sebastianosecondi/iStock via Getty Images

(This article was co-produced with Hoya Capital Real Estate)

Introduction

When investing outside your home currency, the question of whether you want to reduce or eliminate currency risk comes into play. While there are funds that might do some currency hedging, there are a growing number of ETFs that use a 100% hedging strategy that otherwise invest the same as a sister ETF the manager offers against the same index. The two ETFs reviewed here are:

Hedging’s purpose

During times when the USD is strong, a hedged ETF should result in higher returns compared to an unhedged fund. The opposite should happen when the USD loses value relative to foreign currencies.

Hedging ETFs will use currency forwards to minimize this risk. These forward contracts allow the portfolio manager to lock in a set exchange rate on a set a date in the future. If the foreign currency has declined by the time that date arrives, the ETF will realize a gain on the forward contract. The reverse is true if the foreign currency rises, the value of the contract goes down by the corresponding amount. The result, then, is that most of the impact of exchange rate movements get netted out. Some studies have suggested currency fluctuations generally balance out over the long run, but more recent analysis suggests that hedged funds do outperform unhedged portfolios regardless. Of those I reviewed, that was the case 100% of the time over the past decade.

iShares MSCI EAFE ETF review

Seeking Alpha describes this ETF as:

The iShares MSCI EAFE ETF is managed by BlackRock Fund Advisors. The investment seeks to track the investment results of the MSCI EAFE Index composed of large- and mid-capitalization developed market equities, excluding the U.S. and Canada. The index is a free float-adjusted, market capitalization-weighted index designed to measure large- and mid-capitalization equity market. EFA started in 2001.

Source: seekingalpha.com/symbol EFA

EFA has amassed $48.5b in AUM, which provides a lot of fee income at 33bps to BlackRock. The TTM yield is 2.7%.

Index review

Reviewing the index rules helps investors understand the ETF. MSCI provides this description of their Index:

The MSCI EAFE Index is designed to represent the performance of large and mid-cap securities across 21 developed markets, including countries in Europe, Australasia and the Far East, excluding the U.S. and Canada. The Index is available for a number of regions, market segments/sizes and covers approximately 85% of the free float-adjusted market capitalization in each of the 21 countries.

Source: msci.com/eafe

These are the countries included in the Index:

www.msci.com/eafe

EFA holdings review

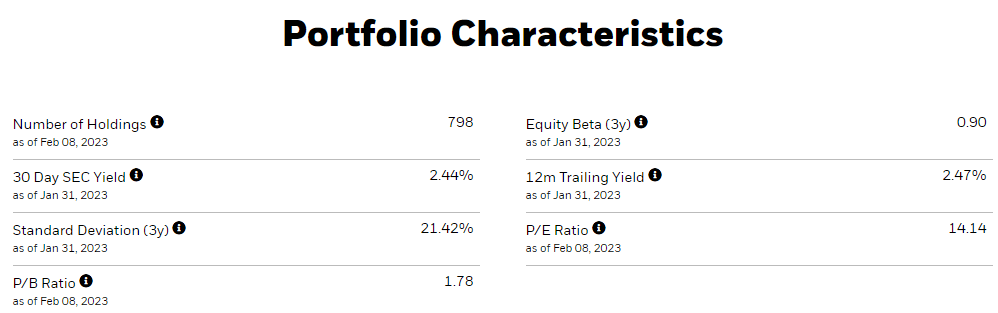

iShares provides some basic portfolio characteristics:

ishares.com EFA

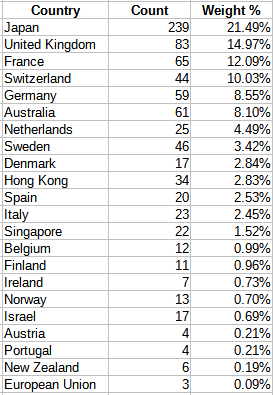

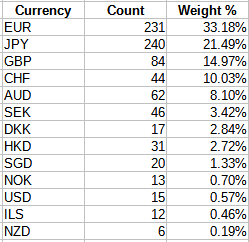

The country allocation by securities and weight is:

ishares.com; compiled by Author

Not surprisingly, the allocation ranking closely aligns with the country’s GNP weight in this set of countries. The regional split is 65% for Europe/Middle East and 35% for Japan, Asia, and Australia. This results in the following currency exposures that the next ETF must hedge against.

ishares.com; compiled by Author

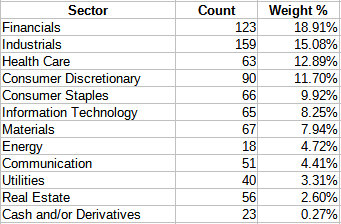

Sectors allocations are:

ishares.com; compiled by Author

Notice where Technology stocks rank compared to a US Large-Cap ETF. Over half of the portfolio weight is contained in the top four sectors.

