JHVEPhoto/iStock Editorial via Getty Images

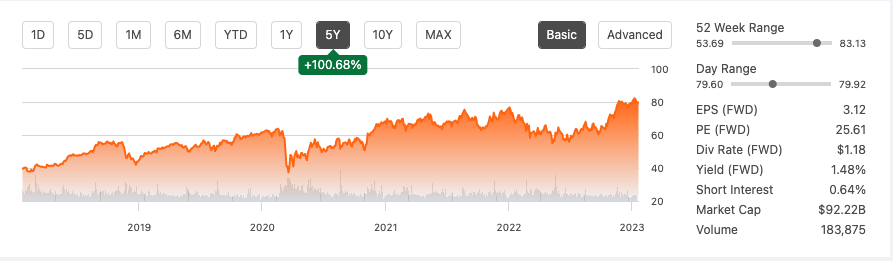

No matter what happens in fashion, everyone loves a bargain. Working with 21,000 vendors to sell recognised brands and designer fashion at 20%-60% under retail price has made thirty-six-year-old The TJX Companies, Inc. (NYSE:TJX) the globe’s fourth largest clothing and ninth largest retail company by market cap, and doubling its sales in ten years to $48.5 billion. It has generously rewarded investors with returns of 100.68% over the last five years.

Five-year stock trend (SeekingAlpha.com)

Due to the company’s minimal online presence, we saw its brick-and-mortar strategy get crippled by the COVID-19 pandemic. That same minimal online presence turbo-boosted demand once stores reopened and the highly anticipated hunt for treasured goods could recommence, resulting in record-high sales.

This year although TJX is in no way immune to freight costs, the inflationary impact on discretionary spending and increased operational costs. However, it is fairing better than other apparel and home fashion retail stocks with its off-price business model, extreme inventory buying power and an increasing number of bargain-hunting consumers, especially during the holiday season. While we can expect growth to slow down due to the company’s sheer size, it has reported a sales growth of 2% over the last nine months to reach $35.4 billion. Its fwd P/E ratio of 26.53 is below off-price competitors Ross Stores, Inc (ROST) and Burlington Stores (BURL) and its stock trades well below the largest market-cap retailers. Although cautious of the downward cash flow trend and the lack of e-commerce growth in the last three years, the business model will remain incredibly compelling in a booming market in the long run. For this reason, I recommend a buy rating.

Overview

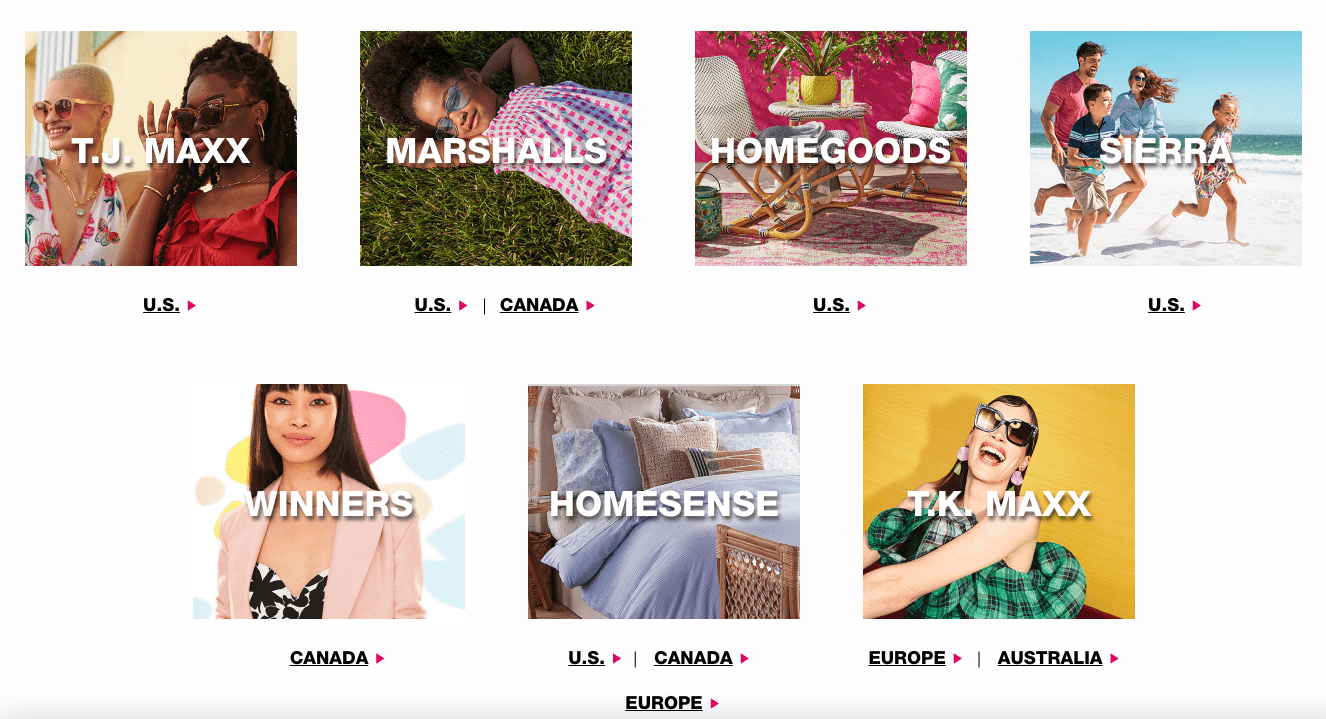

TJX is the leading retailer of off-price apparel and home fashion. TJX buys excess inventory from well-known brands and fashion merchandisers and sells it to consumers 20% to 60% below its regular retail store price through brick-and-mortar, and a much smaller and newer online presence. The business model is simple but challenging to replicate at the scale and speed at which the business turns over competitively priced inventory bought directly from 21,000 vendors. It has a diverse brand portfolio, as seen in the image below, which caters to a variety of consumers, although the typical customer is usually female, middle-to-upper class and between the age of 25 and 54.

Business brand portfolio (tjx.com)

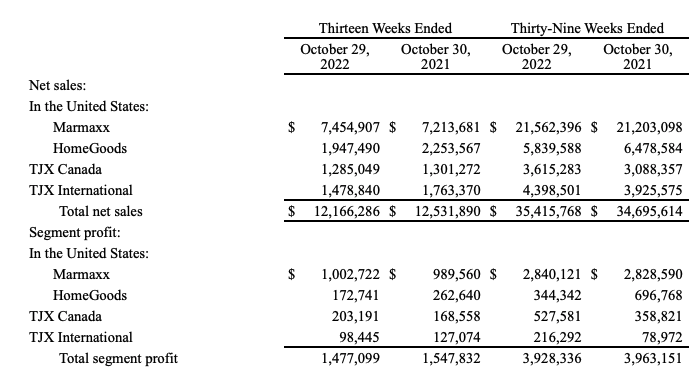

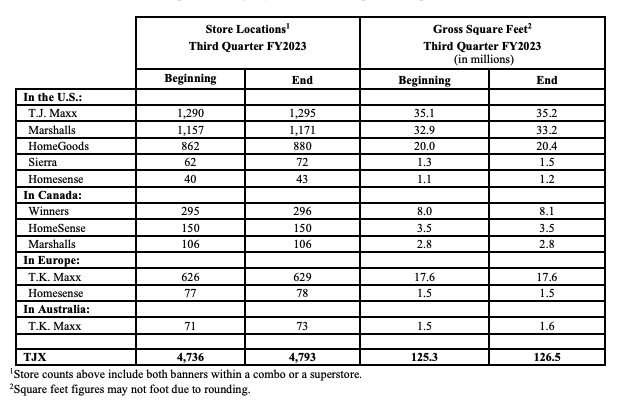

Since Q3 22, it has operated 4,793 stores and has five e-commerce sites across four revenue-generating business segments. Two of these are in the United States, Marmaxx and HomeGoods; there is TJX Canada and TJX International. The diverse portfolio caters to a broad customer target group. Sierra was an online retailer TJX acquired in 2012. However, net sales from e-commerce have been less than 3% for FY22, FY21, and FY20. Over the last nine months, HomeGoods has been the only segment failing to perform. We have seen this downward performance across the home furnishing industries past the stay-at-home and make-your-place pretty COVID-19 boom days.

