tiero/iStock via Getty Images

By Coco Zhang, ESG Research; Warren Patterson, Head of Commodities Strategy; Gerben Hieminga, Senior Sector Economist; & Padhraic Garvey, CFA, Regional Head of Research, Americas

Oil and gas: energy dominance likely to come before transition

There is debate brewing over what the US medium- to long-term energy strategy should be as the war in Ukraine rages on. We think that given the current high energy price environment and rapidly growing demand from Europe, the US is likely to at least partially return to energy dominance through increasing oil and gas output to supply the European market. This will outweigh energy transition efforts in the industry, at least for now, frustrating emission reduction goals through more associated carbon and methane emissions. In the US, Liquified Natural Gas terminals alone could emit an amount close to all the vehicles in California per year; any ramp-up in production and export could further drive up emissions.

This would ideally be accompanied by decarbonisation technologies, such as Carbon Capture Storage (CCS), to help compensate for additional emissions. In reality, however, a handful of oil and gas companies have just established strategies to integrate CCS into their climate plans, and their planned CCS capacity would be only a fraction of emissions from any production increases. This means that it would take time before this technology can meaningfully curb emissions in the US oil and gas sector, which is set to grow.

As an aside, the US Securities and Exchange Commission’s proposed ESG disclosures will help the marketplace to least differentiate between various players through a wider assessment of carbon footprints and carbon shadows. However, this is not really a determining factor until 2024, when the first company results would reflect the disclosures. The prognosis here is not great, all things considered, at least not in the coming few years. Although an accelerated and subsequent improvement is probable thereafter.

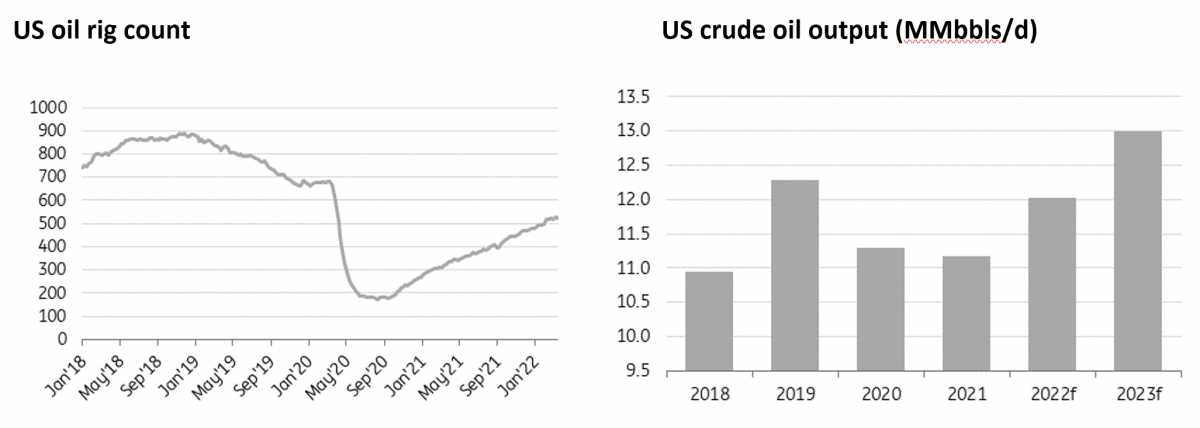

US oil production is on the increase

Latest data shows the number of active oil rigs in the US at 531, more than a three-fold increase from the lows of 2020, but still some 20% below pre-covid levels. The burning question now is whether the capital discipline seen from US producers starts to wane in the current high price environment, and more production is favoured. We think it will, on a solid demand rationale for considerably higher production.

According to the US Energy Information Administration, US oil output in 2022 is expected to grow by 850Mbbls/d YoY to a little over 12MMbbls/d, whilst 2023 output is forecast to hit a record high of 12.99MMbbls/d.

There is also plenty of pressure from the US administration. The US Secretary of Energy has urged US producers to increase output to help bring prices back under control. Action already taken, including the release of oil from the strategic petroleum reserves, is only a short-term solution. And it would appear that the changes we are seeing in Russian supply are likely structural, implying an opportunity for US oil output to increase to help fill the void.

US oil production is getting back to its heyday

Baker Hughes, EIA, ING Research

It is not only upstream where there is potential growth. US refiners will likely also benefit from the tight refined products market. Russia is the second-largest net exporter of refined products after the US. And with Russia, prior to the war exporting in the region of 1MMbbls/d of gasoil, the market is likely to tighten. Europe will need to turn increasingly to the US to help make up for shortfalls from Russia.

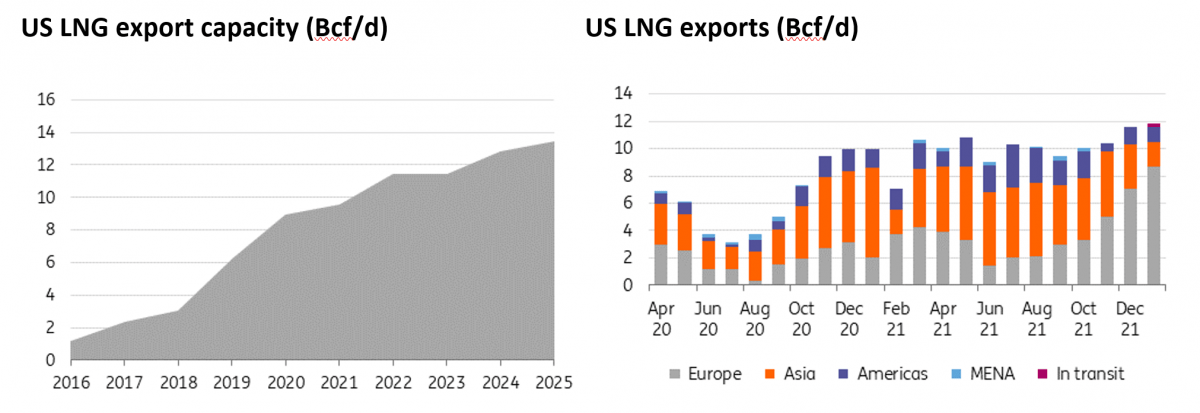

US gas output also set for expansion

Current developments are also supportive for growth in US gas output. Having grown 2.2% in 2021, US dry natural gas production in 2022 is set to grow by around 3.4% YoY to a record level. And this growth should continue through 2023. Although growth in export volumes will be limited due to LNG export capacity constraints.

The US puts its foot on the gas too

Baker Hughes, EIA, ING Research

In 2021, the US supplied the EU with around 22bcm of LNG. The US and EU have agreed a deal, where the US will supply at least an additional 15bcm of LNG to the EU in 2022. Given the strength seen in European prices, market forces are likely to ensure this additional volume will flow to the EU this year regardless. Given the capacity constraints on US exports, an increase in flows to Europe would mean a change in trade flows rather than an increase in absolute export volumes.

Once Europe ends its dependency on Russian gas (the EU imported around 155bcm in 2021), there will be no going back. Therefore, a constructive demand outlook for LNG combined with a relatively small pipeline of projects suggests that we will need to see further investment in US liquefaction capacity in the years ahead.

There are risks. The EU has been a leader in energy transition, and if the EU becomes an increasingly larger home for US LNG, this increases the exposure of US exporters to changes in EU policy, such as a quicker transition away from natural gas to renewables.

That said, the latest deal between the US and the EU suggests that the EU would work towards committing to an additional 50bcm of US LNG until at least 2030, which helps to counter that risk to a certain extent.

Coal not disrupted, but power sector decarbonisation slows

Coal production in the US has roughly remained flat compared to a year ago, and the country’s coal consumption has also been in line with historical patterns as of early March. So far then, the US power sector has not been radically diverted towards more coal production, partly thanks to ample natural gas resources in the US and the geographical distance between the US and Russia/Ukraine.

Looking to the near future, the EIA projects a 4% increase in US coal production and a 1% decrease in total coal consumption in 2022. This would lead to more exports, especially to Europe if it decides to replace Russian gas and coal with more US coal. Stronger export demand for US coal would offer more support to US coal prices, which could favour further domestic coal-to-gas switching.

US coal not significantly disrupted

EIA, BNEF, ING Research

The coal-to-gas switch would have positive environmental potential, but that is not disruptive enough to the US power mix, especially if the new gas generation remains unabated. What the US power sector needs is significantly more renewables to come on line but the swiftness of the energy crisis risks affecting the speed at which renewable energy will be deployed, as many parts of the renewables’ supply chain have also been affected by the war. Slower adoption of renewables would delay the administration’s goal of 100% carbon pollution-free electricity by 2035.

The EIA’s early March forecast predicts that renewable and nuclear energy will together account for 56% of the electricity mix by 2050 in its reference case. This means almost half of the electricity will still come from fossil fuels and these plants will emit CO2 into the atmosphere (if no CCS technology is installed).

Further disruptions from the war would require the US to work extra hard in subsequent years to bring its climate goals back on track. The additional emissions that the US emits now because of the crisis should be taken out at a later stage, for example, by speeding up technologies for negative emissions like CCS with bioenergy (BECCS) or direct air capture. Several BECCS networks are being developed in the US; Tesla’s CEO Elon Musk has committed to setting a $100mn price for direct air capture, a carbon removal technology in its early development stage.

US electricity generation from selected fuels under EIA’s reference case

EIA, BNEF, ING Research

Nuclear supply dynamics need to be revisited

In 2020, 20% of electricity was generated from nuclear sources. The Biden administration views nuclear as a form of clean energy; in fact, the infrastructure bill, which was signed into law last November, allocates $6bn to maintain existing nuclear power reactors in the US. And without nuclear, it would be almost impossible for the US to realise its 2035 100% clean electricity goal.

Russia makes up 16% of the US import of uranium, a major element used to generate nuclear energy. While that 16% of supply is not easily and quickly replaced, the US Department of Energy is advancing programmes to help US nuclear plants secure alternative uranium supply.

Nevertheless, the nuclear industry is not likely to see a significant boost because of cost concerns, long construction periods, environmental controversies, and safety considerations. The US EIA forecasts under its reference case that nuclear generation will slightly drop from 778 billion kilowatt-hours in 2021 to 662 kilowatt-hours in 2050, and its contribution to the US power generation mix will reduce from 19% to 12% within the same period. However, that decrease requires an offsetting growing contribution of renewables to the mix. Frustration on this front could well slow the downsizing of the nuclear contribution, especially should clean energy achievements get hit by a short-term focus on energy dominance and away from the energy transition.

Bottom line, nuclear is primed to remain on the table as a viable and clean energy option, where there already exists expertise despite safety concerns.

Climate legislation and action on hold as power price crisis persists

As an additional dimension, the Build Back Better bill, which would allocate $555bn to clean energy and climate-related investments, remains stuck in the Senate partly due to arguments that heavy new spending would add to inflation. The elevation in the energy crisis on account of the Russia-Ukraine war has only made things worse, further dimming implementation prospects.

As the proposed bill includes $333bn of generous tax credits for renewables, clean energy manufacturing, EVs, hydrogen, and carbon capture and storage (CCS), side-lining the bill takes oomph away from new developments of clean energy and low-carbon technology in the US. The Russia-Ukraine conflict has also affected the supply of metals, many of which are key raw materials for low-carbon solutions such as solar PVs and EVs.

In addition, several US states, including climate leader California, are providing fuel price packages and/or suspending state taxes on gasoline and diesel in response to record-high fuel prices. There have also been discussions at the federal level to temporarily halt gasoline taxes for the rest of 2022.

These policy proposals and actions, plus the uncertain increase of Electric Vehicle (EV) tax credits under the Build Back Better bill, will slow down switches from internal combustion engine vehicles to EVs.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment