stockcam/iStock Unreleased via Getty Images

My kids communicate with friends on Snapchat, and it is one of the most popular interactive social media applications on the market. Unfortunately for shareholders, Snap Inc. (NYSE:SNAP) has struggled to earn a profit, more focused on user and sales growth over the years. The good news is profitability has started to appear in 2021-22, while a crash in Big Tech pricing since autumn has scared away buyers. These two factors have combined to create a superb buying opportunity in Snap’s unique new-age media assets. In fact, I will argue this equity trades at its lowest valuation since becoming a publicly-traded enterprise. If you have ever wanted to scoop up ownership in a high-growth media/social app, but been reluctant to jump in because the investment math didn’t make sense, you now have your chance.

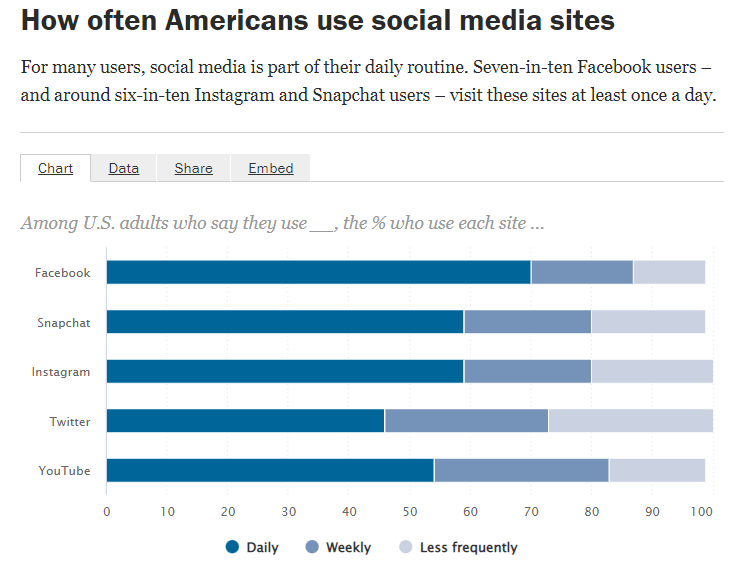

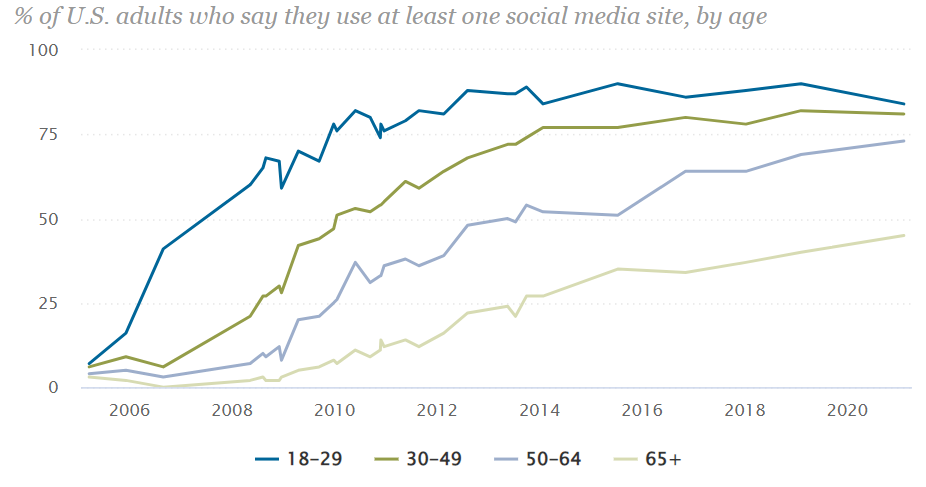

April 2021 Article, Pew Research Center April 2021 Article, Pew Research Center

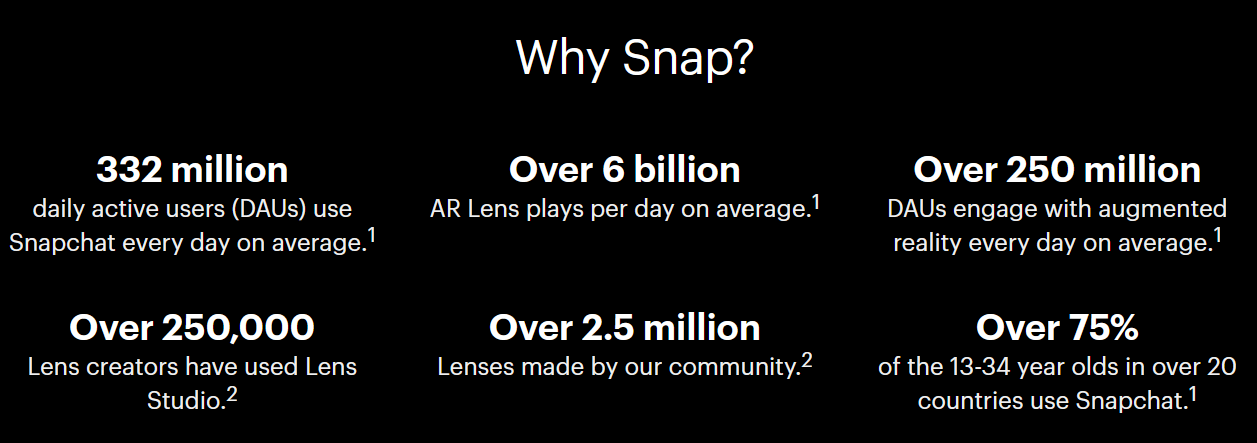

What makes Snap unique? That’s a great question. I think it emphasizes fun over information, with the use of smartphone cameras. If you will, it’s a cross between the video and picture entertainment of TikTok, the friends and family updating feature of Facebook owned by Meta Platforms (META), and the information sharing of Twitter (TWTR). Youngsters love it, and international growth is just now taking off outside a handful of established western-leaning nations. Adding goofy, cartoonish pictures on top of your photos is just the tip of the iceberg to get new users to download the app. Company sales are centered around advertisements, many of them streaming videos/commercials.

Snap Website Snap Investor Relations Website Q1 2022 Earnings Presentation Q1 2022 Earnings Presentation Q1 2022 Earnings Presentation

Wicked Stock Price Crash

I personally had no interest in Snap a year ago, when it was trading at truly ludicrous valuation levels. The present investment opportunity for shareholders wouldn’t be possible without the mindless selling of Snap’s stock since its last earnings report, on mildly reduced growth expectations. Price has declined another 50% over just a few short weeks, after months of heavy liquidation.

Below is a 3-year graph of the amazing bull phase in consumer and investor interest during the stay-at-home pandemic period of 2020-21. Then, we can review on a 12-month chart the stock price dump since September 2021 (from $84 a share), with a close-up of positive bottoming action appearing in several important momentum indicators.

On a longer-term chart, the noteworthy indicator to contemplate is the 14-day Average Directional Index reaching an extended and clearly oversold number above 50 the last couple of weeks. Circled in blue, both today’s score and the last instance of intense selling in March 2020 at the pandemic bottom are highlighted. From my experience, this indicator at a minimum is screaming to expect a large bounce in price closer to $20 by year’s end.

3-Year Chart, Daily Values, with Author Reference Points – StockCharts.com

More reason for optimism, two of my favorite momentum indicators, On Balance Volume and the Negative Volume Index bottomed in May. If these lows hold, I would hazard to guess a building pattern has already begun for shareholders. The OBV low circled in green and NVI setup circled in red are now diverging in a bullish manner for the first time during the massive selloff of 2022. Does this condition guarantee a price bottom is at hand? Not absolutely, but the odds are increasing a great buy opportunity is now present from a technical perspective.

1-Year Chart, Daily Values, with Author Reference Points – StockCharts.com

Vastly Improved Valuation

Today’s $12 stock quote is similar to the level of early 2019, but the company is considerably larger and entering profitability for the first time. If you considered the setup as a buy proposition three years ago (and it was), the current situation could be categorized as a true Big Tech bargain. The underlying fundamental numbers make so much more sense to me, I find it reasonable to project a double or more is coming back to $25 sometime in 2023. Here’s why.

