Kwarkot

As they age, many people decide to sell off their direct investments in real estate properties. They often then look for passive income from REITs.

It is little wonder that we see a lot of such investors at High Yield Landlord. Our guiding approach involves taking a “landlord mindset.”

I ended up chatting with one of these investors, after my December monthly update article, which discusses my own portfolio and related thoughts. It became clear that what he really wanted now was a portfolio that did not need active tending.

Call this a Buy-Hold-And-Go-Fishing Portfolio, or a Go-Fishing Portfolio for short. My own portfolio is definitely not what such an investor would want. I invest nearly full time and a lot of that time is focused on REITs, seeking great returns by reacting to what the firms and the markets do.

The owner of High Yield Landlord, Jussi Askola, offers a Retirement Portfolio that may address some such needs. But that conversation got me to wonder what my own choices would be for a similar portfolio. Jussi and I see eye to eye about the big picture but often not about details.

Writing this article was an exercise, undertaken to see what I would now recommend for such a portfolio, and why. This may prove useful to some of those investors, and maybe to me in a few years.

Setting Expectations

Before getting into portfolio selections, we need to set some context. Landlords of physical properties often report cash returns between 5% and 10%, but this is misleading.

The properties may sell at cap rates (ratios of Net Operating Income or NOI to sale price) of 6% or somewhat more. And leverage can further boost the returns on equity. This makes superficial sense of the returns reported by landlords.

But such landlords handle a variety of tasks that must be paid for when a REIT owns a similar property. They take on roles such as property manager, finance manager, tenant administration, property maintenance and repairs, and so on. REITs must pay for all that activity out of NOI and it is the remaining income that produces actual return on investment.

On top of that, REITs typically run much lower leverage than private owners. This is necessary for them to survive adverse financial events like the Great Financial Crisis and the pandemic.

Putting it all together for REITs, as I did here, the impacts are significant. One ends up with actual cash returns to investors in the ballpark of half of the cap rate (NOI/Property Cost). The ratio is somewhat higher for net lease properties and smaller for office properties, with apartments and shopping centers in between.

To complicate matters further, while some of those cash returns are paid as dividends, others are used to grow those earnings. Later returns purportedly come from growth in value as cash earnings per share increase with time.

But this second part can be disrupted or even reversed by the actions of the public stock markets, which fluctuate quite dramatically. Some former landlords find these fluctuations very disconcerting, and no wonder.

The Worst Case

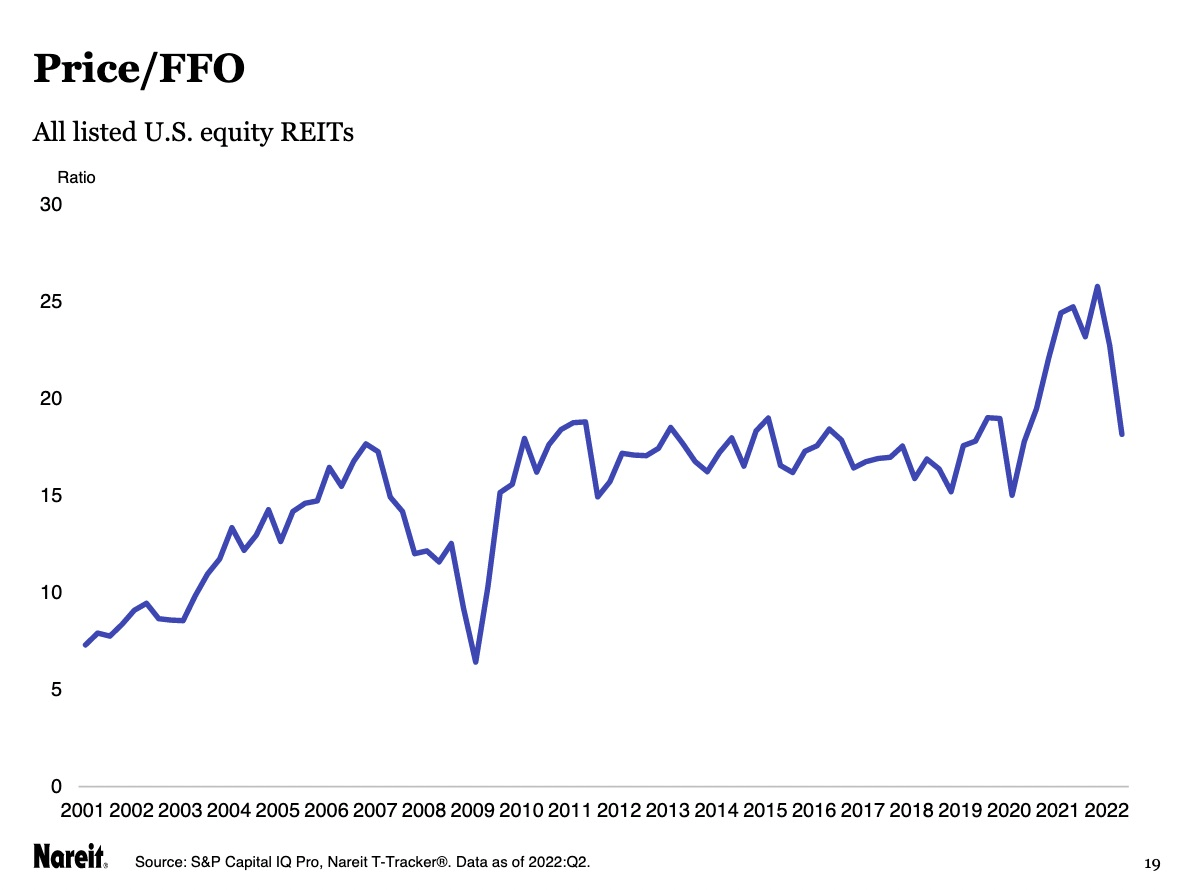

What’s more, the worst case for the market value of cash earnings would not be good. Here is the ratio of Price to per-share FFO from NAREIT. (FFO is a standardized measure of REIT earnings, better than GAAP EPS.)

NAREIT

P/FFO increased from near 10 in the early 2000s to above 20 during 2021. Part of that was deserved; REITs changed in ways that made them better investments.

But part of the reduction in P/FFO was due to the decrease in interest rates, which made distant earnings more valuable. I tried to tease out the relative contributions here.

I’m not predicting a return to a P/FFO of 10. But it could happen, and if it did over 20 years that would represent a 4% per year headwind to REIT stock prices.

Such a development would almost certainly reflect rising interest rates. Nearly all stocks would be affected, not just REITs.

This would pretty much wipe out price gains for REITs, considering the typical growth rates in FFO/sh of 4% that we will see below. Perhaps not entirely, as the likely inflation would produce some earnings increases not seen over the past 20 years.

The idea that growth of FFO/sh will immediately and directly translate into portfolio value increases is not accurate. All you can really count on as a retiree is the dividends, even from the best REITs (or from any stocks).

Principles for REIT Selection

With this bit of perhaps unwelcome context in mind, let’s take up the selection of Go-Fishing REITs. These are, in order, the objectives that make sense to me, followed by brief comments on each of them.

- Superior balance sheet

- Excellent debt management

- Dividend security

- Growth potential

- Favor developers

- Dividend yield

- No preferred stocks

Superior balance sheet: The only thing that has driven any REITs into bankruptcy, to my knowledge, is problems with debt and debt structure. You don’t want debt ratios above 50%, and you want debt maturities either cleared out or very easily covered for the next year and preferably two.

Excellent debt management: You want REITs that operate so that they never need capital. This is explicitly a principle for National Retail Properties (NNN). It may be useful to raise capital but the business model must not require it for survival. On top of that, you desire that the business model will produce growth of dividends even without raising capital.

Dividend security: We want REITs for this purpose who have plenty of excess cash after covering their dividend. Otherwise minor bumps in the road can threaten dividend cuts. In addition, even if such REITs that also meet the standards above are at some point forced to cut the dividend, they will be able to bring it back fairly quickly.

Growth potential: We want REITs with a demonstrated ability to grow per-share cash earnings. Ideally, they should have a long track record of succeeding across cycles.

Favor developers: The most stable, and often the most profitable, growth of earnings comes from effective development. Some REITs, including AvalonBay (AVB), Federal Realty Investment Trust (FRT), and others steadily select locations where they can develop (or redevelop) properties and find strong demand. For such REITs, selling property in locations with high demand and developing new properties there or elsewhere can produce much larger gains than they would get from just increasing rents.

Dividend yield: While yield matters to our target investor, it cannot be high on the list of standards for selecting REITs to own. The yield reflects in large part the current manias of the market. We do like it when we can buy a good REIT that is out of favor. That gets us a larger secure income.

No preferred stocks: Recent years have proven that the much-vaunted investor protections for preferred stocks are in fact easily escaped. What happened in the buyouts of PS Business Parks (PSB) and Cedar Realty Trust (CDR) are examples. There are other weaknesses of preferreds as well. Ask me about them if you like; we have other fish to fry here.

The Primary Candidates

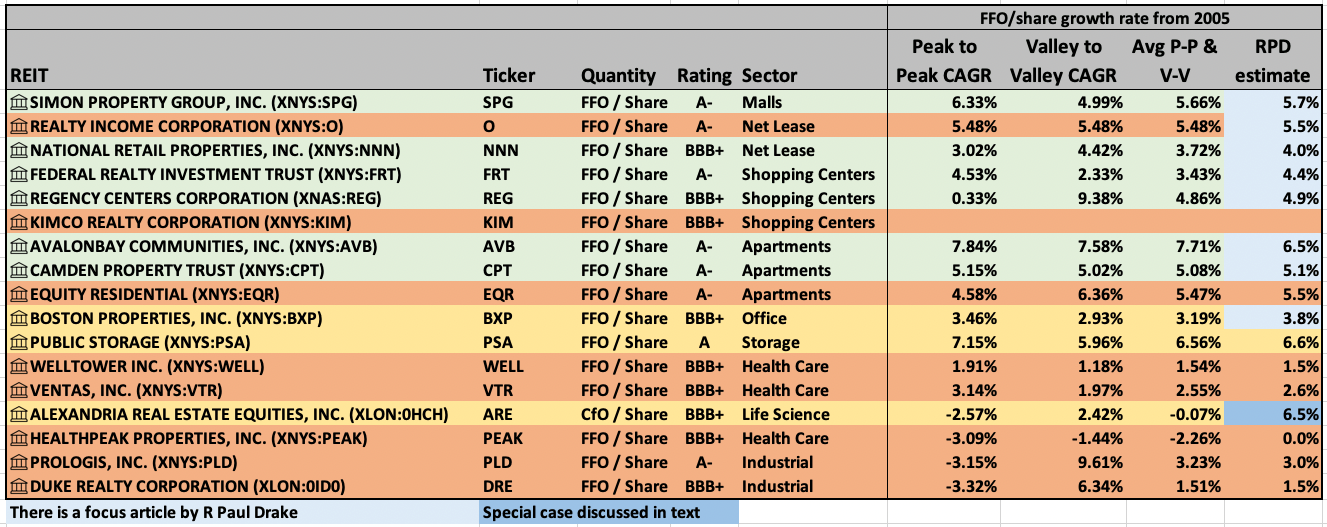

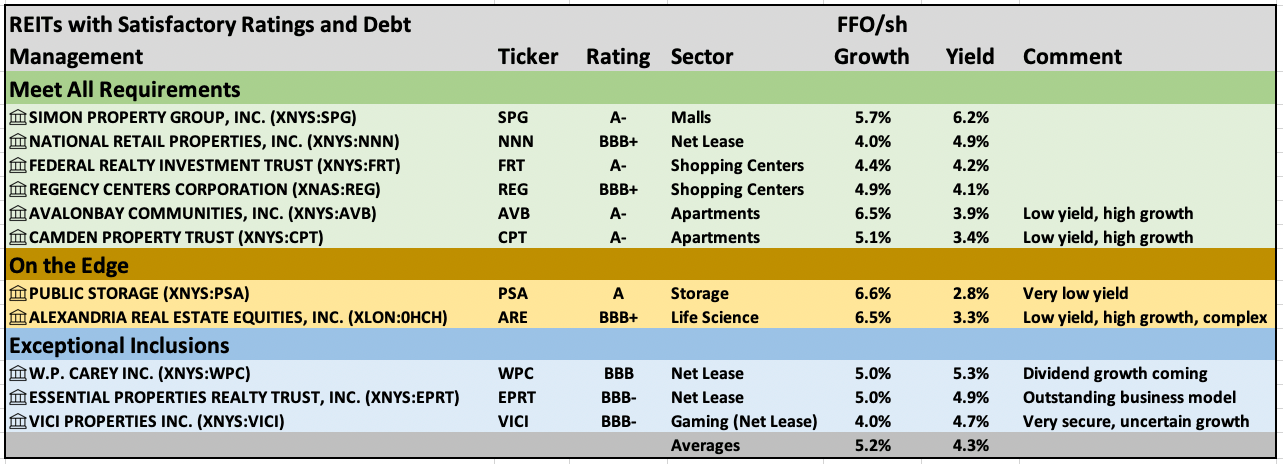

The main candidates for the Go-Fishing Portfolio are those with credit ratings of BBB+ or higher by S&P. We consider other publicly listed REITs below. The highly rated list is shown here:

RP Drake

The table also has information related to growth of earnings measured as FFO/share. We consider this aspect out of order because it is the one that eliminates the most candidates who have high credit ratings.

You can see that REITs from 8 or 9 sectors make the list [depending how you count Life Science REIT Alexandria Real Estate Equities (ARE)]. More than half of the overall REIT sectors have no REITs that make this list.

The rows shaded green show REITs that I consider definitely qualified for the Go-Fishing Portfolio. Gold shows REITs that are on the edge and orange shows rejects. Reasons follow below.

The rows with blue cells show REITs on which I have done at least one focus article. Most of these are public but some may still be exclusive to members of High Yield Landlord [search here by ticker for the public ones].

The rightmost four columns show four values for FFO/sh growth rate. The first shows peak-to-peak rates, typically from 2007 through 2019. The second shows valley-to-valley rates, typically from 2009 through 2020. (These are two meaningful ways to measure wavelike trends.)

The third shows the average of the previous two and the fourth shows my estimate of forward growth. This usually is near the average from the third such column, but sometimes reflects my assessment of details for that REIT.

The major exception is Alexandria. Their FFO/sh growth rates were terrible for much of the past 22 years.

But based on my study of that REIT, they have been on a path of high growth for more than 5 years. Plus they have quite a good moat and also have a Venture Capital arm that is starting to pay off. As a result, my projection is for strong earnings growth, but perhaps I will prove to be wrong about that.

The Rejects

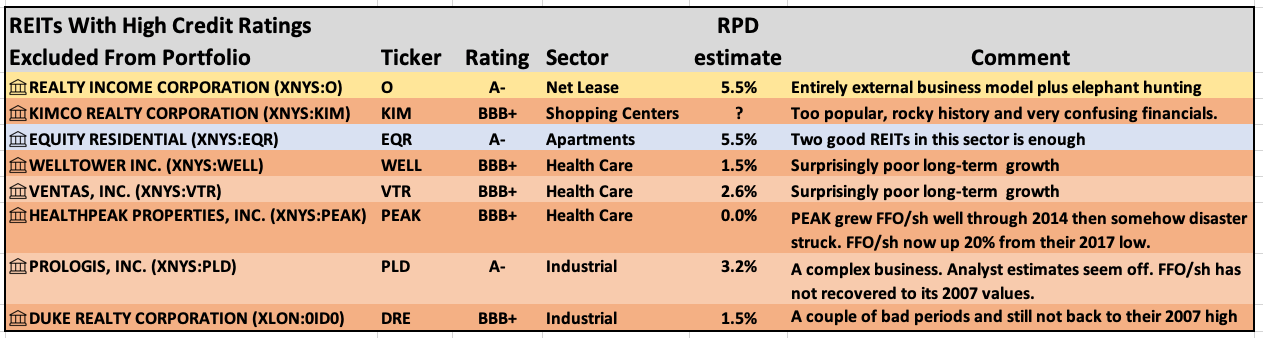

Before discussing the good candidates further, let’s address the rejects. Here is that list, with comments. Some further remarks on some of these REITs follow.

RP Drake

Realty Income (O): Realty income has two weaknesses. First, they operate a business model in which nearly all their growth depends on being able to issue equity and debt at favorable prices. Being able to do this is far from guaranteed.

Second, they have become so large that they cannot operate as they have historically. They have to “elephant hunt,” finding and buying multi-$B portfolios. Their ability to succeed at that, and how much growth per share they get from it, are both uncertain.

Equity Residential (EQR): Equity residential seems a fine REIT but I have not studied them deeply and there are already two great selections in apartment REITs. No objection from me to including EQR if you know them well.

Health Care Sector: This REIT sector seems just plain treacherous. All the REITs in that sector with high credit ratings have a history of low growth of FFO/sh or worse.

To my mind, there are real threats of one kind or another to all segments of that sector except Life Science. This will be a century with massive growth for biotech and bioscience.

Industrial Sector: The two REITs in this sector with high credit ratings both still have FFO/sh below the peak from 2007. My view is that the sector is intrinsically vulnerable to the overbuilding that led to its big crash in the Great Recession.

One might do well with actively monitored investments in the sector. But that is not the point of the Go-Fishing Portfolio.

To complement those shown above, I went through all the publicly listed REITs to see which ones made sense to add. This yielded (only) three, shown below in rows shaded blue.

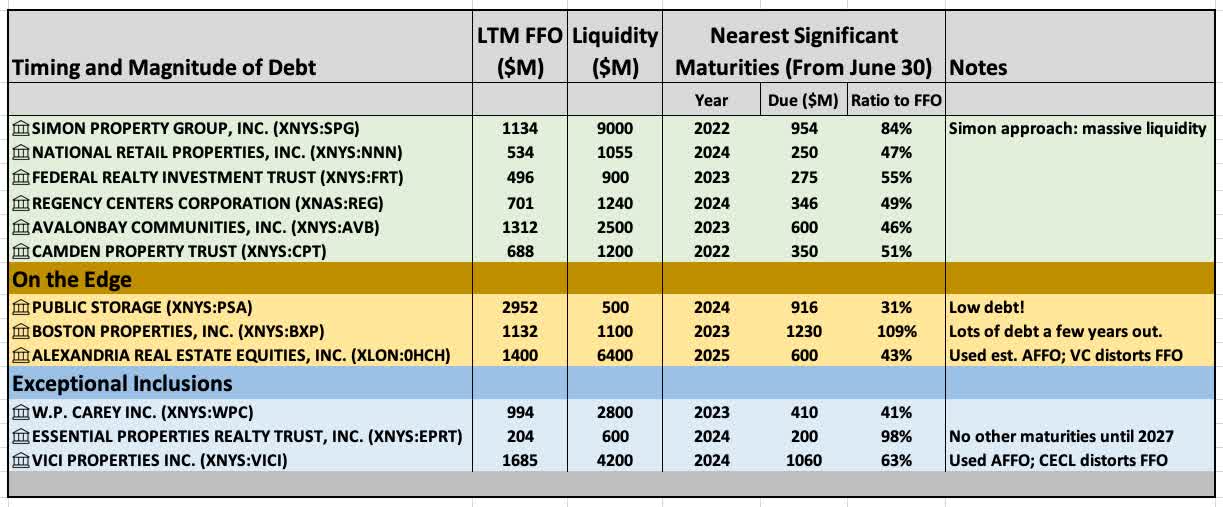

Debt Management

REITs get in trouble related to debt in two ways. First and most often, they violate the covenants associated with their debt. Second, debt becomes due that they cannot pay off or roll forward.

All REITs of interest here stave off the first problem by having low leverage. We will skip a bunch of details about how that can play out.

The best insulation against the second problem is to ladder debt maturities so that near-term years are no threat. The best REITs in this respect have cleared out their debt today so the earliest maturities are in 2024 or later.

Here is how the keepers from above do on that score. Debt numbers are from Q3 SEC filings and usually are effective June 30.

RP Drake

Much of the group has a first major maturity in 2024, and it has a value of about 50% of FFO. This is good. Some comments about special cases follow.

After having been badly burned in the Great Recession, Simon Property Group (SPG) took the path of protecting itself by paying for massive liquidity. Their $9B would cover the debt and keep them going for a couple years even in very severe scenarios.

The liquidity is mainly in a Credit Facility, as is that for most of these REITs. This gives them the contractual right to draw funds on demand for a specified period.

Presumably, this right would keep working during a financial crisis when no one was agreeing to new debt or debt contracts. It has before.

It is disappointing to see the relatively early maturities shown by Camden Property Trust (CPT). They do have plenty of liquidity but still it is bad form.

But so much else is outstanding about Camden that I did not throw them out over this issue. If relevant, you can make your own decision.

Essential Properties (EPRT) is just getting going. They have a large debt maturity, relative to FFO, in 2024. But they have nothing in 2023, 2025, or 2026. They are building out their ladder beyond that with longer maturities.

I expect that to be no problem after credit markets stabilize and have no issue keeping them in the portfolio from this perspective. But an ultra-conservative investor might not want to.

In contrast, Boston Properties (BXP) has a comparatively large amount of debt. And their situation gets worse not better later in the 2020s.

On top of that, I concluded here that office REITs are overpriced in general. So despite admiring many things about Boston Properties, I dropped BXP from the list.

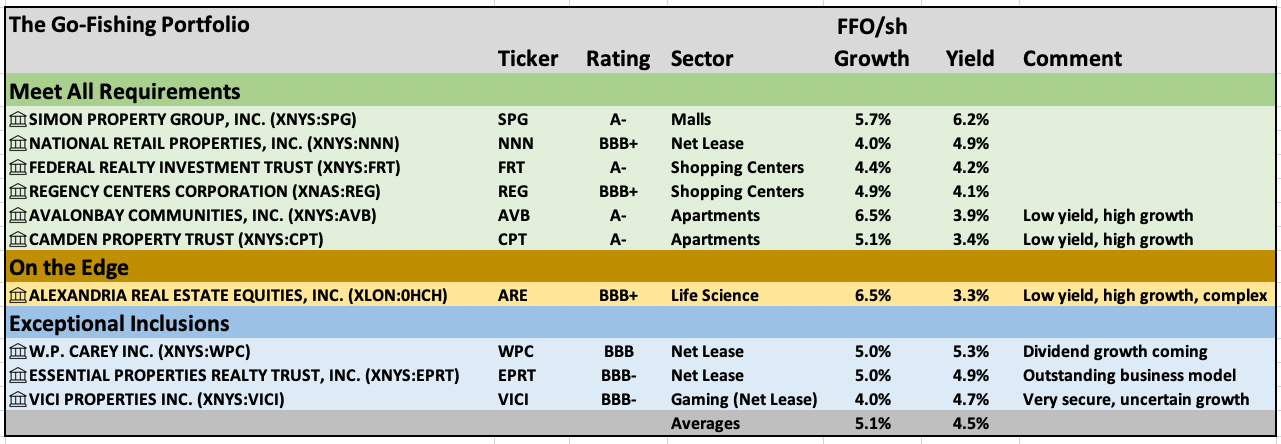

The Good REITs

The next table will show the list of REITs that remain at this point. As before, discussion of some items follows the table.

RP Drake

The first four rows shaded light green show the REITs that are most appealing to me. Simon Property Group, National Retail, Federal Realty, and Regency Centers (REG) all have a long and strong history.

The next two rows show the apartment REITs AvalonBay and Camden, whose issue for me is a relatively low dividend yield. But countering that is their rapid ability to translate inflation into earnings growth.

Alexandria, the only REIT remaining on a row shaded gold, is on the edge because of low yield. They are discussed further below.

Shown on rows shaded blue are the additions based on my broader survey of all publicly listed REITs. Comments on each:

W. P. Carey (WPC): This REIT has nearly completed its transition to a Net Lease REIT with some very positive aspects. But its history is complex, as I covered here, after extensive research. Almost every other article on WPC that mentions history at all gets things very wrong about it.

WPC has some more years of slow dividend growth ahead of it. But that will change, for reasons I discussed here. WPC seems to me an excellent candidate for the Go-Fishing Portfolio.

Essential Properties Realty Trust (EPRT): In my view Essential has the best business model in the Net Lease sector, as I discussed here. Their portfolio is composed of properties that are recession-resistant, e-commerce-resistant, and very fungible.

Essential will prove able to strongly grow their dividend in most circumstances and to sustain it through even deep recessions. That said, Essential is relatively small and new, so included them or not at your discretion.

VICI Properties (VICI): This REIT is incredibly stable since they own major casino properties. Their credit rating seems likely to keep moving up. And they have governance and transparency that is one of the best amongst REITs.

But VICI got very big very fast and now they have to elephant hunt to grow. This may threaten their lofty aspirations for rate of growth. Still they seem to me an excellent choice for this portfolio.

A few notes concerning our other objectives:

These 11 REITs all have secure business models. They retain enough earnings to handle bumps in the road.

Overall, aside from the Net Lease REITs (including VICI), these REITs are all active developers. For most of them it is at their core.

As to dividends, no dividend is absolutely secure and it seems silly to me to obsess about that. But REITs with strong cash flows can rapidly pull back up any dividend that had to be cut. We’ve seen that recently from Simon and Regency.

As you can see in the table, the average dividend yield of the group is 4.5%. That said, the 2.8% from Public Storage (PSA) strikes me as just too low in the context described above. So drop them too.

That leaves us with the ten REITs in this table. I would include no others.

RP Drake

The average rate FFO/sh growth anticipated is 5.1%. The important part of this is that FFO/sh growth will support dividend growth. The average yield is 4.5%.

Time to Go Fishing?

Assembling a portfolio with these 10 REITs would provide dividend income above 4% that likely would grow at a rate above inflation. The growth would not be steady and there would be years like 2022 when inflation exceeded the growth of dividends.

The average US inflation rate over more than a century is 3.1%. The average for the next 20 or 30 years could be larger, but that is not my own expectation.

I would not hesitate to hold these REITs with the intent on checking in on them once a year. But that is speculative as I am not there yet. You get to make your own decisions.

Personally, I would also add some energy midstream companies to an overall Go-Fishing Portfolio. There are not many that seem to me to amply meet the objectives laid out above. Three that do are:

- Enbridge (ENB): Canadian, issues 1099

- Enterprise Products Partners (EPD): USA, issues K-1

- Kinder Morgan (KMI): USA, issues 1099

Going the directions described above would let you escape the “flat decades” one sees in the S&P 500. From the current historical chart the next one of those seems likely to start soon, or maybe it already has.

Index investors will have to worry about whether gains in the S&P 500 will keep up with their needs. In contrast, investing in firms with dividends like those discussed here sounds really good to me.

Be the first to comment