ElsvanderGun

Dear readers/followers,

The Cheesecake Factory (NASDAQ:CAKE) is a restaurant chain located and active in the USA and on an international basis. Like some other typical restaurants, the company operates a mixed ownership model, where parts of the restaurants are directly company-owned and operated in certain areas, while in other areas they are licensed or franchised in some way

The company mainly distributes, as the name suggests, cheesecakes, and operates around 220 restaurants in the US, as well as operating its own bakery production.

In this article, we’re going to be taking a look at the company and I’ll show you why I actually believe this business might make for a good investment.

Cheesecake Factory – a Company worth the money?

I’ve only visited the Cheesecake factory once – and I thought they had pretty decent food. The company’s focus is on Cheesecakes, burgers, pizza, pasta, steaks, and sandwiches. They have a pretty diverse menu, and I believe the main appeal lies in their cheesecakes.

The company has been around for over 50 years and is headquartered in California. It categorizes itself as an experiential dining category leader, with a number of growth engines.

Cheesecake Factory IR (Cheesecake Factory IR)

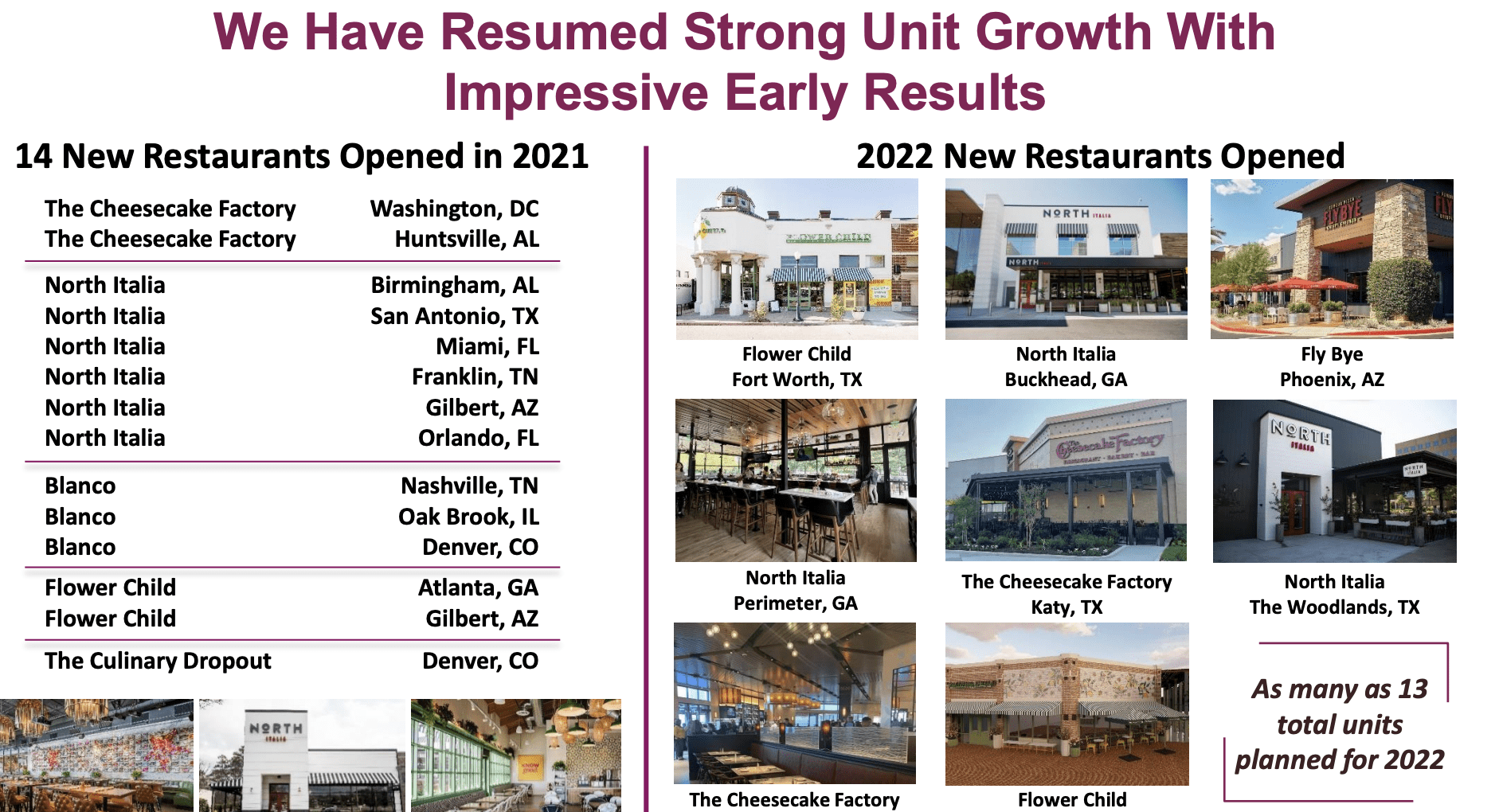

The company doesn’t just own the Cheesecake factory brand either but has expanded into things like North Italia, contemporary Italian dining, that’s recorded impressive overall check sizes with high amount of alcohol mix (25%+), with relatively unique selections. The company’s sales were up 8% in 2021. In fact, the company has several growth engines and brands that are ripe for expansion and growth.

CAKE IR (CAKE IR)

One of the company’s main challenges has been the earnings decline during COVID-19. Like most restaurants, CAKE saw heavy impacts here – but it was one of the few to actually go to negative earnings, with an EPS decline of -157% and EPS of -$1.5.

This has since recovered, now showing EPS at around $1.5-$2, but this is still far below the company’s pre-pandemic results. Also, the company completely cut the dividend for several months, and has since then reinstated it at about 60-65% of the pre-pandemic level, coming to around $0.81/share, implying a yield of 2.8% at the time of writing this article. Not the greatest, especially not for a restaurant that showcases this sort of EPS volatility and potential downside. If you invested during COVID-19, you’re in the green at this time – that much is a positive here.

However, the company is back to growth at this time – new restaurants are opening, and sales are good – or at least decent.

CAKE IR (CAKE IR)

the company’s focus is on providing food that is considered fresh, by combining menu items cooked and assembled on premises with an integrated bakery. The integrated bakery focuses on the desserts like Cheesecakes and other items that the company is known for.

Aside from this, the company focuses on its service and Ambiance, trying to achieve best-in-class service, hospitality, and operational execution. On a high level, what really differentiates CAKE from other companies and restaurants is the integrated bakery in the restaurants, which is also what I believe has delivered some of the sales driving in the past years. This enables the company to produce a wide variety of desserts, which enables creativity, quality control, and efficiency.

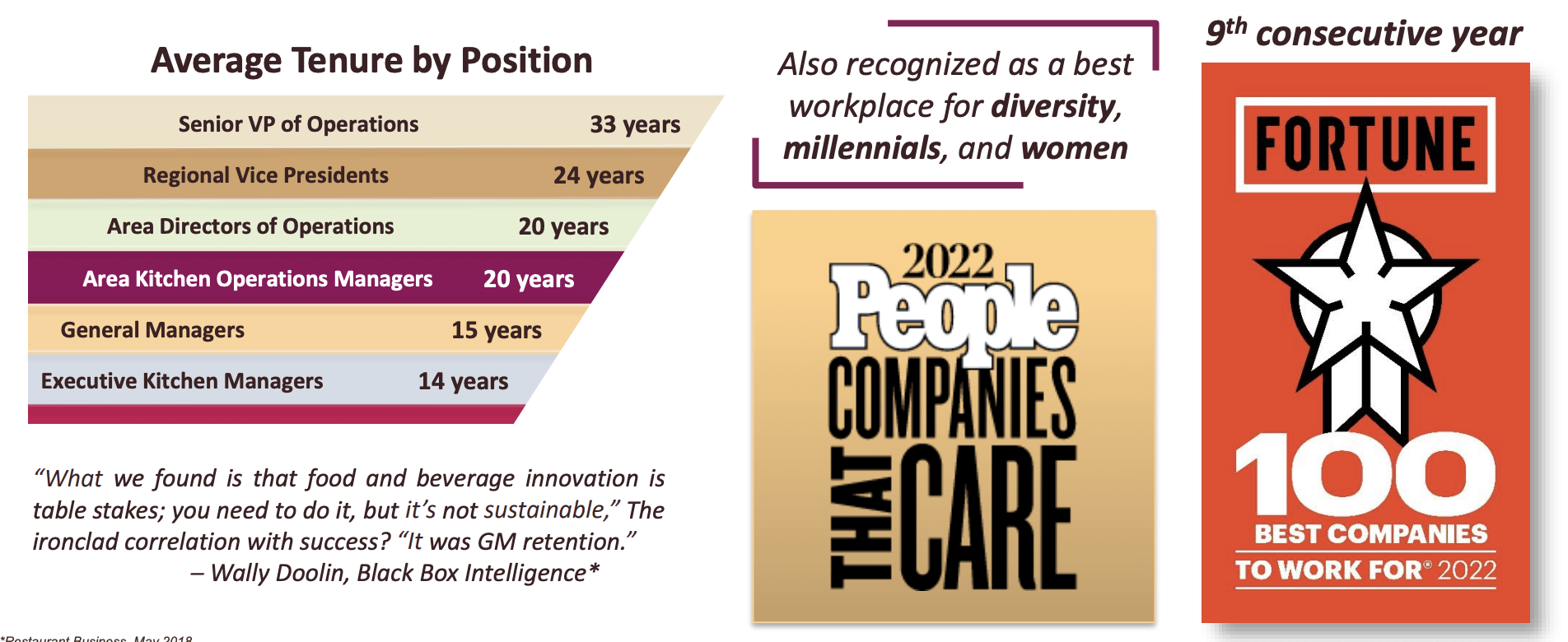

The company also has a very internal recruitment and management structure, with very long tenures in the C-suite. This is something I like to see for a non-franchised restaurant, which is what CAKE is.

CAKE IR (CAKE IR)

CAKE has a number of leadership or close-to-leadership positions. Namely, the company is the leader in unit volumes by a wide margin, and is a solid average check-size restaurant, with only Yard House, Bonefish, and Maggiano’s managing to beat the average $27 check size. The company is trying to make things better by improving takeout packaging and takeout convenience, and pushing its digital channels.

The company’s plan is to build on the Cheesecake Factory’s success, and move forward into diversification – which I would much rather invest in than say, singular restaurants which are some of the most failure-bound businesses out there.

CAKE IR (CAKE IR)

The company believes that its stable but agile brands will be best equipped to handle incoming overall downturns in the market. It has provided us with 2022 guidance.

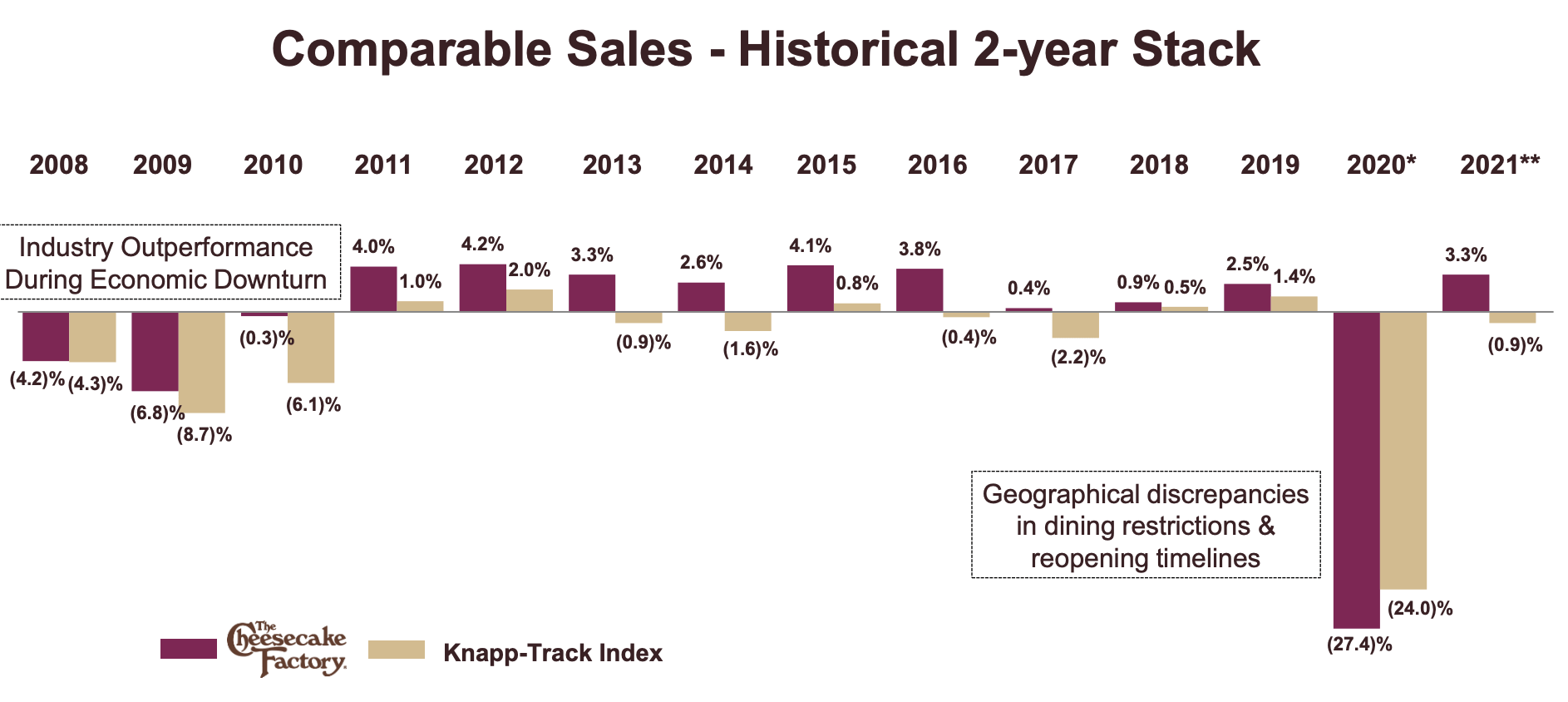

CAKE is, after COVID-19, a higher-beta investment. However, for most of the past 14 years, the company has been more resilient than the overall market, and it’s been extremely rare for the company not to outperform the relevant indices here.

CAKE IR (CAKE IR)

CAKE Bulls will want to give the picture that 2020 was a one-off – something that won’t be repeated as we move forward into different environments. CAKE bears meanwhile, will want to take the stance that this was a foreshadowing of industry rationalization and that companies like CAKE won’t be as resilient or as stable going forward.

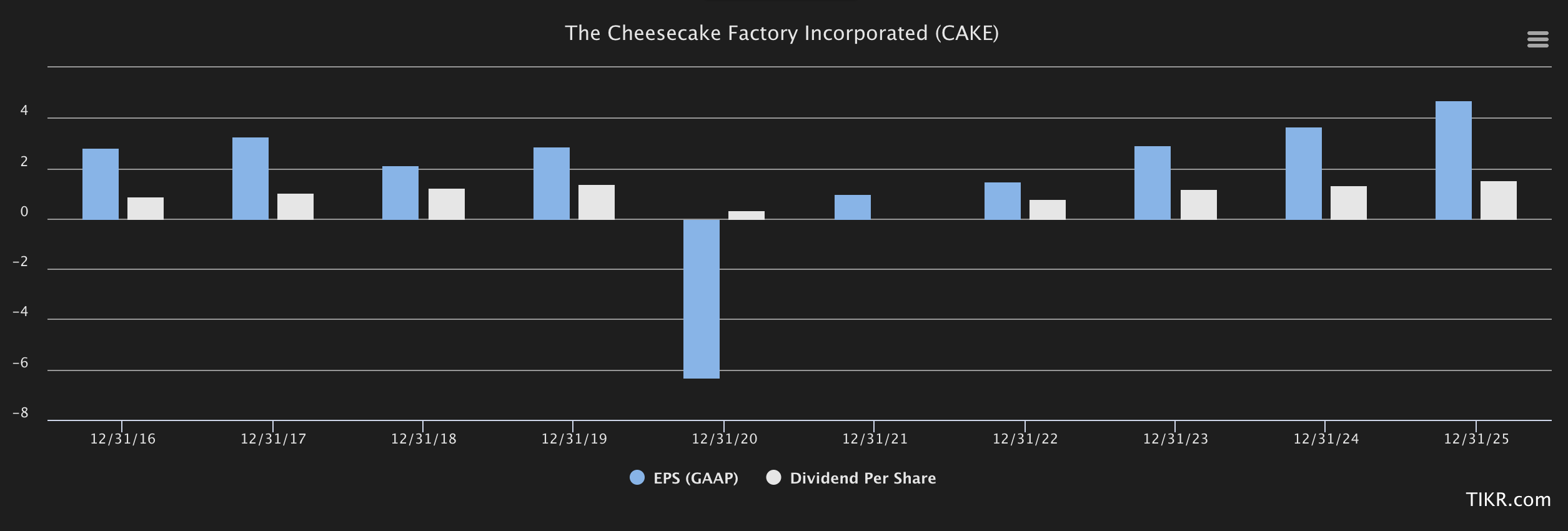

I would personally take the more bullish stance on CAKE. CAKE has been able to maintain very good margins even during more difficult times. Earnings and dividends are, according to forecasts, set to grow morning forward, and go beyond what we’ve seen in the past in terms of both EPS and payouts.

CAKE EPS/dividend forecasts (TIKR.com)

The company did go negative in margins in 2020 but otherwise maintains a healthy 5-9% over time, with the latest LTM of around 3%. Not the best, but decent enough here.

The latest quarterly report came in at a surprise loss, which caused the share price to plummet quite significantly. Revenues finished within the guidance range, but a combination of macro headwinds, inflation, wage increases, SCM and other things made the bottom line not exactly reach the overall expected levels.

Sales increased by 1.1% YoY, with a 2.8% YTD YoY increase, and average unit volume is up to $12M per year, with massive demand for newly-opened locations. This unit-level sales volume is one of the major arguments I’ll make for taking a more bullish than negative stance on CAKE here fairly soon. The company has increased its pricing by 4.3% menu-wide to offset inflation. Challenges came in, especially with building maintenance costs, utility costs, and other things.

Let’s look at the overall valuation.

Company Valuation

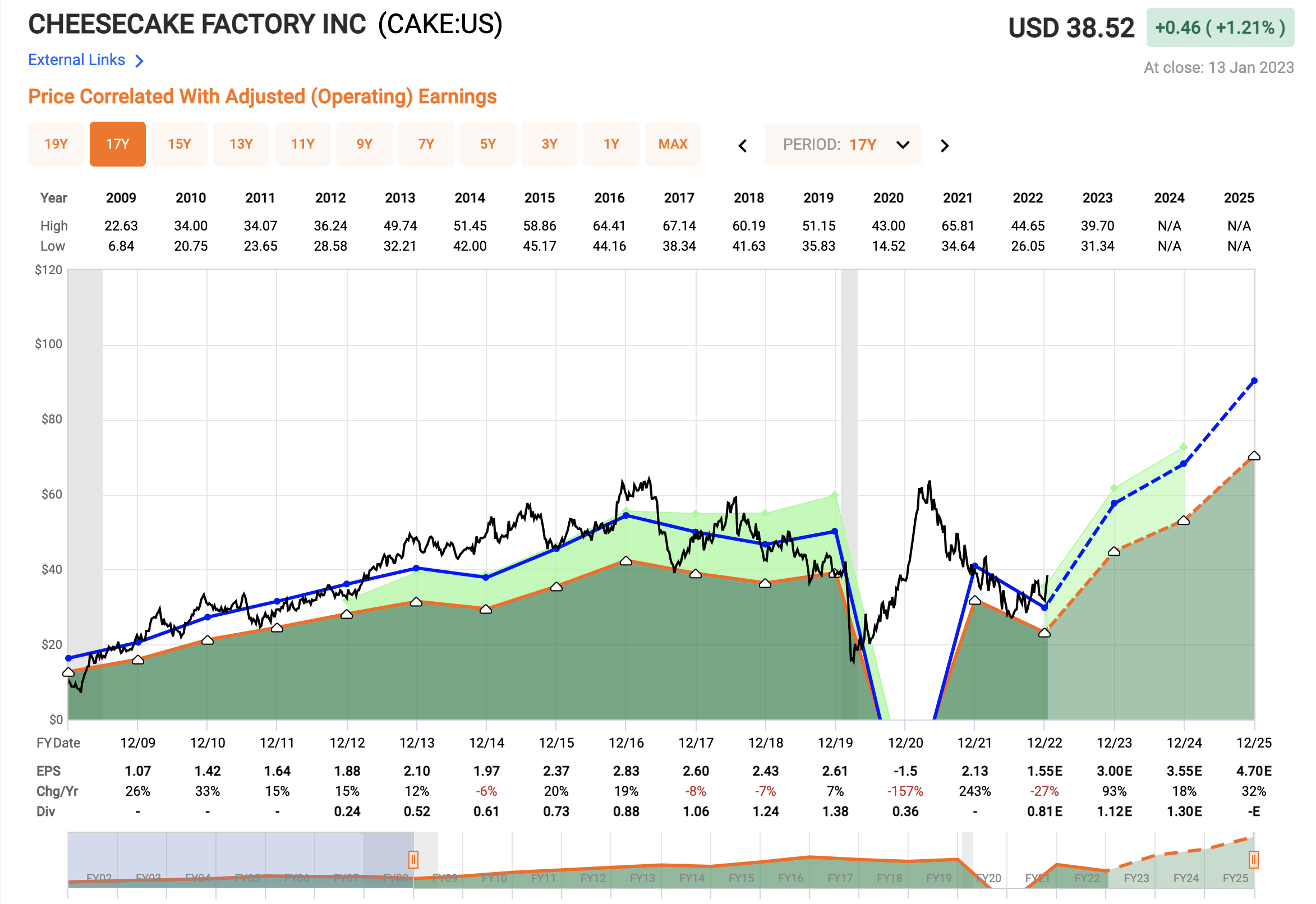

As I’ve said, company valuation has gone up and down.

CAKE valuation (F.A.S.T Graphs)

And it seems likely that the ups and downs will continue – even if the foundational trends here are in a sort of overall upswing, as these challenges normalize. The company still does not have a credit rating, and its relative yield is also rather low.

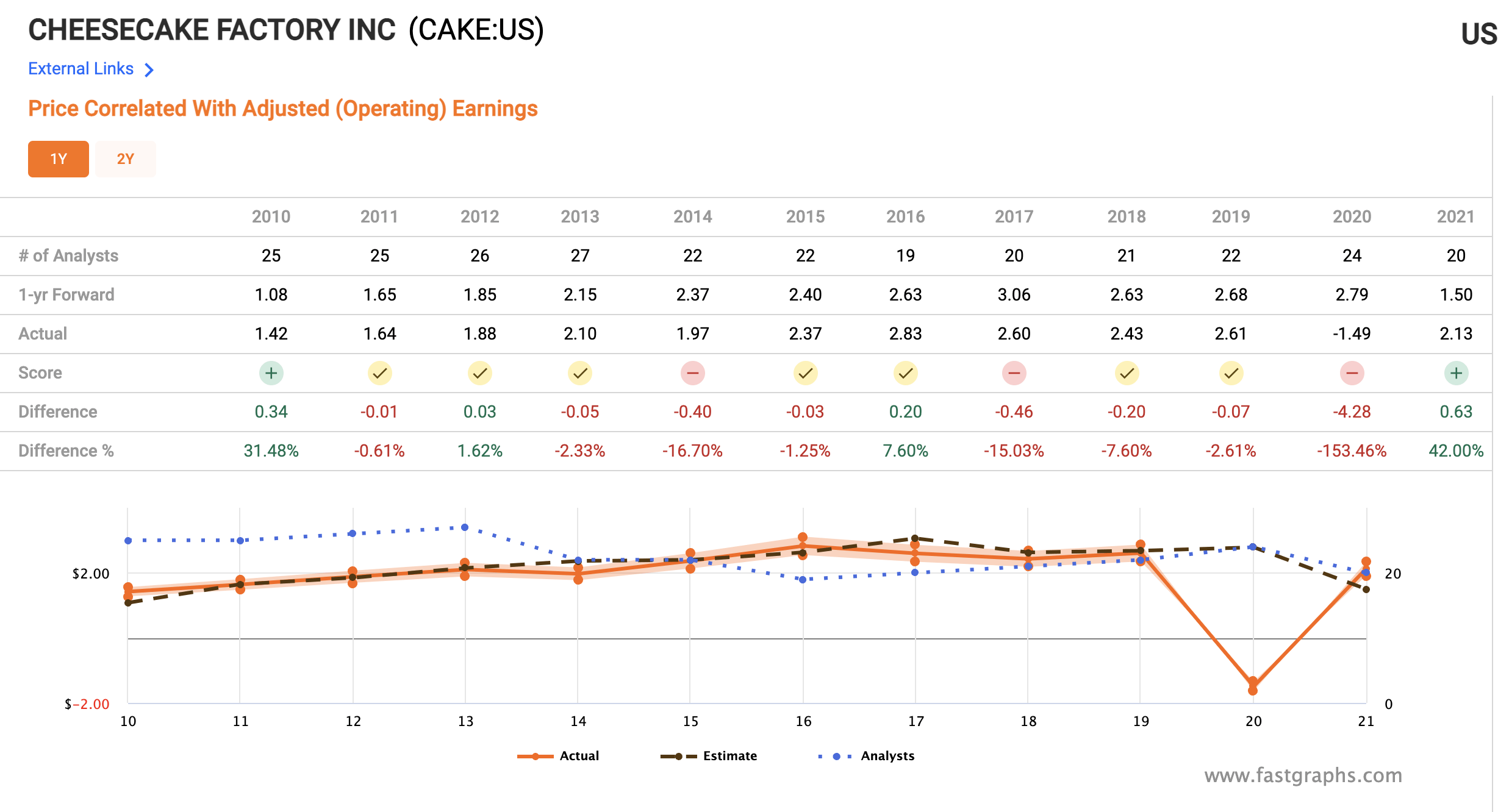

However, the upside is significant if anything of this forecast materializes in terms of EPS growth, with close to triple digits in 2023E, followed by double digits. The company has a decent forecast accuracy – a 25% negative miss ratio, with plenty of COVID-19 misses in the company’s recent memory.

F.A.S.T graphs CAKE accuracy (F.A.S.T graphs)

Other than recent volatility, the company has been relatively simple to forecast and delivered stable/slightly growing forecasts.

I don’t fully expect the ramp-up in earnings to be as massive as analysts are forecasting here. Given the recent set of trends and challenges, I don’t see these being compatible with the sort of EPS growth that is expected from CAKE here.

However, the company has lost most of the historical premium to longer-term earnings, which is what marks most of the attractiveness for the company here, as I see it.

I would not use DCF here as a method of valuing the business given the volatility of the company’s revenues and earnings. There’s too much uncertainty baked into things here for this to be a solid forecast or way to look at the company. Instead, we mix historicals and forecast accuracy with peer averages and other expectations. CAKE is currently followed by 14 analysts – only 7 of which consider it to be a “BUY” at $38.19/share. The averages go from $26 on the low side to $40 on the high side, with an average of around $34.4/share, implying a double-digit overvaluation at this time.

I consider this not taking into account the positivity of the current forecasts and the relative likelihood of some growth at this particular time. Most restaurant companies that aren’t heavily franchised can be used as peers, and the very simple fact is that the company is very conservatively valued on a normalized P/E basis. If we look outside of the current trends, the normalized P/E is closer to 14x than 20x. The peer average in this sector is around 25-28x P/E, with outliers like Wendy’s (WEN) at 16x, and Chipotle at 37x. So there are a lot of up and down, depending on your specifics and what the company is looking at making in the long term.

As I said, current forecasts are for this company to improve materially in the near term, 2023 and up to 2025E.

While I would not agree with the current forecasts of 80-90% adjusted EPS growth in the next 1-2 years, I do believe there will be growth.

What’s more, I believe the recent set of trends implies that:

- The Cheesecake factory is an attractively perceived business, and restaurant chain, together with its other brands.

- The company has proven its ability to generate consistent profitability outside of COVID-19 trends.

- The reinstatement of the dividend communicates management confidence – at least to a degree here.

Because of the non-existent credit rating and the company’s relatively small size, I’m not going “deep” here – but I believe that analysts are underestimating the Cheesecake factory here.

The way I might invest is tied to options – I’m not going into the common here – but I believe that the common may offer you attractive returns for the long term. There’s a bit much here in terms of risk for me to be completely comfortable with this when put into relation to what’s available in the rest of the market, but overall I will call CAKE “attractive” here.

I will give CAKE an overall long-term PT of $40/share here, and I would successively raise it as the company starts coming in with quarterlies that sort of confirm the company’s own, and analyst positive forecasts.

For now, here is my thesis on CAKE.

Thesis for the common share

- CAKE is one of the more attractively-valued Restaurant stocks currently out there. Normalizing the company’s earnings means that the stock is currently trading below its future earnings potential, and I believe it to be undervalued. I expect this undervaluation to become more clear as the company’s results come in and imply how compressed the company’s valuation has become.

- Despite not having a credit rating, I do believe this company to be qualitative enough to warrant a “BUY” rating when it becomes cheap.

- I believe the company warrants this today going into 2023, and I would give the company a “BUY” here.

- CAKE is a “BUY” with a PT of $40/share – though I believe the options to be the better way to invest here.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I can’t give the company a qualitative stamp due to the credit rating, but I can call it cheap and undervalued due to its normalized earnings potential and forecasts. For that, it’s a “BUY”.

Thesis for the Options

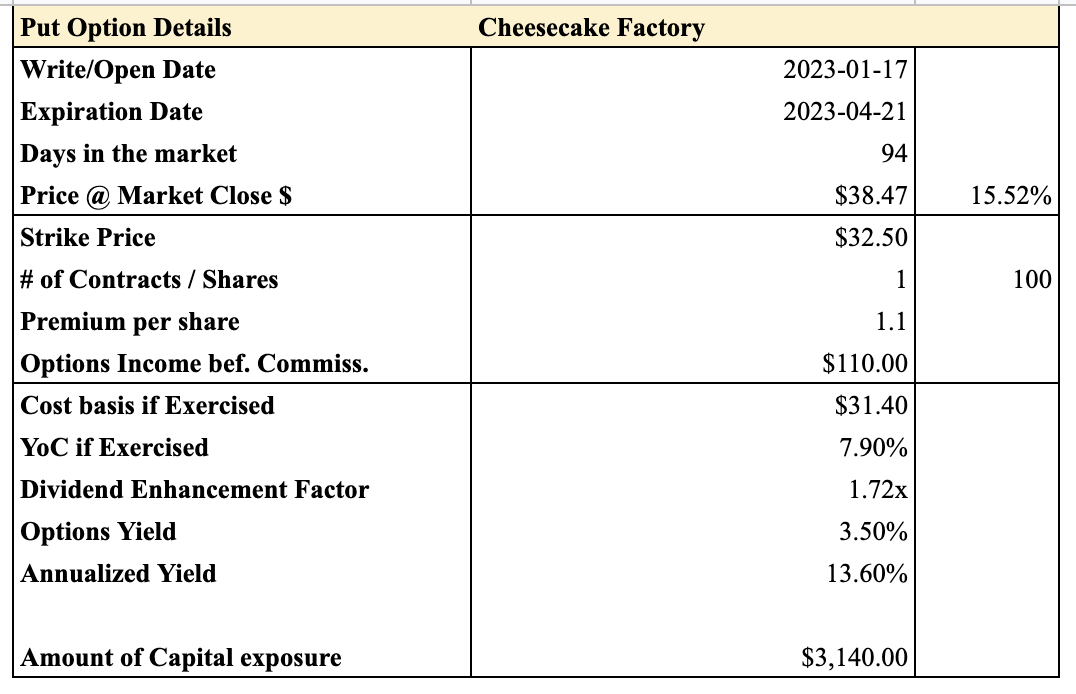

As of this article, I’m able to find the following Put option for CAKE.

Put option CAKE (Author’s Data)

It’s not the best one in terms of RoR, but it’s a very conservative and attractive use of funds, as I see it. Not that much of required capital exposure as a minimum, and respectable at over 12% annualized. What’s more, you’re able to really secure your entry point into CAKE here.

That’s why I’m going for these options, if I invest in CAKE.

Be the first to comment