Byrdyak

It has only taken roughly two days of trading to wipe out all of the gains since Jan. 10. Many investors appeared to be under some belief that the bear market was over and that a new bull market was here for whatever reason – take your pick.

Unfortunately for the bulls, this continues to be a bear market. The biggest reason is that the Fed wants monetary policy to be restrictive and for financial conditions to be tight. Sure, the inflation rate is coming down, but the labor market is still hot, and at least, based on the latest data from the Atlanta Federal Reserve, the economy is still growing at an above-trend pace.

Now that the Fed has seen signs of inflation coming down, they can slow the rate hikes, but that doesn’t mean they are done hiking. Because the Fed also knows that a tight labor market can lead to wage inflation, which leads to other forms of inflation.

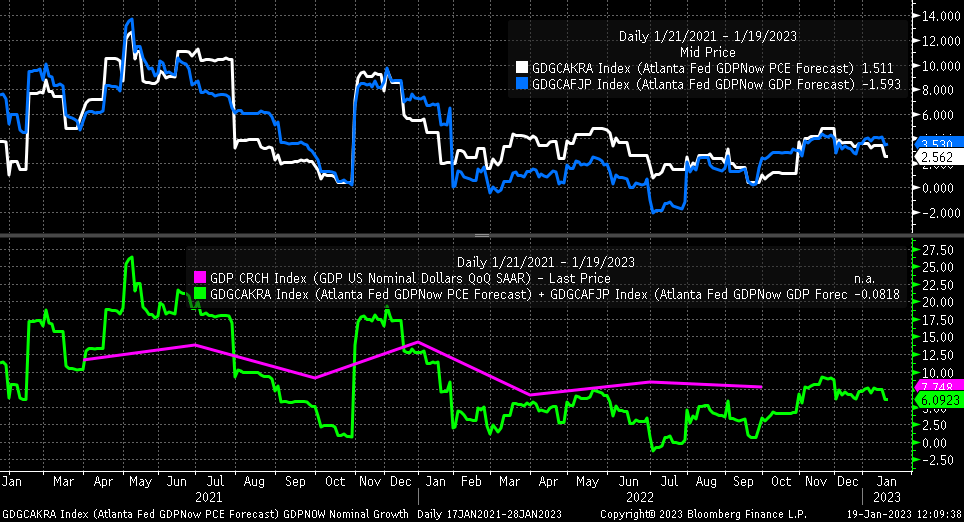

But moving away from inflation, the economy is surprisingly holding up quite nicely, based on the Atlanta Fed’s GDPNow model, which shows the fourth quarter growing at 3.5%, and PCE at 2.56%, which suggests a nominal growth rate of around 6%, which is a very healthy nominal growth rate all around.

Bloomberg

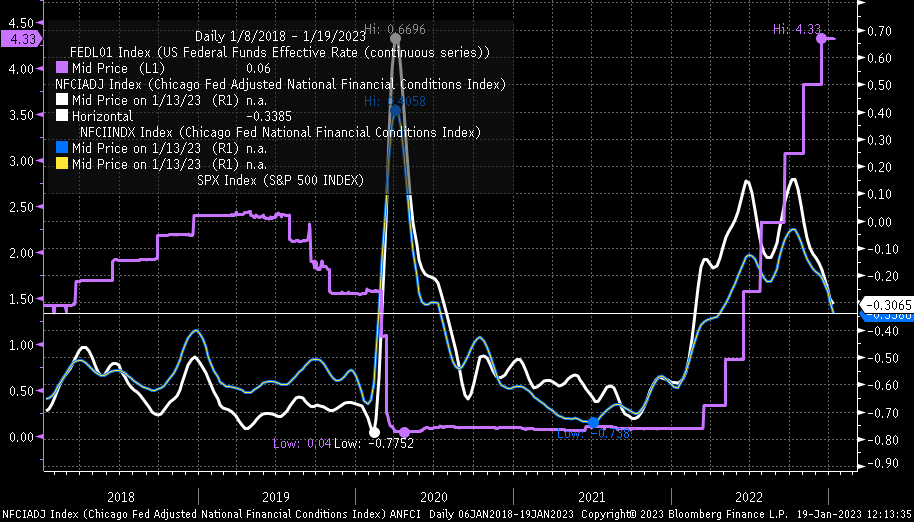

On top of that, financial conditions have eased back to levels last seen in the spring of 2022, when the Fed first started to increase rates. It tells us that financial conditions are nowhere near restrictive levels. It suggests financial conditions are accommodative and aid in supporting the economy.