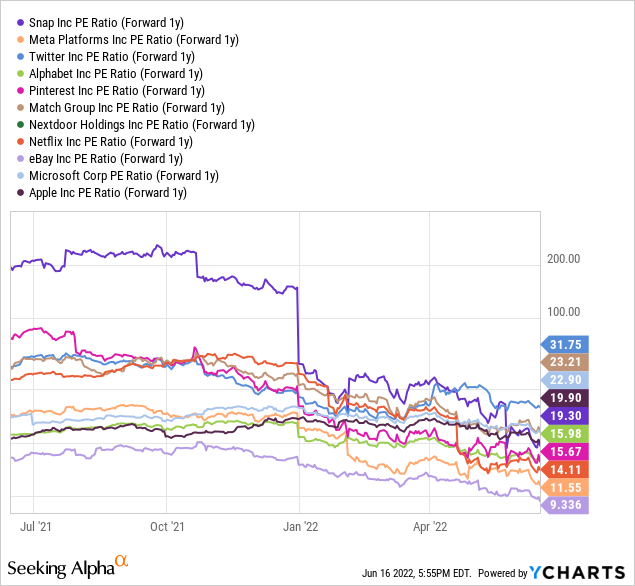

First, gross margins at Snap have been growing rapidly since 2019. Presently, profit potential is entering the mid-point for social media competitors, while resting on the upper end of Big Tech peers generally. Below I have Snap gross margins pictured against social media giants Meta Platforms, Twitter, Alphabet/Google (GOOG) (GOOGL), Pinterest (PINS), Match Group (MTCH), and Nextdoor Holdings (KIND), plus media/online marketing/computer tech peers Netflix (NFLX), eBay (EBAY), Microsoft (MSFT), and Apple (AAPL).

YCharts

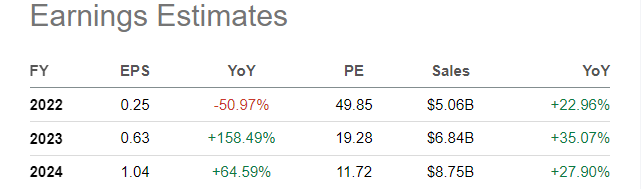

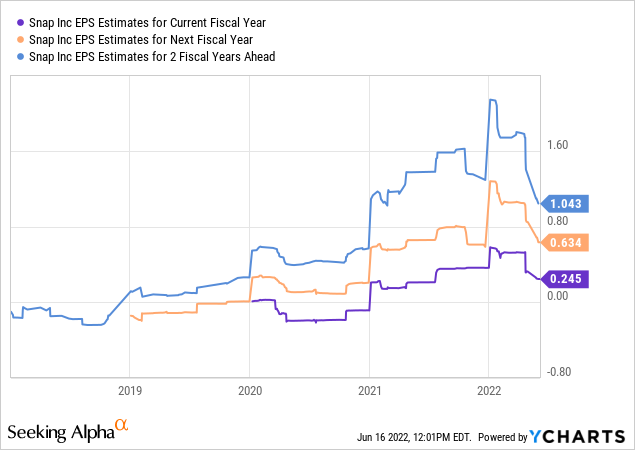

Snap has focused all operating cash flow, debt issuance and equity raises on growing sales and reach rapidly. As a consequence, overall profitability has lagged. Honest income is just now beginning to enter the fundamental equation. Wall Street analysts are looking for cash-based earnings of $0.25 per share this year, rising quickly to $1.04 in 2024.

Seeking Alpha, Analyst Consensus – June 15th, 2022 YCharts

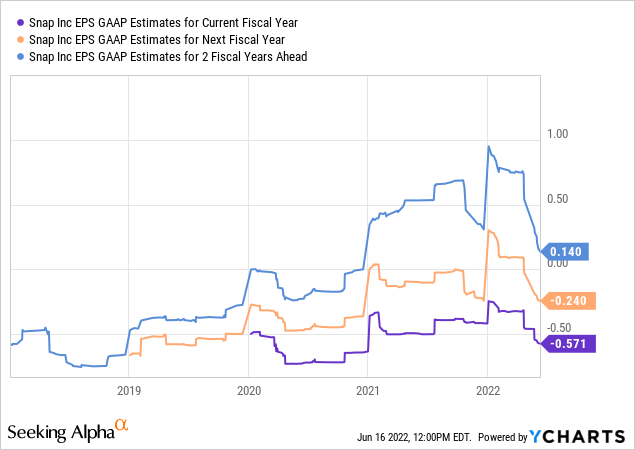

On top of the expected growth in cash earnings, GAAP income is expected to be positive in as little as 18 months.

YCharts

You would think all the positive news on earnings improvement would mean Snap’s valuation on sales and book value is reaching for a high point. Alas, the technology bust of 2022 has pushed the stock to a record low setup vs. trailing sales and accounting book value. Measured from the middle of 2021, the stock’s underlying valuation on these two metrics has fallen a mindboggling 90%!

YCharts

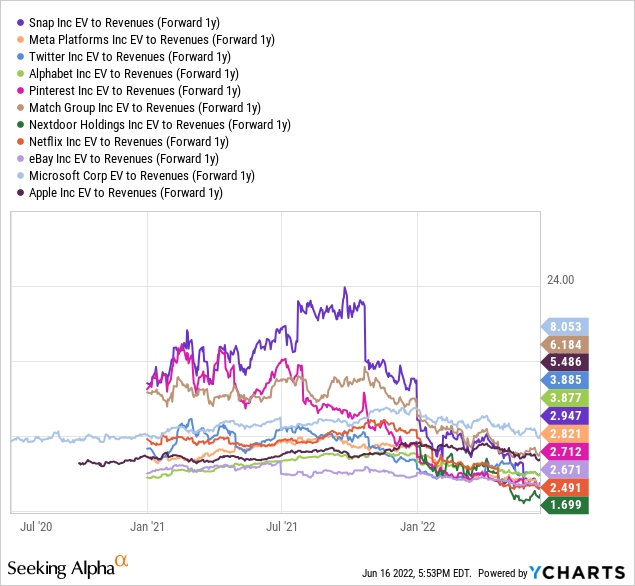

All told, if the company continues its growth ramp as predicted by analysts, total enterprise value (equity capitalization plus debt, minus cash) vs. revenues estimated for 2024 is at a super-low 2.9x ratio. This multiple is in the middle of the competitor and peer pack today, well under its 24x score of September 2021. Believe it or not, the S&P 500 index overall is trading around 3.0x EV to revenue projections for 2024.

YCharts

Lastly, and perhaps most importantly, a forward 1-year P/E of 19x is incredibly cheap vs. EPS growth rates above 50% annually starting in 2023. Note: I am also bullish currently on the lowest forward P/E Big Tech ideas I can find. I have written buy suggestions on eBay here, Meta Platforms here, Google here, and Netflix here in the spring and early summer.

YCharts

Final Thoughts

The company holds $5 billion in cash ($6 billion in total current assets) vs. $5.4 billion in total liabilities. Operating cash flow is accelerating and cash earnings are rising fast. In terms of liquidity, Snap has never been in a better position to fund growth internally, without help from Wall Street bankers or dilutive security issuance. However, many market players are incorrectly assuming Snap will be a money-losing operation into the future, like past years. This misconception best explains why the stock has become so cheap. Investors have sold everything in tech, especially companies viewed as needing external funding to grow.

Exaggerated fears of a recession and its effect on the ad marketplace are other excuses for bears to growl loudly. Granted online advertising sales are in decline, at least vs. elevated projections for 2022, but high Snapchat user growth rates help to offset the impact.

Snap looks to have entered a rare “undervaluation” setup that may not last very long. If the U.S. equity market and economy do not collapse from spiking interest and inflation rates, company growth rates should support a rising share quote in time. I have a target price zone of $25 to $30 in 12 months for a fair valuation on all the moving parts.

When you think about potential business scenarios for investors, Snap is definitely a takeover or combination candidate under $20. A variety of Big Tech names might be interested at a low price.

If you can purchase shares under $13 in the coming days, I would qualify such a price level as Strong Buy territory for a rating. Quotes all the way up to $20 still offer a solid Buy entry proposition. For sure, volatile swings in price are the new norm for a while. One way to reduce risk in a bottom fishing expedition is to spread out your buy orders for a full position over three or four months. The current bullish setup is the exact opposite of the bearish valuation story a year ago. Failing to buy Snap at $12 may prove just as painful to brokerage account value as refusing to sell around $80. Timing matters, and so does intelligent capital allocation when the valuation math says jump. I do not expect this extraordinary buy opening to linger for procrastinators.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Be the first to comment