Joe Raedle/Getty Images News

The following segment was excerpted from this fund letter.

TPL Announcement

On May 16th, Texas Pacific Land Corp. (NYSE:TPL) made what might appear to be a modest announcement: a strategic alliance with two cryptocurrency mining companies to develop a mining operation on some of TPL’s land. It might easily be disregarded as of little importance — unless one properly appreciates the economic value of the company’s land position, to which investors still pay insufficient attention.

Readers of our quarterly reviews might recall an occasional mention that TPL’s land will ultimately be worth even more than its oil and natural gas royalty interests. That might sound odd, since the earnings are so obviously dominated by its oil and gas royalties. Land, though, unlike almost any other business asset, whether a commercial building or a manufactured product or process, is a perpetuity. Almost anything else wears out, or can become displaced or, in the case of most natural resources, depleted. Even very long-lived resources.

Land must be more valuable, because, in contradistinction, it is a perpetuity. And it can’t be replicated. More than that, it’s an increasingly scarce resource, at least on a per-capita basis, since the world continuously becomes more populous. There will be better-use/higher-value purposes to which some tract or lot can be put. That use might be known or speculated about in the present, or it might not be known until, at some future date, circumstances allow. It is easy to underestimate the value of a very long duration asset, and a perpetuity is the longest.

Investors also tend to not give sufficient credit to the power of management to enhance or create additional value with such an asset. The commercialization of land requires considerable management expertise. This particular transaction involves two other parties that will build and operate up to 60 megawatts of bitcoin mining, which was stated could accommodate up to 2.0 Exahash of operational capacity.

That is quite sizable. As a reference point, Marathon Digital Holdings (MARA), which has a $1.0 billion stock market value, even after a year-to-date decline of 70%, had about 3.6 EH/s of capacity at year-end 2021, though it expects to reach 13.3 EH/s during this calendar year. The TPL venture is expected to begin operations in the fourth quarter of this year.

Where does that much electric power for such a large project come from that quickly? Though not necessarily common knowledge, there is a great deal of both excess energy and produced electric power available in the U.S., at least in geographically or temporally (i.e., hour-of-day) localized ways. One of the two venture partners, Mawson Infrastructure Group (OTCQB:MIGI), establishes mining facilities close to renewable energy sources, using modular, scalable facilities, as opposed to the conventional large, fixed-location data-center type buildings. The other, JAI Energy, specializes in using stranded power assets, flared gas and other sources of excess or ‘wasted’ energy, such as occur when there is insufficient infrastructure or take-away capacity. JAI constructs mobile natural gas-powered generators and mobile mining centers in truck-borne containers.

Much of the power for cryptocurrency mining is now generated by energy that would otherwise be lost, as when electric utilities have excess power during low-demand periods, such as the late-night/early morning hours. These have become very constructive relationships, because crypto mining demand can be uniquely helpful, both to electric utilities and renewable power projects, and in reducing greenhouse gas emissions. Those mutual benefits, and the profit opportunity, though, cannot be fully appreciated without some knowledge of how power generation – in this case, the Texas power grid (ERCOT) – works.

In the joint venture announcement, Mawson Infrastructure announced an intention to participate in “demand response programs” and to evaluate “behind the meter renewable solutions.” “Demand response” is a critical practice for power grid integrity, whereby marginal high-demand power customers are willing to curtail use during periods of peak grid load. As an example, such a user can limit or completely cease power use during an extremely hot summer day, in order to ease the burden on the overall grid. Of course, they will be compensated at the market rate for power generation for doing this, but crypto mining is uniquely able to go offline, and restart with minimal economic consequences. That’s because a cryptocurrency miner that can simply pick up at the next “block” after being powered down. Compare that faculty against a conventional data center (think Cloud – Amazon Web Services, Microsoft Azure) or a heavy HVAC system that take tremendous resources and time to start up and wind down. Thus, these mobile mining operations can both consume excess power during normal periods of electric power redundancy, but also provide a market balancing benefit during periods of grid strain.

“Behind-the-meter” renewables are essentially solar and wind generation facilities that have a direct demand source or customer and do not plug into the broader power grid. In this case, consider a solar facility co-located next to a crypto mining operation, with its power directly connected to the mining facility. Here is where the full loop closes: these facilities reduce power costs for miners during normal (redundant) power supply environments, but allow the renewable energy facility to supplement the grid during periods of extreme grid strain. In this sense crypto miners promote renewable generation that, because of their intermittent periods of production, would be uneconomic without a dedicated buyer.

In the Permian Basin, cryptocurrency mining can make use of flared gas, for instance, converting much of it into an economic asset. There is clearly much scope for such mutually constructive (energy producer, miner, greenhouse gas emissions reduction) activity, whereby miners can convert momentary excess power that would not otherwise be utilized into a permanent financial asset. This faculty of mining has been termed an ‘economic battery.’ It appears that this venture will focus, at least initially, on excess power from the electricity grid. There are large transmission facilities with substations located in Western Texas, one of the types of infrastructure the company has sought to encourage on its surface acreage. Apparently, there is a great deal of electricity moving from this region eastward, but with little offtake demand, such that the excess load (no sunset provision for the law of supply and demand) results in lower electricity pricing than elsewhere in the State.

For TPL specifically, its surface land portfolio consists of 880,000 acres strategically dispersed throughout the Permian Basin. It also owns perpetual gas and oil royalty interests beneath nearly 500,000 acres, equivalent to 23,700 net royalty acres. The “net” in net royalty acres refers to the percentage interest TPL has in a given mineral deposit. For instance, TPL has a 1/128th royalty interest on 85,000 acres (separate from its 1/16th and 1/8th interests on other acreage), which results in 664 net royalty acres. Consider that its oil and gas revenues derive from a very modest portion of its net royalty acres. Only about 12% of the estimated total wells on those 23,700 net royalty acres have been drilled.

The assembly of the requisite quantity of mining trailers and natural gas generators for the project can hardly be expected to occupy more than several acres. Yet, irrespective of precisely how many acres that might be, one can contemplate the ultimate long-term earnings potential from the de minimis, rounding error land usage that enables a 60 MW mining operation. Consistent with its traditional business model, TPL will be taking a net royalty interest in this venture, which requires no capital outlay or operating expense obligations, along with an option to acquire an equity stake.

It bears mentioning, in the context of value creation with a land asset – think of a deal to build a convention center on a previously empty downtown lot – that the value is created when the deal is signed. The value realization does not await the placement of the last girder or pipeline or wire. This announcement in particular is no different. Obviously, if it is economically productive, many more such ventures are likely.

TPL’s Land, Generally

As an aside, there is a different way to think about TPL’s land value. It is an accident of the particulars of GAAP accounting standards in the U.S., that land is held on the balance sheet and not revalued or marked to market each year. In other jurisdictions, the annual changes in land value are accounted for and reflected in earnings. What if TPL’s earnings were to reflect – at least from an investment valuation, if not an accounting, perspective – the ongoing appreciation of its land portfolio? This crypto mining venture is plain evidence of the ability to extract a different type of royalty interest from its land.

TPL provides annual data on the sale and purchase of land, separate from any mineral or royalty interests. It can be quite uneven from year to year. Over 90% of its acreage is grazing land. On the other hand, some small parcels might be priced quite high and not representative of the balance, such as for building lots near El Paso, or for sales to industrial buyers, like E&P or mid-stream pipeline companies. Nevertheless, the pattern of rising values for non-royalty acreage is plain to see:

Land transactions, by year, average approximate value per surface acre:

2021: sold 30 acres, $25,000/acre.

2020: sold 22,160 acres, $721/acre.

2019: sold 21,986 acres, $5,141/acre, including 14,000 in Loving & Reeves Counties at $7,143/acre Bought 21,671 acres (Culberson, Glasscock, Loving and Reeves Counties), $3,434/acre. 2017: sold 11.02 acres, $20,000/acre. 2016: sold 775 acres, $3,803/acre

2015: sold 20,941 acres, $1,080/acre

2014: sold 1,950 acres at $1,897/acre

2013: sold 10,399 acres, $617/acre

From approximately $1,000/acre in the 2013 to 2015 period, large sales in the 2017 to 2021 period were in the $3,500 to $7,000 range, with smaller transactions in the $20,000 range.

A less company-specific, more categorical measure of land values in TPL’s portion of Western Texas is provided by the American Society of Farm Managers and Rural Appraisers, the Texas Chapter of which recently published the 2021 edition of its Texas Rural Land Value Trends. For what they term the TransPecos portion, which encompasses seven counties in the most active drilling areas (such as Loving and Reeves Counties), transactions in “rangeland” were valued at $275 to $640 per acre, whereas Rangeland Special Purpose (such as for compressor stations or tank farms, which is to say industrial use), fell in the $4,000 to $4,500 range.

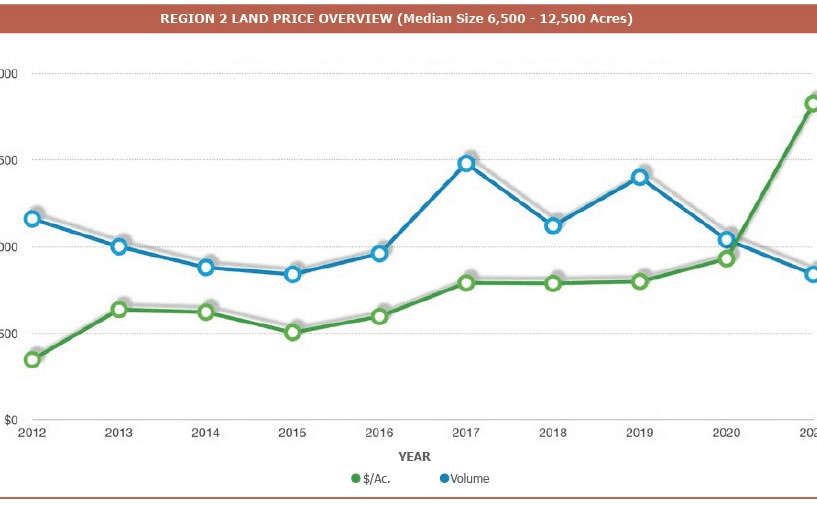

The publication also reports historical trends, with a median price for sales of surface acreage (with a median transaction size of 6,500 to 12,500 acres): this has trended upward from about $400/acre in 2012 to roughly $1,900/acre in 2021. Based on these aggregate figures alone, the land values have been rising at double-digit annualized rates.

Source: American Society of Farm Managers & Rural Appraisers, Texas Chapter, 2021

Simplistically, as an exercise just to test the degree of valuation influence, and using round figures for ease, let’s just say that the TPL surface acreage is worth an average $6,000/acre. The total value for its 880,000 acres would be $5.3 billion, which is one-half of the company’s current $10.6 billion market cap. What if the value of the acreage were to rise by 10%? Inflation is already at 7%-plus, and there is more and more commercial activity in the Permian Basin, including for utility-scale solar and wind projects. The region seems unusually attractive for that use. That would be a value increase of $530 million. If viewed as part of comprehensive earnings, that would double TPL’s total revenues of the last 12 months.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment