ansonsaw

Income investing is a rewarding journey that I don’t take for granted. Its many rewards include the ability for one to balance their household expenses with a recurring and passive income stream. Extra income is always helpful, especially in this era of a seemingly endless parade of layoff announcements from tech companies looking for cost reductions.

Having the ability to cover monthly expenses from passive income is a great first step to becoming financially resilient. This brings me to the following two picks, which provide diversification and may be ideal for those who prize high income.

Pick #1: MPLX

MPLX (MPLX) (issues schedule K-1) is a master limited partnership (issues K-1) that was spun off from Marathon Petroleum (MPC) in 2012. It has a straightforward business model, owning and operating long-lived assets, including pipelines and storage tanks, which are used to transport energy products from one place to another.

MPLX also has an inland marine business, docks, and NGL processing and fractionation facilities linked to key U.S. supply basins, particularly in the Appalachia region, and is sometimes referred to as the Enterprise Products Partners (EPD) of the East, due to having a strong presence in export facilities in Northeast U.S.

MPLX demonstrates many excellent attributes, not least of which includes a safe distribution coverage ratio of 1.6x. Remarkably, this includes the robust 10% distribution increase that MPLX gave to unitholders in 2022, all while maintaining a safe net debt to EBITDA ratio of 3.5x. This sits well below the 4.5x level that most ratings $800consider to be safe for midstream companies.

Importantly, MPLX is seeing strong demand, as it saw volume increases to gathered (14% increase), processed (1% increase), and fractionated (6% increase) natural gas. It also has plenty of growth opportunities as management expects $950 million in capital spend in 2023. This includes $150 million worth of maintenance capital and $800 million of growth capital, as outlined by management during the recent conference call:

Our growth capital plan is anchored in the Marcellus, Permian and Bakken basins. In addition to new gas processing plants in the Marcellus and Permian, the remainder of our capital plan is mostly focused on other investments targeted at expansion or debottlenecking of existing assets to meet customer demand.

While our capital outlook is primarily focused on our current L&S and G&P footprint, we will continue to evaluate low carbon opportunities where we can leverage technologies that are complementary with our asset footprint and expertise.

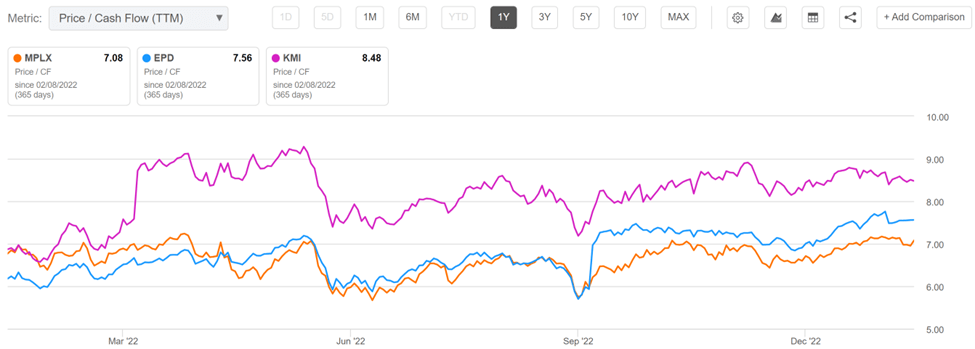

Lastly, MPLX remains attractively priced at $34.59 with a price to cash flow of 7.1. As shown below, this sits below that of natural gas midstream peers Enterprise Products Partners and Kinder Morgan (KMI). Analysts rate MPLX has a Buy and have an average price target of $38, which combined with the 9% distribution yield equates to a potential total return near 20% over the next 12 months.

Seeking Alpha

Pick #2: Blackstone Mortgage Trust

Blackstone Mortgage Trust (BXMT) is a giant in the commercial mortgage REIT space, generating senior loans collateralized by real estate in three continents, in North America, Europe, and Australia. It’s externally managed by Blackstone (BX), one of the largest asset managers in the world, with over $200 billion worth of real estate assets under management. This affiliation benefits BXMT in that it provides it with a deal pipeline and valuable line of sight into the commercial real estate space.

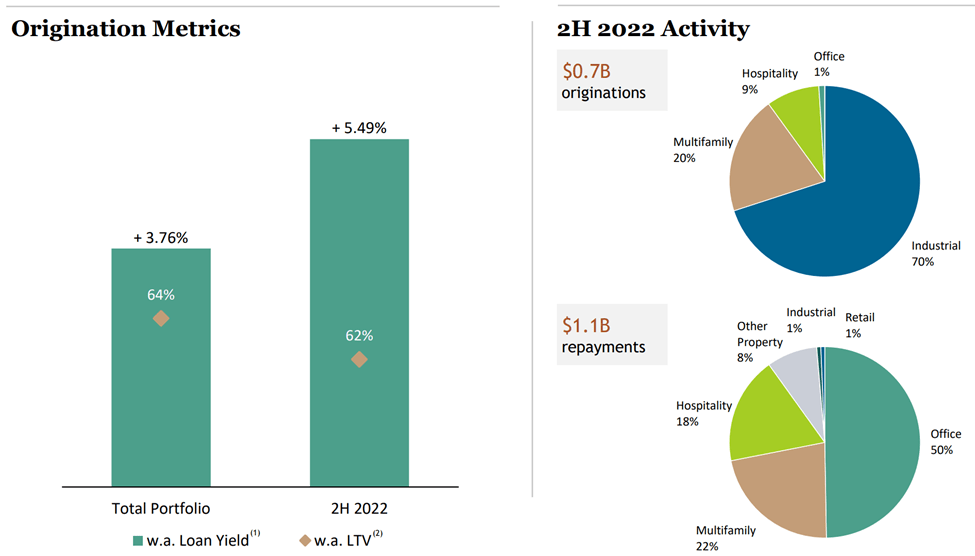

BXMT has a sizeable $26.8 billion senior loan portfolio that’s secured by institutional quality real estate, with a weighted average origination loan-to-value ratio of 64%, implying significant equity stakes in the underlying properties from borrowers. Its borrower base is also in overall healthy shape despite a 400 bps increase in short term rates, as BXMT saw 100% interest collection during the fourth quarter.

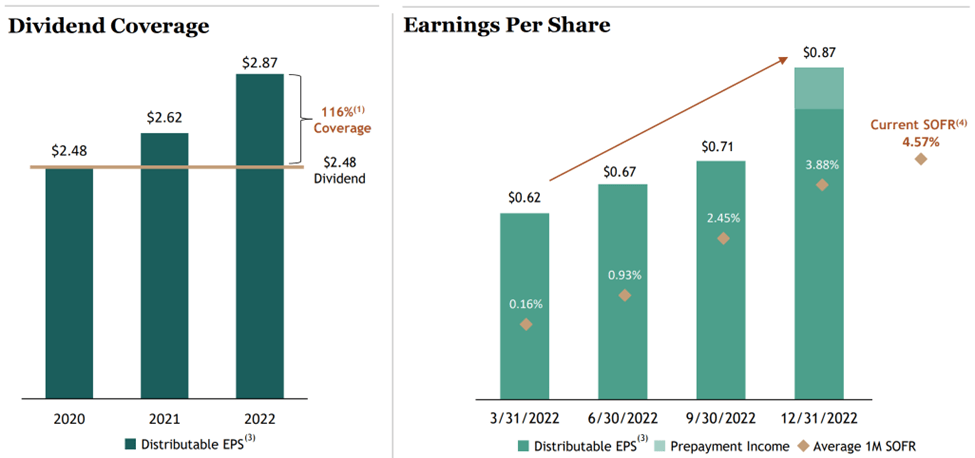

As one can imagine, BXMT is benefitting strongly from higher interest rates, due to its floating rate investment portfolio. This resulted in strong upward momentum in EPS over the past 4 quarters, with EPS coming it at $0.87 during Q4, resulting in a 140% dividend coverage ratio.

Management estimates that a further 100bps increase in base rates from the Q4 average would generate $0.05 per share of incremental quarterly earnings. As shown below, BXMT’s full year 2022 dividend coverage ratio was a strong 116%.

Investor Presentation

Looking forward, BXMT’s balance sheet is in good shape, with $1.6 billion in net liquidity, which is more than enough to cover the $220 million in debt maturities this year. Beyond that, BXMT has no other debt maturities until 2026. Plus, while 40% of BXMT’s collateral is tied to office properties, most of its loan investments mature in the next 3 years and as shown below, management is heavily pivoting investments towards industrial property types.

Investor Presentation

Turning to valuation, BXMT appears to be cheaply valued at just $23.07 with a price to book value of just 0.85x, which as shown below, sits at the low end of its trading range over the past 5 years. Analysts have a consensus Buy rating on the stock with an average price target of $27.14, which translates to a potential one-year 28% total return including dividends.

BXMT Price to Book (Seeking Alpha)

Investor Takeaway

Both MPLX and Blackstone Mortgage Trust appear to be attractively valued with big dividend yields. Both stocks are leading names in their respective industries, with high quality assets and income streams that should continue to generate attractive distributions for investors over the foreseeable future.

Be the first to comment