Sales over three and nine month period across segments (sec.gov)

The business grows through opening stores, whereby it increases foot traffic. It aims at high sales per square foot and rapid inventory turnover and advertises shopping at the stores rather than promoting specific merchandise. Its online strategy has yet to deliver much in terms of results, although its strategy this coming holiday season quarter is posting a weekly flow of new products, which differentiates itself from competitors who do not have access to nearly as large an inventory base.

Store growth locations (sec.gov)

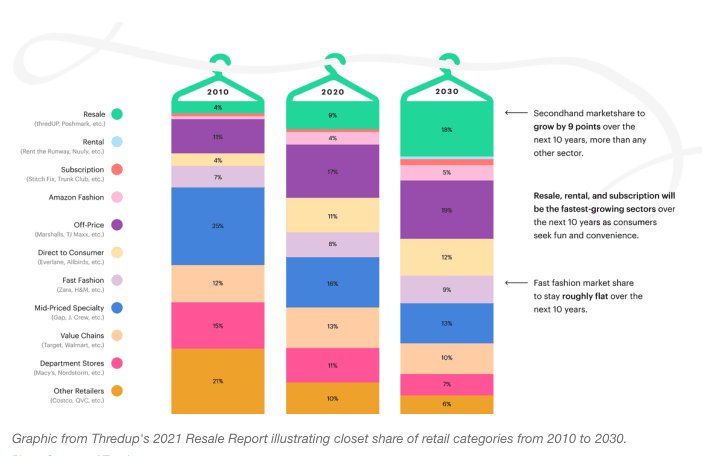

We see exciting dynamics in a study by Thredsup considering the average person’s closet mix. The off-price industry has seen colossal closet share growth while its traditional retail and department store peers have struggled. This trend is expected to grow if we look at the chart below.

Changing closet share dynamics (fashionista.com)

The off-price retail market is expected to see tremendous growth, mainly due to increased online shopping and the consumer behaviour of Gen Zs. Both are areas that TJX has yet to tap into successfully.

Off-price industry growth (reports.valuates.com)

Financials and valuation

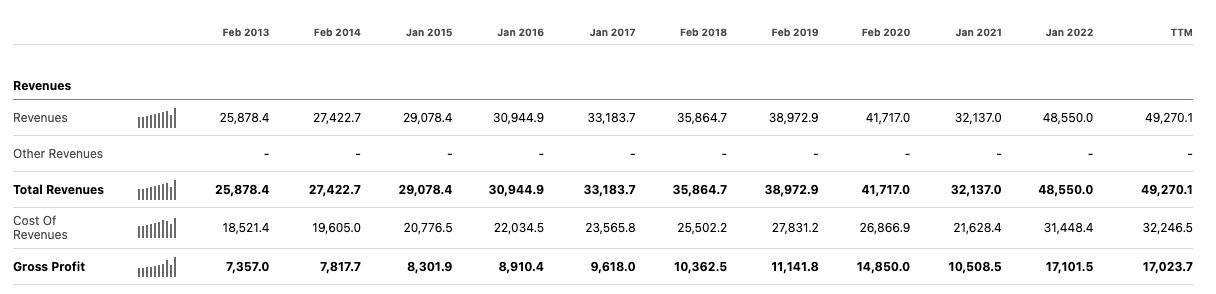

TJX is a gigantic company that has doubled its sales over ten years. Its revenue for the company has been trending upward over the last ten years, with TTM at $49.27 billion. The gross profit margin has improved over this period, from 28.43% to 34.55% if we look at the TTM. The company’s 2020 COVID performance is a clear outlier and made a quick recovery in last year’s financial report.

Annual revenue (SeekingAlpha.com)

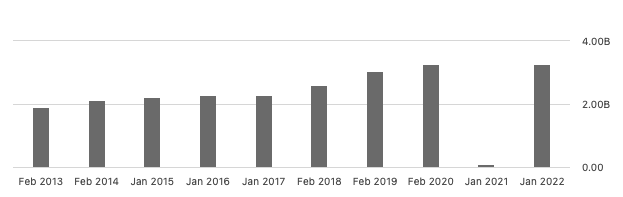

Net income gradually increased over the same period, with an exceptional dip during FY 2020. TTM is currently $3.399 billion, an increase of 78% since FY2012.

Annual net income (SeekingAlpha.com)

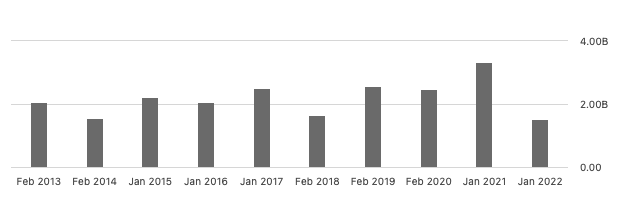

The company has positive annual cash flow, which is essential to pay its dividend program, cover expenses and grow the company further. We can see that the cash flow has not been consistent and has decreased the last two financial years. In the third quarter the company generated $1.1 billion of operating cash flow and finished Q3 at $3.4 billion in cash.

Levered cash flow (SeekingAlpha.com)

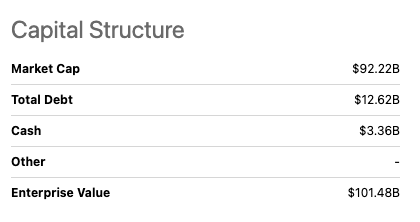

The balance sheet has a high total debt of $12.62 billion and cash of $3.36 billion, with an enterprise value of $101.48 billion. It has a current ratio of 1.6 and a quick ratio of 0.36. Its total debt-to-equity ratio is on the risky side at 222.84%. Furthermore, its total inventory for Q3 22 increased over the quarter to $8.3 billion.

Capital structure (SeekingAlpha.com)

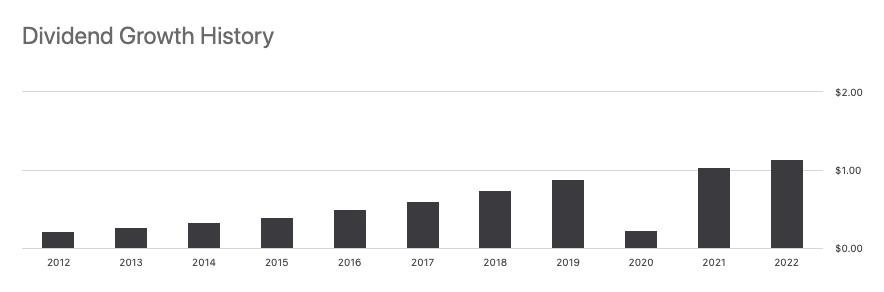

TJX has a long-term dividend program that is paid out quarterly. It has a forward dividend yield of 1.48%, which is not exceptionally high. For those interested in becoming a shareholder, it has an upcoming ex-dividend date on 8 February 2023, which will be paid out on 2 March 2023 at $0.295 per share. Last quarter it returned $843 million in the form of share repurchases and dividends.

Dividend history (SeekingAlpha.com)

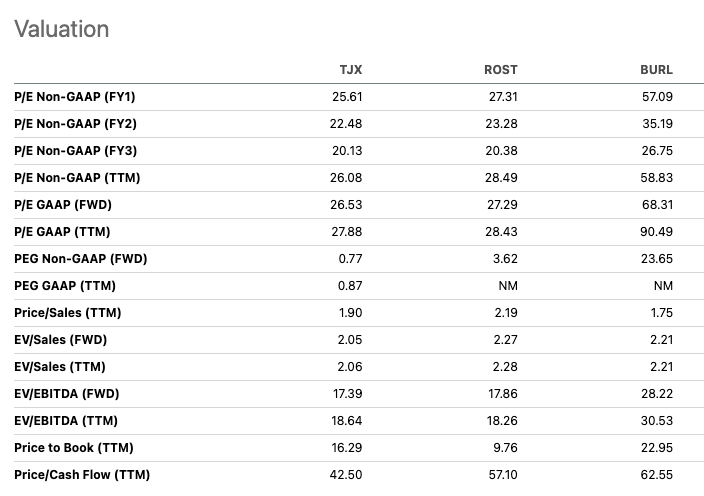

If we compare TJX to its immediate off-price peers Ross Stores (ROST) and Burlington (BURL), we can see that the company has the lowest price to earnings ratio at 26.53, and if we take growth into consideration and look at the PEG TJX may even be undervalued at 0.87.

Relative peer valuation (SeekingAlpha.com)

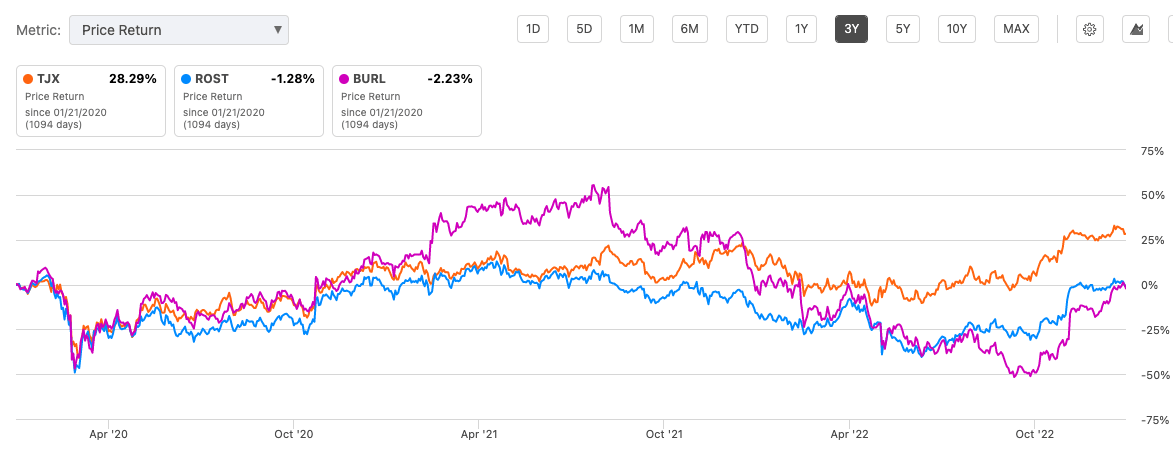

We can also see that the stock has been delivering better returns over the last three years at 28.29%.

Price returns three year trend (seekingalpha.com)

Risks

The retail industry is challenging industry. Small changes in the economy can have dramatic effects on the performance of these companies. We have seen that TJX has been heavily impacted by the rising freight costs due to its fast-paced inventory turnover model and by wage costs due to the 340,000 employees that work for the company. With an expensive operational side to the business, it remains essential to stay effective and efficient in maintaining its margins. On the positive side, freight costs have been reducing and expect to continue into 2023. Another impeding factor is the growing online, digital-born off-price alternatives available on the market. Although they cannot compete against the scope and diversity that TJX provides, they play into the Gen x consumer needs for aesthetically pleasing e-commerce experience and flexible terms. Saks Fifth Avenue split its e-commerce business last year, reflecting a growing value in online shopping. Otrium is a Dutch e-commerce off-price alternative that has recently entered the US market. Lastly, TJX may damage its brand reputation through data breaches and misoperations. Recently TJX was fined $13 million for selling recalled products. This could have long-term reputational effects on the company that may negatively impact its performance.

Final thoughts

TJX aims to become a $60 plus billion dollar annual sales company and is investing in its long-term growth through brick-and-mortar and online growth. It has an easy-to-understand business model that is not easily replicated due to the buying power, inventory turnover capabilities and flexibility to adjust to different economic environments. The company has proven resilient, and although its online sales are minimal, it has excellent continued growth potential in a massive market. Investors may want to take a bullish stance on this stock.

Be the first to comment