Bloomberg

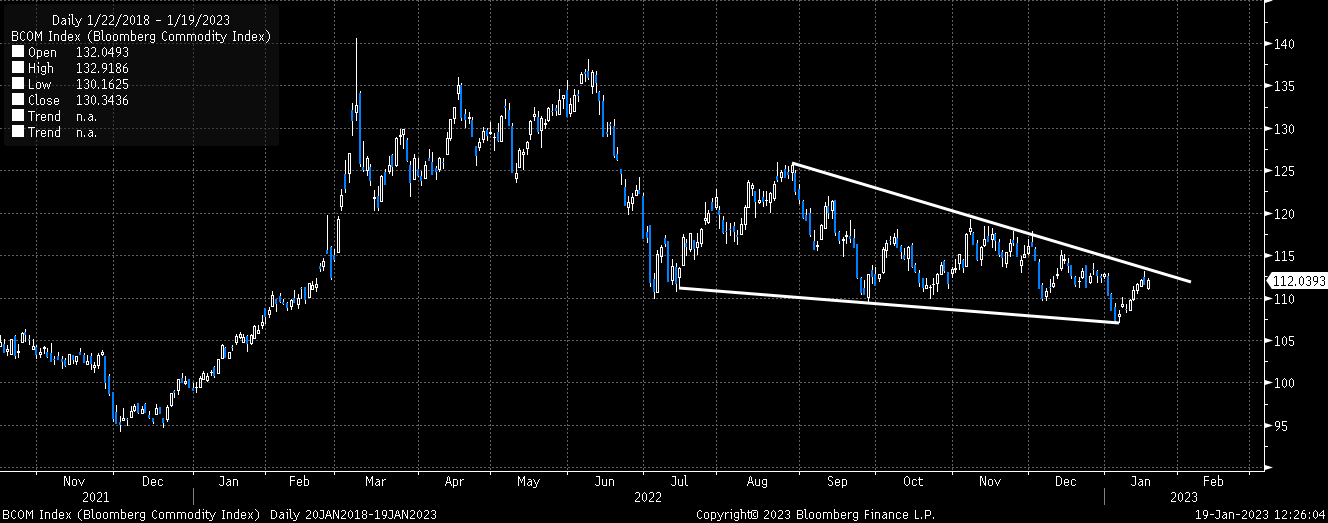

This is happening with the added help of China re-opening trade, pushing prices even higher for copper, gasoline, oil, iron ore, and many other commodities. The Bloomberg commodity index is on the rise and, from a technical standpoint, looks bullish and could be on the cusp of rising sharply.

Bloomberg

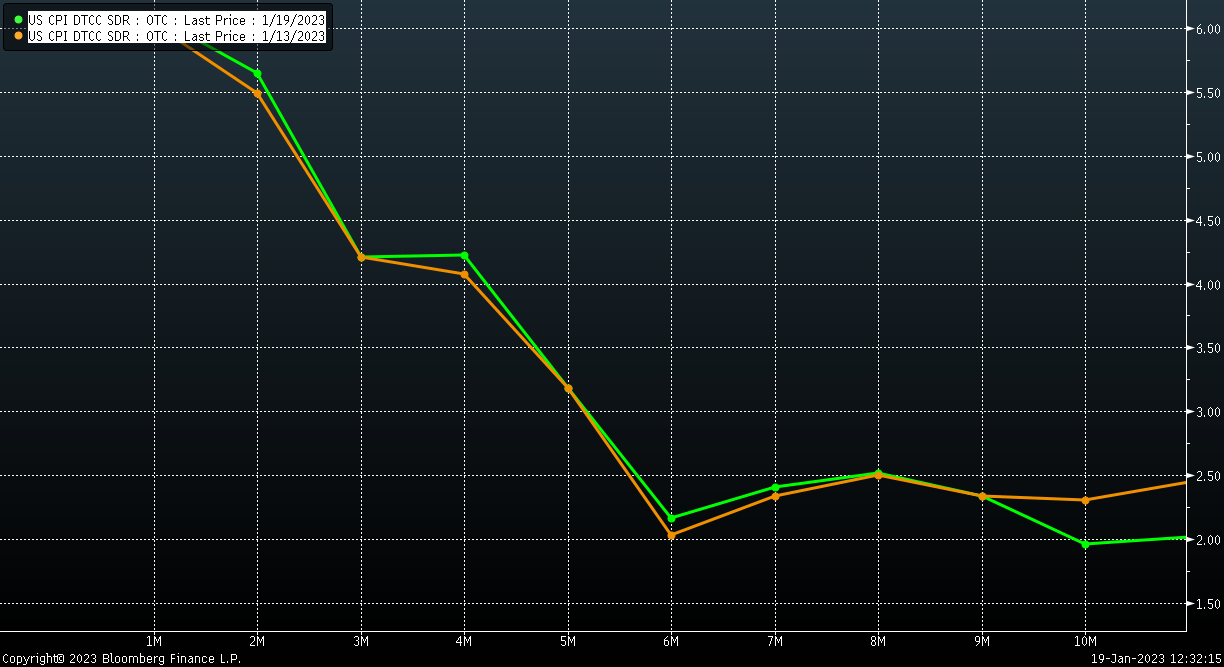

The shift in commodity prices could be why we are now seeing inflation swaps beginning to creep higher since last’s week CPI report. These are minor moves at this point, but the higher commodity prices rise, the more likely it is that inflation expectations will continue to rise.

Bloomberg

But this isn’t the Fed’s fault – the Fed has made quite clear over and over again that rates are to go higher and stay high for some time to come. As long as the market allows financial conditions to ease because the market gets this idea that the Fed will pivot, this cycle will drag on. The most significant contributor to the recent rise in commodity prices has been the dollar’s recent decline. It was back in September when I noted that A Weaker Dollar Could Be A Disaster For Stocks. To no surprise, a weaker dollar has worked to push commodity prices higher, and well, here we are with the cycle starting all over again.

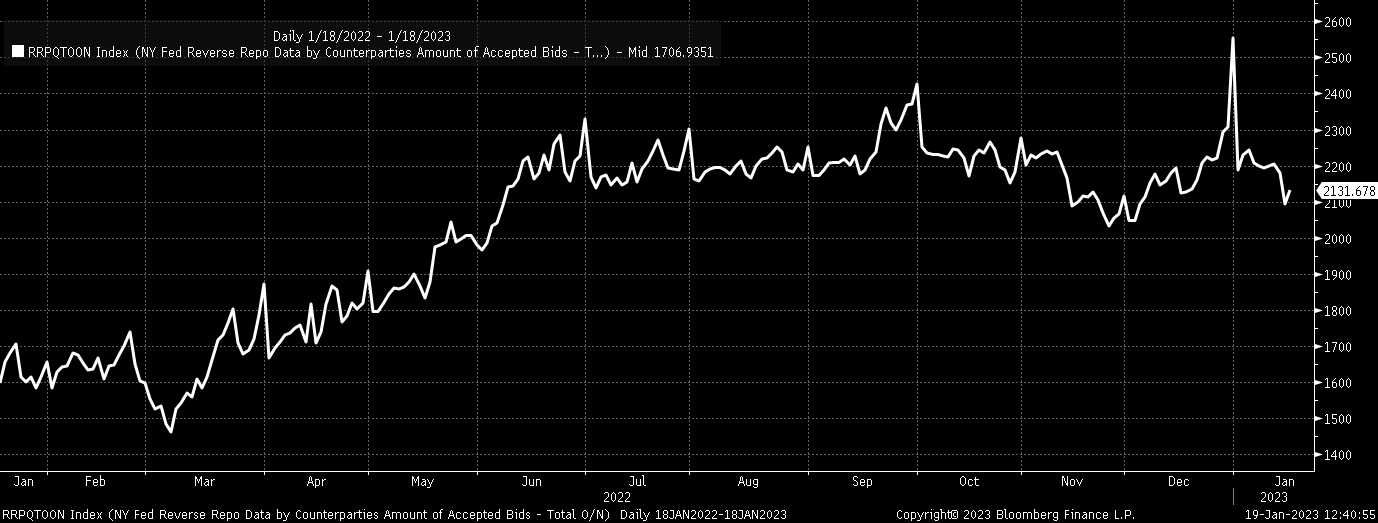

This idea investors get about a new bull market being born at this point in the game is premature. This isn’t 2020 – the Fed isn’t going to start cutting rates to 0% and printing $120 billion a month anytime soon. Based on the size of the Reverse Repo Facility, the Fed still has $2 trillion too many floating around in the system with nowhere to go.

Bloomberg

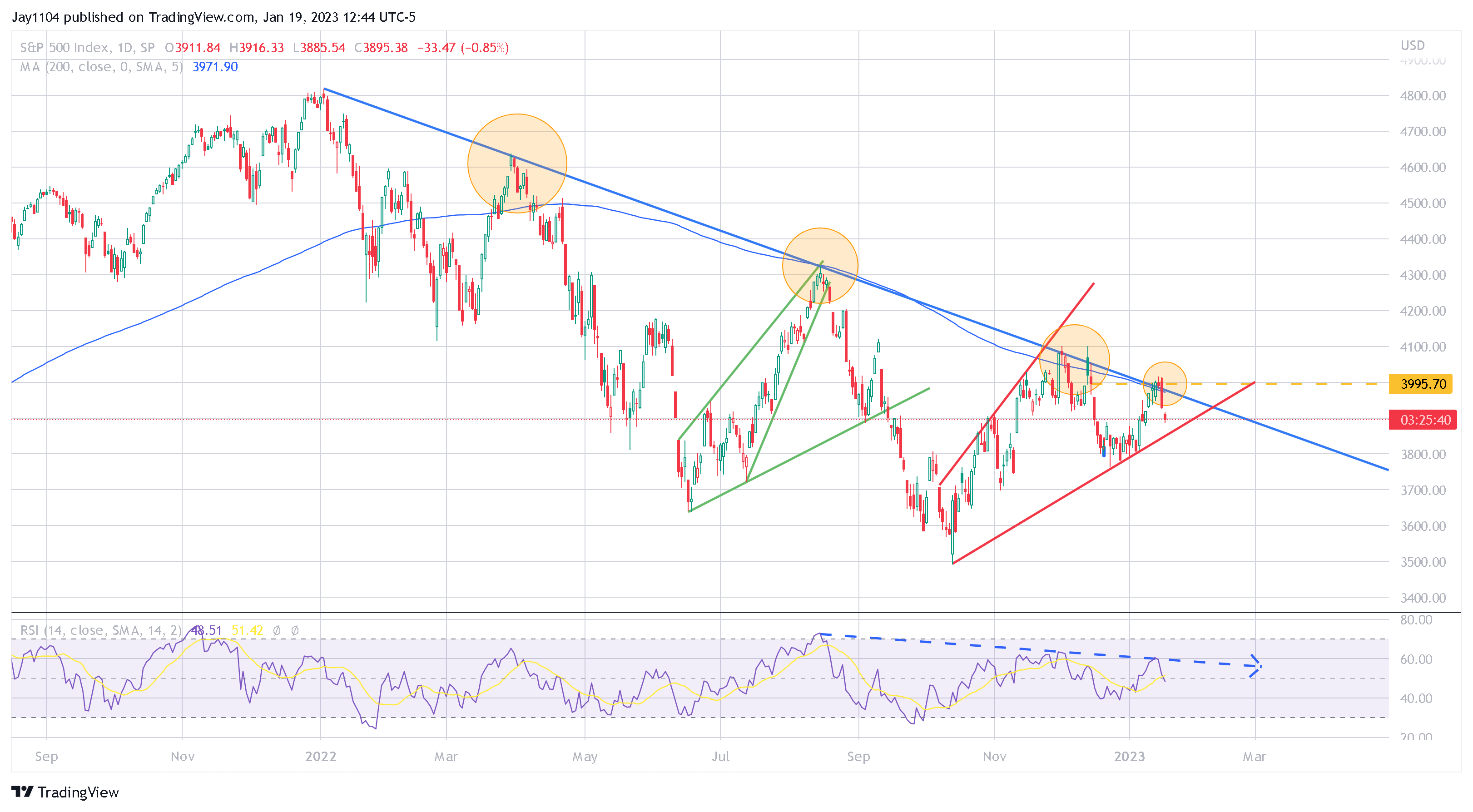

Front running the Fed hasn’t worked on the prior three occasions, and it doesn’t seem like it will work on this fourth occasion. Because what will probably happen, at this point, is that the Fed will get financial conditions to begin tightening again, and they have plenty of tools to jawbone the market to where they want it to go.

TradingView

Front running the Fed hasn’t worked out well the last three times and probably won’t be the fourth time because a new bull market is probably a long way off.

Be the first to comment