bymuratdeniz

Article Thesis

Bulls and bears argue heavily about the outlook for the oil and gas industry over the coming years. In this report, I’ll explain why I believe that the outlook for the foreseeable future is far from bad, and that oil prices will likely remain at a high level for a longer period of time. We’ll also look into some oil and gas equities, as many of those trade at very undemanding prices that price in a considerable decline in oil prices already.

Why Oil Prices Could Be Higher For Longer

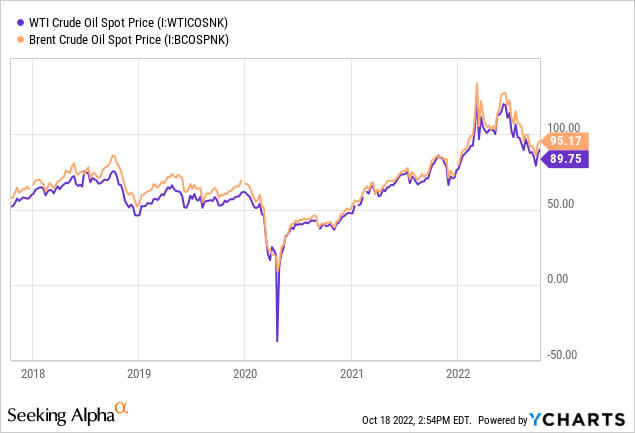

Today, WTI crude is trading at $90 per barrel, while Brent crude is trading for $95 per barrel right now (looking at spot prices). That’s relatively in line with where oil traded at when the Russia-Ukraine war began, as the spike in oil prices we have seen in spring and early summer has faded in the more recent past, due to worries about a recession that could hurt global oil demand.

But even with crude oil trading below the highs from 2022, they are still at an elevated level today, relative to where oil traded over the last couple of years:

These oil prices are still higher than at any point over the last five years, outside of 2022. In other words, crude oil prices are at an elevated level versus where they traded at in the more or less recent future. This includes 2020, when oil prices were very low, but oil is also trading well above pre-pandemic levels today.

I do believe that it is unlikely that oil prices will fall back to $40, $50, or $60 in the foreseeable future, unless there is another black swan event — more on that later. Oil prices could remain at the current level, or potentially even rise above it, due to several reasons.

First, oil demand has recovered strongly and will likely rise to new highs soon. In 2022, oil demand is forecasted to grow by 2 million barrels per day, before growing by another 1.7 million barrels next year. This would lift global oil demand to more than 101 million barrels daily next year. Prior to the pandemic, oil demand did not rise above 100 million barrels per day:

Statista

In other words, oil demand will most likely hit a new record level next year, and forecasts see further demand growth in 2024 and after that, as we can see in the above chart. The pandemic led to a decline in oil consumption, but that was rather short-lived — it did not change the long-term trajectory of global oil demand, as demand keeps growing. The driving factors for that are population growth and rising income and living standards in emerging and developing countries. More and more consumers in these markets buy their first vehicles, more and more people begin to travel via airplanes, consumers shift from heating their homes with wood to oil and gas, and so on. There are some efficiency gains via new technologies, but for many years those gains have not been large enough to offset the factors that lead to growing global demand, and it looks like that trend will remain in place.

Growing demand alone does not necessarily translate into high prices, as it is possible that supply grows as well. That has happened in the past during some time frames, e.g. due to the shale oil boom in the US that led to oil price declines despite the fact that global oil consumption grew. But due to several reasons, supply will likely not grow too much in the foreseeable future.

ESG narratives have led European supermajors such as Shell (SHEL) and BP (BP) to reduce their exploration spending, for example. Their oil output will likely decline slightly going forward. Other oil companies have felt pressure from ESG funds as well and will likely not pursue a lot of production growth, or potentially none at all. Even non-ESG-driven investors are not too interested in a lot of production growth. Instead, investors have become more focused on free cash flows, which has also had an impact on how company boards and management teams think about capital budgets. Many are happy with keeping production levels stable while generating strong free cash flows that can be used for dividends, buybacks, and debt reduction. The growth-at-all-costs mindset was very common especially among shale oil players before the pandemic, but that is no longer the case.

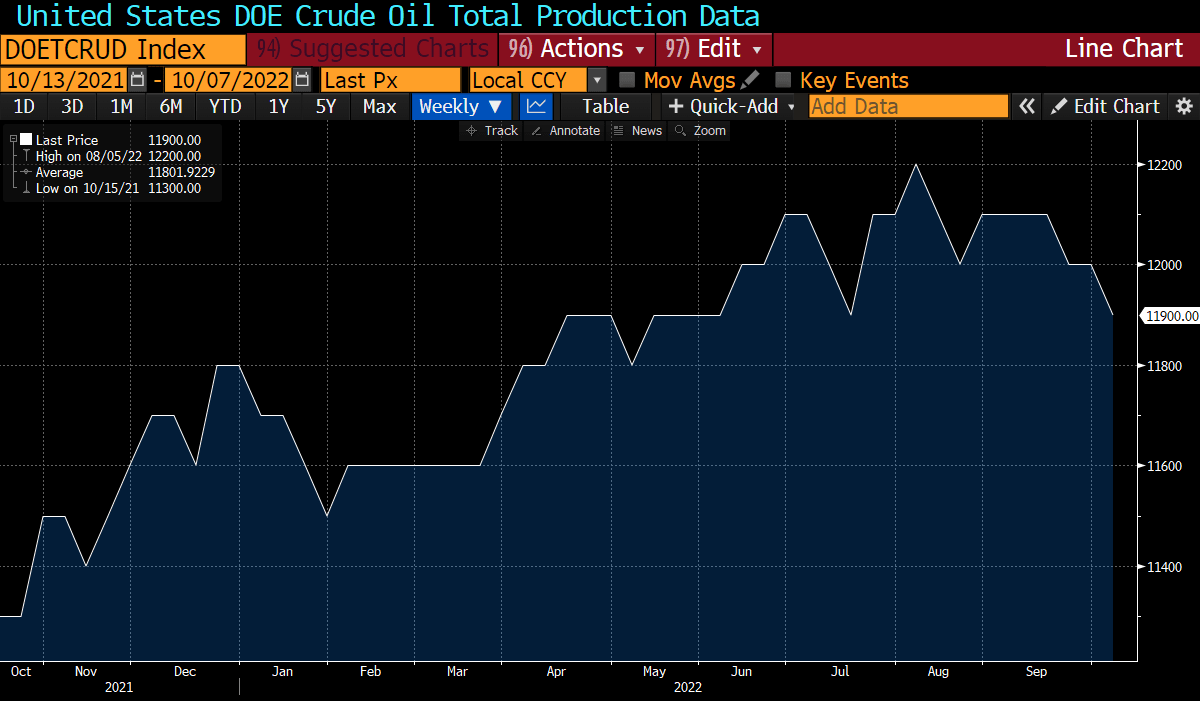

On top of that, even if companies wanted to grow their production meaningfully, it wouldn’t be easy. Regulatory pressures, such as fewer permits and harsher environmental standards, lead to headwinds for oil production growth. There are also shortages for all kinds of material, and even when it comes to employees — some have left the industry for good during the pandemic slump, and not too many young people want to get into this industry, which is why oil companies have a hard time replacing retiring employees. With shortages across employees, frack sands, machinery, and so on, it will be hard for oil companies to grow their output at all. The following chart shows that US crude oil production has not grown in recent months — it has actually declined:

Bloomberg

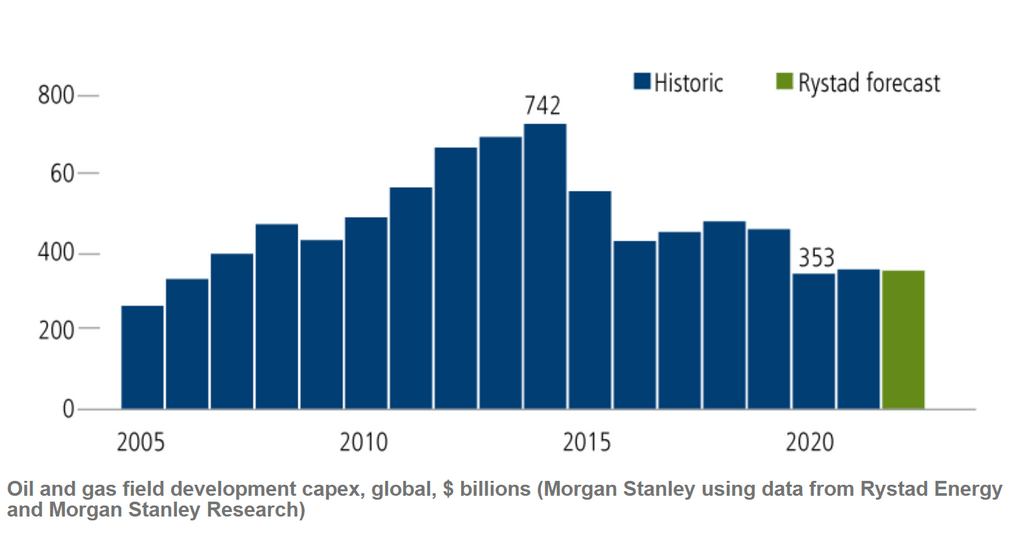

Investors should also consider the lag time between new project approvals and the point in time when these projects start to produce oil. Major projects take several years to finish, thus even if oil companies were to ramp up their capital budgets massively in the near term, it would take years for that additional supply to come to the market. Oil and gas companies have been underinvesting in new production for years, especially during the midst of the pandemic when oil prices slumped to a multi-year low. The following chart shows the huge gap between actual spending and what would be required to keep up with demand:

Rystad

Oil demand is hitting new record highs, and yet, capital spending is at roughly half the previous peak from 2014. In the meantime, almost everything became more expensive, from materials to equipment, fuel expenses, and so on. In real terms, the spending cut has thus been even more drastic, which makes it even less likely that the global oil and gas industry will deliver any significant growth in production in the near term — after all, spending levels were around twice as high as they are today when the company last managed to grow production at a sizeable pace, which was prior to the 2015 oil price crash.

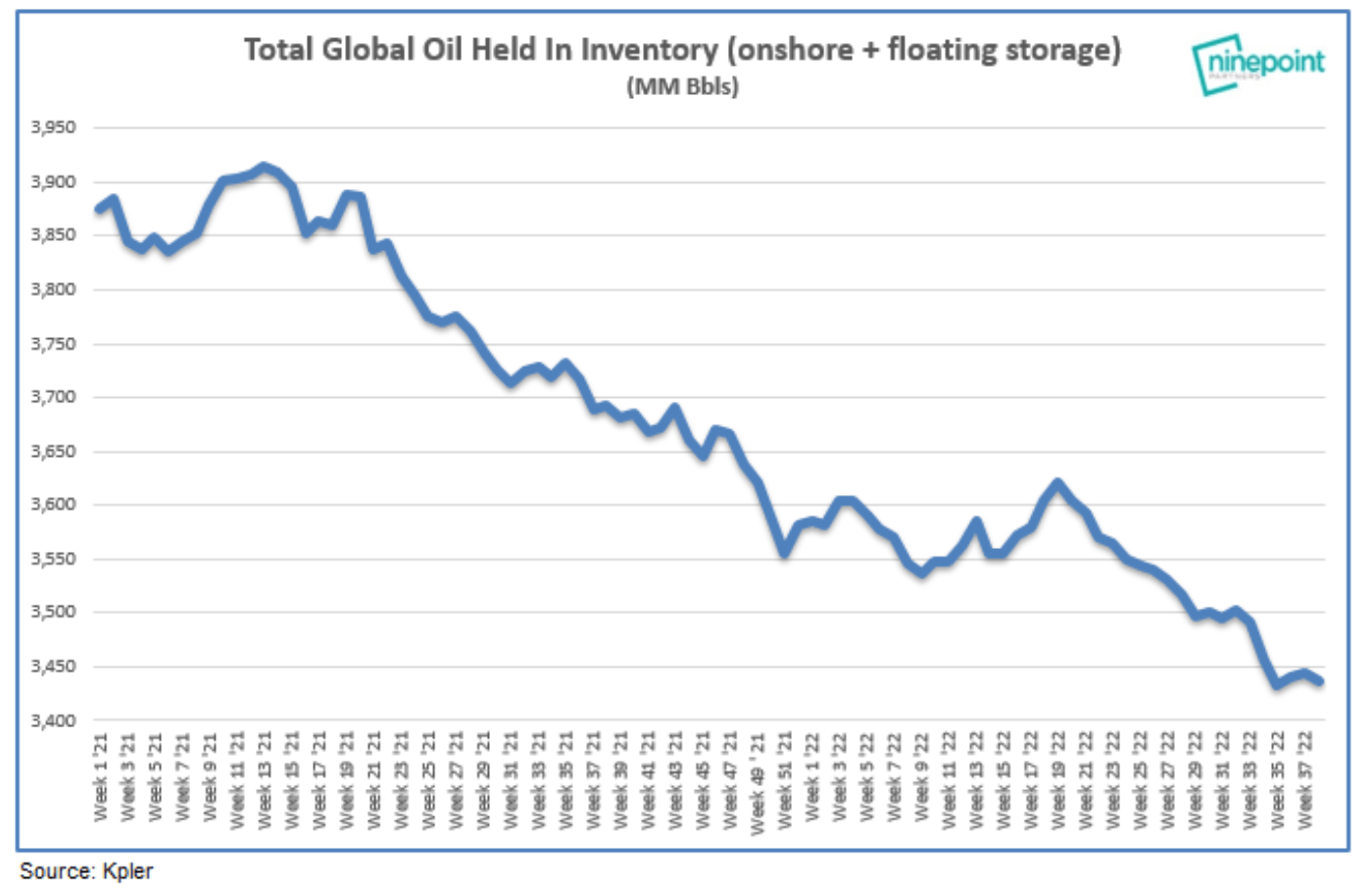

There are other reasons to believe that oil prices will remain high going forward. Oil inventory levels are pretty low, for example:

Ninepoint

Even more important, they continue to fall, suggesting that markets are not in balance right now. Instead, the market is undersupplied, which is why inventories have to be drawn down in order to meet demand. And that is before the forecasted demand growth in 2023, that will be driven by the ongoing recovery from the pandemic, e.g. when it comes to airline travel.

Also, OPEC has recently been flexing its muscles recently. The cartel is very powerful in the current global energy crisis, and it’s willing to capitalize on that by keeping oil prices high via production cuts. I do believe that the cartel would be willing to cut production further in case oil prices were to decline, thereby offering additional downside protection.

Investors should also consider that Russian oil production is forecasted to decline going forward, as sanctions prevent the country from receiving needed equipment and spare parts. The lockdowns in China are also a potential upside catalyst — when they end, global demand should increase further, thereby tightening the already tight supply-demand picture even more.

Risks For Oil Prices

Of course, there are also some potential risks to consider for oil prices. If a new especially dangerous variant of COVID were to emerge, new lockdowns could be put in place, which would result in lower oil demand. But in the recent past, there was a clear trend of easing measures around the world, so I do not see this as very likely.

An Iran deal also could hurt oil prices, as it potentially would bring new supply to the market. But due to the recent deadly protests in Iran, it seems unlikely to me that Western nations will be interested in a deal.

Oil Equities Are Cheap And Promise Compelling Returns

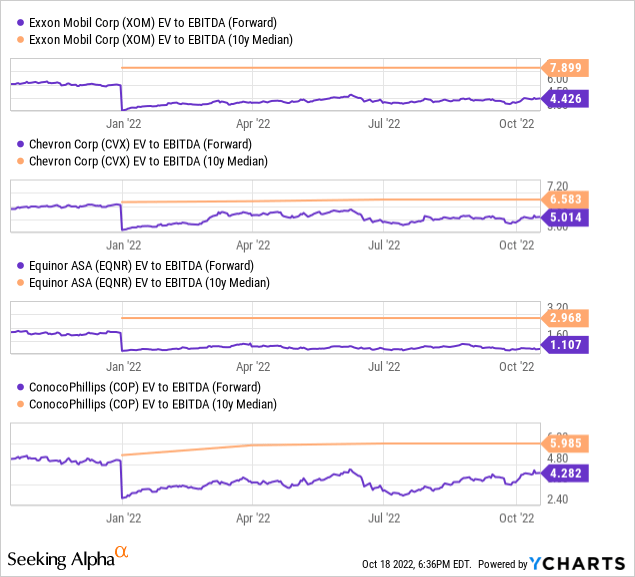

With the aforementioned reasons indicating that oil prices could remain high for quite some time, oil equities should benefit from the macro environment. At the same time, many oil equities are quite inexpensive. This includes, for example, the major international oil companies such as Exxon Mobil (XOM), Chevron (CVX), Equinor (EQNR), or ConocoPhillips (COP):

All of these companies trade at least 30% below their long-term average valuations right now, while their EV/EBITDA multiples are also inexpensive to very low in absolute terms. With them offering solid dividend yields and benefitting from high oil prices, meaningful multiple expansion seems possible over time.

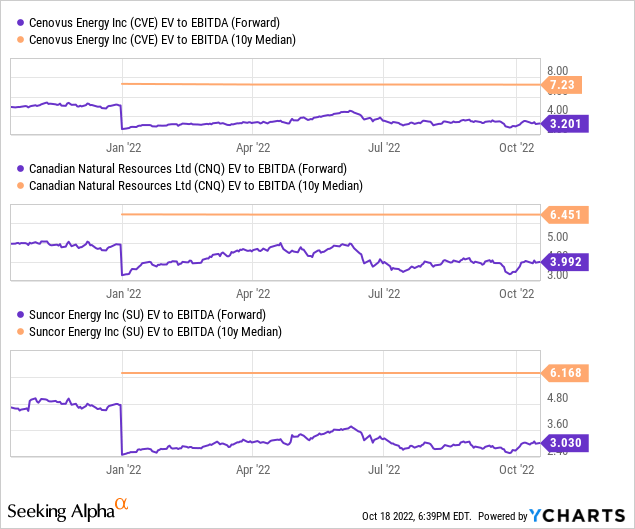

Canadian oil sands companies also look attractive in many cases, as they combine low decline rates, low break-even costs, and high free cash flow yields:

These companies trade at 3x to 4x EBITDA, while their long-term average valuations are more than 50% higher than that. They can pay down debt, buy back shares cheaply, while also offering solid dividend yields on top of that. Over time, this will force multiple expansion, I believe, which is why their total return potential is attractive.

Shale oil players have higher decline rates generally, but their low valuations still could allow for considerable upside potential, especially when paired with high shareholder returns via either buybacks (such as Marathon Oil (MRO)) or dividends, as offered by Devon (DVN) and others.

ETFs offer broad-based exposure for those that do not want to invest in individual picks. The Energy Select Sector SPDR ETF (NYSEARCA:XLE) is an obvious choice for those looking for ETF exposure to energy names — it contains the major energy companies, such as XOM and CVX, and has a very low expense ratio of just 0.11%. It currently yields 3.8%, and that yield should continue to rise as many energy companies will be increasing their shareholder returns, including dividends, in the coming quarters as their balance sheets get stronger and stronger thanks to hefty profits and cash flows. XLE also includes some non-energy companies that are related to the industry, such as Schlumberger (SLB), which could benefit from growing demand for its services in a high oil price environment.

Takeaway

Not too long ago, some people were pretty sure that oil and gas would be cheap forever, as the pandemic had temporarily reduced demand. But we see now that this is not the case — demand is growing to new all-time highs, while supply is constrained due to too-low capital spending, ESG mandates, increasing regulation, and so on.

Add OPEC being willing to cut spending to the mix, and it looks like oil prices could remain high for a long period of time. Many oil equities are not pricing in oil at $80, $90, or higher. I believe that many of these stocks could provide attractive returns going forward, especially those with a strong shareholder return framework and management teams skilled in capital allocation.

Be the first to comment