JHVEPhoto/iStock Editorial via Getty Images

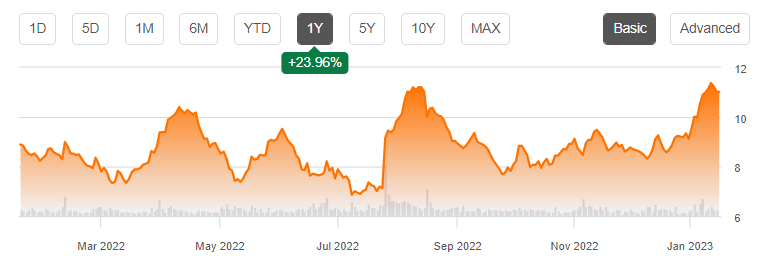

Teva Pharmaceutical Industries (NYSE:TEVA), the world’s largest generic drugs maker, has in the last six months gone up +56% amid sharp volatility, including a 30% drop between August and October 2022 during the broader market’s recent low (S&5 500 reached the 3500-3600 points range in October).

TEVA has become a volatile stock (Seeking Alpha)

Volatility is an expression of risk and the higher it is the more the risk. These risks can be specific to the company or part of common risks facing the industry or broader financial markets. In the case of TEVA, I view the risks to be largely company-specific and for this reason will look at its corporate narrative in this analysis.

A messy deal

TEVA is an Israel based pharma giant with a well established presence in the US and other international markets. The bulk of its business is generic drugs manufacturing and marketing, though it produces a few proprietary brands. TEVA’s journey over the past decade has had three distinct phases that any potential long-term investor needs to be familiar with.

Firstly, there’s the (in retrospect) good phase before the 2015 move to buy the generics drugs business of Allergan in a $40.5 billion cash and stock deal.

Secondly, there’s the turbulent period following the deal. The acquisition didn’t lead to the expected financial results and instead resulted in regulatory action by the Federal Trade Commission (FTC), which in 2016 forced TEVA to divest the rights and assets to 79 generic products to “preserve competition” in the US pharma markets. This at the time represented the largest divestiture order in a US pharmaceutical merger case and inadvertently undermined the strategic aim of the deal which was to ramp up volumes in TEVA’s generics drugs business.

These factors contributed to the stock’s implosion from above $50 a share to below $20 a share. As if to rub salt in the wound, Allergan started aggressively unwinding its position in TEVA at a loss in 2018, adding selling pressure to the stock which has never recovered to former glories. Allergan was itself acquired by AbbVie (ABBV) in a $60 billion deal in 2020.

TEVA’s acquisition of Allergan’s generic drugs business had no strategic value, derailed the company’s focus, and degraded the balance sheet. This messy deal set the stage for the third and current phase in TEVA’s story. This chapter started in the second half of 2017 following a management shakeup that led to the appointment of current CEO Kare Schulz.

Schulz, who is expected to retire in November, launched a turnaround plan that involved aggressively cutting costs and focusing on “ensuring that we protect our revenues.” However, in the five years that the plan has been actively implemented, TEVA’s revenues have been falling. Margins have also not improved materially despite a 30% reduction in headcount from around 51,000 in 2017 to approx. 35,000 currently, and a halving in R&D expenses from $1.7 billion in 2017 to $872 million in the trailing twelve months.

Slowing growth

The generics drugs business involves the sale of cheap generic versions of formerly exclusive drugs whose patents have expired. It is a high-volume- low-margin business since generic drugs are like commodities.

Scale is therefore one of the most important competitive advantages in the generic drugs business. This explains why TEVA made a play for Allergan’s generic drugs business back in 2015. However, the FTC mandated divestiture of a section of its US generic portfolio in 2016, followed by the aggressive cost cutting in 2017 to date, has resulted in TEVA having less scale today than it did a decade ago. This dims future profitability prospects given a generic drugs business that needs scale to pull in strong earnings.

Moreover, the higher margin section of TEVA’s business, which is developing its own limited line of proprietary drugs, has come under pressure since the patent for Copaxone, its blockbuster multiple sclerosis drug, expired in 2015, thus opening the way for the market to be flooded with cheap generics.

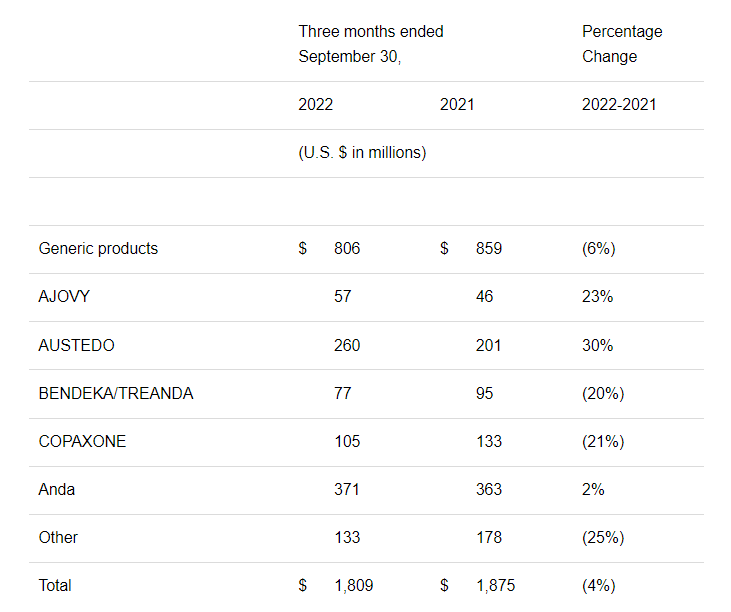

TEVA has in recent years launched two new proprietary brands that were supposed to counter the decline in Copaxone. These are Ajovy, its migraine drug, and Austedo for Huntington’s disease treatment. The key highlights so far is that Austedo reported 30% U.S. revenue growth in Q3 22 and is on track to reach ~$1 billion 2022 annual revenues. Ajovy grew 23% in Q322 but is still much smaller than Austedo as per the below table.

Teva Q3 earnings press release

TEVA missed revenue and earnings estimates in Q3 22 and has since 2020 beaten analysts’ quarterly revenue estimates in only three quarters. This is an indicator that TEVA’s growth is falling behind expectations, which is not good for the stock.

Meanwhile, the company’s balance sheet has meaningfully deteriorated. Its long-term debt for the trailing twelve months is $18.49 billion, a reduction from $26.7 billion in 2017 when it commenced its turnaround. The paying down of debt while positive in itself has only made a bad situation “less bad” which is not satisfactory in my view. Moreover, net interest expenses have increased from $791 million in 2017 to $873 million for the trailing twelve months, meaning the cost of capital has increased despite reducing long-term debt by more than $7 billion. This has happened amid slowing revenues.

Speculative short-term play

TEVA is as far as I’m concerned a speculative short-term play, despite the underlying business being a solid company with an established brand. Going by past management projections and actual performance, it appears stuck in a deepening cycle of hope and disappointment from which it is unlikely to break free from in 2023. Because of this, the 56% run in the last six months is a sell signal in my book and I think the risk is more tilted to the downside.

TEVA’s valuation looks historically low as it has an EV/EBITDA of 6.92x vs a 5-year average of 8.16x. While it is cheaper today relative to the past, this does not represent a bargain as investors are discounting factors like slower growth, no dividends, fewer competitive advantages given its declining scale in a low margin industry, lower R&D spend, and the balance sheet and high interest expenses.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment