garett_mosher/iStock Unreleased via Getty Images

Value investors who have read the early investments made by legendary investors like Warren Buffett and Peter Lynch probably experience a little bit of envy about some of the extraordinary opportunities that existed at that time.

One example was Buffett’s investment in the Sanborn Map Company, where at one point Buffett allocated nearly 35% of the portfolio. While the core map business was experiencing declining profitability, the company had an investment portfolio of high-quality stocks valued at roughly $65 per share, while its shares were trading at roughly $45. In other words, the map business was valued at a negative $20 per share. While it has become extremely difficult to find such clear value investing opportunities in the U.S., where valuations have become extremely stretched, it is a little bit easier in markets where valuations have remained closer to historical averages.

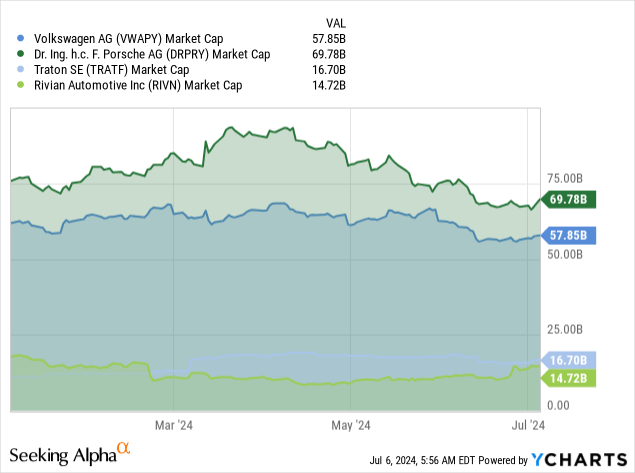

Case in point, Volkswagen Group (OTCPK:VWAPY)(OTCPK:VWAGY), which, considering they own 75% of Porsche AG’s (OTCPK:DRPRY)(OTCPK:DRPRF) capital, and almost 90% of Traton SE’s (OTCPK:TRATF), investors are roughly paying negative $10 billion for the rest of Volkswagen. We are not the only ones to have noticed, with Barron’s pointing out in an article last year that Volkswagen stock was “practically free”. If the company was losing money, perhaps it would be understandable, but the company remains profitable and it has a very credible plan to transition towards electric vehicles. In other words, investors are basically being paid to own Volkswagen’s other brands, including its namesake, Audi, Lamborghini, Bentley, SEAT, CUPRA, Ducati, Škoda, and investments in other public companies. These other investments include a 5% stake in Xpeng (XPEV) bought for $700 million in 2023, and the recently announced $5 billion investment in Rivian (RIVN). The investment in Rivian is a little complicated, with only $1 billion to be invested this year, $1 billion in 2025, and another $1 billion in 2026, with the remaining $2 billion allocated to their joint venture. Therefore, the final shareholding Volkswagen will have in Rivian will depend on how its share price develops over the coming years. Still, it is likely Volkswagen will become one of Rivian’s largest owners.

Share Classes

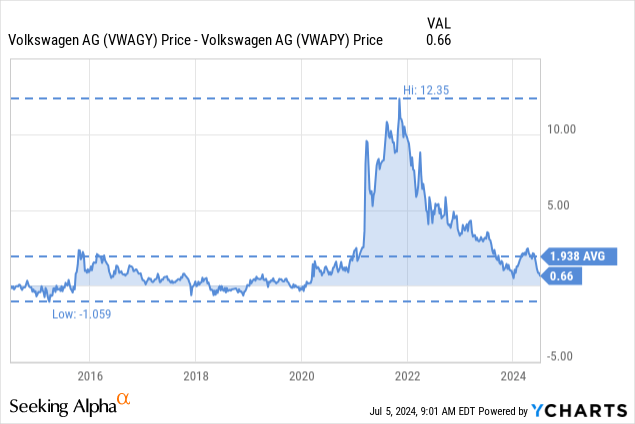

One thing Volkswagen is not is a simple company, that includes the different ways to invest in the company. The company has voting shares, which trade under the symbol VOW in Germany, and preferred shares with the symbol VOW3. The preferred shares are really more similar to non-voting shares than what U.S. investors normally associate with preferred stock. The difference is similar to Alphabet’s (GOOGL) voting shares, which have voting rights, and its non-voting shares (GOOG). The corresponding OTC ADRs in the U.S. are VWAGY for the voting shares, and VWAPY for the preferred non-voting ones. Despite the non-voting shares paying a slightly higher dividend, they tend to trade at a lower price. This has not always been the case, as can be seen below, but the non-voting shares have only traded higher for brief periods of time. Further complicating things, it is also possible to invest in Volkswagen indirectly through Porsche SE (OTCPK:POAHY)(OTCPK:POAHF), which is a holding company that owns about 31% of Volkswagen’s capital, has roughly 53% of its voting rights, a smaller stake in Porsche AG, and some VC type investments.

Competitive Moat

We believe Volkswagen has two competitive advantages that will help it fend off competition to a certain degree, even if the automotive sector is known as a very tough industry. One is its enormous economies of scale, with only Toyota Motors (TM) producing more cars annually. The second is the value of its premium brands, which give the company strong pricing power.

Volkswagen Investor Presentation

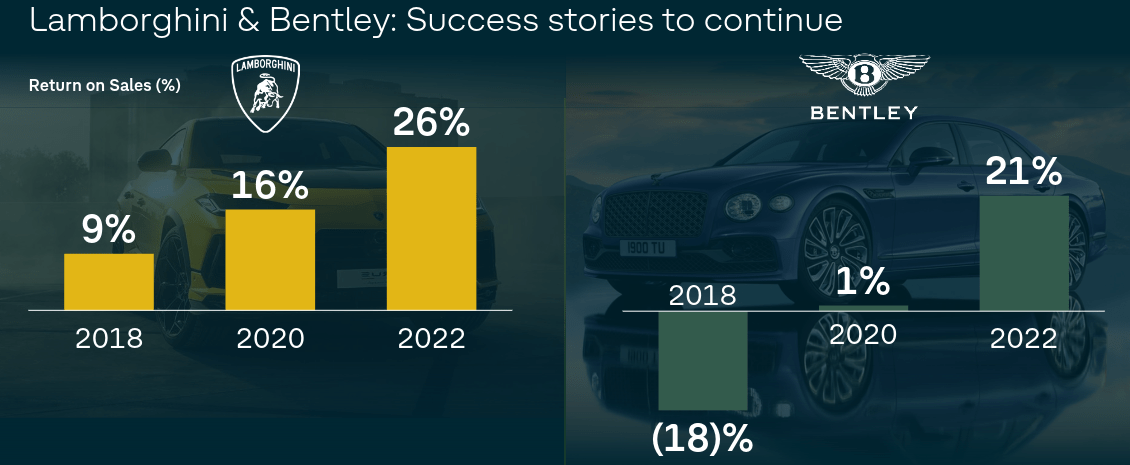

In fact, Porsche has been considered the most valuable luxury brand in the world. Ferrari (RACE) is considered less valuable, despite the high premiums the brand commands, given the significantly lower volumes produced. Other brands that give Volkswagen premium pricing power include Lamborghini, Bentley, and Audi. In fact, Volkswagen is considered to have a similar market share of the premium market to that of rivals BMW (OTCPK:BMWYY) and Mercedes-Benz Group (OTCPK:MBGYY).

Volkswagen Investor Presentation

Rivian Investment and Partnership

One reason we are excited about the Rivian investment and partnership, is that it might help solve one of the big issues Volkswagen has been fighting: software bugs. Volkswagen calls its automotive software division CARIAD, and it had previously disclosed it had plans for a comprehensive re-alignment of this business segment. It therefore makes complete sense to join forces with Rivian, which we believe has strong automotive software development skills, even if Volkswagen already has its wholly-owned electric pick-up startup Scout. For Rivian, Volkswagen’s investment gives it a credible path towards profitability, which is expected to happen once the company starts delivering its mass-market R2. Rivian recently had its investor day, and we were impressed with the presentation, the advanced software functionalities, and the planned cost reductions.

Rivian Investor Day

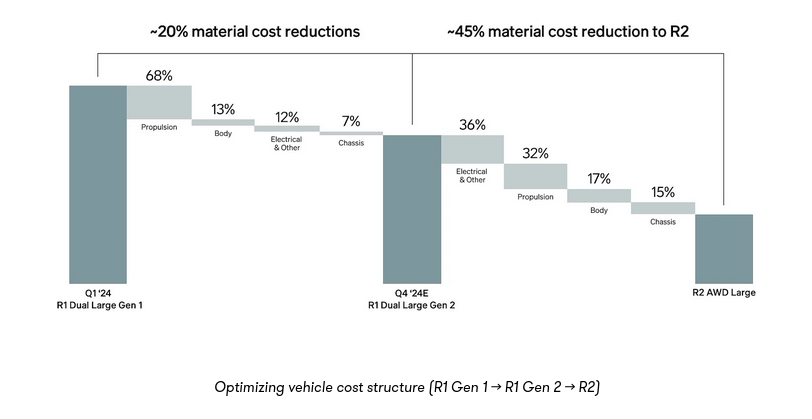

While Rivian is expecting a meaningful cost reduction for its second generation R1 model, it is really the R2 where a major improvement is expected. If things go according to plan, it is possible that the company could achieve profitability with the R2. While we see enormous potential with Rivian, there is also significant risk as the company continuous burning cash at a rapid pace. Right now we are happy having an indirect exposure to Rivian through Volkswagen, especially considering that at the current Volkswagen valuation, it appears to be basically given for free.

Rivian Investor Day

Financials

The Q1 financial results the company reported at the end of April were not particularly good, with the company itself saying that, “Q1 was never going to be our best quarter”. Part of the reason is that the company’s most important product launches are scheduled for later in 2024, particularly for the Audi and Porsche brands. It is also taking some time for the Volkswagen brand efficiency program to deliver results, in part due to wage increases started in 2023, and are not showing their full impact. Still, the company managed to deliver €75.5 billion in revenue for the quarter, which is a decrease of only about 1% year-over-year. Volkswagen also experienced some supply shortages that affected Audi vehicles with V6 and V8 engines.

Despite significant headwinds over the past decade, including some of its own making like the emissions scandal, the company has managed to grow revenue and restore profitability. More recent headwinds included the initial impact of the COVID pandemic, and currently the higher interest rate environment impacting potential customers that would have considered buying a new car using a loan. The company has been particularly open about its disappointment with the operating margin its namesake brand is generating and has an efficiency plan aimed at significantly increasing the VW brand’s margin to ~6.5% by 2026, from the ~3.6% it delivered in 2022. Reducing losses in the software division (CARIAD) should also significantly help improve profit margins.

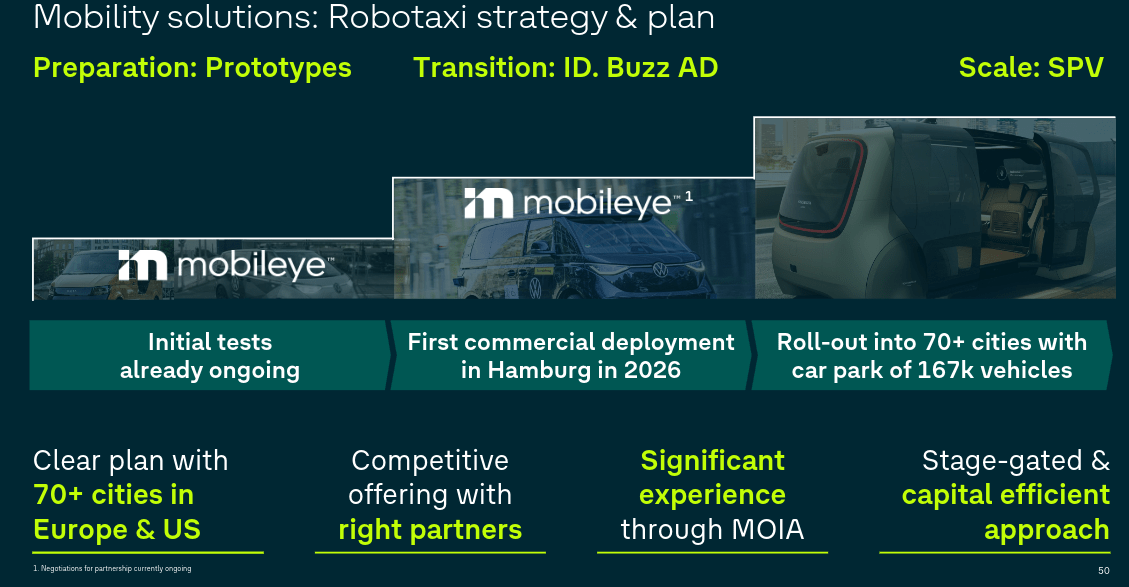

Robo-taxi Strategy

It will come as a surprise to some investors, but Tesla (TSLA) is not the only company with a robo-taxi strategy. Volkswagen’s strategy is, however, more similar to Microsoft’s (MSFT) AI strategy in the sense that it depends on strategic partnerships.

For example, Microsoft has invested in and made exclusivity deals with OpenAI and Mistral, while Volkswagen is working with the likes of Mobileye (MBLY) and Qualcomm (QCOM). We think Rivian is likely to help in some way as well, as they are also working on autonomous driving technology.

Volkswagen Investor Presentation

Trucks

As mentioned at the start, Volkswagen did a partial IPO of its truck business, which was well received and has been doing well operationally. For example, in the most recent earnings call, management shared that Scania is operating with double-digit profit margin once again. With Traton SE showing a market cap of ~$16.7 billion, it is a significant asset for the company. Volkswagen is therefore considering selling more shares to increase the free float, and generate cash for other investments.

Volkswagen Investor Presentation

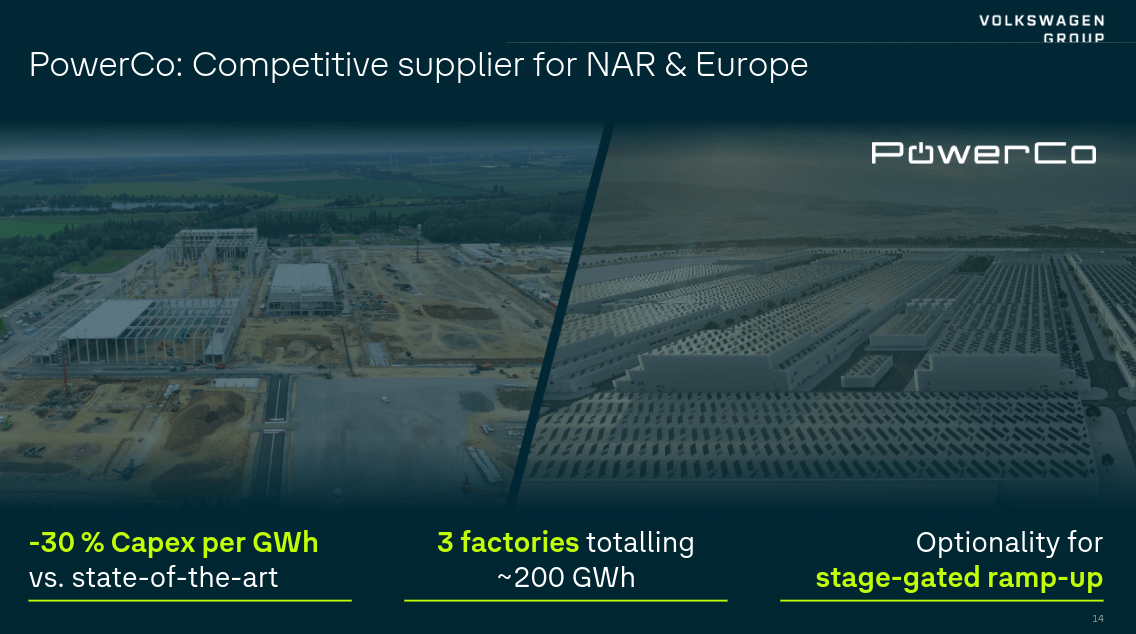

PowerCo

One division that will certainly require more investment is the battery company, which Volkswagen has named PowerCo, and which it plans to eventually introduce to the stock market too. Volkswagen’s ambition is for PowerCo to become a global battery champion, with economies of scale unlocking cost advantages. It is currently planning three factories, one in Canada, one in Spain, and another one in Germany. It believes this business could eventually supply approximately 50% of Volkswagen’s battery needs. It is planning for up to ~200 GWh capacity in 2030, and believes it can deliver EBIT margins above 10%.

While the company plans to be flexible in terms of technology, it is working closely with QuantumScape (QS), in which Volkswagen has previously invested and had a 17% equity stake at the end of 2023. In early 2024, PowerCo and QuantumScape announced promising results from the testing of some of QuantumScape’s solid state batteries. Volkswagen is also evaluating LFP battery technology which is expected to reduce battery costs by one-third. Improvements in battery costs are critical for the company to achieve cost parity with Chinese battery electric vehicle (BEV) leaders by 2026.

The Volkswagen 2023 annual report also shows a 23% equity interest in one of Europe’s most talked about clean tech startups, Northvolt AB. Northvolt is also planning several gigafactories in several different locations.

Volkswagen Investor Presentation

China

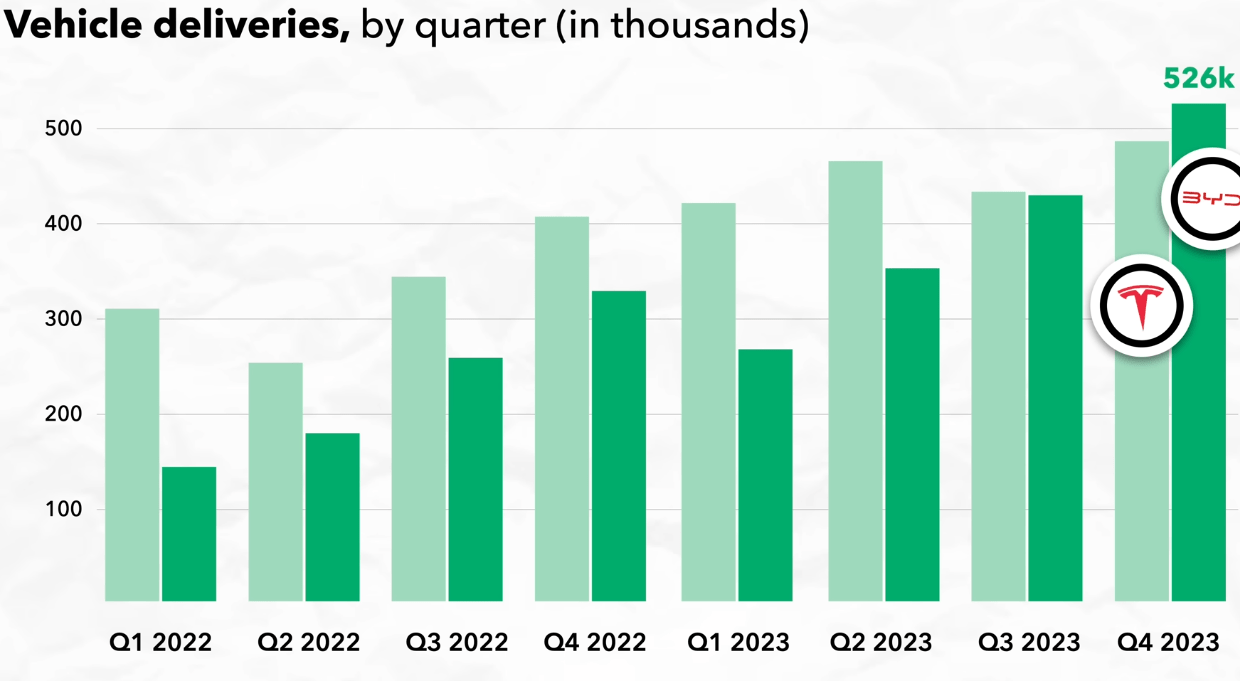

When it comes to China, for Volkswagen its the best of times and its the worst of times. On the one hand they have become the #1 foreign automaker in the country, but on the other hand they are facing steep competition from fierce EV makers. In some cases these EV competitors have found ways to produce electric cars at surprisingly low prices, such as BYD (OTCPK:BYDDF), in part thanks to their vertical integration and advances in areas such as battery technology and software development.

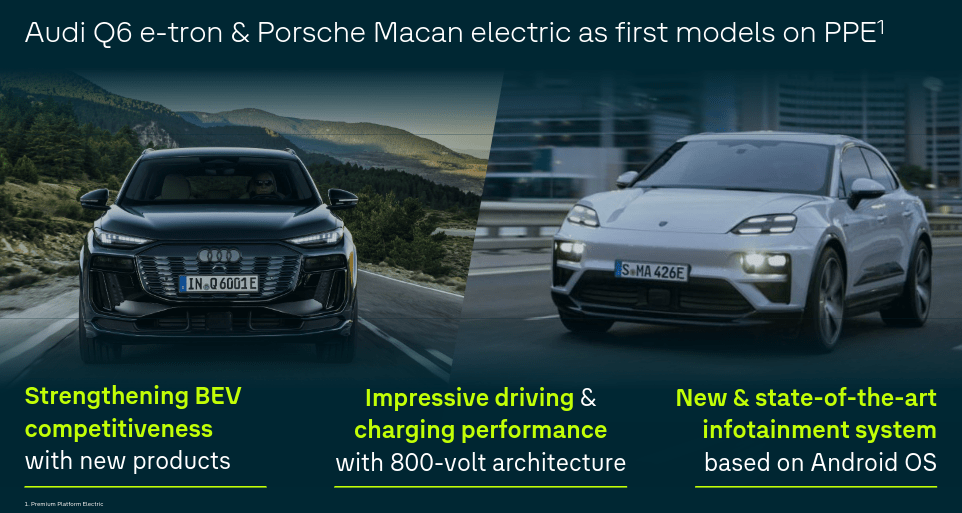

Still, we think being forced to compete with these Chinese companies is a blessing in disguise for Volkswagen. It has forced the company to improve its efficiency and productivity, close technology gaps through joint ventures and partnerships, and work on a long-term strategy to remain profitable while fending off competition. Some of its competitors more focused on North America or Europe are simply lobbying for tariffs, which will only delay the inevitable. The horse-and-buggy industry could have lobbied extremely hard and perhaps delayed the transition, but cars were eventually going to win. In any case, Volkswagen is coming up with very compelling models on its Premium Platform Electric (PPE), with the Audi Q6 e-tron and the Porsche Macan already generating significant excitement.

Volkswagen Investor Presentation

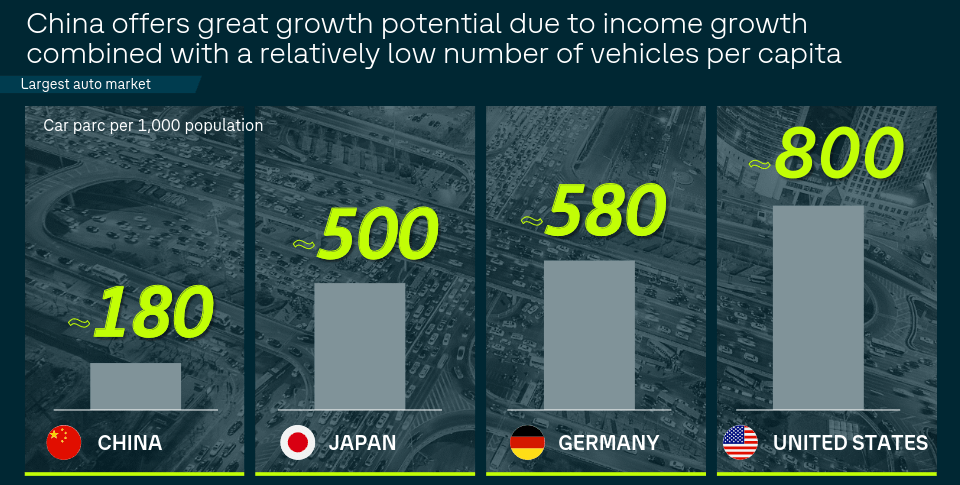

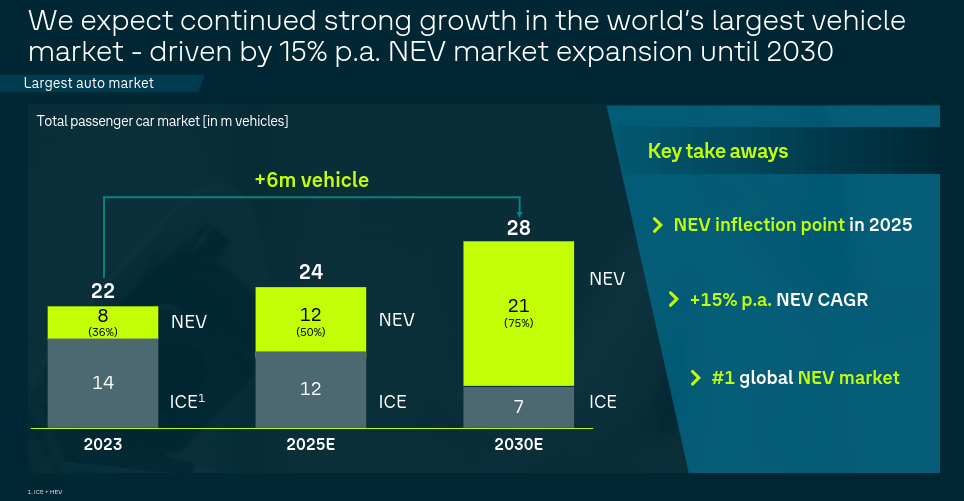

In 2023 Volkswagen even managed to slightly increase its already massive market share for internal combustion engine cars in China by a little over 1%, and importantly, it also increased its battery electric vehicle (BEV) market share by 2%. While 2% market share gain might not sound very significant, take into consideration that it took an almost doubling in its BEV sales to accomplish it given how fast EVs are growing in China. Despite the country already being the largest auto market in the world, Volkswagen still sees opportunity for growth given that China’s cars per capita is still significantly below most developed economies.

Volkswagen Investor Presentation

However, the company is well aware that most of that growth will come from EVs, and that they need to be able to also compete at lower price points. The company therefore needs to reach cost parity with the local BEV leaders, which it expects to accomplish by 2026. This will come from cost reductions from new battery technology and increasing the use of local R&D skills, as well as partnerships with companies like Xpeng.

Volkswagen Investor Presentation

Tough Competition

As can be seen in a YouTube TLDR Business video, in 2011, Elon Musk laughed hard when asked about the risk that Chinese rival BYD (OTCPK:BYDDF) posed to Tesla. He is probably laughing a lot less now that BYD is outselling Tesla some quarters. The point is that competition with Chinese auto manufacturers is going to be fierce, and companies will need to continuously innovate and lower costs if they want to retain their market share. Of course, this is not only a problem for Tesla but for the entire industry, and it is one of the reasons many auto manufacturers are trading with extremely depressed valuations.

TLDR Business

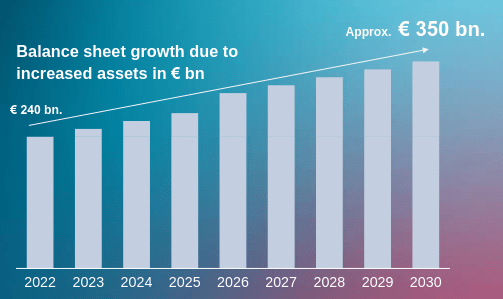

Balance Sheet

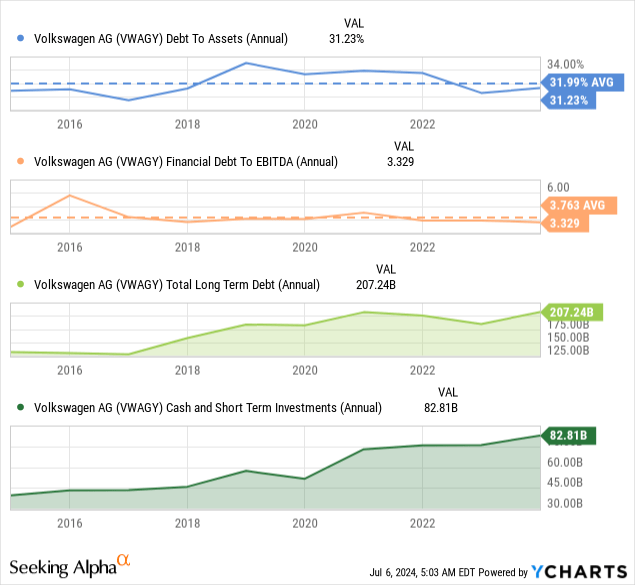

The transition to electric vehicles, building the required gigafactories, and investing in autonomous driving and other advanced software features is going to be expensive. Fortunately Volkswagen’s balance sheet is in good shape, even if some investors worry that the company has too much debt. Most of the debt is related to the financial services arm of the company that provides auto loans and leasing services. The automotive net liquidity at the end of Q1 was €37.2 billion, clearly a very significant sum.

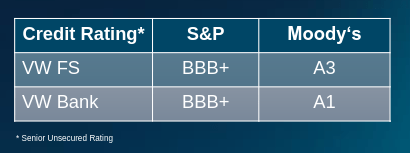

Looking specifically at the financial services divisions, we are reassured by their excellent investment grade credit ratings by S&P Global (SPGI) and Moody’s (MCO).

Volkswagen Group

Investors should not be surprised if this debt continues to increase as the company provides more loans or leases to customers. Volkswagen has even provided guidance as to how they expect the balance sheet to grow in the coming years. Investors should simply remember that this debt has collateral, and that the financial arm has usually been a source of profits for the company.

Volkswagen Investor Presentation

Outlook

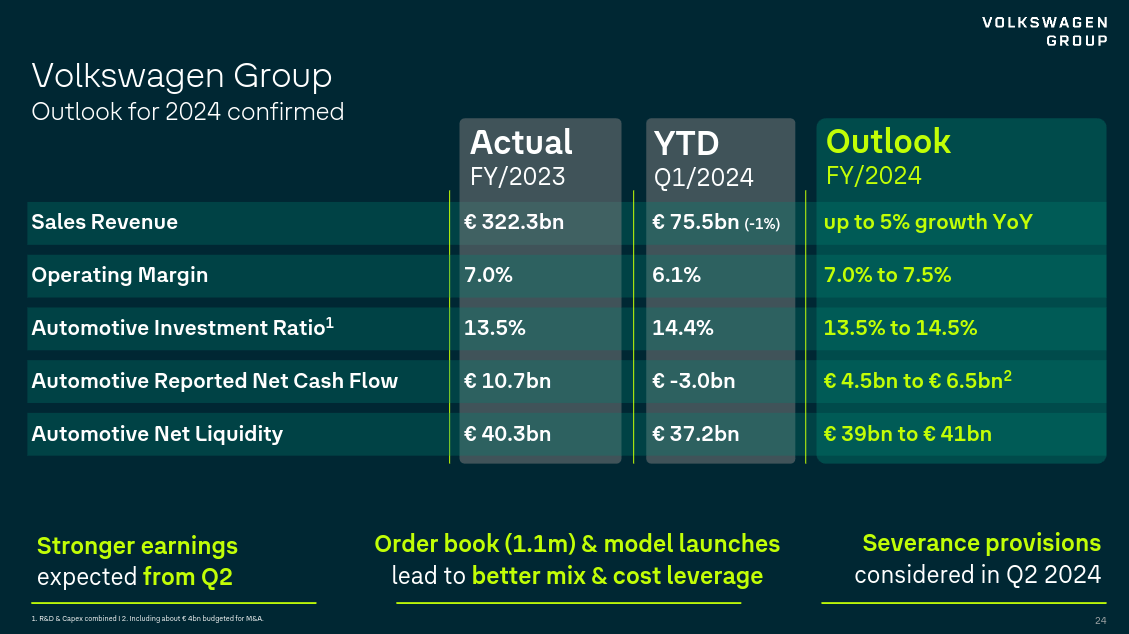

During the earnings call management sounded confident about its fiscal year 2024 guidance, pointing to an order book that currently stands at 1.1 million cars and a massive increase in the order intake of BEVs of more than 100%.

Volkswagen continue to expect revenue to grow by up to 5%, with an operating margin in the range of 7% to 7.5%. In order to meet guidance the company is factoring a step up of sales at Porsche and Audi based on the ramp-up of their new models. The company also confirmed its BEV share target of 9% to 11%. Looking further ahead, the company will have some attractive mass-market EV options, including the recently revealed Škoda EPIC which will be available starting in 2026 at a very attractive price of around €25,000.

Volkswagen Investor Presentation

Valuation

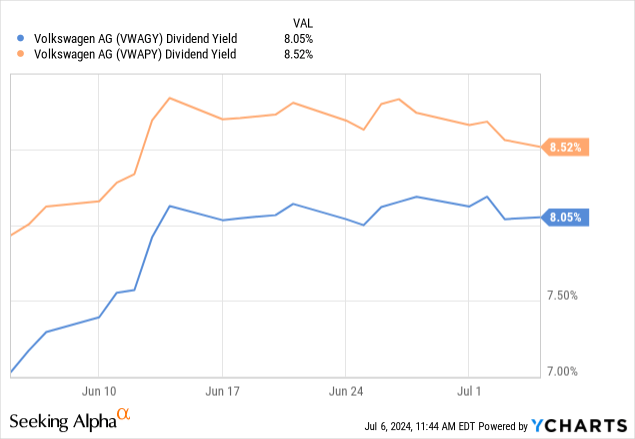

To get an idea of how cheap Volkswagen shares have become, the dividend yield is above 8% for both VWAPY and VWAGY, despite the company having a policy of distributing only about 30% of earnings.

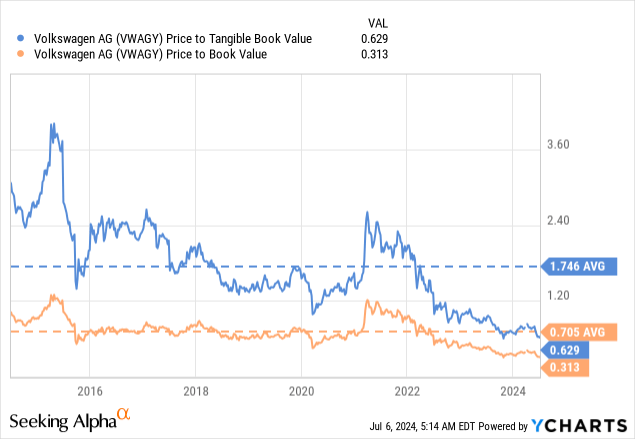

Shares are trading at less than a third of their book value, and even if we remove intangibles, they still trade at a roughly 30% discount to tangible book value. And we would argue that the goodwill in the balance sheet is probably quite real, considering the value of brands like Porsche, Lamborghini, and Audi, not to mention patents and other IP.

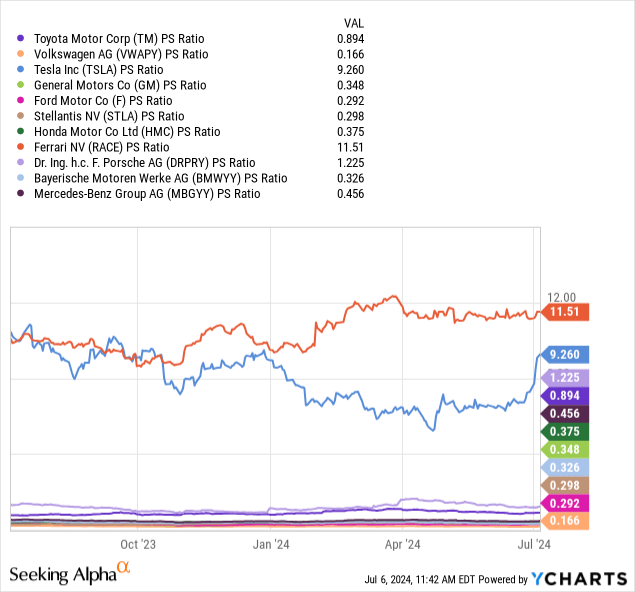

Most auto manufacturers are sporting low valuations, with most competitors trading with a price/sales ratio below 1. Still, Volkswagen has the lowest multiple even though we would argue it has a stronger position compared to many of its rivals. Tesla’s price/sales multiple is 55x higher than Volkswagen’s, and Ferrari’s multiple is almost 70x higher.

If you think this valuation does not make any sense, you are not alone, as Morningstar (MORN) estimates Volkswagen’s fair value at more than 3x current prices. For its part, Barron’s published early this year an article on “the mystery of Volkswagen’s ridiculously low valuation.” According to Barron’s calculations, after adjusting for net cash and leasing Volkswagen is basically trading for negative times earnings.

Stellantis has a market capitalization of about $63 billion. Net of cash and leasing, that number is closer to $30 billion, leaving Stellantis shares trading for 2 times estimated 2024 earnings. BMW shares trade for about 3 times earnings. Ford Motor and Toyota shares both trade for about 4 times earnings, after adjustments, while GM stock trades for roughly 3 times. Yet Volkswagen shares trade for negative 3 times earnings.

Risks

Despite the extremely low valuation, investing in Volkswagen still comes with significant risks. The company has had serious issues with its software development and is in the process of restructuring CARIAD. It remains to be seen if they can right the ship, and if the Rivian partnership will provide much needed help in this area.

Then there is the issue of fierce competition from Chinese, Japanese, and Korean auto manufacturers. While Volkswagen has very strong brands, its rivals often have labor and manufacturing cost advantages. The company is also less agile, and has to take several stakeholders into consideration, including labor groups that are part of its board. Finally, the company suffered significant reputational and financial damage from its emissions scandal, and it has to adapt to changing regulations around the world.

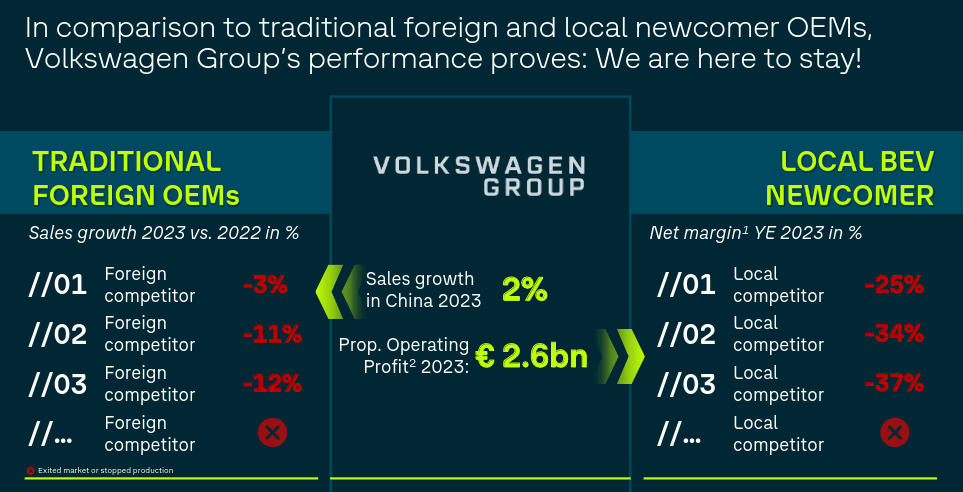

The company has to face all these challenges at the same time that it has to work on the transition to EVs. Still, we see signs for optimism and believe that some of these risks are mitigated by the company’s competitive advantages, such as its very strong brands and attractive designs. As the slide below shows, Volkswagen is delivering better sales growth compared to other foreign competitors in China, while local BEV manufacturers are seeing their profit margins significantly decrease.

Volkswagen Investor Presentation

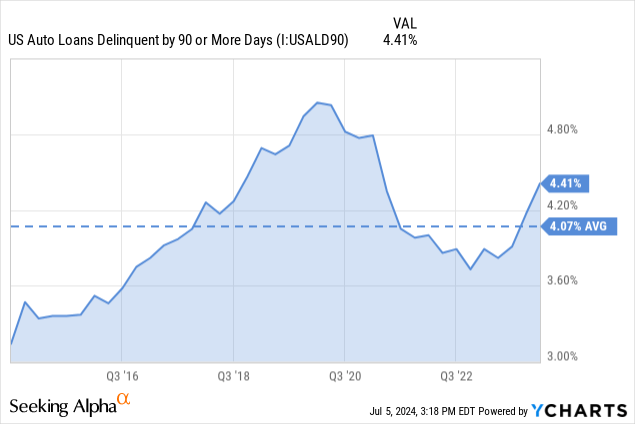

Another area investors should keep an eye on is auto loan delinquencies. Volkswagen reported that operating results in Q1 for its Financial Services division fell by about a quarter to €881 million or a 6% margin. According to management this decline reflects the continued normalization of used car prices and provisioning for residual value risk, as well as the significantly increased interest rates. Still, delinquent auto loans in markets like the U.S. are clearly trending higher and could further spike if the economy enters a recession.

Conclusion

While the auto industry is not one we particularly like, there are times that the valuation becomes so depressed that it makes no sense. This is the type of situation many value investors dream of, like when Buffett purchased shares in a maps company for negative $20 per share after adjusting for their investment portfolio. Similarly, Volkswagen appears to be valued at negative $10 billion after adjusting for their holdings in Porsche AG and Traton SE. Which means that investors are being paid to take the rest of the company, including Lamborghini, Audi, PowerCo, and minority investments in companies like Rivian.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment