Images By Tang Ming Tung

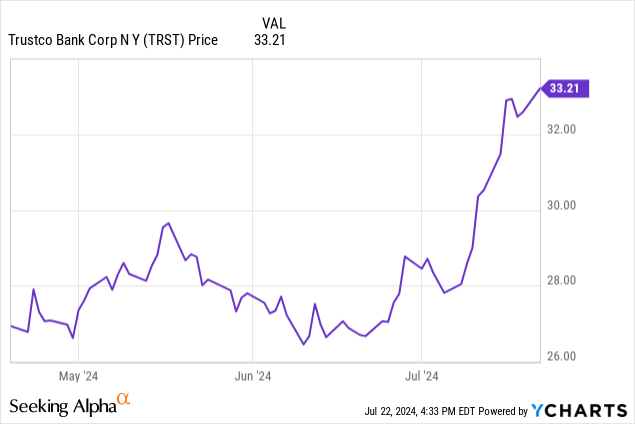

Back in April of this year, we came out with a buy call on then 5.5% yielding TrustCo Bank Corp NY (NASDAQ:TRST). Since then, the stock has had a significant rally, along with many other regional. This little known bank is still one of our favorite regional banks to trade and invest in. After the run-up, we see a hold here as appropriate following the run. The company is operating in this macro environment quite well, as evidenced by the just-reported Q2 earnings.

TrustCo Bank’s Q2 earnings, better than expected

TrustCo in Q2 enjoyed robust loan activity and still had pretty solid returns on assets. The revenue once again surpassed consensus. However, as expected, revenues were down 10.7% from last year, to $43.44 million, exceeding consensus by $2.5 million. The return on average assets and return on average equity came in at 0.82% and 7.76%, respectively. These were both improvements from the sequential first quarter, which saw 0.80% and 7.54%, for both key metrics, respectively. Margins are another story, and we have gone on record saying that margins have bottomed in the sector. Of course, not every bank is created equal.

Net interest margin slipped 16 basis points from a year ago to 2.44%. Net interest income was $37.8 million, up from $36.6 million compared to the sequential first quarter. The net interest margin was 2.53%, up 9 basis points from 2.44% in the sequential first quarter. This stems from the yield on interest earnings assets increasing to 4.06%, up 7 basis points from 3.99% in Q1. At the same time, the cost of interest-bearing liabilities decreased to 1.98%, versus 1.99% in Q1. Combined with operating expenses, TrustCo reported earnings per share of $0.66. This was a sizable $0.13 beat against expectations.

In terms of valuation, TRST is still pretty attractive here at $32.90 per share. We say this because you are collecting income that is now a 4.4% yield, and are buying below book value. Book value per share at June 30, 2024, was $34.46, up 5.5% compared to $32.66 a year earlier, and was up from $34.12 in Q1. Moreover, there was solid loan growth, and deposits were up.

TrustCo Bank loans and deposits

TrustCo’s average loans were up from last year, as the loan book continues to grow. On average, total loans were up $182.2 million or 3.8% from a year ago. Average residential loans and home equity lines of credit, TrustCo’s primary lending focus, were up $89.9 million, or 2.1%, and $61.1 million, or 20.1%, respectively versus a year ago. Average commercial loans also increased $31.5 million, or 12.7%, from a year ago, while average deposits were up $77.4 million, or 1.5% from last year. Despite this tough macro environment, TrustCo is growing its loan book and taking in more deposits. Asset quality also remains high.

Asset quality at TrustCo Bank remains strong, but declines slightly

TrustCo once again maintained strong asset quality metrics as well in Q2. Over the last 7 quarters, that asset base has improved in quality, though there is quarter-to-quarter variability. Non-performing assets as a percentage of total assets were 0.35%, rising 2 basis points from the sequential quarter’s 0.33%, and a basis point higher from 0.35% last year. The ratio of allowance for credit losses on loans to total loans was 0.99%, 3 basis points higher than a year ago.

In total, the allowance for credit losses on loans was $49.8 million at the end of Q2, compared to $46.9 million a year ago. Total nonperforming loans were lower than a year ago. They were $19.2 million versus $19.4 last year, or 0.38% of total loans, compared to 0.40% last year. And we will add that the efficiency ratio increased (which is negative), coming in at 62.84% versus 59.96% in Q1. While 63% is respectable, we are keeping an eye on this key metric going forward.

Final thoughts

So even with shares up really hard from our last buy call, TrustCo Bank Corp NY stock is still at a discount-to-book, and still offers a 4.4% dividend yield. Cash flow covers the dividend, and the payout ratio is quite safe, in our opinion. TrustCo is effectively growing loans and deposits, has strong asset quality (though it declined slightly from the sequential quarter), and is well-run with a conservative lending approach. We think you can hold here, but those who entered in the mid $20’s when we last covered should consider backing out the initial investment and running a house position.

Be the first to comment