vitpho/iStock via Getty Images

TravelCenters of America Inc. (NASDAQ:TA) operates travel centers and truck service facilities in the U.S. and Canada. The truck stop industry is highly fragmented, with the top three companies controlling a quarter of the market.

With the appointment of Jon Pertchik as CEO in late 2019, the company began a transformation that has the stock outperforming the S&P 500 by better than a two-to-one margin over the last five years. However, despite the run up in the stock, TA currently trades for a P/E below 5x.

One reason for the low P/E is a 23% plunge the shares took following Q3 results. However, a review of recent developments reveals little to warrant a decline of that magnitude. Furthermore, the company’s growth initiatives remain intact.

Dissecting TravelCenters of America

With over 280 locations in 44 states, TA is the nation’s largest publicly traded full-service travel center network. The company operates under the TravelCenters of America, TA, TA Express, Petro Stopping Centers, and Petro brand names.

179 of the TravelCenters properties are leased from Service Properties Trust (SVC). Franchisees run 42 of the properties, and 51 of the sites are owned by TA.

The products and services provided by the travel centers include a range of truck repair and maintenance services and both full and quick service restaurants.

The TA Restaurant Group is a division of TravelCenters of America. The division sells franchise opportunities for its Iron Skillet and Country Pride brands and also operates a number of franchises. A list of the restaurants found at TravelCenters includes but is not limited to IHOP (DIN), Popeyes (QSR), Burger King, Starbucks (SBUX), Pizza Hut (YUM), Taco Bell, Fuddruckers, and Dunkin’.

TA operates parking spaces under the Reserve-It brand name, and the company runs three truck service facilities.

The average TA site is on 25 acres and has 200 truck parking spaces. TravelCenters’ largest competitor’s sites are from 9 to 13 acres in size and offer parking for 80 trucks. Management believes the larger properties offer a distinct competitive advantage.

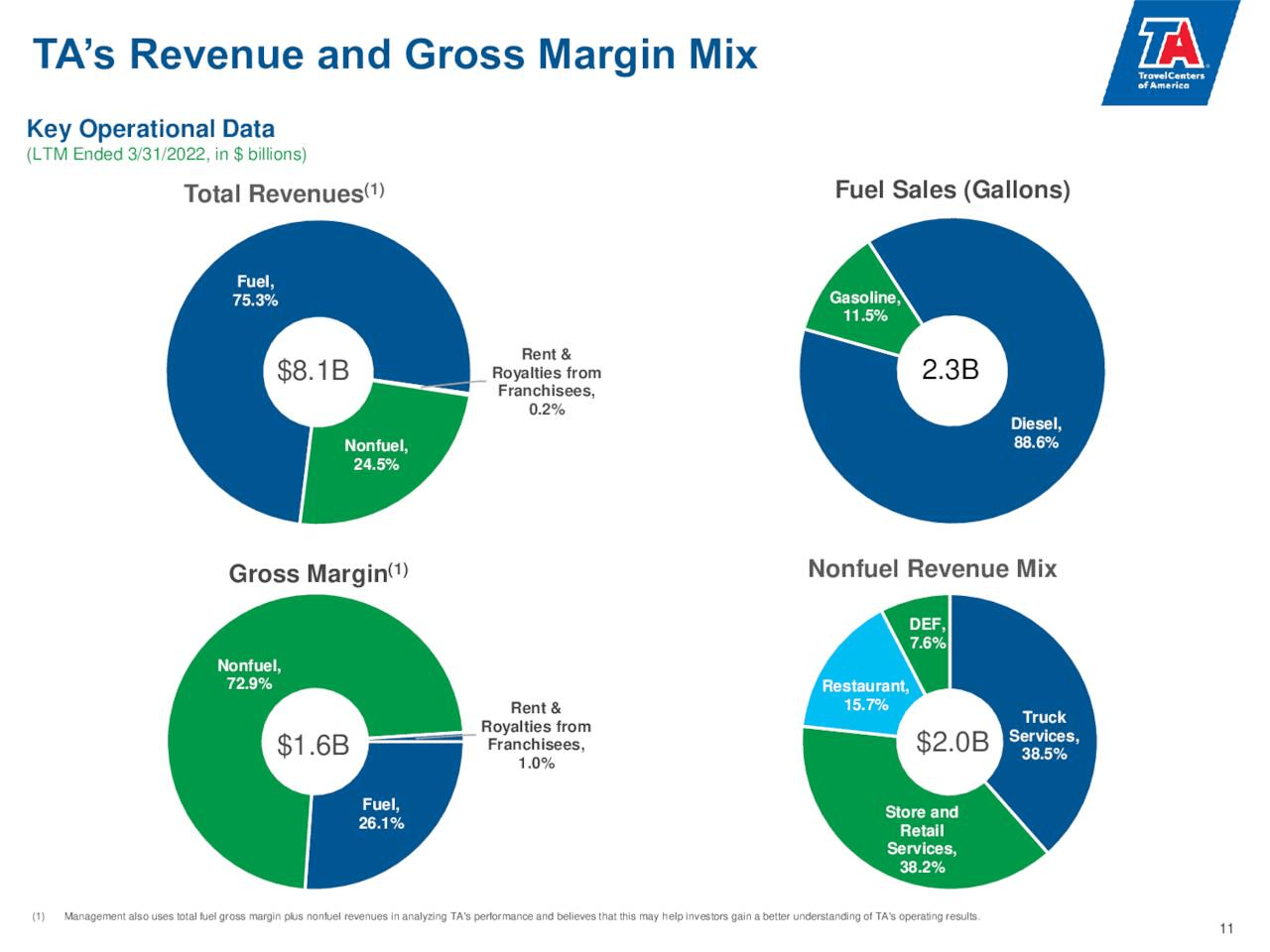

It is important to understand that over 75% of the company’s revenue is derived from sales of fuel; however, nearly three-quarters of the firm’s gross margin is gained through services and products other than fuel. This can result in rather wide swings in revenue from quarter to quarter.

TravelCenters of America Investor Presentation

In the first half of 2022, fuel margins averaged 23.9, and in July CPG was at 26. This was significantly higher than the 17.2 cents per gallon margins in 2021. As many investors may assume that the fuel margins will fall markedly in the near future, this could account for the swoon the stock took following Q3 results.

Management guided for a long-term fuel CPG target range of $0.17 to $0.19 during the September Investor Day.

B Riley analyst Bryan Maher forecasts an average CPG of $0.192 in 2023, and $0.184 in 2024.

Will The Robust Growth Continue?

In 2019, before the new CEO took the company’s reins, TA’s adjusted EBITDA was $131 million. In 2020, despite pandemic headwinds, adjusted EBITDA hit $147 million.

In 2021, it surged to $220.2 million, and as of Q3, the company posted a trailing 12-month adjusted EBITDA of $320 million. That marked a 57% increase in adjusted trailing 12-month EBITDA.

Since 2020, TA has added 56 travel center franchisees. Five began operations in 2020, two during 2021, and one in the second quarter of 2022.

Most of the franchised centers will be built from the ground up, with the balance of the remaining franchise locations expected to be up and running by the fourth quarter of 2024.

TA targets $75 million to $120 million annually in acquisitions to strengthen the firm’s geographic footprint. During the first nine months of 2022, TA acquired five travel centers and two truck service locations.

Management has a long-term target of opening 30 locations annually. To place this in context, TA operates around 280 sites today.

TA has a projected non-acquisition CapEx budget for FY 22 of $175 million to $200 million. Those projects focus on improving the overall customer experience through significant upgrades of the travel centers, expansion of the restaurants and food offerings, and through improvements in TA’s technology systems and infrastructure.

By expanding the store count along with other initiatives, TA has a three-to-five-year long-term EBITDA target in the mid $400 million to $500 million range.

TravelCenters Of America’s Debt And Valuation

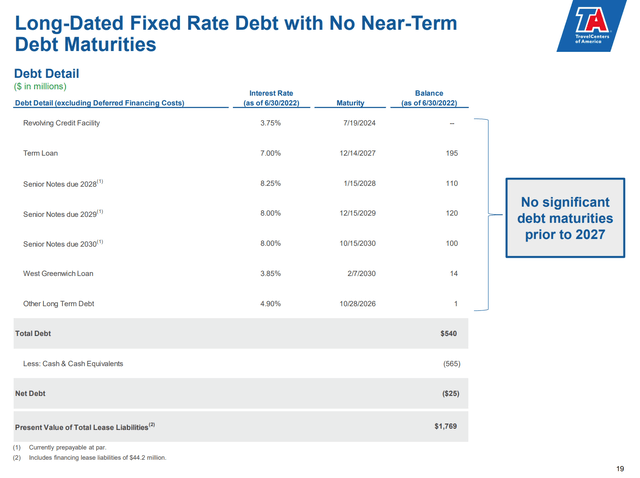

As of September 30th, TA held cash and cash equivalents totaling $467 million, and $524 million of long-term debt outstanding. The company has $179 million available in its revolving credit facility for total liquidity of $646 million. There are no significant debt maturities prior to 2027.

TA trades for $45.74 per share. The average one year price target of the 3 analysts that rated the stock in the last four months of 2022 is $68.33.

TravelCenters’ forward P/E is 4.87x. The trailing twelve month PEG is 0.02x. Investors should note that the sector median TTM PEG is 0.28x.

TA Investor Presentation

Is TA a Buy, Sell, Or Hold?

Jon Pertchik’s leadership transformed TA into a growth machine. There is an oft repeated truism, attributed to Harold Samuel, “location, location, location.” Those three words are considered the three most important factors when considering a property.

I will now attempt to coin the phrase, “management, management, management” to emphasize one of the deciding factors dictating the success of a business. Pertchik’s leadership has turned TA into a growth machine, and I believe his management of TA will continue to drive growth.

While I think investors must weigh the effect fluctuating CPG has on the company’s revenues, I believe TA manifests strong growth prospects.

TravelCenters operates in a highly fragmented industry. The company has a solid financial foundation, and a robust pipeline of franchisees set to boost sales over the short to midterm. With 48 franchisees set to open new locations, and TA currently operating 280 travel centers, it only takes back-of-the- napkin math to verify my perspective.

I’ll also add that “Location, location, location” applies to a lesser extent to the company’s properties.

I rate TA as a Buy.

I’ll add that a recent study released by Forbes rates TA as one of the top 100 small businesses in the U.S.

During my investigation into TravelCenters of America, I initiated a small position in the stock.

Be the first to comment