ljubaphoto/E+ via Getty Images

Headquartered in Scottsdale, Arizona, The Joint Chiropractic (NASDAQ:JYNT) is a revolutionary chain that offers affordable, accessible, and approachable non-acute Chiropractic treatment. Over the past decade, JYNT has experienced explosive growth and built strong brand recognition. Although the stock price has declined significantly (85% down from an all-time high), I think JYNT’s growth is far from over. For long-term investors who value patient-centered care, JYNT may offer significant value.

Quarter updates:

Last quarter, JYNT continues to grow. System-wide sales increased to 110M, up 18%. The comp sales for clinics opened 13 months or more continue to grow at a rate of 6%. Total revenue grew 27% to 26.6M with Company- owned or managed clinic revenue increasing 36% and contributing $15.8 million. Franchise operations increased 15%, contributing $10.8 million. More potential growth could be realized as their price increase plan only applied to 50% of their members yet. Future price increases should be implemented for the other 50%.

Regarding profitability, JYNT continues its high level of gross margins. Since 2012, JYNT has improved its gross margin rate from 60% to 90.64% in the last quarter. This is really amazing. Operational margin suffered from higher growth (23%) of selling and marketing expenses. G&A costs increased by 41% to support total clinics and revenue growth in the tight labor market.

Given the tough macro environment, I think JYNT showed the resilience of its business model. The market also seems satisfied with the 2022 Q3 performance as the stock price jumped after its earnings release.

JYNT offers profitable growth

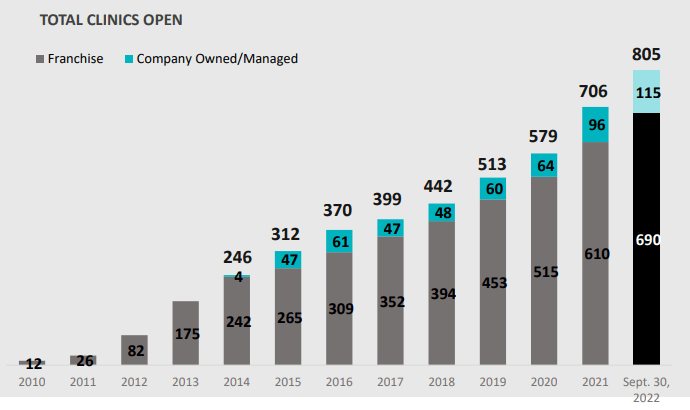

JYNT has delivered tremendous growth since its inception with 805 clinics opened In 2022 Q3. As a consumer-facing service, this is a really positive sign since great brands often go viral in the beginning. JYNT is already in the top 2% of franchisors in the US. This is a significant achievement considering the company only started in 2010. The closure rate is less than 1% annually which is very low in the franchise community. Currently, JYNT has 690 franchise clinics paying franchise fees, and 115 company-owned or managed clinics (14% of total clinics) that directly collect sales. With a cumulative 1176 franchise licenses sold (252 in active development), it is highly likely that JYNT will open more clinics in the future.

JYNT clinics growth (JYNT presentations)

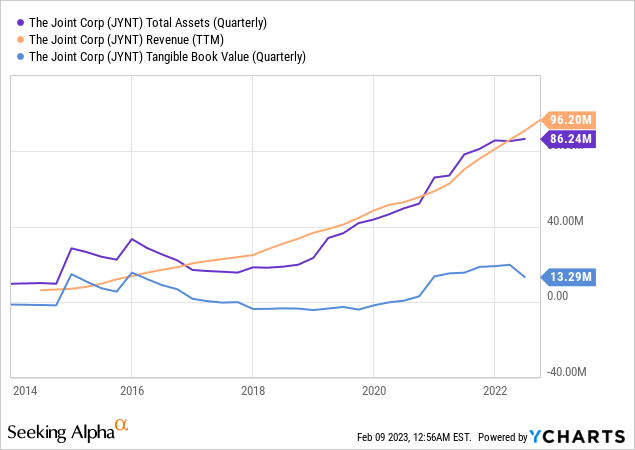

Consequently, JYNT saw a tremendous increase in its revenue, going from $2 million in 2012 to a staggering $96.2 million TTM in the current year, with an impressive Compound Annual Growth Rate [CAGR] of 47%. Despite being a traditional brick-and-mortar business, this is a remarkable accomplishment. During this time frame, the number of outstanding shares grew by just 173%, while long-term debt remained low at 2 million, demonstrating JYNT’s ability to achieve organic growth and minimize capital requirements. As the chart below, JYNT’s revenue growth outpaces the increase in total assets, while the tangible book value remains modest. These figures illustrate JYNT’s impressive capacity for organic growth and low capital requirement.

The JYNT Competitive advantage

I think JYNT has a very compelling unit of economics. The Chiropractic services JYNT offers are non-acute treatment which doesn’t focus on severe injuries. No expensive and invasive diagnostic tools such as MRIs and X-rays are needed for JYNT clinics. This significantly lowered fixed operational costs and improved per-clinic profitability. Each clinic opening requires only a 300K investment and could break even at 27K to 30K monthly sales. The typical cash-on-cash return is 3.5 years. According to the management, the 4-wall EBITDA margin of each clinic has been 30+% on average and is expected to continue in the future.

The business simplicity leads to 48% lower cost than the industry average. Most of the clinics locate near grocery centers and no appointments are needed. No insurance is needed for a patient to receive care. As a result, JYNT has 347 patients per week vs 112 from traditional Chiropractic providers. With more convenience, more value, and simpler service, I do think JYNT’s model is superior to many others.

The market position and growth space

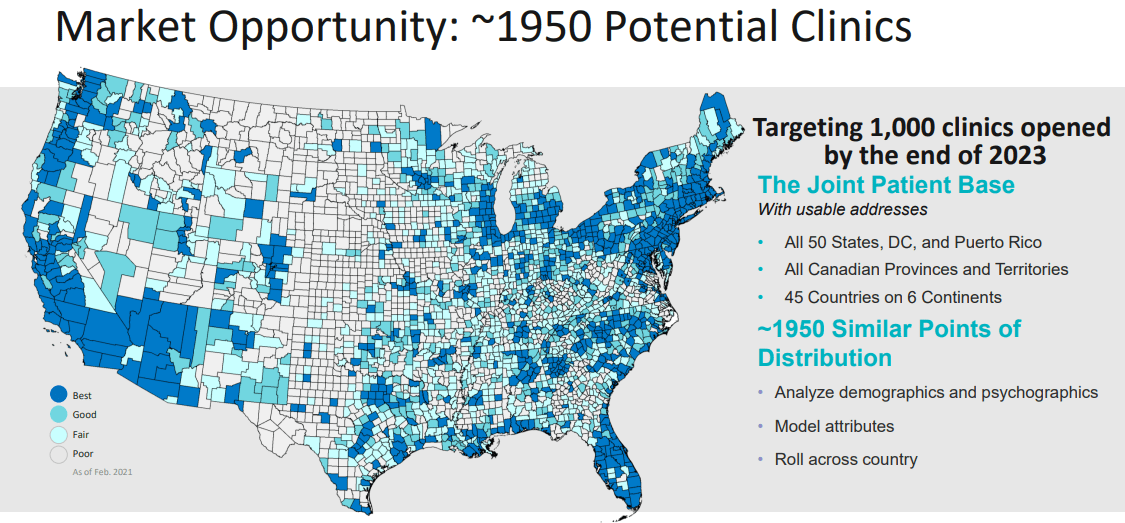

JYNT is currently the clear number 1 in the chiropractic market. The next competitor franchise brand with the non-insurance model is Nuspine which only has 19 stores. This is a very fragmented industry. JYNT’s market share is 2% while other chain brands combined only have 2% too. 96% of the market is made of independents. JYNT has a huge runway ahead as the 2022 IBES World report noted that the chiropractic market equals 19.5 billion. The management aims to continue its geographical expansion to 1950 clinics (1.2k license already sold) based on demographic distributions. Given average clinic generates around 500k sales right now, 1950 clinics could mean 950M system-wide sales. Assuming JYNT keeps the same system take rate right now, a short-term future revenue of 228M is totally achievable.

JYNT market opportunity (JYNT presentation)

Risk and concern for the future slowdown

Historically, JYNT can expand its market demand very fast as 36% of the patients have never tried Chiropractic care. Its marketing technology, media channels, and consumer engagement campaigns (such as messages) make it more effective for attracting new patients than single practitioners and other small competitors.

However, JYNT’s new patient per clinic decreased for the first time in Q3 2022 which may signify a slowdown in momentum. The management listed two possible reasons for this: 1. Google’s algorithm change affected JYNT’s organic search traffic. 2. inflation lowered consumers’ willingness to pay for discretionary spending as JYNT’s patient base is just 36.4 years old. It is understandable that there are fewer new patients as no one can avoid the effects of current macroeconomic challenges. However, the chiropractic field has encountered numerous skepticisms as scientific studies only exhibit limited advantages from the treatment. There are some who question the validity of it being considered a legitimate form of treatment. As an unconventional care type, you always encounter uncertainties.

Bottom Line

As our lifestyle is more sedentary, Americans will likely face more physical health issues such as obesity, back pain, etc. JYNT is in a great position to develop a large franchise brand in the healthcare space which is essential to lots of people. It has already established a strong foothold in the market in a relatively short time. The management understands the business and runs the company very efficiently. I think the future of JYNT is very bright and investors have lots of opportunities to gain a decent return.

Be the first to comment