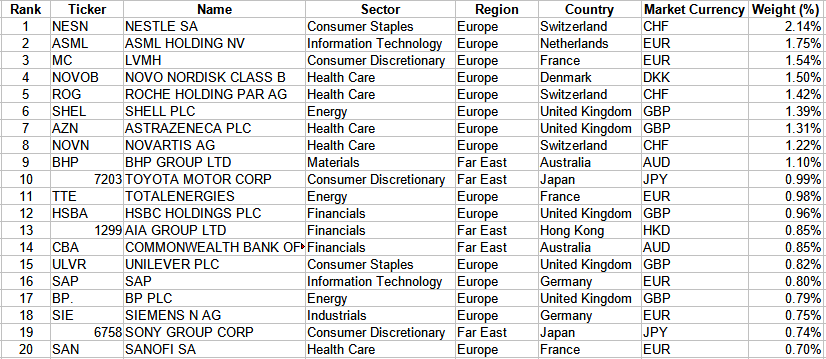

Top holdings

ishares.com; compiled by Author

These stocks, out of almost 800, account for 22.6% of the portfolio. The smallest half, by weight, are 13% of the portfolio. EFA also holds these futures.

ishares.com; compiled by Author

They also hold small positions in each of the 13 currencies.

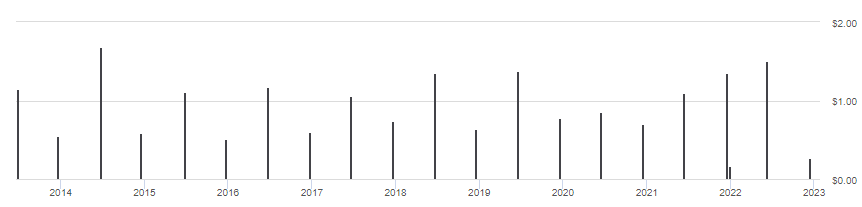

EFA distribution review

seekingalpha.com EFA DVDs

Like many international ETFs, the payouts occur semi-annually, a common practice for the companies held.

iShares Currency Hedged MSCI EAFE ETF review

Seeking Alpha describes this ETF as:

The iShares Currency Hedged MSCI EAFE ETF is managed by BlackRock Fund Advisors. It invests in public equity markets of global ex-US/Canada region and invests based on the MSCI EAFE® 100% Hedged to USD Index. HEFA started in 2014.

Source: seekingalpha.com HEFA

HEFA holds $3.1b in AUM. Here the managers charge 35bps, only 2bps more than the unhedged version. Not counting the large extra payout at the end of 2022, the average yield is about 2.6%.

Index review

Except for the hedging, it is the same Index as used by EFA, which is why the comparison is possible as the hedging effect can be isolated. They provided how the hedging is executed:

The MSCI EAFE 100% Hedged to USD Index represents a close estimation of the performance that can be achieved by hedging the currency exposures of its parent index, the MSCI EAFE Index, to the USD, the “home” currency for the hedged index. The index is 100% hedged to the USD by selling each foreign currency forward at the one-month Forward weight.

Source: msci.com Hedged Index

HEFA holdings review

The only non-cash/Forwards positions is the 98.7% weight from holding the EFA ETF. That slight underweight of the equities held will effect performance relative to the EFA ETF. Each of the currency exposures have seven Forwards against the USD for that currency.

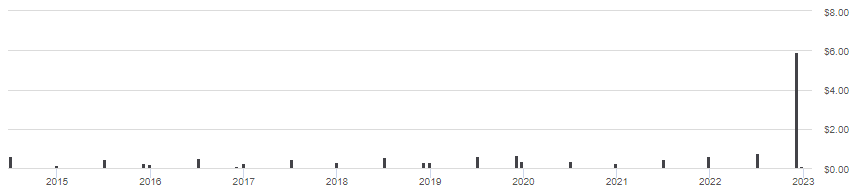

HEFA distribution review

seekingalpha.com HEFA DVDs

The extra December payout of $5.89 was from both Short-term gains ($2.35) and Long-term gains ($3.54). Since the stocks would have generated the same income as the EFA ETF, these must have come from the hedging strategy.

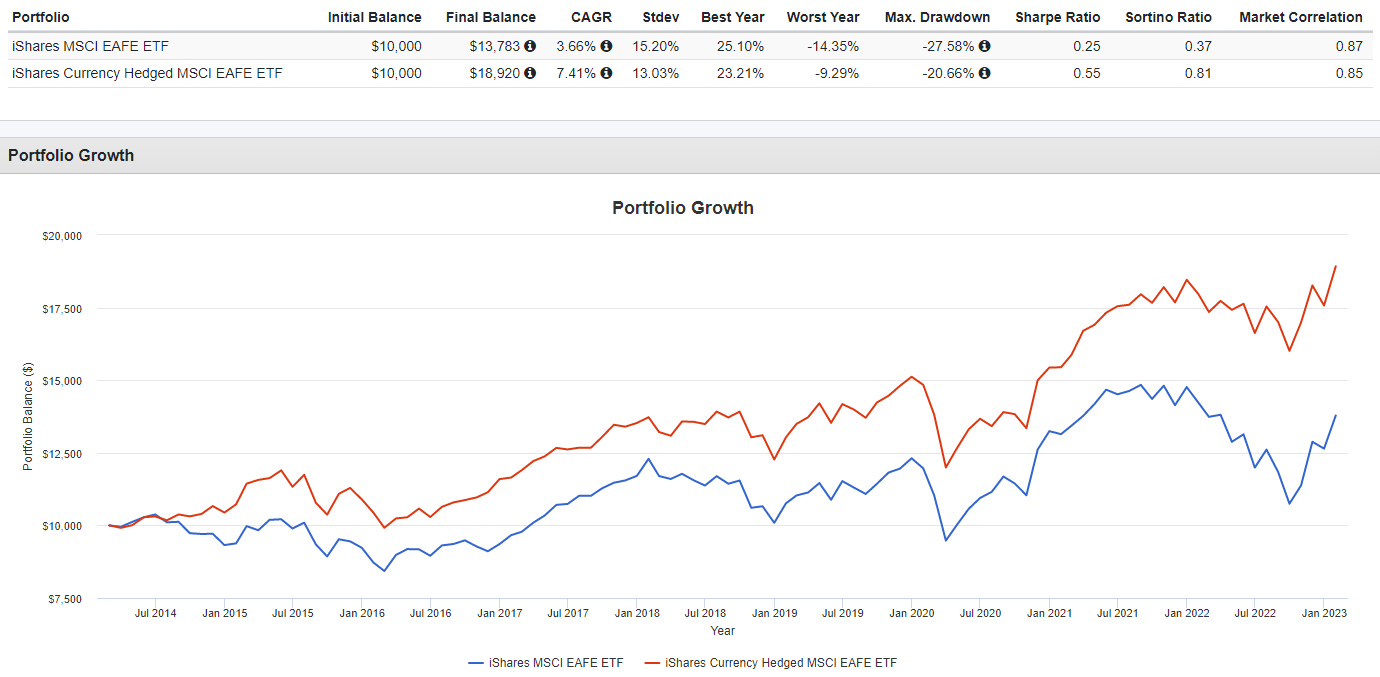

Comparing results

PortfolioVisualzier.com

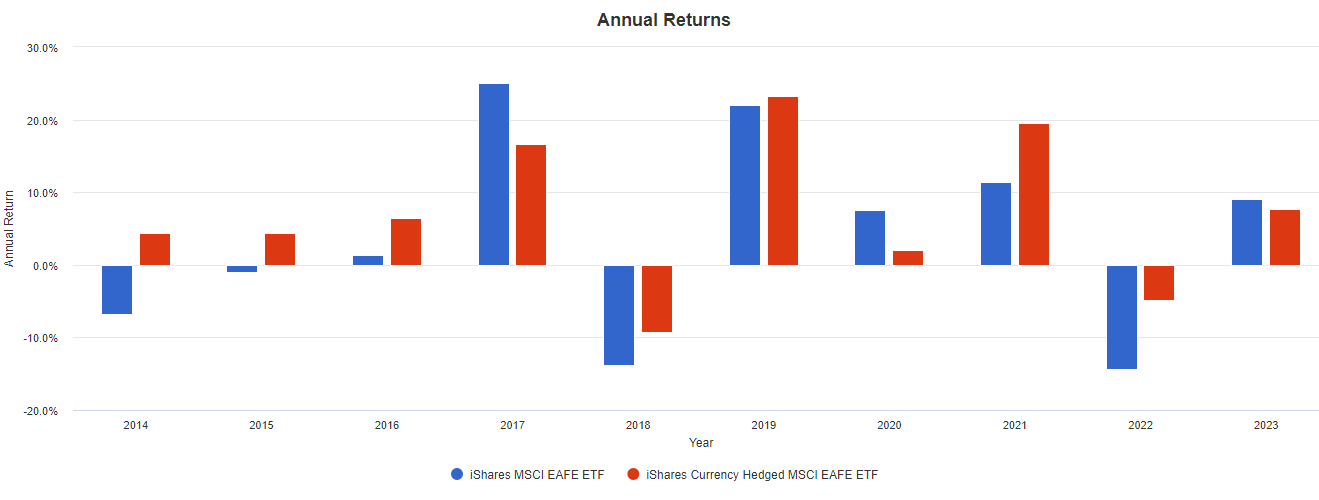

Besides having a superior CAGR, hedging reduced the StdDev and Worst Year results, though the Best Year was impacted. As the next chart shows, HEFA outperformed EFA most years, as measured by the calendar.

PortfolioVisualzier.com

With exchange-rates not being very stable over the past decade, it paid off to be hedging and this occurred in other combinations that I list below.

Portfolio strategy

Like almost everything else when it comes to an investment strategy, not all opinions align. Here are a few “expert” views on the subject.

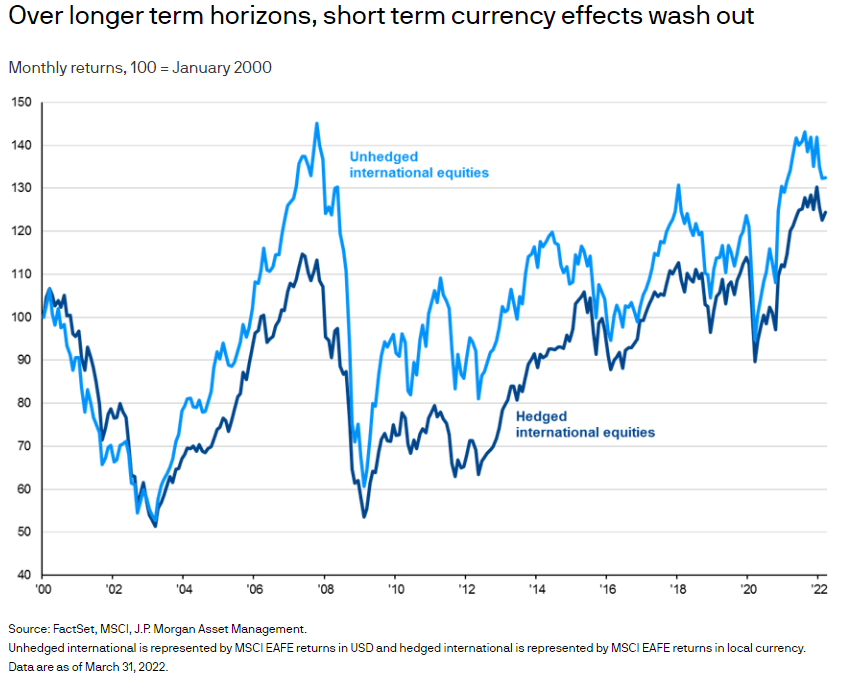

We would suggest allocating to international equities without hedging currency for two reasons: maximizing diversification and boosting total returns. An unhedged international portfolio has demonstrated a more attractive correlation to the U.S. dollar (-0.52). When the U.S. dollar is overvalued and may experience headwinds over the medium term, an allocation to unhedged international equities may not only achieve portfolio diversification benefits, but also contribute to total returns.

Source: am.jpmorgan.com

They presented this chart to show that over time, it all evens out.

am.jpmorgan.com

Russell Investments doesn’t completely disagree as they explain why it should be used.

Leaving foreign currency exposures unhedged could be an implicit bet that the appreciation of the U.S. dollar is over. However, for many investors the foreign currency exposure is not an investment decision they expect to earn returns from but a mere by-product of the equity position. In that case, the unintended risk could be reduced or molded into rewarded risk.

In our view, static currency hedging (on average) reduces risk without giving up expected return, when looking at an appropriately long period. For that reason, some academics have called currency hedging a “free lunch”. This effect is very pronounced for international bonds but also visible for international equities. Between 1997 and today, full currency hedging would have reduced the volatility of global bonds ex-U.S. by roughly 1/2 and that of developed-market equities ex-U.S. by about 17% compared to the unhedged investment.

Source: russellinvestments.com hedging

Is this the time to hedge?

I found this chart to help with this question and some commentary that went with it.

freshbusinessthinking.com hedging

As of that date, they have these observations to consider when deciding if hedging makes sense at this time.

- Relatively high US rates and slowing global growth should help keep the dollar strong in the coming months. Yet the greenback has already appreciated sharply and its current valuations are high.

- Beyond 2023, we expect the US dollar to depreciate further from its multi-decade highs (above chart). As markets begin to anticipate Fed rate cuts and a trough in economic activity.

Source: freshbusinessthinking.com hedging

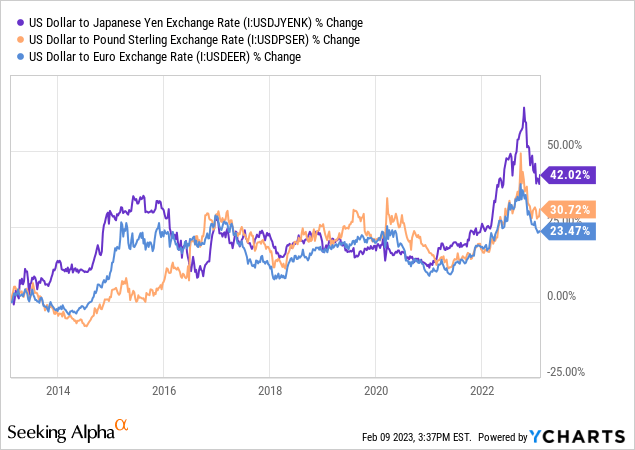

That said, the trend has reversed in the final months of the year, with the Euro strengthening to around $1.08 from below parity with the dollar. The UK Pound has recovered to above $1.20 from as low as $1.03.

Foreign currencies might have further to run. Chris Turner, ING’s global head of markets, says the euro could climb to $1.15 by the end of 2023, and the pound could go as high as $1.30. That would juice any stock gains by another 6% when converted into bucks. “Normally, equity investors think returns in equities far outweigh any ups and downs in currency markets,” says Turner. “But currencies can really add and detract from your overall return.”

Source: barrons.com

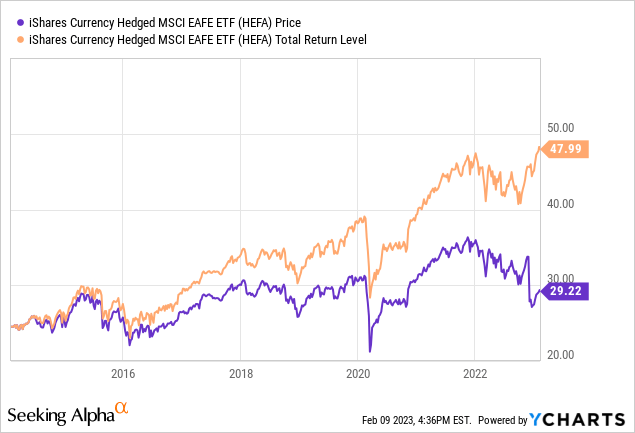

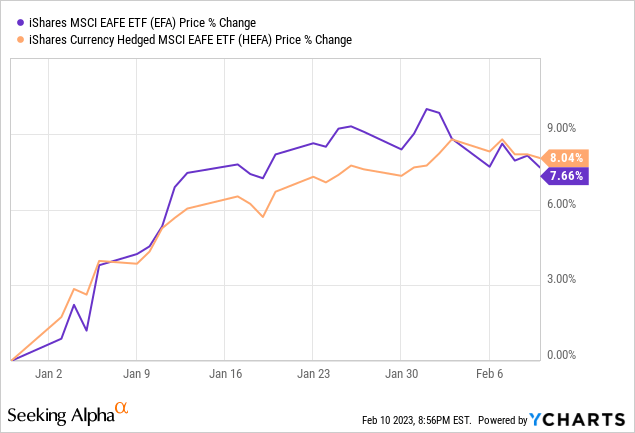

This is how that reversal has played out for the two ETFs reviewed here.

My strategy

I have only part of my international equity exposure hedged. As for bonds, most of the funds I own only hold USD-issued debts, regardless of the country of issue.

Other hedging opportunities

There are more than what I list here where I only looked for where the same manager ran both a unhedged and hedged ETF against the same index; otherwise, there would be noise in the results.

If I found an article on the pair, I used that link versus the Seeking Alpha homepage links.

Be the first to comment