jihlav/iStock via Getty Images

In the first half of this year, U.S. stock markets suffered a fall not seen in more than 50 years. The S&P 500 index on Thursday June 30 was more than 20% down compared to January, a drop not experienced since 1970.

The S&P 1500 index, built by Bloomberg and incorporating companies of various sizes, has seen more than $9 trillion in stock value disappear since January. Except for energy stocks, all sectors have suffered value reductions. On Wednesday June 29, Citi announced that it expects the S&P 500 to fall by around another 11% by the end of the year.

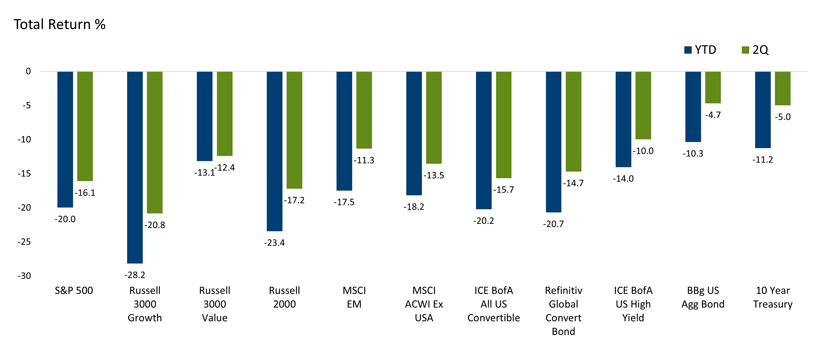

Stock market declines have also occurred in Europe and Asia. The European Stoxx 600 index is down about 17% since January, while the MSCI index for Asia-Pacific markets is down 18% in value in U.S. dollar terms. The FTSE All World index, which brings together stocks from advanced and emerging economies, has also shrunk, by just over 20% so far this year. Figure 1 shows how generally bad the global asset class performance has been in the first half of the year.

Figure 1: Global Asset Class Performance: A Painful 1H22

Calamos Investment

The perception of recession risks in the U.S. and Europe has been a major factor in this flight of investors out of stock markets. Although the numbers in the U.S. labor market in May still showed a high degree of heating, household consumption spending decreased in the month, on top of the numbers in the previous months that have been revised downwards. Consumer confidence indices have plummeted. In housing, the unprecedented rise in mortgage interest rates since 2010 has reinforced this worsening. An Institute of Supply Management (ISM) report, released Friday July 1, showed signs of a sharp drop in the pace of manufacturing activity in June in the U.S. economy.

In Europe, there was also a strong deterioration in indicators of manufacturing activity and consumer confidence in the German economy. The European economy was already expected to feel the full impact of the supply and price shocks resulting from the war in Ukraine. In Asia, the impacts of China’s zero-COVID policy had also already led to a downward revision in growth forecasts for the year. The real change now corresponds to earlier signs that, in fact, the growth slowdown in the U.S. economy has joined that of other advanced economies.

A major factor in the withdrawal of equity investors has been the perception that signs of a slowdown will not reverse the trajectory of rising interest rates on both sides of the Atlantic-previewed for later this year in the euro area-and tightening of financial conditions. At the annual conference of European central bankers in Portugal on June 30, US Federal Reserve (Fed) Governor Jerome Powell even spoke of “some pain” as a bitter medicine necessary to return inflation to closer to the average 2% established as a target.

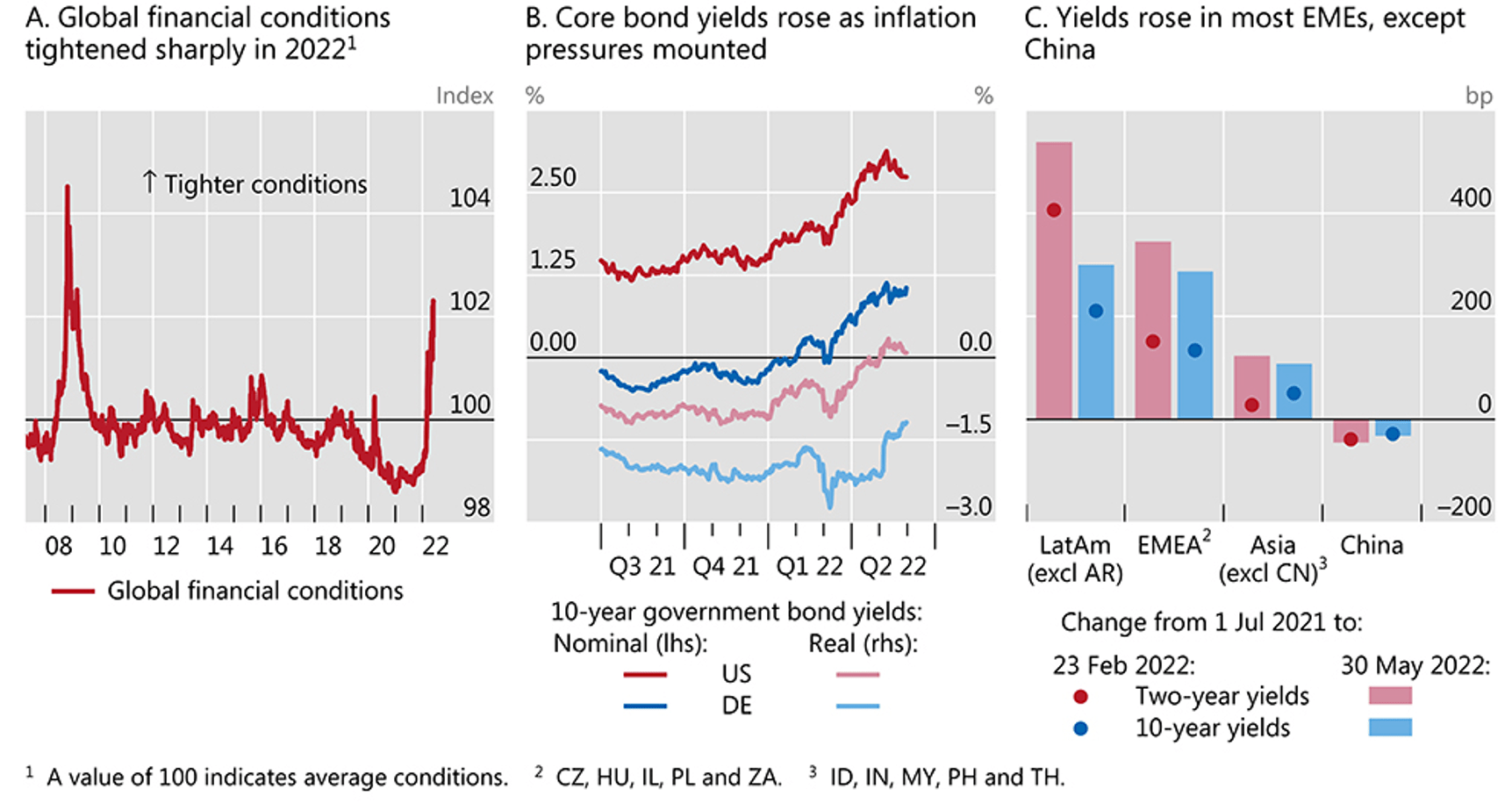

As Figure 2 shows, financial conditions have tightened as government bond yields have risen globally, including in most emerging-market economies, except China. Such tightened conditions are expected to worsen as central banks keep moving along that path.

Figure 2: Financial Conditions Have Tightened as Government Bond Yields Have Risen

BIS

In this context, the stock devaluation fits in with other items of U.S. monetary policy in the pursuit of lower inflation rates. In addition to the ‘quantitative tightening’ – the gradual reduction of the Fed’s balance sheet, without a replenishment of the assets in the portfolio that mature as of this month – the negative ‘wealth effect’ of the fall in the value of shares will help to contain aggregate demand, which corresponds precisely to the Fed’s policy objective.

This is a significant difference from other moments in the recent history of the relationship between Fed policies and asset markets. In 1987, after an almost 30% drop in U.S. stock prices, then-Fed President Alan Greenspan cut interest rates in what became known as a ‘Greenspan put’: a kind of insurance against losses, similar to a put option purchased as protection against sudden losses in value, only in this case provided by the Fed and free of charge to asset holders. In the years that followed, the expectation of bailouts via Fed monetary policies as a reaction to asset devaluations ended up being incorporated as a premium in asset values.

That was the case, for instance, in 2018. But not this time. The commitment to reduce inflation by containing aggregate demand now sounds like the priority.

Strictly speaking, the Fed can ignore falling stocks while keeping an eye on credit markets, not least because there is a direct relationship between credit and bank money creation, and therefore implications for aggregate demand and inflation. But the Fed cannot ignore systemic risks that financial intermediaries will go insolvent.

And how are prices in the credit markets behaving? Risk spreads have widened both for high-risk bonds-rated CCC – and ‘investment grade’ cases. In addition to the risks arising from the rise in interest rates, attention has now turned to the risks of credit and liquidity disappearance.

Judging by reports from credit rating agencies, U.S. non-financial corporations have taken advantage of the facility opened by the Fed, in March 2020 in the wake of the financial crisis triggered by the pandemic, to lengthen debt maturities on favorable terms. The apparent scope for rate hikes, with little concern for their impact on corporate equity structures, provides comfort for the Fed to continue raising rates. Furthermore, rates are still low in real terms when discounted by expected inflation rates this year and next.

How far the Fed will go is an open question. It will depend on the signs of inflation as interest rates move up. A bad sign was the fact that the index that serves as the official reference-the Personal Consumption Expenditures (PCE) Price Index-rose in May and reached a level 6.3% higher than a year ago. In the euro area, inflation in June hit a record 8.6%.

Long-term inflation expectations expressed in 10-year inflation-protected U.S. Treasury bonds are around 2.36% per annum, remaining in the range between 1.5% and 2.5% that has been a trademark for the last twenty years. If inflation shows clear signs of slowing in the months ahead, the Fed may not reach the 3.5%-3.75% range currently expected for the middle of next year. The problem is that, even knowing that there is a time lag between interest rate decisions and their effects, the Fed will not be able to ignore what happens to monthly inflation rates in the period until next year, even if that poses a risk to a soft landing of the economy.

Of course, significant negative surprises on the corporate-finance side could also lead to some sort of ‘Powell put’. What seems more likely, however, is the combination of a global economic slowdown and continued tightening of global financial conditions. Equity markets in advanced economies will continue to exhibit downward slides until the monetary-financial grip eases.

Be the first to comment