Luis Alvarez

Through continued revenue growth combined with expense controls, we are committed to reaching cash flow neutrality from our operations in calendar year 2023

The above statement was made by CEO Lyron Bentovim on the Glimpse Group’s (NASDAQ:VRAR) Q1 earnings call on the 14th of November. Maydan Rothblum, CFO and COO of Glimpse then further underlined their determination to achieve this goal.

And again, as Lyron stated, getting to cash flow breakeven and beyond from operations in the calendar year 2023 is a key strategic objective.

This is quite the statement. The VR/AR industry is in its early innings – Glimpse achieving cash flow neutrality whilst simultaneously achieving strong growth would be impressive.

I believe that if Glimpse can achieve this target and grow at a fast clip, there is further upside to the stock in 2023. Nonetheless, investors buying Glimpse shares should do so with a long-term view, it’s very hard to call near-term market moves.

In this article, I will take a look at what makes Glimpse unique in the VR/AR space, how the company’s contingent considerations are structured, what to expect in Q2 and the risks that face the software services firm.

A bet on Glimpse’s subsidiaries is well… a bet on Glimpse

Investors who are buying Glimpse shares are buying into management. Whilst this is the case for most micro caps, it is particularly true for Glimpse.

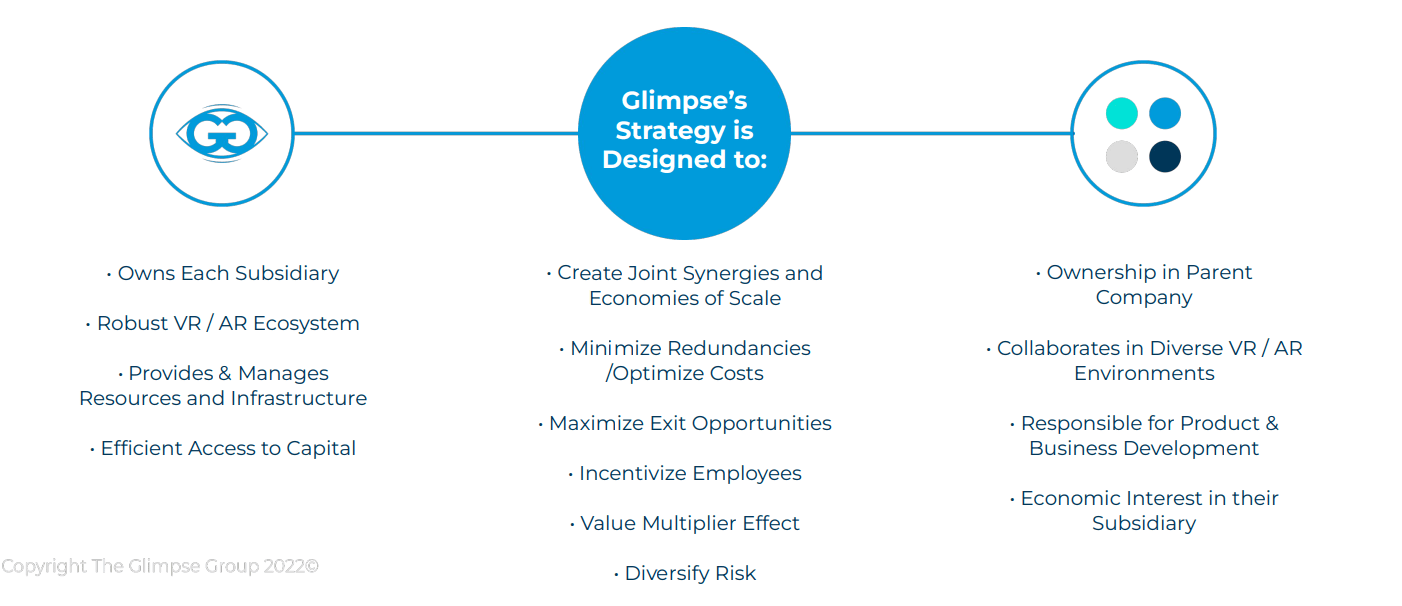

Glimpse’s strategy is to build a VR/AR ecosystem, that’s been the purpose since its inception and the public listing allowed them to accelerate toward the goal of becoming the premier software services provider.

Glimpse benefitted from the large run-up in its stock price back in late 2021, this allowed management to offer 1.5M shares at $10 (100% higher than today’s price, mind), bolstering the balance sheet and helping to fund the acquisitions of both Sector 5 Digital and Brightline Interactive in December ’21 and May of last year. Whilst frustrating for those who bought in the high teens, those assessing Glimpse today can view this as a shrewd move.

Glimpse isn’t acquiring these companies to hold them as standalone businesses – the aim is to generate go-to-market synergies, build expertise and provide resources.

Glimpse Investor presentation

This strategy has merit in consideration of the VR/AR environment. The VR/AR space is fragmented. There are a lot of new start-ups entering the space which will intensify competition in the future but a lot of the competition on the software side, are small in size. That’s why when Glimpse completed the acquisition of Brightline, they noted that they are now one of the largest software services providers. In an industry with a global market size of $25.3B (~$16B of that being Glimpse’s focus market), this is quite unusual. It’s therefore unsurprising to see why management wanted to go public and raise funds – it’s allowing them to try and obtain scale where it doesn’t really exist.

It’s the management’s job to successfully integrate these businesses into Glimpse and then scale the whole ecosystem. You are betting on their ability to attract and retain tier 1 customers and capture the significant growth that many perceive is coming for VR/AR.

A heavily invested and well-aligned management team

Considering that a bet on Glimpse is a bet on management, ensuring incentivization and alignment of leadership to shareholders is important. A major positive is that both founders and Maydan Rothblum are all heavily invested in Glimpse. Below I have tabled the holdings of those three (Bentovim, Rothblum and Smith) along with the other directors.

| Director | Shares owned | % of shares outstanding |

| Lyron Bentovim | 1,039,170 | 7.6% |

| Maydan Rothblum | 481,414 | 3.4% |

| David John Smith | 1,002,550 | 7.2% |

| Amen Lemuel | 100,000 | 0.72% |

| Jeffrey Enslin | 3,000 | 0.0021% |

| Jeffrey Meisner | 84,000 | 0.6% |

Cash flow neutrality target

So can this cash flow neutrality target be achieved? Well, the simple answer is yes. As management has noted, the company’s cost structure is highly variable, making it a lot easier to adjust expenditures quickly. The bigger question is about the potential implication this could have on growth for FY23. There was a lot of confidence from management on the conference call to that end:

As we’re looking in 2023, I think we can get to a scale position where we can cash flow self-sustain, meaning that we will have enough – generate enough cash flow from operations to sustain R&D investments

Essentially leadership thinks they can achieve cash flow neutrality through scale – potentially alluding to further growth. As mentioned by Bentovim in the above quote, the significance is that they are going to be able to continue to invest in R&D. Remember the company is targeting cash flow neutrality, not profitability – the company will still likely experience losses in the future due to non-cash charges like amortization related to intangibles.

Contingent considerations

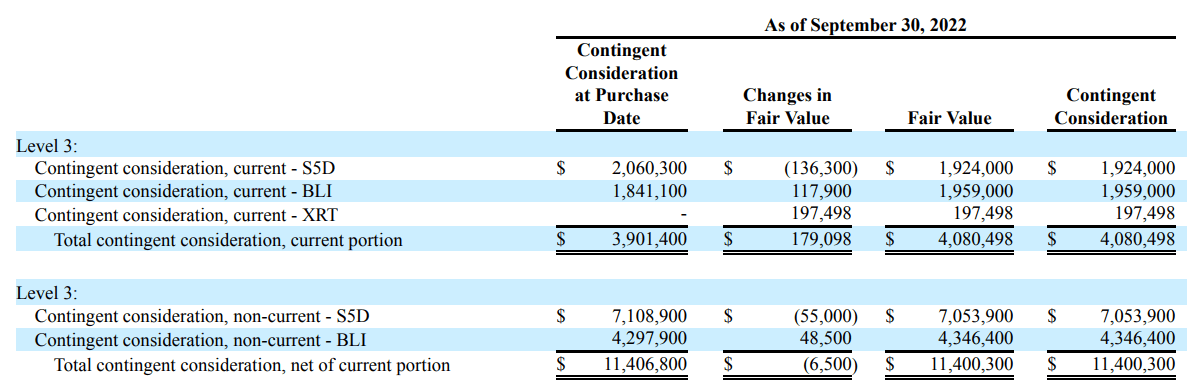

Because Glimpse is an acquirer, they have built up a lot of Goodwill on their balance sheet. Under accounting standards, goodwill cannot be internally generated and can therefore only be recorded from business combinations.

Considering Glimpse’s strategy, a big component of the company’s future obligations will come from contingent considerations (otherwise debt free). Finding the fair value of contingent considerations when assessing goodwill to be capitalized as an intangible asset is known to be quite a grey area in accounting and requires a fair degree of judgment. The Glimpse Group used the Monte Carlo method to calculate this.

The contingent considerations are based on S5D, Brightline and XR Terra achieving ‘significant’ revenue milestones. Glimpse doesn’t disclose what they are specifically, but we can look at the current/non-current liability breakdown in the 10-Q to see what obligations may arise over the next 12 months:

Glimpse 10-Q

Glimpse estimates that $4.08M of the contingent consideration will arise within the next 12 months. For both S5D and Brightline half of the total future considerations are made up in stock with a $7 floor issuance price and half in cash. The breakdown of the current portion of contingent consideration isn’t disclosed, so it’s difficult to know how much of this current portion will eat into cash reserves.

Considering the uncertain backdrop and a cash balance of $11M, it makes sense to pursue cash flow neutrality. Glimpse still has a large cash buffer even if the entire current portion of contingent considerations were cash-based, but with a great deal of macro uncertainty, it’s better to be safe than sorry. Besides, it’s not exactly disappointing if these contingent considerations are realized because it means that these subsidiaries are likely contributing to revenue growth.

Expectations and valuation

There aren’t any direct publicly listed competitors to Glimpse, which makes valuation comparisons difficult. Glimpse’s revenue run rate after accounting for the substantial recent acquisitions is ~$16M. Glimpse produced $3.8M in revenue for Q1 ’23 and the market expects revenue to be $18.2M for the FY, so an average of $4.8M for the next three quarters, with Glimpse achieving an extra $2.2M in additional growth vs run rate. The backdrop is uncertain and Glimpse may lose certain contracts but considering recently secured ones by S5D this seems conservative to me.

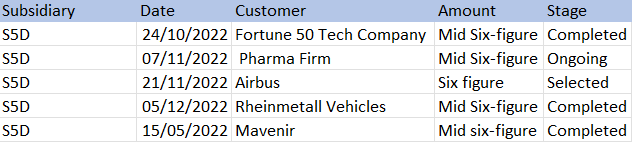

These contracts may lead to Glimpse exceeding financial estimates, I have tabled the contracts announced during Q4 below.

Glimpse announced contracts in Q2 (Glimpse Press Releases)

As shown above, all recently announced contracts relate to recently acquired Sector 5 Digital (S5D). Assuming the ‘mid-six figure’ contracts equate to roughly $500k each, the (announced) completed contracts may contribute ~$1.5M in revenue alone in Q2. Historically the majority of Glimpse’s revenues are recorded ‘at a point in time’, which means when a contract is completed and the customer takes control of a project, so these contracts could relate entirely to Q2.

These are only the publicly announced contracts, for reference in Q1 Glimpse didn’t produce any press releases for new contracts and achieved $4m in revenues.

Due to lack of disclosures from Glimpse for competitive reasons, we are limited on available information from previous quarters to be able to predict Q2 revenues but I think the recent contract wins combined with Glimpse’s existing strong relationships with the likes of Snap Inc. (SNAP) (through subsidiary Qreal) make for a positive quarter with further short term progress. Revenues around the $4.8m would be positive as analysts likely expect greater revenues in the back half of ’23.

if Glimpse hits estimates for the FY23, it would be trading on a EV/sales ratio of 3.5x, considering the expected growth in the industry and if Glimpse achieves cash flow neutrality I consider this to be quite cheap. As a barometer other formerly deemed ‘metaverse stocks’ like Vuzix trades on 15x EV/sales. Considering how early-stage Glimpse and this industry is I believe EV/Sales is a fair metric, but it does also reflect the highly speculative nature of this company and this industry. More common metrics such as P/E, EV/EBITDA, FCF, ROIC are all unsuitable as Glimpse isn’t profitable and is focused on reinvesting into R&D.

Risks

Glimpse management has stood steadfast by its seven-dollar floor issuance price, so the current risk of further dilution is low. Any further dilution would come from entirely share-based acquisitions, but these should incorporate that seven-dollar floor.

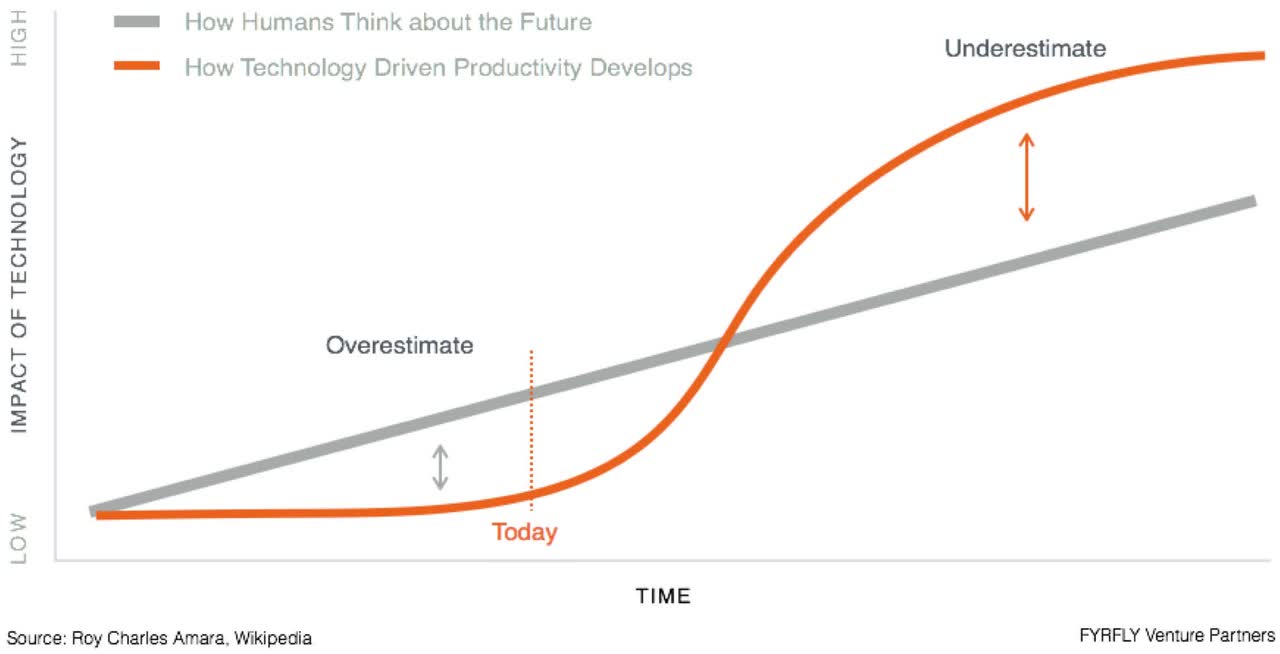

Glimpse’s current solutions are quite experimental. For example, an ordinary person would probably look at Qreal’s work with Scent beauty and struggle to understand the appeal and/or potential applications for this technology. In response, I will point you to Amara’s Law Graph (used by Glimpse’s CMO James Watson) which describes the relationship between our expectations and the maturity of technology over time.

Wikipedia

It therefore wouldn’t be too unreasonable to think that if businesses start to cut back on spending in the event of a recession, Glimpse may be on the receiving end of this. So far they haven’t and as mentioned, S5D continues to secure new contracts which I believe may surprise the market in terms of its contributions to the top line. The customers Glimpse works with are generally large businesses and therefore a contract size that may be significant for Glimpse, is proportionally a lot smaller for the customer. One of the attractive aspects of investing in micro-caps is the large effect partnerships can have on financial performance – but this can be felt in both directions (gains and losses).

This brings me to my final point which is customer concentration, in Q2 55% of Glimpse’s revenue came from two customers. I expect the recent acquisitions to help start to diversify this revenue mix but it still poses a risk and this is noted by the company itself in the SEC filings. The company noted that both companies accounted for either 29% ($1.14M) or 26% ($1.027M) of Q1 FY23 revenues. One of the same customers also accounted for 56% of Q1 FY22 revenues ($572,320).

This is extremely positive, by reading between the lines we can see that Glimpse has a strong partnership with a certain customer which has likely nearly doubled Y/Y in terms of quarterly revenue contribution. I speculate that this is Snap, who have worked with subsidiary Qreal for a long period – Qreal was a Glimpse company when it IPO’d in 2021. This partnership forms an important base for Glimpse’s revenues but also presents a risk – if Glimpse loses these customers it could have significant implications on the company’s ability to scale and achieve cash flow neutrality.

The bottom line

I maintain my buy stance on Glimpse, which is a high-risk, high-reward proposition. The move to cash flow neutrality in FY23 is a sensible one, Glimpse has a large cash buffer but this may be reduced slightly through contingent payments related to acquisitions in 2023.

We are in the early innings of the VR and AR industry, at the moment a lot of the solutions on the ‘metaverse’ side remain quite experimental. Many analysts are forecasting significant growth within this industry, others predict that the applications of this technology will be limited. I sit on the more optimistic side of the fence, and believe Glimpse is a great way to get exposure to the industry in a more diversified manner than you would usually see in the micro-cap space. I would also argue that even if many of the current bullish forecasts don’t materialise, Glimpse and investors can still make money through the large capital inflows that are likely to come into the industry over the next few years.

The Glimpse Group will report Q2 ’23 earnings on the 14th of February.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment