Aleksander Kaczmarek/iStock via Getty Images

I have never considered myself to be much of a fan of investing in retail stocks, particularly those focused on clothing, accessories, and other related goods. But every so often, I will find a firm in this space that seems to offer some nice potential relative to the risk incurred. A great example of this can be seen by looking at The Cato Corporation (NYSE:CATO), a fashion retailer that has had something of a mixed operating history but that has a fortress balance sheet. Recently, financial performance achieved by the company has been anything but great. Although the most recent sales figures were promising, profits have pulled back and the number of locations it has in operation are down year over year. The good news though is that the company has no debt on hand and has a significant amount of cash relative to its market capitalization. This creates a very favorable risk-to-reward opportunity in my opinion that could go on to create a nice bit of upside for investors moving forward.

Mixed results continue

Back in October of 2022, I wrote an article in which I changed my opinion on the opportunity offered by Cato. At that time, I raised my rating on the company from a ‘hold’ to a ‘buy’, reflecting my renewed view that shares should outperform the broader market for the foreseeable future. This assessment came even as the company faced some deterioration in its operations leading up to that point. At the same time, however, shares of the company looked cheap and the structure of the company’s balance sheet made it look like a low-risk player for long-oriented investors. Since then, the market has not exactly agreed with my assessment. While the S&P 500 is up 9.4% since the publication of that article, shares of Cato have experienced downside of 1.2%.

Author – SEC EDGAR Data

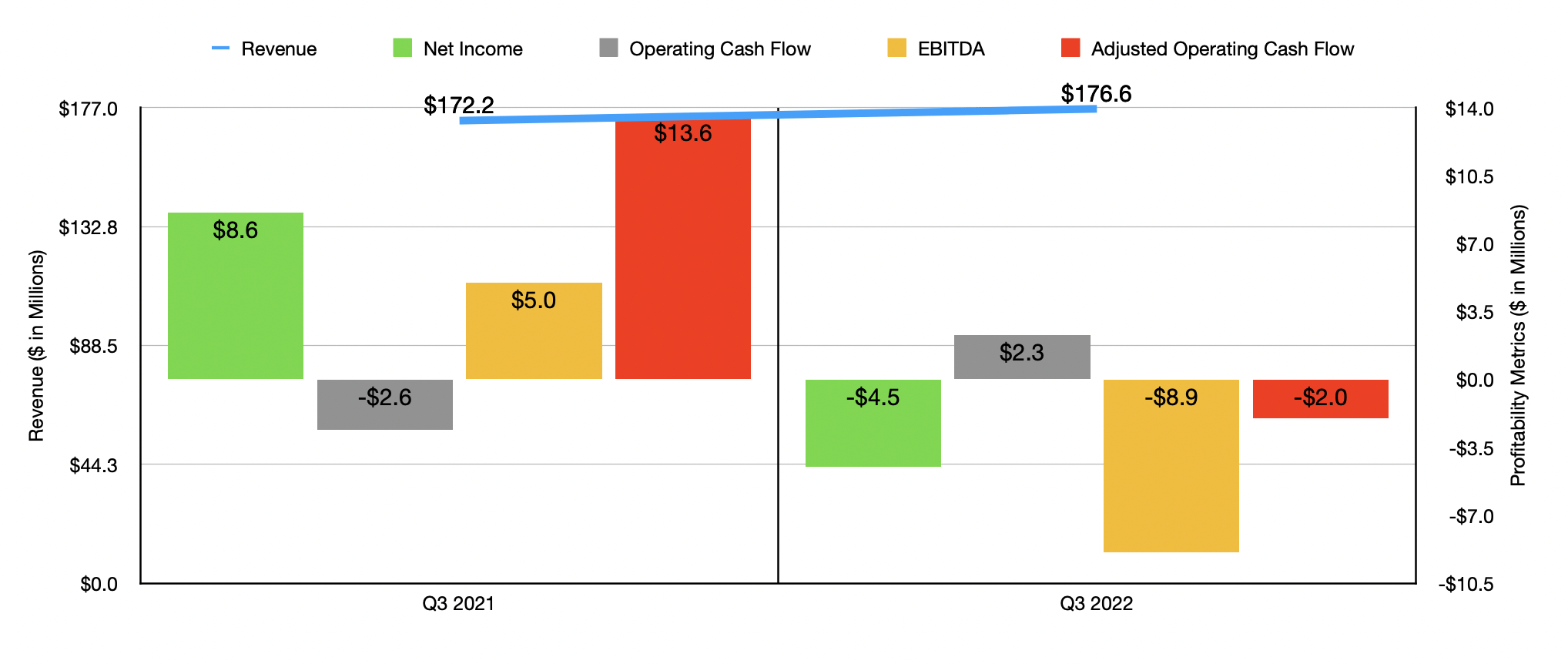

This return disparity comes in response to mixed financial results covering the third quarter of the company’s 2022 fiscal year. This is the only quarter for which new data is available that was not available when I last wrote about the firm. On the positive side, sales achieved by the company came in at $176.6 million. That’s 2.6% higher than the $172.2 million generated at the same time one year earlier. What’s really remarkable about this is that it developed even though the number of locations the company has an operation dropped from 1,324 to 1,317 over the course of a year. The real driver behind this increase, then, was a 3% improvement in comparable store sales.

It’s great to see top line results improve. Unfortunately, however, bottom line results did worsen. The firm went from generating a net profit of $8.6 million to generating a net loss of $4.5 million. The primary driver behind this was a surge in the firm’s cost of goods sold, excluding related depreciation, from 61.1% of sales to 70.7%. This change, management said, was driven by higher revenue associated with marked-down goods, combined with increases in freight and distribution costs. Considering the broader economic environment we are dealing with, this makes a great deal of sense. Excess inventories lead to markdowns, and high energy prices, combined with other supply chain issues, would have impacted freight and distribution. With energy prices now falling and supply chain issues working themselves out, some of this pain is certainly short-term in nature. But I digress. Other profitability metrics largely followed suit. Although operating cash flow went from negative $2.6 million to positive $2.3 million, this figure actually went from $13.6 million to negative $2 million if we adjust for changes in working capital. And finally, EBITDA declined from $5 million to negative $8.9 million.

Author – SEC EDGAR Data

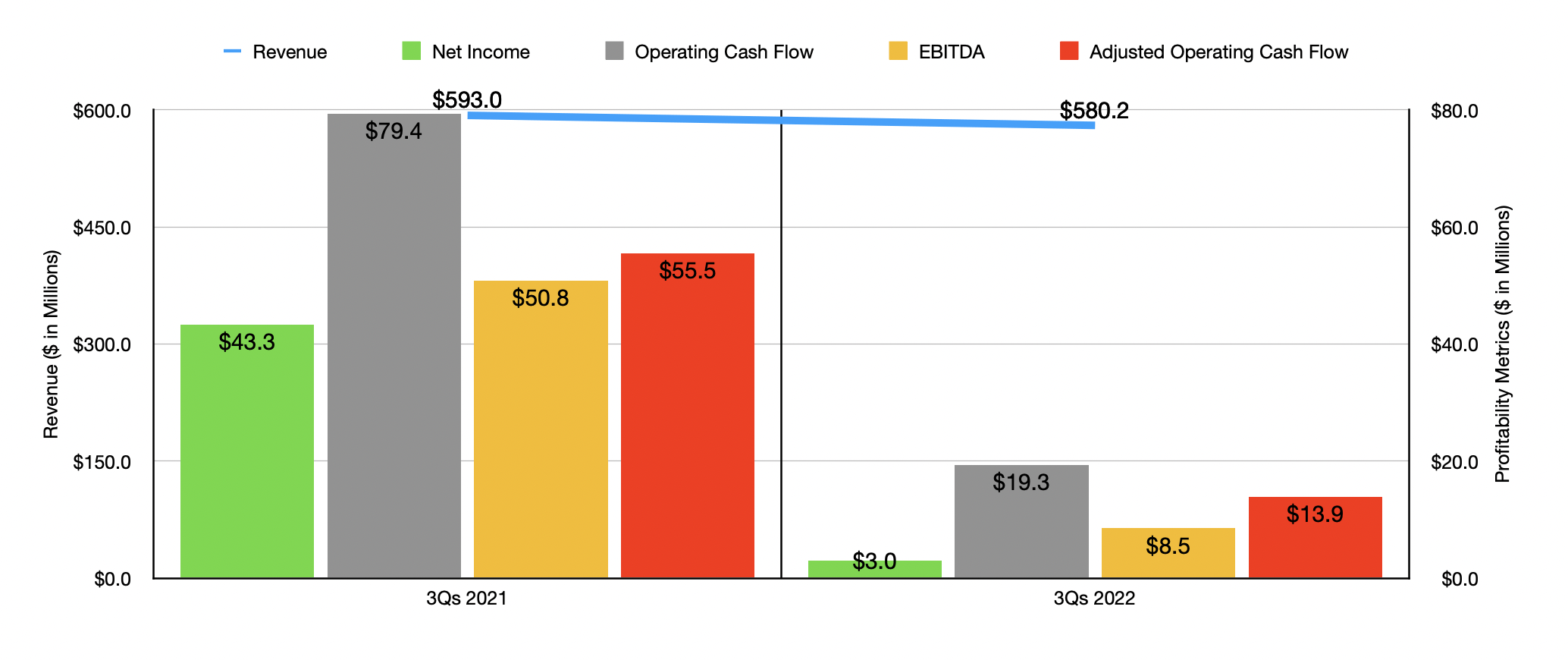

For those who haven’t followed Cato very closely, it’s worth noting that the firm was troubled for much of 2022. For the first nine months of the year as a whole, sales came in at $580.2 million. That’s actually down from the $593 million reported the same time one year earlier. The decline in sales, combined with the other issues I already mentioned, were instrumental in pushing profits down from $43.3 million to only $3 million. Operating cash flow shrank from $79.4 million to $19.3 million, while the adjusted figure for this went from $55.5 million to $13.9 million. And finally, EBITDA for the company dropped from $50.8 million to $8.5 million.

Author – SEC EDGAR Data

We don’t really know what to expect for 2022 as a whole. But if we annualized results experienced for the first nine months of the year, we would anticipate net income of $2.4 million, adjusted operating cash flow of $12.9 million, and EBITDA of roughly $8 million. Given the extreme volatility of net profits over time, I don’t believe it’s the best metric to value the firm with. But using the price to adjusted operating cash flow approach, we would end up with a trading multiple for the company of 15.8. This compares to the 3.9 reading that we would get using data from 2021. Meanwhile, the EV to EBITDA multiple of the company would be 6.8. That stacks up against the 1.1 reading that we would get using data from the year before. As part of my analysis, I also compared the company to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 3.4 to a high of 48.7. Four of the five businesses were cheaper than Cato. Using the EV to EBITDA approach, the range was from 1.8 to 6.4. In this case, our prospect was the most expensive of the group. Even though shares are a bit pricey compared to similar firms, it’s worth noting that Cato has no debt on its books and enjoys $149.5 million in cash. This makes the risk of near-term collapse virtually 0 absent something unexpected like fraud and it reduces the company’s enterprise value to only $54.3 million. It doesn’t take a lot of cash flow to justify that valuation.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| The Cato Corporation | 15.8 | 6.8 |

| Tilly’s (TLYS) | 48.7 | 3.5 |

| Citi Trends (CTRN) | 3.4 | 1.8 |

| J.Jill (JILL) | 4.0 | 3.5 |

| Express (EXPR) | 7.7 | 6.4 |

| Destination XL Group (DXLG) | 11.4 | 5.5 |

Takeaway

Although I wouldn’t necessarily call Cato the greatest retail prospect ever, the company has a lot going for it. Yes, profits and cash flows have been a major pain over the past several quarters. At the same time, however, the recent uptick in sales is promising and the surplus of cash on the company’s books mitigates risk materially. Due to these factors, I have no problem keeping the ‘buy’ rating I had on the stock previously.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment