PPAMPicture

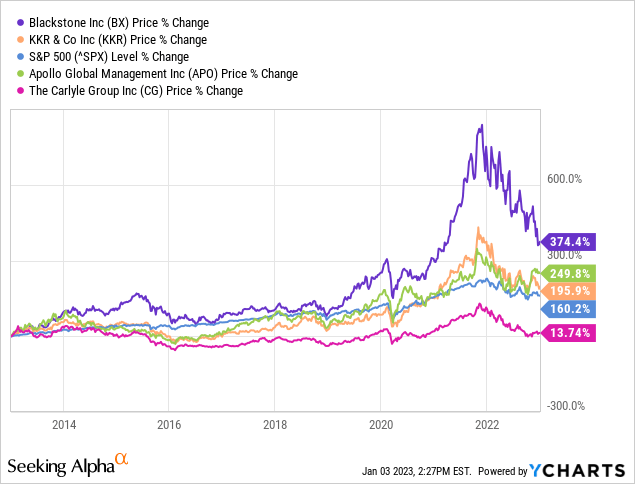

Private Equity (PE) has long had a track record as a highly disputed alternative asset class, even before the financial crisis in 2008. However, while private equity stocks, including KKR (KKR), Carlyle (CG), and Apollo (APO), have underperformed the broader markets in large parts of the 2010s (excluding Blackstone), they have massively appreciated on the value on the back of the pandemic and the favorable financing and exit environments. While the public has long questioned both the used measures and the fee structure of private equity funds, criticism of the industry has recently exuberated with Blackstone’s BREIT limiting investors’ withdrawals to 2% per month (of NAV). While I am not the right person to question the practices of PE firms, I will elaborate on the last point, whether the broader market of private equity stocks is worth investing in. This market analysis takes a closer look at the state of the private equity market and provides an outlook for the market. It presents the first article of a series on private equity that will be published over the next week.

The case for private equity

Private equity can be a compelling investment opportunity for those looking to participate in the growth of successful companies. Here are some reasons why private equity stocks may be a good investment:

- Strong track record of returns: Private equity firms have a history of delivering strong returns to their investors. These firms are experts at identifying undervalued assets and driving operational improvements in the companies they invest in, which can lead to value creation and strong returns. From 2000 until now, private equity allocations by state pensions produced an 11.0% net-of-fee annualized return, which compares to the S&P 500’s return of just 6.29% over the same time. This does not translate directly into shareholder return, as shall be explained later. However, it weakens claims concerning inconsistencies of above-average returns over a long-term horizon.

- Active management approach: Private equity firms often take a dynamic management approach to their investments, bringing in new management, implementing cost-cutting measures, and developing new strategies to drive growth. This can drive value creation and generate solid returns for investors.

- Access to debt financing: Private equity firms often have access to debt financing, which can be used to leverage their investments and increase returns.

- Diversification benefits: Private equity can provide diversification benefits to an investment portfolio, as it is not correlated with the stock market. This means private equity investments can hedge against market volatility.

The BREIT controversy

The ‘Roar’ was big when Blackstone (BX) announced at the beginning of December that it would limit withdrawals to one of its flagship funds BREIT as contractually agreed upon by its limited partners. While the signaling of such an announcement is undoubtedly bad, the overreaction of a more than 20% drop in Blackstone’s stock was more than unjustified in my opinion.

BREIT Performance (Blackstone Investor Presentation)

There are two main reasons why I sense the sell-off on the back of the news is unjustified:

Fire-Sale Myth

However, looking closely, the imposed withdrawal limit is a reaction to what happened in the financial crisis when banks and PE funds cascaded due to fire-sale spirals. First, plenty of people argued that the withdrawals were to lead to a fire-sale of its property assets, marking a downward spiral that, once it gets going, is hard to stop. Second, the withdrawals in October and November amounted to just $3 billion, which compared to the $11 billion in cash are still small amounts.

Foreign Investors

Some 70% of the withdrawals can be linked back to foreign, primarily Asian investors, whose share of contributions of the fund makes up roughly 20%. Therefore, claims concerning a general loss of confidence in the fund appear farfetched, as most limited partners remain confident or even extend contributions, as is the case for the University of California, which recently invested $4 billion in the fund that popular opinion labeled as a potential Kickstarter of a new financial crisis.

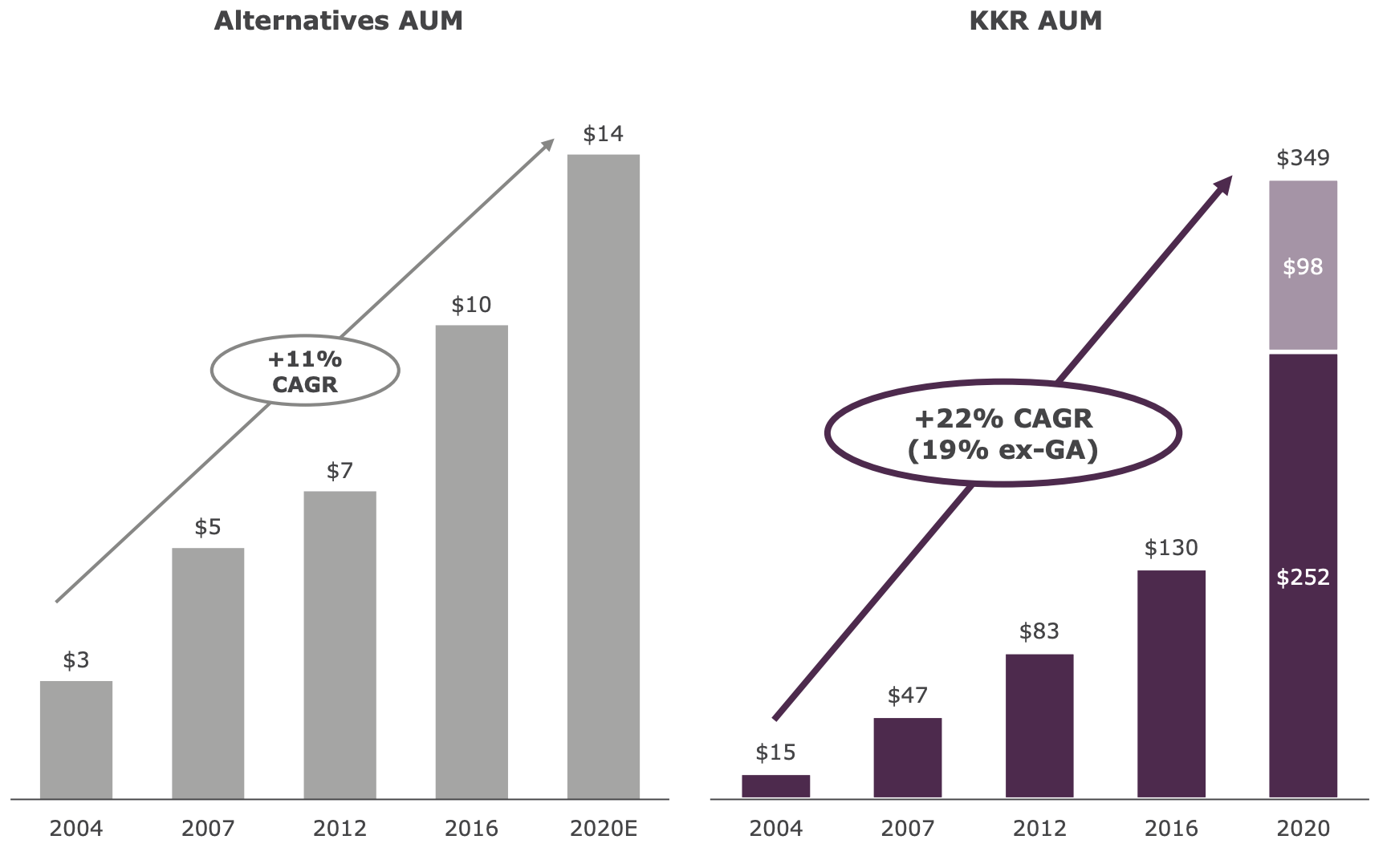

AUM Growth (KKR AUM) (KKR Investor Presentation)

The next Golden Age of Private Equity

Assets under management (AUM) have significantly risen throughout the last two years, which saw significant price increases in private equity stocks. This generated a lot of so-called distributable income for investors through the 2/20 rule in private equity classes. 2% of AUM are management fees, and the other 20% are performance fees, which bring in the bulk of income for successful funds, at least in attractive market environments. If you were to conduct a DCF analysis based on income over the last quarter, you would think I am out of my mind. However, people forget that a huge chunk of assets for PE funds is liquid, as it was raised in 2021 under excellent market conditions, but most funds still need to be deployed. Hence there is a lot of so-called ‘dry powder’ available for funds to invest at 20-30% lower valuations. This will allow funds to invest in 2023 and 2024 at lower valuations that might drop further in a likely recession scenario and then sell when markets recover and overall IPO sentiment lightens again. Therefore, the investor who patiently waits 5-10 years to see this investment cycle pan out will reap hefty rewards once market sentiment lightens. In the meantime, lower valuations should be taken advantage of, bearing in mind that valuations could drop further in line with economic sentiment. It makes sense to dollar-average over the next 12-18 months.

Risks

Private equity firms are subject to various regulatory risks, which can impact their operations and financial performance. One regulatory risk that private equity firms face is the possibility of increased scrutiny or regulation by government agencies. For example, private equity firms may be subject to increased scrutiny by regulatory bodies in the wake of a financial crisis or other economic events, which could lead to increased costs and burdens on their operations.

Private equity firms may also face regulatory risks related to the industries in which they invest. For example, a company that is the target of an acquisition by a private equity firm may be subject to regulatory approval, which can be a lengthy and uncertain process. Additionally, private equity firms may face regulatory risks related to the financing of their investments, as they often rely on debt financing, which is subject to regulatory oversight.

Overall, regulatory risks can pose significant challenges to private equity firms, and investors should carefully consider these risks when evaluating potential investments in the personal equity space.

Conclusion & Outlook

Private equity stocks can be an attractive investment opportunity for those looking to participate in the growth of successful companies. Private equity firms have a history of delivering solid returns to their investors through their ability to identify undervalued assets and drive operational improvements in the companies they invest in. Additionally, the private equity industry has benefited from solid service demand and a shift in investor sentiment toward alternative investments.

However, private equity investing carries certain risks, including the potential for the companies in which private equity firms invest to underperform or fail, the risk of overpaying for assets, and the use of leverage, which can increase the risk of financial distress for the companies they invest in. Private equity firms are also subject to regulatory risks, which can impact their operations and financial performance.

Overall, the outlook for private equity stocks is generally positive, with strong demand for personal equity services and a favorable economic environment expected to drive continued growth in the industry. However, it’s essential for investors to carefully evaluate the risks and potential rewards of any investment before making a decision.

Be the first to comment