On Wednesday, April 29, 2020, offshore drilling giant Transocean Ltd. (NYSE:RIG) announced its first-quarter 2020 earnings results. At first glance, these results were quite disappointing as the company failed to meet the expectations of its analysts either in terms of top-line revenues or bottom-line earnings. With that said, few people really expected anything fantastic out of this company as the steep decline in energy prices has caused many upstream producers to cut back on their exploration and development programs, which is the primary thing that offshore drilling rigs are used for. A closer look at the actual earnings report reinforces our disappointment, although the results overall were not as bad as some may have feared. It is going forward that Transocean may begin to have problems unless oil prices quickly recover, which seems unlikely.

As my long-time readers are no doubt well aware, it is my usual practice to share the highlights from a company’s earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from Transocean’s first-quarter 2020 earnings results:

- Total contract drilling revenues were $759 million in the first quarter of 2020. This represents a slight 0.66% increase over the $754 million in the year-ago quarter.

- Operating loss was $199 million in the most recent quarter. This compares rather unfavorably to the $13 million operating loss that the company reported in the prior year quarter.

- Transocean achieved a revenue efficiency of 94.4% in the current quarter. This compares somewhat unfavorably to the 96.2% in the fourth quarter.

- The company took a $167 million non-cash impairment charge related to some of its assets.

- Net loss was $391 million in the first quarter of 2020. This compares very unfavorably to the $171 million net loss in the first quarter of 2019.

It seems likely that the first thing that anyone reviewing these highlights will notice is that Transocean’s revenues were up slightly compared to the prior year quarter. This may not be as encouraging as it seems, however, since revenues were actually down about $33 million from the fourth quarter of 2019. The reason was mostly due to the fact that Transocean had more rigs idle during the first quarter than it had during the fourth. The company did see higher revenues from two of the rigs in its fleet, however. The ultra-deepwater floaters Deepwater Mykonos and Deepwater Corcovado started work on their current contracts during the fourth quarter so they only generated revenue during part of it. This was not the case during the first quarter as both rigs operated for the entire time and this generated more revenues for the company and offset some of the weakness elsewhere.

Another disappointment that we see in these highlights is the fact that Transocean’s revenue efficiency declined compared to the fourth quarter. Revenue efficiency is a measurement used by offshore drilling companies that expresses the amount of revenue that the company actually brought in compared to the maximum that it could have brought in given its current contracts. This is necessary because of the way an offshore drilling rig is compensated. In short, these rigs are only compensated for time that they actually spend working for the customer and not for time spent out of service such as when it is undergoing maintenance or repairs. Thus, in order to maximize its revenues, the drilling contractor would like for its rigs to have no downtime. However, offshore drilling rigs are highly sophisticated pieces of machinery that require regular maintenance in order to perform optimally so this is an impractical scenario. Therefore, the challenge for the drilling company is to minimize downtime while keeping its rigs performing optimally and the revenue efficiency is a measure of how well it did this task. As we can see, the quarter-over-quarter decline in Transocean’s revenue efficiency implies that the company had more downtime across its fleet and was further away from maximizing its revenues than it was in the previous quarter. This also had an adverse effect on the company’s revenues.

As noted in the highlights, Transocean posted a $167 million impairment charge against the value of its assets during the quarter. This means that the company’s assets are no longer worth as much as what was stated on the company’s balance sheet. Accounting rules therefore require that the company change its balance sheet to reflect what the assets are actually worth. In order to do this, it must take a charge against its net income equal to the amount that it decreased its assets by. Unfortunately, the company did not disclose in either its earnings report or in the conference call exactly which assets saw their values decline, although we can assume that it was one or more of the company’s drilling rigs. It is also important to note that this was a non-cash charge and Transocean did not actually see $167 million leave its bank account as a result of this charge. As a result, we can safely ignore it when it comes to actually evaluating the company’s money generation during the quarter. If we do that, the company still would have had a loss but admittedly it would have been a much smaller loss.

Unfortunately, the company’s cash generation was quite disappointing as well. We can see this by looking at the company’s operating cash flow. In the first quarter of 2020, the company had a negative operating cash flow of $48 million. This means that its ordinary operations actually consumed more cash than they generated. This is not something that we like to see as it essentially means that the company is depending on external financing to operate and this is not a sustainable situation over the long-term. With that said though, the company had a negative operating cash flow of $51 million in the year-ago quarter, so this was a slight improvement even though both figures were very disappointing.

