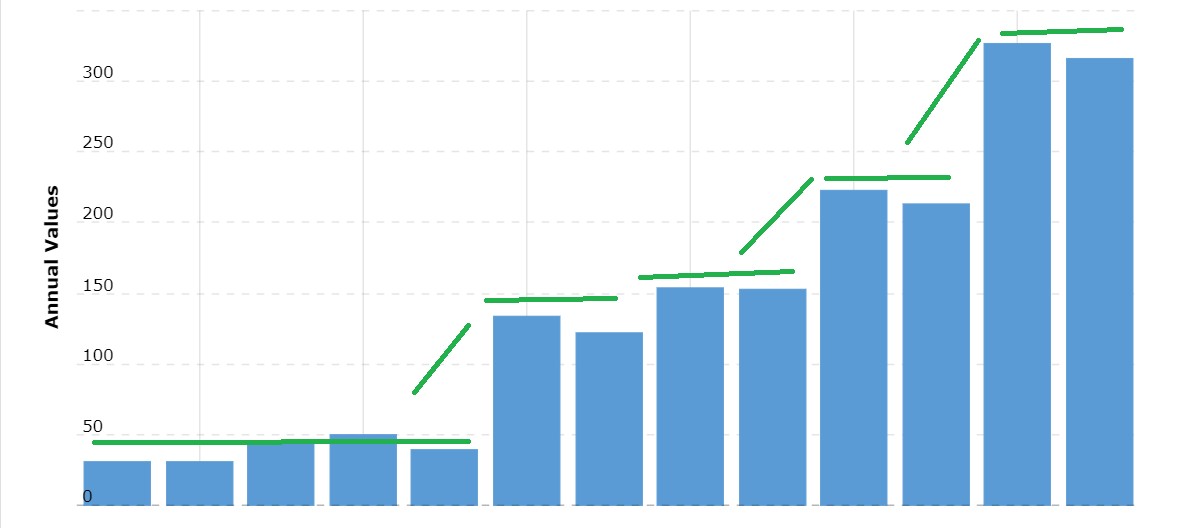

- Tyler’s strength as a going concern is also evident by its free cash flow. There is a pattern to the chart shown below. Few years of steady consolidation, followed up a ramp-up, likely due to acquisition effects (both new acquisitions as well as the synergy from the previous ones).

- In short, the company is steady and profitable but as discussed in the business sections above, I am a bit skeptical about the growth prospects considering the market Tyler deals with and the acquisition-based strategy.

Tyler Annual FCF (macrotrends.net)

Debt-Equity (macrotrends.net)

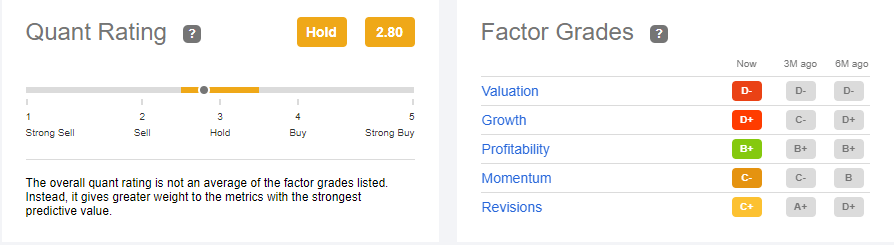

Fundamentals – SA Quant Ratings

SA quant ratings seem to be in agreement with my findings above as Tyler gets a B+ in profitability and D+ in Growth. I will cover the Valuation and Momentum indicators below, and those are in agreement with my findings as well.

SA Ratings (seekingalpha.com)

Fundamentals – Price Target

Out of all the stocks I’ve profiled recently, Tyler stands out in this regard with a median price target that is almost 35% above the current trading price. Does that make the stock a buy automatically? I don’t think so, because I need to see the EPS catching up with the lofty expectations as without that, the stock would need to trade at a forward multiple of 62 to reach the median price target of $433.

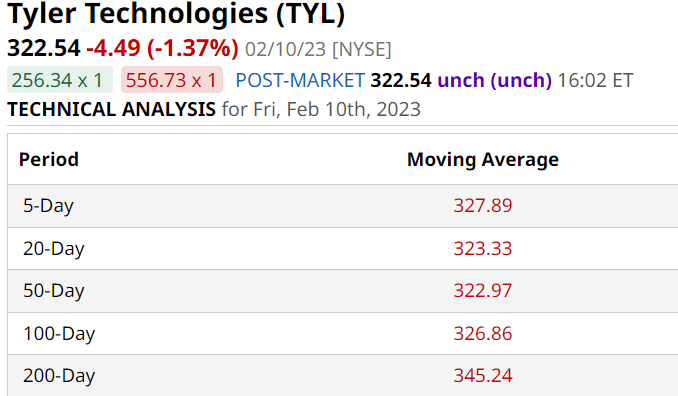

Technicals and Upcoming Earnings Report

From a technical perspective, the stock is in a bit of no man’s land right now or perhaps in a long period of consolidation (hence the classic C- rating on SA Quants). The current price is within a hair’s distance from the 5-, 20-, 50-, and 100-Day moving averages with only the 200-Day moving average being a bit farther at 7%. Tyler is set to report earnings on Wednesday, February 15th and perhaps that might be the direction setter.

TYL Moving Avgs (barchart.com)

Recent history is not on Tyler’s side as shown below when it comes to beating earnings estimates. The company has missed revenue estimates 75% of the time and EPs estimates 50% of the time.

EPS Surprise (seekingalpha.com)

Conclusion

Tyler is operating in a great space, undoubtedly. It may not be growing exponentially but is also unlikely to go out of business ever. What are the odds that every Government agency modernizes at the same time, and they all go to Tyler? Close to zero. What are the odds that thousands of Government agencies at various levels stop serving their Citizens? Even closer to zero. Put those two together, you get: steady and perpetual. That means valuation is key when buying this stock. At 42 times forward earnings, Tyler is richly rewarded here. I’d be more interested in the stock should it ever be available at a forward multiple of 30, which as things stand now is in the early to mid $200s.

Be the first to comment