STK steakhouses have a unique “vibe” Cameron Prins/iStock via Getty Images

The ONE Group Hospitality (NASDAQ:STKS) has emerged as one of the very best performing publicly held full service restaurant companies, and one of the least expensive. At the same time it is almost an unknown story, as evidenced the fact that only 1,400 Seeking Alpha subscribers follow it. (At the other end of the spectrum is Starbucks, with 414,000 followers.) Safe to say that that there is lots of room for discovery here.

The Business

As the Company puts it: they are a “global restaurant company that develops and operates upscale and polished casual, high-energy restaurants and lounges and provides hospitality management services for hotels, casinos and other high end venues both in the US and internationally.”

They operate 25 STK steakhouses (their most important expansion vehicle), 25 Kona Grill casual dinner houses, and hospitality services that manage restaurants & food & beverage services within 14 high-end hotels and casinos in the US and Europe. STK is a concept that combines a high energy social atmosphere with the quality and service of a high quality steakhouse. The Kona Grill is a polished casual bar-centric grill that features American favorites, award-winning sushi, and specialty cocktails. As of the Investor Presentation in September, 2022, the average expenditure per guest was $115. and $40., at STK and Kona Grill respectively.

The History

The history is pertinent. STKS came public about ten years ago, when it was merged with a SPAC, the initial price being $5.00 per share The stock languished, trading under $2.00 per share in 2017, as operating performance was uninspired. The company’s fortune turned when Emanuel Hilario (“Manny”) became a member of the Board in April, 2017, appointed President and CEO in October 2017.

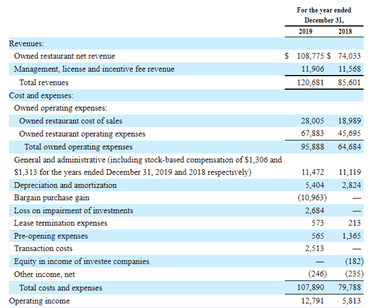

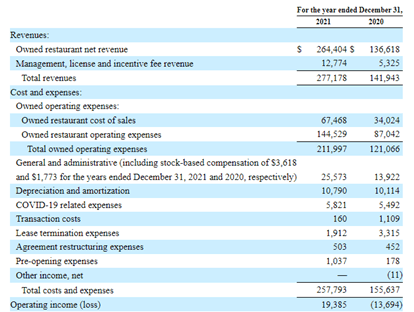

Operating Results 2017 and2016 (Company 10-K) Operating Results 2021 and 2020 (Company 10-K)

Acquisition of Kona Grill

In October 2019, six months before Covid hit, STKS acquired out of Kona Grill’s bankruptcy proceedings 24 domestic restaurants (about half of Kona’s system at its peak), for a contractual price of $25.0 million plus approximately $1.5 million for the apportionment of rent and utilities and approximately $7.7 million in current liabilities at the time. Fast forwarding to the resultant performance, Kona Grill generated about $14.7M of EBITDA for STKS in the twelve months ending September, 2022, generating a handsome return on investment and promising more going forward.

The Company Today

In terms of a financial summary, as of 9/30/22 there were 32.3M shares outstanding, $17M of cash and marketable securities and a modest $28M of long term debt (excluding capitalized leases). With $42M of trailing twelve months (TTM) EBITDA, as of 9/22, the Enterprise Value (after the very recent move to about $8.00/share) become a still 6.4x TTM EBITDA.

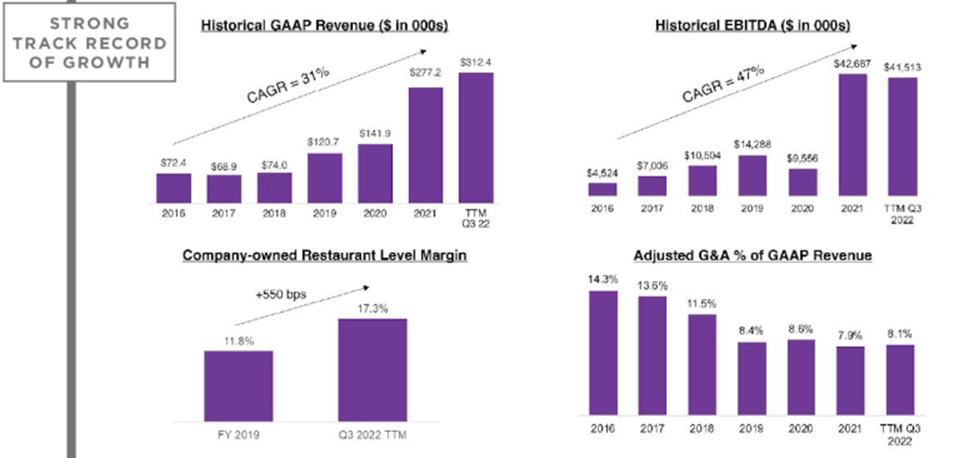

The following charts show the overall progress, consolidating both concepts and the food service management division as well.

Consolidated Results (Company Investor Presentation)

In the restaurant and retailing industries, the most important aspect is “four wall economics”, EBITDA at the store level, and STKS’s two concepts stand out from that respect.

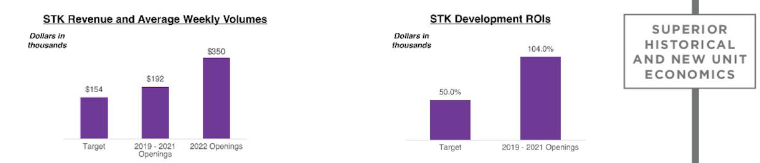

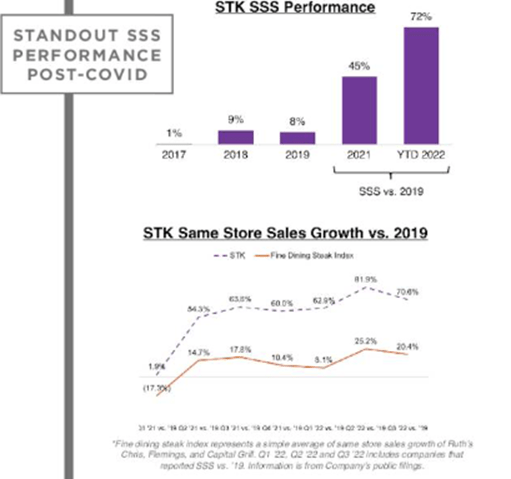

The STK concept, in particular the units opened in 2022, is generating the highest Average Weekly Volumes ($350k/wk) and annual Cash on Cash return (104%) of any publicly held chain that we know of. The dramatically improved same store sales comparisons versus pre-Covid 2019 are especially worthy of note.

STK AUVs and Cash on Cash Return (Investor Presentation) STK Same Store Sales History (Investor Presentation)

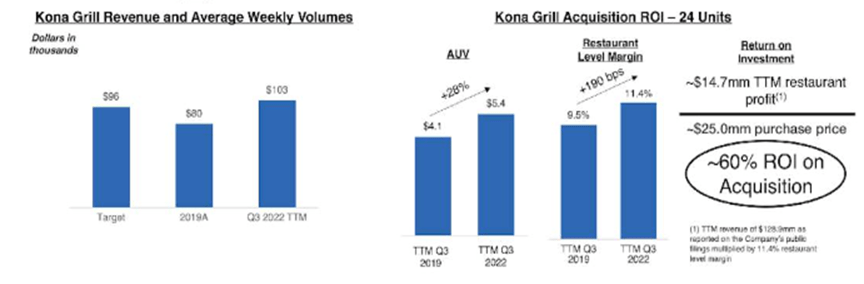

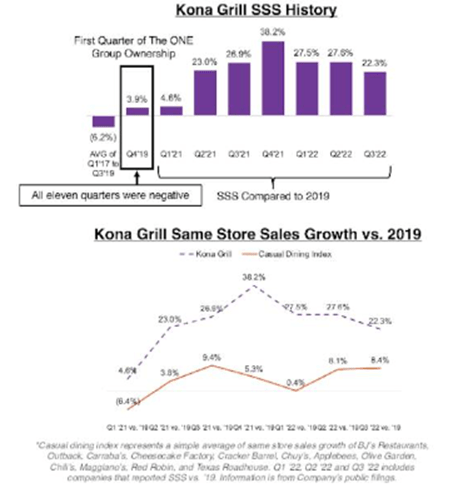

Kona Grill, while the economics take a back seat to the extraordinary returns at STK, is generating unit level returns as good or better than other publicly held chains. The Average Weekly Volume in Q3’22 was $103k, up from $80k in Q3’19, with restaurant level EBITDA margin of 11.4%, up 190 bp from 2019. The charts below show the progress at Kona, impressive on their own, though trailing the STK results as described above. As indicated below, the $14.7M trailing twelve month cash flow from the Kona chain represents about a 60% return against the $25M purchase price.

KONA AUVs and ROI (Investor Presentation) KONA Same Store Sales History (Investor Presentation)

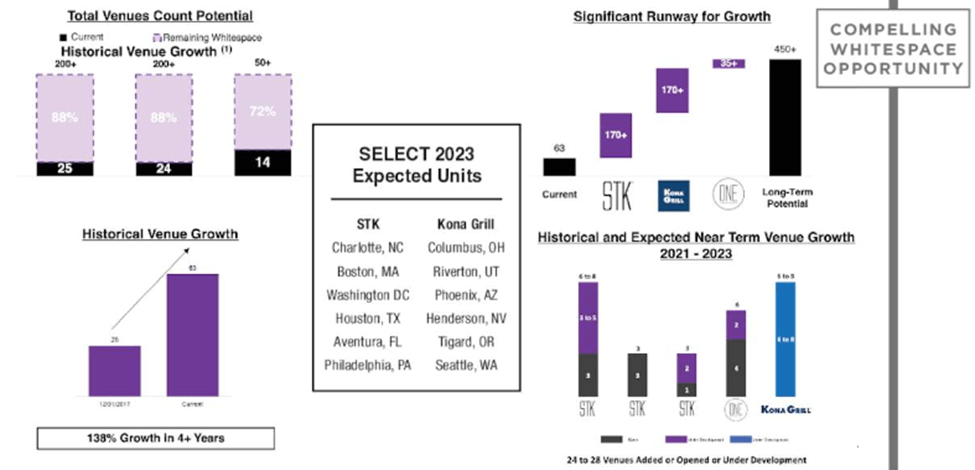

The Expansion Plan

There is lots of room for growth, as indicated in the charts below. A strong balance sheet combined with $42M of cash flow from operations should comfortably support the planned expansion. Six new STK locations alone should add substantially more than $10M of annualized cash flow by the end of calendar ’23. Readers can create their own models, with assumptions of revenues per unit and margins. It is obvious that, with a reasonable degree of success, corporate cash flow can expand by 15-20% annually as far as the eye can see, possibly at a much faster pace.

Expansion Potential (Investor Presentation)

The Balance Sheet and Cash Flow Supports Stock Repurchase

STKS had, as of September ’22, $17.5M of cash, and a modest $24.4M in term loans, against $42M of trailing twelve months EBITDA. They indicated within their Q3’22 report that they had repurchased 500,000 shares for about $7.00 per share in Q3. $6.5M remained on a $10M repurchase authorization as of 9/7/22. On December 14, the Company announced an additional $50M term loan facility, on top of their $25M term loan and $12M revolving credit facility. As announced, this “allows the Company to redeem, repurchase or otherwise acquire its own capital stock, up to $50M subject to a 1.75 Net Leverage Ratio incurrence test.”

Since the 32.3M share total outstanding is worth about $267M at $8.00 per share, $50M would obviously represent a significant percentage of the equity. The demonstrated willingness to purchase stock in the September quarter at about $7.00 per share is a reflection of management’s view of STKS’ current valuation.

Conclusion

The ONE Group Hospitality is selling at one of the most reasonable valuations among publicly held restaurant companies, about 6.4x trailing twelve months corporate EBITDA. While we cannot discount (1) the always present operating risks in the very competitive restaurant industry (2) the macro-economic questions marks that every business faces, compounded here by the highest average ticket among publicly held casual diners: management has demonstrated their ability to manage through the toughest of environments. STK does not need $17M AUVs to generate a very high cash on cash return, and Kona Grill will have generated a handsome return for STKS if it merely maintains its current trends. Management has shown itself to be capable and the corporate balance sheet can support substantial, sustainable growth for the foreseeable future. Nothing happens in a straight line forever, but The ONE Group Hospitality, Inc. should be able to build on its recent impressive performance and STKS should be rewarding over time.

Be the first to comment