andresr

If you want to invest in Ad Tech, The Trade Desk (NASDAQ:TTD) can be your top pick. TTD is a leading pure-play Demand Side Platform serving digital programmatic ad buying over the Open Internet on the globe. TTD has a massive Total Addressable Market of $816B according to TTD’s Q3-22 earnings presentation. Its financial performance is highly predictable, as 95% of its revenue comes from master service agreements (MSAs).

Trade Desk’s Pure-play DSP Advantages

TTD is a unique company because 1) it is serving Ad buying over the Open Internet (as opposed to the Walled Gardens); and 2) it is a pure-play DSP as opposed to a Conglomerate. TTD’s unique positioning has turned into its advantage.

First, TTD remains nearly intact post IDFA thanks to its efforts on UID 2.0. UID 2.0 is an industry-wide approach that leverages email-based identifiers to enable targeted advertising without the reliance on third-party cookies. TTD self-reported that “while the messaging and creative was the same for all strategies, the click-through rate for UID2-based display ads was 2.9 times higher than for The Trade Desk’s non-UID2 ads. The cost per acquisition for the UID2-based segment was $1.60 compared to $5.37 for non-UID2-based segments (a 2.4 times improvement).”

UID 2.0 has kind of united all efforts in enabling richer data (as opposed to competing and isolating from each other) on the Open Internet side. The partnership between TTD and LiveRamp is one of the examples. Another evidence is that UID 2.0 is transitioning from TTD to independent governance.

Second, TTD as a pure play is the best partner that others, e.g. Streaming Services, and Retail Media Networks, are eager to go after without worries of competition. In Aug-21, Walmart Connect launches its brand-new DSP (built in partnership with TTD) to expand offsite offerings to advertisers. In Jul-22, Disney announced its agreement with TTD as part of its bold vision in CTV. The Ad Tech ecosystem may continue to evolve through competitions and consolidations, and TTD, in its unique position, will continue to see many ways to collaborate with winners along with the industry’s evolution.

Third, TTD as a pure play is more aligned with buyers (advertisers and agencies). Unlike the Walled Gardens players, TTD does not sell any media, and does not arbitrage over media. Its platform is all in a Self-service manner, which means buyers operate the platform and reporting tools for best ROAS. All the transparencies helped TTD gain trust as well as allocated budget from buyers.

TTD’s Profitability Outlook

TTD was founded in 2011, and became profitable in 2023, which is impressive given that TTD runs a self-service business (less DSP fee) with 100% 3P Media (which means 70%-80% of gross revenue is passed through to Publishers). TTD is estimated to grow its revenue to $1.6B in 2022, and generate ~$100MM in Operating Income (6% Operating Margin). Please note, TTD revenue is net based (Gross revenue less payout to 3P media partners), unlike most of other Ad Tech companies. Its Gross Revenue is ~$8B in 2022.

In my opinion, TTD’s self-service and agency/head focused business is well positioned to further improve its profitability. First, the self-service model means it does not rely on a ton of labor support on campaigns. Second, the agency/head focused model means it serves buyers with high spend per buyer, and enjoys better operating leverage than one serving the tail and torso. In my forecast, I have assumed TTD to reach $1B watermark in Operating Income and achieve 23% Operating Margin by 2026E.

TTD’s Growth Benefiting from CTV and Retail Media Networks

In my previous articles, I discussed the future exciting growth trajectories for CTV (CTV Stocks to Invest In) and Retail Media Networks, respectively. There are already strong evidences about how TTD will benefit from its partnership with Disney and Walmart. More to come in my opinion. I think TTD is one of the biggest beneficiaries of the future growth of CTV and Retail Media Networks.

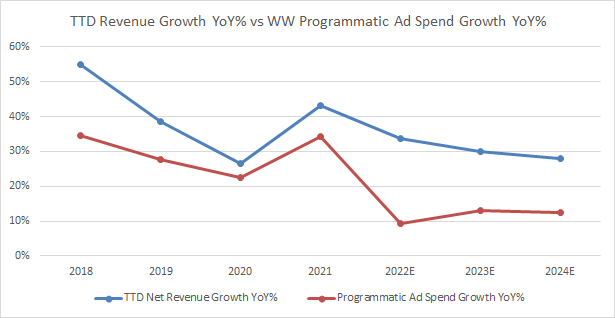

The following figure shows how TTD’s revenue growth is expected to outpace the growth of the Programmatic Ad market.

eMarketer, and TTD financials

Additionally, if you look at the guided growth rates for Q4, it is obvious how much TTD has outperformed relative to other Ad Tech peers.

- The Trade Desk Q4-22 Revenue growth guidance: +24% YoY

- Netflix Q4-22 Revenue growth guidance: +9% YoY

- Meta (META) Q4-22 Revenue growth guidance: +7% YoY

- Snap (SNAP) Q4-22: “Given uncertainties related to the operating environment, we are not providing our expectations for revenue or adjusted EBITDA for the fourth quarter of 2022.”

- Roku (ROKU) Q4-22 Revenue growth guidance: -7.5% YoY

TTD’s Valuation

TTD’s stock price has dropped by half since the beginning of 2022. It’s currently traded at 15x EV/2023 Sales. My valuation based on its intrinsic value is around $70 per share in 12 months. Key assumptions include: 1) a 4-year CAGR of 27% for TTD’s revenue; 2) operating margin increase from 6% in 2022 to 25% in 2026E. At $70 by the end of 2023, its implied 2023 EV/2024 Sales multiple is 12.4x.

Conclusion

One may argue that TTD’s valuation is rich considering its 2022 Operating Margin of $6 and 2022 EPS of $0.2. I think investors should take a longer-term view here: 1) TTD is a unique leading DSP serving the Open Internet, partnering with Streaming and Retail leaders, and operating an advanced DSP platform; 2) TTD may be one of the biggest beneficiaries of the future growth in CTV and Retail Media Networks, and may continue to outpace the market growth; and 3) TTD could achieve better profitability with a bigger scale in next few years.

Be the first to comment