The management was cautiously optimistic about the company’s future in both the earnings report and the conference call, which is admittedly nothing new for Transocean. This was despite the severe impact that the outbreak of the COVID-19 pandemic has had on energy prices. In fact, Jeremy Thigpen, Transocean’s President and CEO stated:

With the challenges we confronted related to COVID-19, I am very proud of the strong quarterly financial results we delivered. Through outstanding effort across our entire organization, we delivered revenue in-line with our guidance, and at lower than projected costs; even with the additional hurdles we overcame crewing and equipping our rigs to meet their contractual requirements for our customers. Looking forward, we recognize the dramatic decline in oil prices, coupled with the continued uncertainties surrounding the containment of COVID-19, and the resumption of the global economy, will invariably delay the contracting activity that we expected in 2020. However, with our industry-leading backlog and proven track record for managing costs, we expect to continue to deliver industry-best margins. With continued strong operating performance, and prudent management of our liquidity, Transocean is well-positioned to continue delivering the highest level of service while keeping our employees and customers safe.

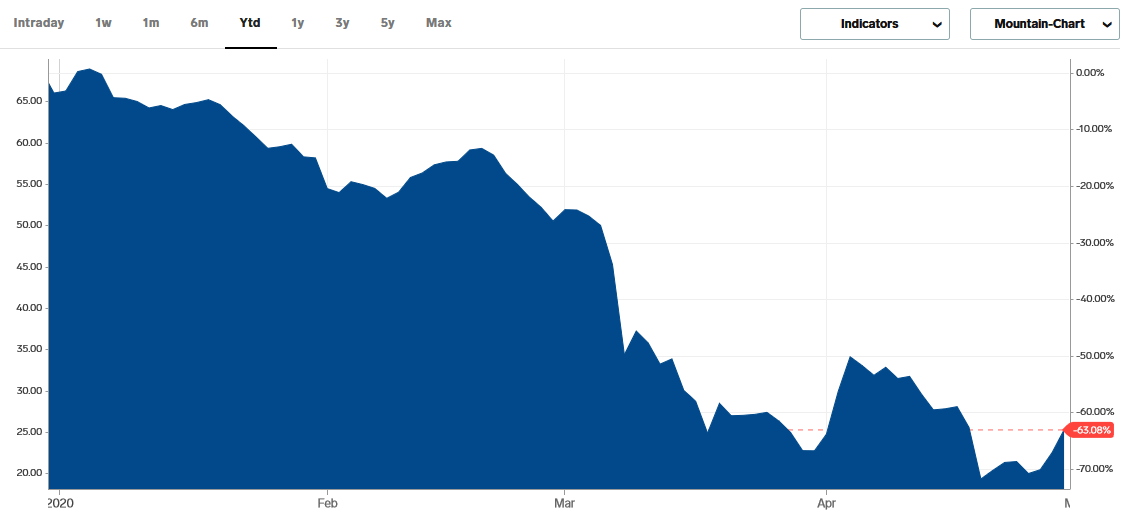

I will admit that I am nowhere near as optimistic as Transocean’s management seems to be. It is unlikely to be a surprise to anyone reading this that the outbreak of the COVID-19 pandemic has been absolutely devastating for oil prices. Brent crude oil traded for $66.00 per barrel at the start of the year and has since fallen to $26.19 as of the time of writing, a 60.32% decline.

{kind=link}

As I discussed in recent articles on BP (BP) and Equinor (EQNR) (see here and here), the largest oil companies in the world have already begun to slash their 2020 capital spending plans, which include both exploration and development spending. These are the two primary tasks performed by offshore drilling rigs so it makes sense that there will likely be fewer drilling contracts awarded this year than what the company originally expected and likely fewer than there were last year. This will almost certainly pressure dayrates downward and thus reduce Transocean’s ability to generate cash flow off of any contract that it manages to get.

The company makes mention of its sizable contract backlog as something that will help it weather the current industry conditions. Indeed, it may have a point here as Transocean has a contract backlog of $9.6 billion, which represents 12.6 quarters of revenue at the current run rate. As these revenues are backed by contracts that the company already has, this is about as close to guaranteed revenues as we can get in this industry. With that said though, one thing that we learned from the oil crash over the 2014-2016 period is that oil companies can and will cancel these contracts when their cash flows are constrained. In order to reduce the risk of this, offshore contractors do typically include a relatively large cancellation fee in the contract but the oil companies may decide that it is more cost-effective to pay this fee than actually honor the contract, as they did the last time oil prices crashed. Thus, while Transocean’s large contract backlog is nice to have, it is certainly no guarantee against potential trouble ahead.

In conclusion, Transocean’s first-quarter results were decent and were likely better than what some expected to see. They were still somewhat disappointing though as the company once again failed to generate positive cash flow or generate a profit. Unfortunately, this may also be as good as it gets for the company for a while as low oil prices have begun to strain the cash flows of its customers and it may even see some contract cancellations. Overall, Transocean looks like a rather speculative play.

At Energy Profits in Dividends, we seek to generate a 7%+ income yield by investing in a portfolio of energy stocks while minimizing our risk of principal loss. By subscribing, you will get access to our best ideas earlier than they are released to the general public (and many of them are not released at all) as well as far more in-depth research than we make available to everybody. We are currently offering a two-week free trial for the service, so check us out!

Disclosure: I am/we are long EQNR. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment